Wood Fillers Market By Type (Solvent-Based Wood Fillers, Water-Based Wood Fillers, and Epoxy-Based Wood Fillers), By Application (Flooring, Windows, Doors, Furniture, Cabinetry, and Others), By Sales Channel (B2B and B2C), Industry Analysis, Size, Share, Growth, Trends, and Forecast, 2024-2031

Report ID

MSI-2619

Published

February 17, 2026

Pages

257 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

MARKET OVERVIEW

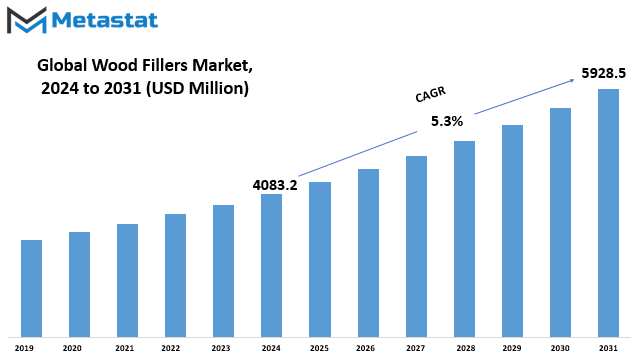

The Global Wood Fillers market is estimated to reach $5928.5 Million by 2031; growing at a CAGR of 5.3% from 2024 to 2031.

The Global Wood Fillers market stands as a dynamic force within the woodworking industry, embodying the essence of innovation and utility. This market, rooted in craftsmanship and construction, plays a pivotal role in shaping the landscape of wood-based applications across various sectors. As an integral component of the woodworking industry, wood fillers serve as versatile substances, seamlessly merging functionality with aesthetics.

Within the sphere of the Global Wood Fillers market, the industry gravitates around the creation and utilization of wood fillers—a class of materials engineered to enhance the structural integrity and visual appeal of wood products. This market’s significance extends beyond mere product enhancement; it acts as a silent enabler, allowing artisans and manufacturers to overcome challenges associated with wood imperfections.

Wood fillers, unlike static elements, adapt to the unique characteristics of different wood types and facilitate a seamless blend between natural beauty and practicality. The Global Wood Fillers market, in essence, thrives on its ability to cater to a spectrum of woodworking needs, offering solutions that range from minor repairs to substantial structural improvements.

Navigating the intricacies of this market unveils a tapestry woven with innovation and craftsmanship. Artisans and manufacturers leverage wood fillers not only for rectifying knots, cracks, and voids but also for sculpting intricate designs that push the boundaries of conventional woodworking. The industry’s vibrant ecosystem is a testament to the relentless pursuit of excellence within the woodworking community.

Woodworkers, architects, and designers find themselves intertwined with the Global Wood Fillers market, seamlessly integrating these solutions into their creative processes. This symbiotic relationship extends beyond the mere transactional exchange of products; it encapsulates a shared commitment to elevating the standard of woodworking, pushing the boundaries of what can be achieved with wood as a medium.

In construction and interior design space, the Global Wood Fillers market takes center stage, addressing the practical challenges associated with utilizing wood in diverse environments. These fillers become indispensable companions in the hands of builders and designers, ensuring that every project attains a level of durability and aesthetic appeal that stands the test of time.

The Global Wood Fillers market emerges as a cornerstone within the woodworking industry, offering a diverse array of solutions that go beyond mere surface-level enhancements. Its impact resonates in the hands of craftsmen and industry professionals who leverage these fillers to sculpt, repair, and refine wood products, contributing to a world where the beauty and utility of wood coalesce seamlessly.

GROWTH FACTORS

The Global Wood Fillers market is influenced by various factors that drive its growth, hinder its progress, and present opportunities for expansion. In this essay, we will delve into the drivers, restraints, and opportunities shaping the landscape of the wood fillers industry.

Wood fillers play a crucial role in catering to the rising demand for wood furniture and interior woodwork. The increasing inclination towards wooden aesthetics in furniture and interior design has propelled the demand for repair and finishing products, including wood fillers. This surge is primarily driven by consumers seeking solutions to enhance the longevity and appearance of their wooden assets. As individuals continue to embrace the timeless appeal of wood, the demand for wood fillers is set to witness a sustained increase.

Another key driver influencing the Global Wood Fillers market is the continuous advancements in wood filler technologies. These innovations focus on delivering superior adhesion and durability, addressing the evolving needs of consumers. With ongoing research and development efforts, manufacturers are introducing wood fillers that not only repair but also enhance the structural integrity of wood surfaces. This technological progress not only caters to the current demand for effective solutions but also anticipates and adapts to future requirements.

However, the market faces certain restraints that impede its seamless growth. One notable hindrance is the availability of alternative materials such as metal and plastic. These substitutes offer comparable functionality and, in some cases, surpass wood fillers in terms of durability and versatility. Consequently, industries that traditionally relied on wood may shift towards these alternatives, reducing the overall demand for wood fillers.

Environmental concerns add another layer of restraint to the Global Wood Fillers market. Some wood fillers contain chemical components that raise apprehensions about their ecological impact. As environmental awareness grows, consumers and industries alike are becoming more mindful of the materials they use. This heightened awareness could lead to a shift towards eco-friendly alternatives or the development of wood fillers with reduced environmental impact.

On the brighter side, there exists an opportunity within the wood fillers market that aligns with the growing trend towards do-it-yourself (DIY) home improvement projects. The surge in interest and participation in DIY activities creates a conducive environment for the retail wood filler market. Consumers, empowered by the accessibility of information and materials, are increasingly inclined to take on home improvement projects themselves. This trend presents an opportunity for the wood filler market to cater to the needs of DIY enthusiasts, providing them with reliable and user-friendly products.

The Global Wood Fillers market is shaped by dynamic forces, balancing the demand for wood-related products, technological advancements, challenges posed by alternative materials, environmental considerations, and the growing DIY trend. As the industry navigates these factors, it is poised to adapt and thrive in a market driven by consumer preferences and evolving trends.

MARKET SEGMENTATION

By Type

In the vast landscape of the Global Wood Fillers market, the classification by type brings clarity to the diverse products available. This segmentation reveals three main categories: Solvent-Based Wood Fillers, Water-Based Wood Fillers, and Epoxy-Based Wood Filler.

Solvent-Based Wood Fillers represent one facet of this market. These fillers, as the name suggests, contain solvents as a key component. They are known for their quick drying time, making them a practical choice for those seeking efficiency in wood repairs. This type of wood filler finds its utility in various applications, from minor touch-ups to more substantial renovations.

On the other hand, Water-Based Wood Fillers present a different avenue for wood repair enthusiasts. Unlike their solvent-based counterparts, these fillers use water as the primary solvent. This characteristic makes them more environmentally friendly and less harsh in terms of fumes. Their ease of use and cleanup add to the appeal, making them a preferred choice for those who prioritize a more user-friendly approach to wood restoration.

Epoxy-Based Wood Filler introduces a unique formulation to the market. Epoxy, a versatile polymer known for its robustness, is a key ingredient in this type of wood filler. This variant stands out for its durability and strength, often chosen for demanding applications where resilience is paramount. Epoxy-Based Wood Fillers are adept at handling challenges that go beyond the scope of routine repairs, providing a reliable solution for more strenuous tasks.

The market's segmentation into these distinct types caters to the diverse needs of consumers. Solvent-Based Wood Fillers offer swift solutions, Water-Based Wood Fillers prioritize environmental considerations, and Epoxy-Based Wood Fillers excel in durability. Each type addresses specific concerns, allowing consumers to make informed choices based on their unique requirements.

As we delve deeper into the dynamics of the Global Wood Fillers market, it becomes evident that consumer preferences play a pivotal role in shaping the demand for these products. The appeal of Solvent-Based, Water-Based, or Epoxy-Based Wood Fillers is not universal, and understanding the nuances of each type empowers consumers to make decisions aligned with their priorities.

The Global Wood Fillers market, segmented by type, offers a comprehensive range of solutions for wood repair and restoration. From the swift efficiency of Solvent-Based Wood Fillers to the environmentally conscious approach of Water-Based alternatives and the robust resilience of Epoxy-Based options, the market caters to diverse needs. This segmentation enhances consumer choice, ensuring that individuals can find the right wood filler to meet their specific requirements.

By Application

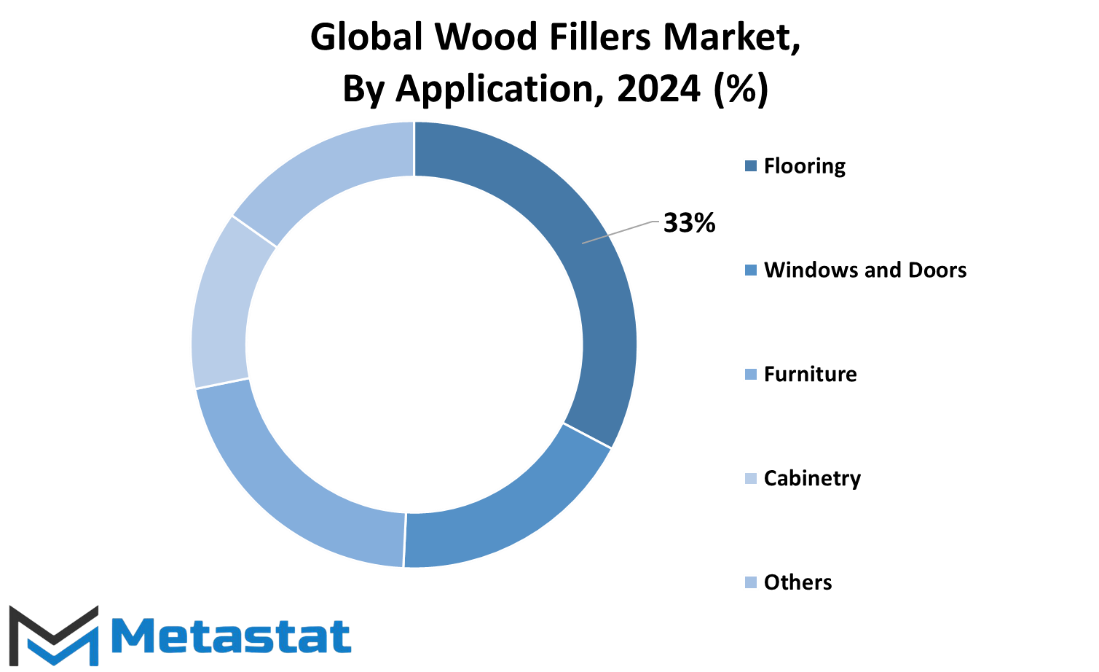

The Global Wood Fillers market finds its application in various sectors, branching into Flooring, Windows and Doors, Furniture, Cabinetry, and Other areas. These applications underscore the versatile utility of wood fillers in diverse contexts.

Wood fillers play a crucial role in the flooring industry, seamlessly addressing imperfections in wooden floors. Whether it’s covering gaps, holes, or uneven surfaces, these fillers contribute to the aesthetic appeal and longevity of wooden flooring. In the realm of windows and doors, wood fillers step in to mend damages, ensuring a seamless and well-maintained appearance. Their ability to blend seamlessly with the natural wood color makes them a preferred choice in maintaining the visual integrity of these essential components of a structure.

Furniture manufacturing benefits significantly from the use of wood fillers. They prove invaluable in repairing nicks, scratches, or other blemishes on wooden furniture, thereby enhancing the overall quality and appearance. The adaptability of wood fillers in cabinetry is noteworthy, as they effectively address any imperfections, contributing to the durability and visual appeal of wooden cabinets. This application aligns with the growing demand for aesthetically pleasing and well-maintained interior spaces.

Beyond these specific applications, wood fillers find utility in various other areas, collectively referred to as “Others.” This broad category encompasses diverse applications, reflecting the versatility of wood fillers in catering to different needs across industries. Whether it’s minor repairs, surface enhancements, or ensuring a consistent finish, wood fillers prove to be an asset in the ever-expanding spectrum of applications.

The market dynamics of Global Wood Fillers reflect the increasing reliance on these products across industries. Manufacturers and consumers alike recognize the practical benefits of wood fillers in addressing issues related to wood surfaces. The demand for these products is not confined to a particular sector, but rather extends across multiple domains, showcasing their widespread relevance.

The Global Wood Fillers market’s segmentation by application into Flooring, Windows and Doors, Furniture, Cabinetry, and Others highlights the diverse roles these fillers play in enhancing and maintaining wooden surfaces. Their seamless integration, ease of use, and effectiveness in addressing imperfections contribute to their growing popularity across various industries. As the market continues to evolve, the significance of wood fillers in ensuring the longevity and visual appeal of wood-based products remains a consistent and noteworthy aspect of their contribution to different sectors.

By Sales Channel

The Global Wood Fillers market is segmented based on its Sales Channel, which is further categorized into Business-to-Business (B2B) and Business-to-Consumer (B2C). This division highlights the varied approaches employed in distributing wood fillers to different target audiences.

In the wood fillers market, the Sales Channel plays a crucial role in determining how these products reach end-users. The B2B sector focuses on transactions between businesses, where wood fillers are often acquired in bulk for various purposes. This could include construction projects, manufacturing, or other commercial applications. B2B transactions involve negotiations and collaborations between different businesses, emphasizing the importance of professional relationships.

On the other hand, the B2C segment revolves around transactions directly between businesses and individual consumers. In this channel, wood fillers are packaged and marketed for personal use by homeowners, DIY enthusiasts, or small-scale projects. The B2C approach targets a broader consumer base, often emphasizing user-friendly packaging, product accessibility, and ease of use.

Understanding the dynamics of these sales channels is essential for both manufacturers and consumers. For businesses operating in the wood fillers market, a strategic focus on B2B interactions involves building strong relationships with other businesses, ensuring a steady and reliable supply chain, and adapting to the specific needs of commercial clients. This might involve custom formulations, bulk packaging, or tailored delivery options.

Conversely, companies engaging in B2C transactions must navigate the intricacies of individual consumer preferences. Packaging, labeling, and product information become crucial in capturing the attention of the end-user. Consumer-friendly attributes such as easy application, environmentally friendly formulations, and clear instructions on usage can significantly influence purchasing decisions in the B2C wood fillers market.

The dichotomy between B2B and B2C channels underscores the versatility of wood fillers as products that cater to diverse needs. This market’s segmentation recognizes the varied demands of both large-scale commercial projects and smaller, individual endeavors.

The Global Wood Fillers market’s Sales Channel segmentation into B2B and B2C provides a comprehensive perspective on the diverse ways these products are distributed and consumed. Whether facilitating large-scale construction projects or meeting the needs of individual consumers engaged in home improvement, the market’s segmentation aligns with the distinct requirements of its stakeholders. The B2B and B2C channels stand as integral components in the ever-evolving landscape of the wood fillers market, reflecting its adaptability to different scopes and scales of application.

REGIONAL ANALYSIS

The global Wood Fillers market is geographically categorized into North America, Europe, Asia-Pacific, and other regions. This division allows for a comprehensive analysis of market trends and dynamics across different parts of the world.

In North America, the Wood Fillers market exhibits a steady growth pattern. The demand for wood fillers in this region is primarily driven by the construction sector, where these materials find extensive use in various applications. The consistent expansion of the construction industry, coupled with the need for durable and aesthetically pleasing wood products, contributes to the sustained demand for wood fillers.

Moving on to Europe, a similar trend is observed in the Wood Fillers market. The construction and woodworking industries play pivotal roles in driving market growth. The European market witnesses a robust demand for wood fillers as they prove essential in addressing imperfections in wooden structures and enhancing their overall quality. The awareness of sustainable building practices further fuels the adoption of wood fillers in construction projects across the continent.

In the Asia-Pacific region, the Wood Fillers market experiences dynamic growth, fueled by the rapid urbanization and infrastructure development in countries like China and India. The construction boom in these nations creates a substantial demand for wood fillers, as they are instrumental in improving the durability and appearance of wooden structures. Also, the cultural significance of wood in architecture and design contributes to its popularity in the region.

Other regions also play a role in shaping the global Wood Fillers market landscape. These areas, though diverse in their economic and industrial profiles, collectively contribute to the overall market dynamics. The use of wood fillers in small-scale construction projects, furniture manufacturing, and DIY applications ensures a widespread and versatile market presence.

One of the key drivers of the global Wood Fillers market is the increasing awareness of environmental sustainability. Consumers and industries alike are leaning towards eco-friendly building materials, and wood fillers align with this preference. The market sees a surge in demand for wood fillers formulated from renewable resources, contributing to the overall sustainability goals of the construction and woodworking sectors.

Moreover, technological advancements have played a role in enhancing the quality and performance of wood fillers. Innovations in manufacturing processes have led to the development of high-performance wood fillers that offer improved durability and ease of application. This, in turn, boosts their acceptance in various end-use industries.

The global Wood Fillers market demonstrates a diverse and dynamic landscape across different regions. From the steady growth in North America to the robust demand in Europe and the dynamic expansion in Asia-Pacific, the market's trajectory is shaped by various factors, including construction activities, cultural preferences, and the growing emphasis on sustainability. The ongoing advancements in technology further contribute to the evolution of the Wood Fillers market, making it a pivotal player in the construction and woodworking industries worldwide.

COMPETITIVE PLAYERS

In the expansive arena of the Global Wood Fillers market, several notable players shape the landscape, contributing to the dynamics of the industry. Among these key participants are 3M Company, Liberon Limited, and Woodwise (Design Hardwood Products).

3M Company stands as a prominent player in the Wood Fillers sector, bringing a wealth of experience and innovation to the table. With a focus on quality and performance, 3M has solidified its position as a reliable contributor to the industry, catering to diverse consumer needs.

Liberon Limited is another significant player, recognized for its commitment to delivering effective wood fillers. The company's dedication to craftsmanship and product excellence has earned it a place of trust among consumers, contributing to its noteworthy presence in the market.

Woodwise (Design Hardwood Products) adds its unique touch to the competitive landscape. Known for design-centric hardwood products, Woodwise brings creativity and functionality to the forefront. In the realm of wood fillers, the company's offerings contribute to the aesthetic and practical aspects, enhancing its competitive standing.

These competitive players not only navigate the challenges of the Wood Fillers market but also drive innovation and quality assurance. Their contributions extend beyond mere market presence, influencing trends and setting benchmarks for others to follow.

Understanding the significance of these key players is crucial for stakeholders and consumers alike. 3M Company, Liberon Limited, and Woodwise (Design Hardwood Products) collectively play a pivotal role in shaping the market's trajectory. Their products not only address practical needs but also reflect evolving consumer preferences.

In the competitive landscape, the distinctive strengths of each player come to the forefront. 3M Company's commitment to innovation, Liberon Limited's emphasis on craftsmanship, and Woodwise's fusion of design and functionality create a dynamic ecosystem within the Wood Fillers industry. Consumers benefit from this diversity, finding products that align with their specific requirements and preferences.

As market dynamics continue to evolve, these key players remain agile, adapting to changing consumer demands and industry trends. This adaptability ensures their sustained relevance and influence in the competitive Wood Fillers market. The synergy of these players contributes to a vibrant marketplace where quality, innovation, and consumer satisfaction converge.

The Global Wood Fillers market is significantly influenced by key players such as 3M Company, Liberon Limited, and Woodwise (Design Hardwood Products). Their distinct contributions, ranging from innovation to craftsmanship and design-centric approaches, collectively shape the industry's landscape. Understanding the roles and strengths of these players provides valuable insights into the evolving dynamics of the Wood Fillers market, benefiting both stakeholders and consumers alike.

Stage Hoist market size is valued at USD 236.3 million in 2025 and is projected to reach USD 395.3 million in 2033, at a CAGR of 6.3% from 2026 to 2033.

Global Taper Lock Bushing market is valued at USD 1,187.8 million in 2025 and is projected to reach USD 1,808.0 million in 2033, at a CAGR of 5.4% from 2026 to 2033

Europe Mini Excavators Market Size, Share, Trends, 2033

Europe Mini Excavators market size is valued at USD 2,162.9 million in 2025 and is projected to reach USD 3,004.1 million in 2033, at a CAGR of 4.2% from 2026 to 2033

Europe Mini Excavators Market, Europe Mini Excavators Market Size, Europe Mini Excavators Market Share, Europe Mini Excavators Market Analysis, Europe Mini Excavators Market Growth, Europe Mini Excavators Market Trends, Europe Mini Excavators Market Research Report, Europe Mini Excavators Market Forecast, Europe Mini Excavators, Europe Mini Excavators Market Research, Europe Mini Excavators Industry, Europe Mini Excavators Industry Report, Europe Mini Excavators Market Data, Europe Mini Excavators Statistics, Europe Mini Excavators Market Statistics, Europe Mini Excavators Industry Trends, Europe Mini Excavators Market Report, Europe Mini Excavators Market Trends, Europe Mini Excavators Market News, Europe Mini Excavators Forecasts, Europe Mini Excavators Market Intelligence Report

Global Switch Actuators market size is valued at USD 18.4 billion in 2025 and is projected to reach USD 30.6 billion in 2033, at a CAGR of 6.6% from 2026 to 2033