MARKET OVERVIEW

The global plastic pellets market and industry will remain at the core of the flow of raw polymer feedstocks across various manufacturing industries. These small, bead-shaped units, manufactured through polymerization and compounding processes, will serve as the building blocks for millions of plastic commodities. Years ahead, they will continue to be the best form in which resin is shipped, warehoused, and converted, given their consistency, ease of use, and compatibility with automated systems. From films used to package products to car parts, the market will support a broad spectrum of production processes as the interconnecting layer between producers of chemicals and end-user industries.

At its essence, the business will be about converting base chemicals into solid, shipping-friendly pellets that can be melted and molded into consistent products. Production will go on to formulate pellets to highly specialized performance specifications whether that involves making lightweight yet durable materials for aerospace use, or formulating plastics with very high heat resistance for electronics applications. It will be accomplished through additives, fillers, and blending methods that will develop as a function of technological progress.

The global plastic pellets market supply chain will extend from petrochemical complexes, polymer processing plants, logistics companies, to manufacturers on multiple continents. Manufacturers will place investments in upgrading pellet quality, reducing impurities, and enhancing pellet size consistency to optimize downstream processing effectiveness. The sector, in turn, will see changes in the sourcing approach, with regional production clusters looking to lower reliance on solitary geographic suppliers. This re-balancing will be influenced by trade policies, transportation costs, and developments in polymer chemistry.

End-use markets will increasingly require pellets with high performance and sustainability credentials. The next stage of market evolution will come with heightened penetration of recycled or bio-based pellets due to regulatory need and customer willingness to accept environmentally friendly materials. Whereas virgin resin pellets will continue to rule in high-performance applications, recycled pellets will gain increasing market share with improvements in processing technology and diminishing quality gaps.

In the future, the competitive dynamics of the industry will depend on the capability of manufacturers to respond to rapidly evolving material requirements. The emphasis will not merely be on bulk production of standard grades but also on the manufacture of specialty pellets for specialty uses, including medical equipment or sophisticated composite materials. Firms that can combine sophisticated quality control systems, predictive maintenance on production lines, and accurate material characterization will establish new standards for efficiency and reliability.

The global plastic pellets market will also be determined by how rapidly it can respond to disruptions be they supply shortages, energy price swings, or regulatory system shifts. Companies that prepare for such disruptions and have versatile production capacities will be able to stay stable. The path of the market in the coming years will be shaped by its capacity to reconcile the mass production of products with innovation, servicing both world demand and the niche requirements of industries that rely on high-quality pelletized polymers.

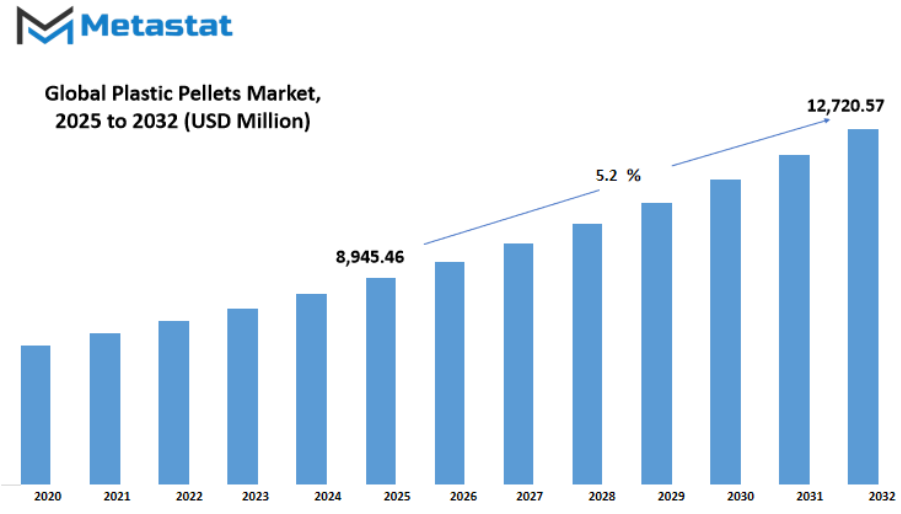

Global plastic pellets market is estimated to reach $12,720.57 Million by 2032; growing at a CAGR of 5.2% from 2025 to 2032.

GROWTH FACTORS

The global plastic pellets market is expected to see notable changes in the coming years, shaped by both rising demand and shifting production approaches. These pellets, widely used in packaging, automotive, and consumer goods industries, are a fundamental material in manufacturing a wide range of products. As consumer needs grow and industries look for efficient, durable, and cost-effective materials, the demand for these pellets will likely continue to increase. Packaging remains a major driver, with its broad applications in food storage, product safety, and transportation. Similarly, the automotive industry’s interest in lightweight yet strong materials, and the consumer goods sector’s push for variety and durability, are adding to the rising use of plastic pellets worldwide.

Another strong factor contributing to this growth is the increasing focus on recycling. Governments, companies, and consumers are becoming more aware of the environmental impact of plastic waste. This has encouraged the development and use of recycled pellets, which help reduce waste while supporting manufacturing needs. Recycling initiatives are now more advanced, enabling the production of high-quality pellets that can be reused in different applications without compromising on performance. This trend is expected to expand further as technologies improve and recycling becomes more efficient and cost-effective.

Despite these positive developments, certain challenges may slow the pace of market growth. Environmental regulations in various regions are placing limits on plastic production and waste generation. While these rules are aimed at reducing pollution and encouraging sustainable alternatives, they may restrict supply and affect production rates. Another concern is the volatility in raw material prices, which can cause unpredictable changes in manufacturing costs. This instability can make it difficult for producers to maintain consistent pricing, potentially affecting demand.

Looking ahead, advancements in biodegradable and bio-based plastic pellets could transform the market. These innovations are designed to offer the same strength and flexibility as traditional plastics, while being more environmentally friendly. As research and investment in this area continue, such materials may become a significant part of the market, meeting the needs of both industry and sustainability goals. Businesses that adopt these alternatives early could gain a competitive advantage, especially as global demand for eco-conscious products grows.

Overall, the future of the global plastic pellets market will be shaped by a mix of industrial demand, environmental responsibility, and technological progress. The balance between meeting production needs and addressing sustainability challenges will determine how the market develops over the next decade.

MARKET SEGMENTATION

By Type

The global plastic pellets market will continue to play a significant role in shaping industries and manufacturing processes in the future. Plastic pellets are the basic form in which many plastic products begin their life. They are small, uniform pieces that are easy to transport, store, and process into finished goods. With growing demand for packaging, automotive parts, construction materials, and consumer goods, the market will expand steadily. As industries adopt more efficient production methods, the use of plastic pellets will remain central to delivering consistent quality and performance across applications.

By type, the global plastic pellets market is further segmented into LDPE, PET, HDPE, PE, PVC, PP, and others. LDPE, known for its flexibility and resistance to moisture, will continue to be widely used in films, bags, and other packaging materials. PET, valued for its strength and clarity, will maintain strong demand in beverage bottles and food containers. HDPE, with its high strength-to-density ratio, will serve applications like piping, containers, and durable goods. PE in general will remain a versatile material with broad uses in packaging and household products. PVC, recognized for its durability and resistance to environmental stress, will keep its position in construction materials, pipes, and profiles. PP, which offers a balance of toughness and heat resistance, will find demand in automotive, textiles, and storage solutions. The “others” category includes specialty plastics that will serve niche applications and innovative product designs.

Future growth will not only be driven by industrial demand but also by changes in consumer expectations and environmental considerations. As the call for more sustainable practices grows, manufacturers will explore bio-based or recycled plastic pellets. Advanced recycling technologies will make it easier to turn used plastics back into high-quality pellets, reducing waste and reliance on virgin materials. This will create new opportunities for companies that invest in green technologies and responsible sourcing.

Automation and digital monitoring in pellet production will also improve efficiency and consistency. Factories of the future will use real-time data to adjust production parameters, ensuring better quality control and less material waste. Additionally, global trade in pellets will be influenced by shifting regulations, environmental policies, and raw material availability.

Overall, the global plastic pellets market will remain a key part of manufacturing, adapting to technological advancements and the push for sustainability. With ongoing research and investment, the industry will evolve to meet the demands of a growing population while balancing performance, cost, and environmental responsibility. This combination of practicality and innovation will ensure its relevance for many years ahead.

By Application

The global plastic pellets market is expected to grow steadily in the coming years as industries continue to demand versatile and reliable raw materials. Plastic pellets are small granules that are melted and molded into different shapes, making them essential for a wide range of applications. By application, the market is divided into automotive, construction, electronics, machinery, packaging, and others. Each of these sectors will play a significant role in shaping the future demand and direction of this market.

In the automotive industry, plastic pellets will be used increasingly to create lighter and stronger parts. As manufacturers aim to improve fuel efficiency and develop electric vehicles, the use of lightweight plastic components will continue to rise. This trend will not only help in reducing emissions but also open opportunities for more innovative designs that can withstand higher performance demands.

The construction sector will also remain a major consumer. Plastic pellets are used to produce pipes, fittings, insulation materials, and other building components. With urban development expected to grow in many countries, the demand for durable and weather-resistant materials will expand. Builders and engineers will turn to plastics for solutions that are easier to transport, install, and maintain, which will help construction projects become faster and more cost-efficient.

In electronics, plastic pellets will be vital for producing casings, connectors, and insulation parts. As devices become smaller, smarter, and more integrated into daily life, manufacturers will rely on plastics that can offer high durability while keeping production costs reasonable. The rise of wearable devices, smart home products, and advanced communication systems will create a steady stream of demand for these materials.

For the machinery sector, plastic pellets will support the creation of components that are resistant to wear, corrosion, and heat. Industries that operate heavy equipment will need materials that can handle intense working conditions without frequent replacement. This will encourage continued innovation in pellet formulations that improve strength and performance.

Packaging will remain one of the largest segments. With e-commerce continuing to grow and consumer goods needing protection during transport, the use of plastics for packaging will stay high. However, more attention will be given to producing recyclable and biodegradable options to address environmental concerns while still benefiting from the versatility of plastic pellets.

Other applications, including household goods, medical devices, and agricultural tools, will also add to the market’s expansion. As technology advances and industries seek efficiency, the global plastic pellets market will adapt to meet these new needs, ensuring it stays relevant in a fast-changing world.

|

Forecast Period |

2025-2032 |

|

Market Size in 2025 |

$8,945.46 million |

|

Market Size by 2032 |

$12,720.57 Million |

|

Growth Rate from 2025 to 2032 |

5.2% |

|

Base Year |

2024 |

|

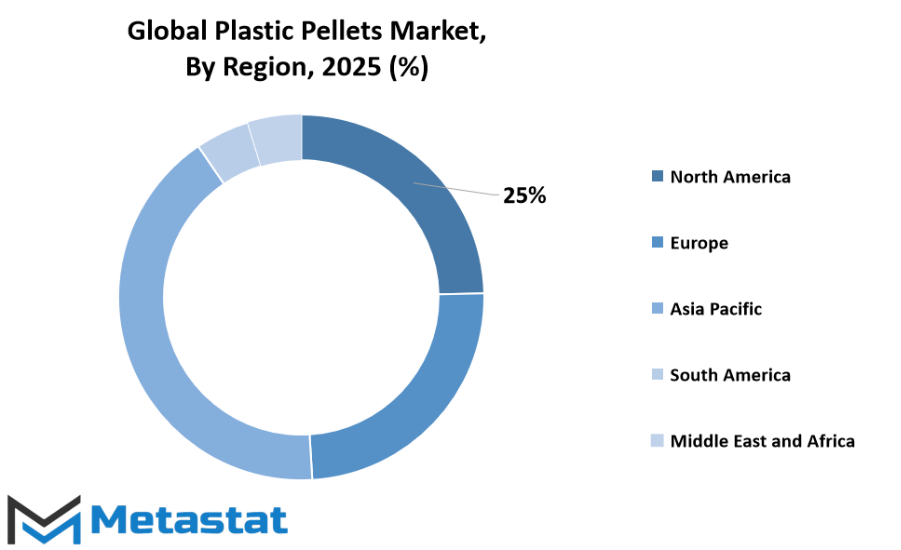

Regions Covered |

North America, Europe, Asia-Pacific Green, South America, Middle East & Africa |

REGIONAL ANALYSIS

The global plastic pellets market shows significant regional variations, reflecting differences in industrial capacity, raw material availability, and demand patterns across the world. In North America, which includes the U.S., Canada, and Mexico, advanced manufacturing infrastructure and strong demand from industries such as packaging, automotive, and consumer goods continue to drive growth. The U.S. remains a leading producer due to its established petrochemical sector and investment in sustainable pellet production methods. Canada benefits from its abundant natural resources, while Mexico’s growing industrial base and trade links strengthen its role in regional supply chains.

Europe, including the UK, Germany, France, Italy, and the Rest of Europe, places a strong emphasis on environmentally responsible manufacturing. Stringent regulations on plastic usage and waste management push producers to innovate and adopt recycled or biodegradable pellet options. Germany and Italy maintain their leadership through precision manufacturing and high-quality exports, while the UK and France show steady demand fueled by packaging and consumer product manufacturing.

Asia-Pacific, which covers India, China, Japan, South Korea, and the Rest of Asia-Pacific, is projected to hold a dominant position in the future. China leads global production with large-scale facilities and extensive export networks, while India’s expanding manufacturing sector and infrastructure projects boost its consumption levels. Japan and South Korea focus on high-tech applications, such as electronics and advanced automotive components, using pellets tailored for specialized needs. This region’s rapid industrialization, population growth, and increasing urbanization will ensure it remains a key driver of global demand.

In South America, with Brazil, Argentina, and the Rest of South America, market growth is supported by rising industrial activities and improving manufacturing capacities. Brazil’s strong petrochemical industry and Argentina’s focus on agricultural packaging materials contribute to regional expansion. Investments in production facilities are expected to increase as demand for both conventional and eco-friendly pellets rises.

The Middle East & Africa, including GCC Countries, Egypt, South Africa, and the Rest of the Middle East & Africa, benefits from abundant petrochemical resources. GCC Countries remain important suppliers due to their low-cost raw material availability and large-scale production plants. South Africa’s growing automotive and construction sectors drive domestic consumption, while Egypt plays a strategic role in connecting regional trade routes.

Looking forward, each region’s growth in the global plastic pellets market will be shaped by technological improvements, sustainability efforts, and trade partnerships. With ongoing investment and innovation, regional markets are likely to evolve toward producing higher-quality, more sustainable pellet options to meet global demand.

COMPETITIVE PLAYERS

The global plastic pellets market is expected to experience notable changes in the coming years as industries, governments, and consumers adapt to new economic and environmental conditions. Plastic pellets, small granules used as the base material for producing a wide variety of plastic products, remain a vital part of modern manufacturing. With the rising demand for efficient and versatile raw materials, the competition among producers is expected to intensify. Leading companies in this sector, such as The Dow Chemical Company, DuPont de Nemours, Inc., Exxon Mobil Corporation, Chevron Phillips Chemical Company LLC, LG Chem Ltd., Formosa Plastics Corporation, Borealis AG, Braskem S.A., Sinopec Group, and Lanxess AG, are positioning themselves to maintain an edge through innovation, strategic investments, and expansion into emerging markets.

In the future, these players will likely increase their focus on advanced production technologies that can improve efficiency while reducing environmental impact. As global regulations around waste and emissions grow stricter, companies in the global plastic pellets market will be under greater pressure to introduce sustainable solutions. This will encourage investments in bio-based and recyclable pellet production, allowing manufacturers to appeal to both environmentally conscious consumers and industries seeking long-term compliance with changing standards.

Competition will also be shaped by the expansion of production capacities and the establishment of facilities closer to key markets. By reducing transportation costs and ensuring a steady supply, companies can respond quickly to changing customer needs. Furthermore, advancements in polymer science will open opportunities for developing specialized pellets with enhanced properties, catering to sectors like automotive, construction, healthcare, and packaging.

The global plastic pellets market will also be influenced by fluctuations in crude oil prices, as petroleum remains a primary feedstock for many pellet types. This will drive some companies to explore alternative raw materials to secure supply stability. Collaboration between industry leaders and research institutions is expected to increase, leading to new formulations that improve performance while minimizing environmental harm.

Digital technologies, such as AI-based quality control and automated logistics, will likely become more integrated into production and distribution systems. These developments will help major companies operate with greater precision, efficiency, and flexibility, further shaping the competitive landscape.

In the years ahead, success in the global plastic pellets market will depend on a company’s ability to balance cost, quality, sustainability, and adaptability. The leading players already have strong global footprints, but the next phase of competition will be determined by how effectively they anticipate change and deliver innovative solutions that meet the demands of a fast-moving world.

Plastic Pellets Market Key Segments:

By Type

- LDPE

- PET

- HDPE

- PE

- PVC

- PP

- Others

By Application

- Automotive

- Construction

- Electronics

- Machinery

- Packaging

- Others

Key Global Plastic Pellets Industry Players

- The Dow Chemical Company

- DuPont de Nemours, Inc.

- Exxon Mobil Corporation

- Chevron Phillips Chemical Company LLC

- LG Chem Ltd.

- Formosa Plastics Corporation

- Borealis AG

- Braskem S.A.

- Sinopec Group

- Lanxess AG

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential

US: +1 3023308252

US: +1 3023308252