MARKET OVERVIEW

The Global Underfloor Heating Manifold Market is a specialized sector of the heating and plumbing industry. It deals specifically with systems that allow efficient distribution of water or energy within underfloor heating setups. These manifolds, therefore, play central roles in regulating and controlling the flow of heated water across multiple zones within a building, thus evenly distributing heat and using energy resources optimally. As modern construction trends shift toward sustainable and energy-efficient solutions, the role of underfloor heating manifolds has gained prominence in both residential and commercial spaces.

This market is technical and precise. The primary purpose of an underfloor heating manifold is to regulate the flow rates and temperatures of water in different heating circuits. Advanced control mechanisms, such as thermostats and sensors, are also used in these systems to maintain consistent thermal performance. Manifolds are being designed to integrate with smart homes, allowing users to remotely control heating preferences, increasing user convenience and energy savings.

Manufacturers within the Global Underfloor Heating Manifold Market have strived to innovate and improve their products. Material inputs in the manufacturing process, including brass, stainless steel, and polymers, have been optimized for durability, thermal conductivity, and corrosion resistance. This has made new applications for the manifold more viable, especially in severe climatic regions, which demand stronger and more reliable heating systems.

The demand for underfloor heating manifolds is closely related to the growth in underfloor heating systems themselves. These are increasingly recognized both for their environmental and economic advantages. They distribute heat better than traditional radiators do, making them an attractive alternative for modern building designs focused on comfort and energy efficiency. Further, integration of manifolds with renewable energy sources, like solar thermal systems or heat pumps, will further redefine their relevance in sustainable construction practices.

Geographically, the Global Underfloor Heating Manifold Market encompasses different regions with their own requirements and regulatory frameworks. In colder climates, the focus will be on maximizing heating efficiency, whereas in regions with milder winters, cost-effectiveness and system compatibility may take precedence. Manufacturers will have to contend with these regional differences while keeping pace with evolving building codes and environmental standards that will determine the future of the market.

As the construction industry adopts increasingly stringent energy efficiency mandates, the Global Underfloor Heating Manifold Market is expected to witness significant advancements in design and technology. Features such as flow meters, pressure gauges, and automated controls will likely become standard components, enhancing system efficiency and usability. Moreover, as the Internet of Things continues to shape up building technologies, manifolds in connected ecosystems have the potential to unlock innovative possibilities in remote monitoring and predictive maintenance.

The Global Underfloor Heating Manifold Market is an extremely important driver in the push for the development of new energy-efficient heating technologies. This market, supporting the very backbone of modern underfloor heating systems, supports the green building practice and follows end-user preferences in search of comfort and cost. When innovation accelerates, when new markets emerge, industry will adapt and prosper by following the global demands for smarter and more efficient heating solutions.

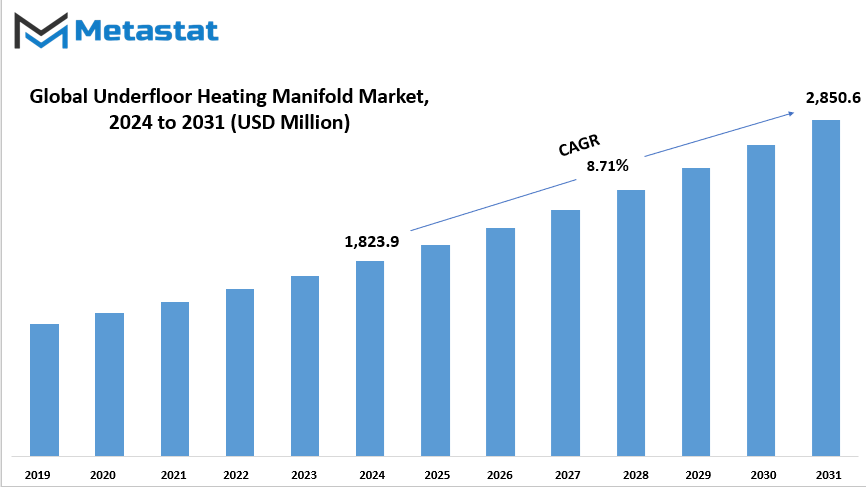

Global Underfloor Heating Manifold market is estimated to reach $2,850.6 Million by 2031; growing at a CAGR of 8.71% from 2024 to 2031.

GROWTH FACTORS

The global energy-efficient heating systems market has been experiencing a growing trend, with increased use in residential and commercial buildings. This trend reflects an increasing preference for systems that not only reduce energy consumption but also provide enhanced comfort. One of the driving factors behind this market is the increasing demand for underfloor heating, especially in modern construction. Underfloor heating has been favored because it provides a more comfortable feel since heat is distributed uniformly, thereby increasing the aesthetics of any dwelling and workspace by getting rid of radiators and heaters that would otherwise have to be on full display.

However, despite all the positive aspects, some limitations may come in to curtail the market. Some of the major disadvantages include a relatively high installation cost, which may limit the uptake by potential users. Compared to traditional heating systems, energy-efficient options, including underfloor heating, often involve more complex installation processes and require a significant upfront investment. Additionally, the limited options for retrofitting these systems in older buildings pose another challenge. Many older structures were not designed to accommodate modern heating systems, making upgrades more complicated and expensive, which in turn restricts broader market penetration.

However, advancements in technology are creating promising opportunities. One of the innovations is a smart manifold that comes integrated with controls. Such a system optimizes energy consumption through efficient distribution of heat in accordance with specific requirements. Moreover, remote-operating capabilities are an attractive feature, where users can access their heating controls remotely with the help of smart devices. These innovations are likely to play a crucial role in making energy-efficient heating systems more accessible and attractive to a wider population.

In the coming years, these technological advancements along with growing awareness about energy conservation and sustainability are expected to fuel further growth in the market. Although initial costs and retrofitting challenges may continue to act as barriers, the long-term energy savings and the comfort that these systems will provide will likely outweigh the drawbacks for many users. The future of the market looks bright, especially with new solutions being developed to address the existing limitations and make these systems more adaptable to different types of buildings.

MARKET SEGMENTATION

By Type

The design for manifolds is different, hence catering to the varieties that can serve in respective functions for particular applications. The major kinds are Single Circuit Manifolds, Multiple Circuit Manifolds, Hydraulic Manifolds, Electronic Manifolds, and Compact Manifolds, in which every kind serves to a different extent regarding system complexity and demands of systems.

Single Circuit Manifolds are used for managing one flow path where the fluid or gas flows in one direction. They are used in less complex systems where one function has to be controlled or managed at a time. Such manifolds are easy to maintain and economical for simple applications.

The multiple circuit manifolds can accommodate several flow paths at one time. It is the best for those systems requiring various functions to be controlled or activated at one time. This component is typically used in industrial applications that require accuracy and efficiency. Multiple Circuit Manifolds provide for improved control and distribution of fluids, hence, they are very versatile for several applications.

Hydraulic Manifolds are used in machines like construction machinery, industrial equipment, and automotive systems, where the hydraulic system is a significant portion of their functioning. Such manifolds are engineered to operate at high pressures and provide consistent fluid delivery in hydraulic circuits.

Electronic manifolds are intended for applications in which the flow of fluids or gas is controlled through electronic control; the sensors and actuators control them electronically. The electronic manifolds are primarily used in highly modernized automated systems requiring precise fluid flow control monitoring. For this purpose, integration of electronics will yield greater flexibility, efficiency, and accuracy and therefore it is ideally suited for the high-tech industries.

Compact Manifolds are shorter in length, so these are more suitable for application where space is limited. They are small in size, but reliable flow control is provided, and they are designed to fit into systems where saving inches of space is a necessity without sacrificing performance. They are used in smaller machines and systems where every inch of space counts. Each of these manifold types will serve specific needs depending on the system's design and the level of control required.

By Material

The market is segmented based upon the materials used in manifolds, which include brass, stainless steel, plastic, and more. Brass manifolds are widely selected for toughness and resistance to corrosion due to their long-lasting application in various plumbing and heating systems. Brass has innate strength and is longlasting, making it a desirable choice in many industrial applications and residential applications.

Stainless steel manifolds, however provide much more resistance to corrosion and wear, especially for conditions where the manifolds are exposed to temperatures that are very high and challenging. Stainless steel products have a reputation for solidity; hence, they receive very high regard in applications such as gas and water systems and even food-processing applications, where hygiene as well as long-term durability must be assured.

Other alternatives by the market are plastic manifolds, which are characterized more by their lightness and even affordability. They find usage where conditions of high temperature and pressures are not that serious or significant. Plastic manifolds are easier to put in place and often end up costing less than one made from brass or steel, making them more the choice for more budget-strained projects or systems under significant weight factors.

Other materials are used in making manifolds, though not as frequently as brass, stainless steel, and plastic. These can be chosen for specific applications or to fulfill certain requirements, such as resistance to specific chemicals or extreme temperatures. Manufacturers are constantly innovating and coming up with new materials that can cater to the needs of different industries, and these "other materials" can be made for specialized use cases.

Each of these material options, with its specific advantages and challenges, depends on what kind of demand the system or project would require. For instance, brass against stainless steel or plastic depends more on factors such as cost, environment, and requirement. As the industries will keep growing and changing in every way, these will also continue to play important roles in the design and construction of manifold systems across the world.

By Application

The market can further be divided based on the application of the market in residential buildings, commercial buildings, industrial buildings, and public infrastructure. Each one of these sectors plays an important role in determining the total demand and supply of the market.

Residential buildings are one of the most prominent segments, as they satisfy the needs of people in search of homes. It ranges from single-family houses to multi-unit apartment buildings. The growing demand for housing, fueled by population growth and urbanization, remains a driving force behind the growth of the residential building sector.

Commercial buildings are focused on spaces used for business activities. The buildings are meant for offices, retail shops, hotels, and other business-related purposes. As businesses expand and grow, the need for more commercial spaces increases. It makes this a very important sector of the market. Usually, demand for commercial buildings follows the economic health because businesses need a physical space to operate and interact with customers.

Industrial buildings are the next in the list. The structures of such buildings are the factory and warehouses that deal with producing and distributing commodities. Given the trend in globalization of trade and increasing demand in supply chains, industrialization is one area that has shown much growth. Efficient production and storing facilities will, in the near future, call for many industrial buildings.

Public infrastructure includes roads, bridges, airports, hospitals, schools, or any other public facility as part of the necessary provisions for society to function normally. This category is often capitalized upon during periods of growth in the economy or when governments choose to focus on improving standard of living and meeting societal wants.

These categories are all important to the growth and development of the market. As urbanization and population growth continue, it is likely that demand will increase for residential, commercial, industrial, and public infrastructure buildings. Understanding these categories allows for better planning and development of resources for future needs.

By End-User

The Underfloor Heating Manifold market, which is global in scope, can be categorized into three major segments according to the end-user. These categories are the residential sector, the commercial sector, and the industrial sector. Since each of these sectors possesses different requirements and demands as far as underfloor heating systems are concerned, they make up unique application and growth areas in the market.

Underfloor heating is in common use in the residential sector for heating up houses and living areas more comfortably, efficiently, and quietly. Private houses, apartments, and other residential buildings form part of this sector, where underfloor heating finds appreciation in the equalization of heat distribution in the rooms. The trend of energy-saving homes and the increasing awareness to live sustainably have supported the increased popularity of underfloor heating in residential houses.

Underfloor heating systems have been used in offices and retail stores, among other businesses. In commercial spaces, underfloor heating is preferred because it is able to provide consistent warmth without bulky radiators or heating units that occupy so much space. This is particularly important in settings where aesthetics and space utilization are factors. In addition, underfloor heating in commercial properties can help improve energy efficiency, which is a major draw for businesses looking to save on heating costs.

Underfloor heating is also utilized by the industrial sector, although it usually applies to specific niches. Underfloor heating is useful in huge industrial complexes, warehouses, and factories where optimal working temperatures in the production area are essential. It also finds great applications in this sector by being an energy-efficient heating system that ensures uniform heating. Moreover, underfloor heating helps to ensure comfort for workers and smooth operations, especially in large rooms where traditional heating systems will not be as effective.

Overall, the market for underfloor heating manifolds is growing across these three sectors, with each sector’s unique requirements driving demand for tailored heating solutions. As technology improves and the focus on energy efficiency increases, it is likely that the adoption of underfloor heating will continue to rise across these different sectors.

|

Report Coverage

|

Details

|

|

Forecast Period

|

2024-2031

|

|

Market Size in 2024

|

$1,823.9 million

|

|

Market Size by 2031

|

$2,850.6 Million

|

|

Growth Rate from 2024 to 2031

|

8.71%

|

|

Base Year

|

2022

|

|

Regions Covered

|

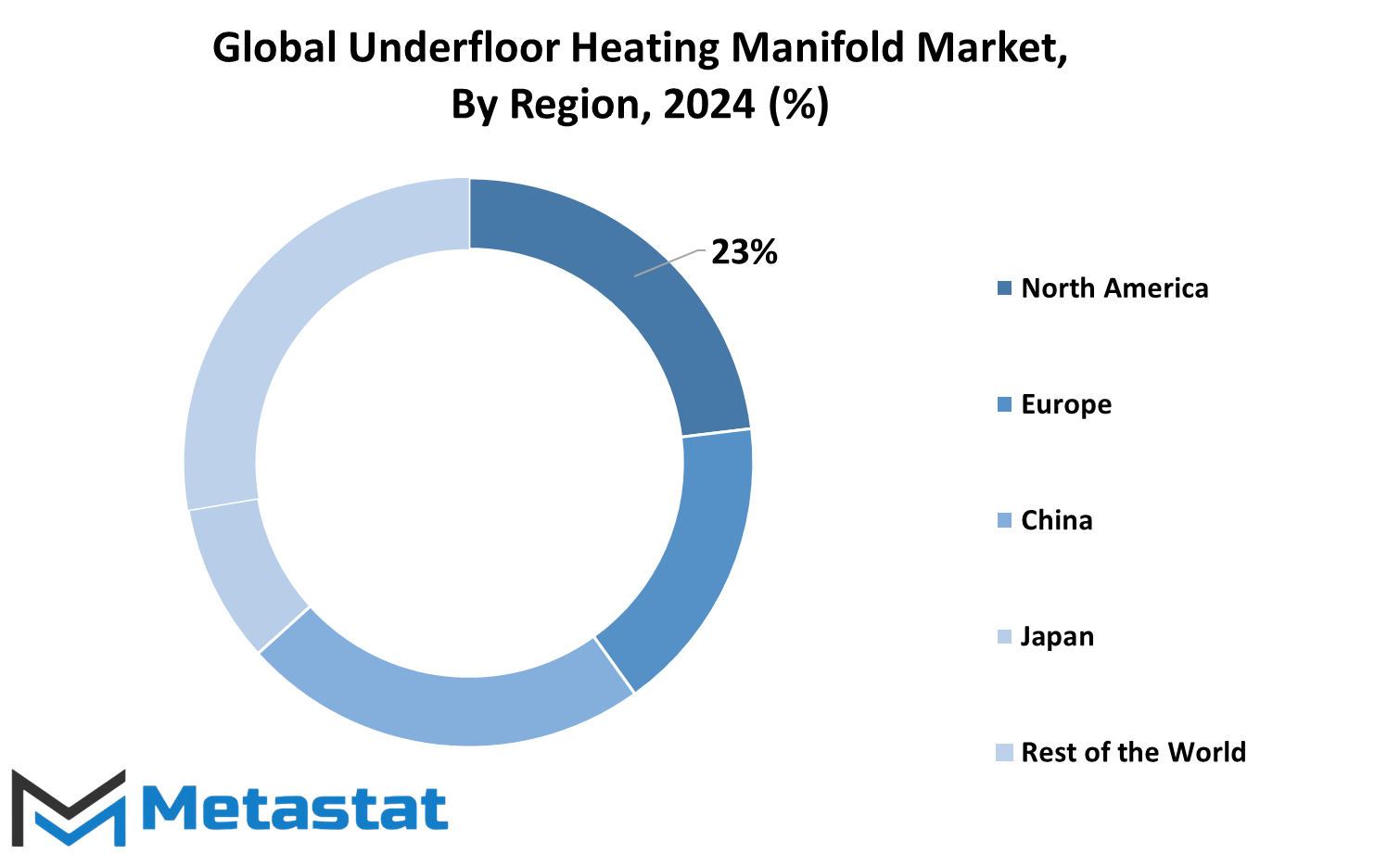

North America, Europe, Asia-Pacific Green, South America, Middle East & Africa

|

REGIONAL ANALYSIS

The Underfloor Heating Manifold market in respect to geography is divided globally. The regions are further split into North America, Europe, Asia-Pacific, South America, and Middle East & Africa. Here in North America, again further broken down into the U.S., Canada, and Mexico, whereas Europe is the countries which are split with regard to the UK, Germany, France, Italy, and the rest of the nations. Asia-Pacific is divided into major countries such as India, China, Japan, South Korea, and other rest of Asia-Pacific. The last region is South America with Brazil, Argentina, and other countries in the remaining part of the region. Finally, the Middle East & Africa is divided into GCC countries, Egypt, South Africa, and other regions in the Middle East & Africa. This geographic distribution in the market provides an avenue for better understanding the way and manner in which the underfloor heating manifold industry is spread in the world. It further enables determining the major players and growth in each of the above regions, therefore making it easy to target individual markets and satisfy regional demands. The knowledge of these distributions is essential to companies and stakeholders who wish to venture in new opportunities, invest in the specific markets, or broaden their businesses into new locations.

COMPETITIVE PLAYERS

The Underfloor Heating Manifold industry is dominated by several key players, each contributing to the growth and innovation of this sector. Among these companies, Uponor Corporation, Rehau Group, and Danfoss A/S are recognized for their advanced product offerings and global presence. These companies are known for their expertise in manufacturing high-quality underfloor heating systems that are widely used in both residential and commercial applications. Other notable companies are Watts Water Technologies, Heatmiser, and Oventrop GmbH & Co. KG, all specialized in producing efficient and reliable heating systems.

Apart from these, Honeywell International Inc. is also famous for its range of smart home products that comprise underfloor heating controls which improve energy efficiency and user comfort. Henco Industries and Emmeti S.p.A. are other big names in the industry offering innovative solutions for underfloor heating systems, and Polypipe focuses on providing sustainable heating products that are easy to install and maintain.

With their technologically advanced products suited for demand in the residential and industrial sectors, Giacomini S.p.A. certainly did its share of making mark; another significant name in this business is Inrusstrade.ru heating solutions for various regions of demand; Zehnder Group, Viega GmbH & Co. KG and Wavin Limited complete the roster of the top players; each with its own virtues which include energy-efficient systems and smart control technologies or robustly-designed products.

These companies play a quintessential role in the further development of underfloor heating systems by providing a range of solutions that ensure comfort and high energy efficiency in homes and offices. As consumer demand for more environment-friendly and effective heating solution continues to grow, there is an expectation that the influence of these industry leaders should increase, driving further innovative and improvement in underfloor heating technology. The contributions of such companies will keep on framing the industry and will certainly help in fulfilling the changing demands of consumers all over the globe.

Underfloor Heating Manifold Market Key Segments:

By Type

- Single Circuit Manifolds

- Multiple Circuit Manifolds

- Hydraulic Manifolds

- Electronic Manifolds

- Compact Manifolds

By Material

- Brass Manifolds

- Stainless Steel Manifolds

- Plastic Manifolds

- Other Materials

By Application

- Residential Buildings

- Commercial Buildings

- Industrial Buildings

- Public Infrastructure

By End-User

- Residential Sector

- Commercial Sector

- Industrial Sector

Key Global Underfloor Heating Manifold Industry Players

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential