MARKET OVERVIEW

The Global Physical Vapor Deposition Market should be guided by equipment design, material targets, and process deposition. Sputtering and evaporation, with some arc deposition in close pursuit, will be pivotal in innovations. With a move toward tampering with automation and digital monitoring of the processing, PVD systems will continue to be operated further, even in an environment of adaptive control, along the mentioned features, which might eventually see a further shrinking or alteration in their actual designs. Hence, such systems ought to survive at any level of complexity in component geometry and substrate diversity, so that the function requirement from the surface finish under thermal constraint remains precisely satisfied.

Playing in the league of advanced materials with new materials, application areas, and methods, the Physical Vapor Deposition global market answers the requirement for the deposition of thin films and coatings by vacuum. Manufacturing processes are placing emphasis on precision sliced many times as accuracy has become the business of manufacturing. With this in mind, the demand for consistent performance coating processes will significantly affect the evolving nature of this market. Physical Vapor Deposition techniques or PVD results are lowered as they classically represent material deposition onto various substrates, thereby promoting enhanced tendency toward tougher texture and consequently anti-corrosion qualities and high weight retention where finesse and durability are the prime necessities.

To produce these coatings, companies use a number of technologies, equipment, and materials applicable to coatings in industries such as microelectronics, medical devices, energy, and automotive. The Cracow's Physical Vapor Deposition market is endlessly dynamic as new technology brings the sun for disruptions and pitfalls. The market will evolve to lure producers who are interested in methods to improve tool life without tampering with the essential properties of substrates. If made with high-pulsed power, PVD will allow coatings to be deposited atom by atom, often inside the great depths of vacuum chambers, generating very uniform and aggressive films. Such milestones will continue to be the favorite playground for precision and function.

The physical vapor deposition business will be obliged to meet the minimum standard of growth and failure demands in industries requiring transparent coatings with virtually no defects. Adhesive quality is an issue in regard to semiconductor fabrication. The physical vapor deposition market shall produce tools and materials that allow for sub-micron features and good electrical and mechanical properties. This mandates the imperative to develop equipment and control systems that can deal with clean environments and rougher state environments at a lower level of material purity levels. In addition to saturation technologies of film, systems that can solve problems related to contamination, thorough vacuum operational facilities, interface contamination, and reliable film properties are critical.

Sustainable development and energy efficiency could largely turn the tide to innovation for the future physical vapor deposition market; PVD is one of the more sustainable methods as it is much cleaner than some of the chemical-based court using techniques out there. Further developments will enhance material usage and energy consumption.

By influencing innovation in the Global Physical Vapor Deposition market, research laboratories will be linked with industrial producers. PVD equipment and materials will be challenged by experimental thin films for next-generation optical devices, data storage technologies, or biomedical tools to be fabricated on a smaller scale and into more complex structures. This market will therefore be innovated from the technical requirements coming from applications that stress surface integrity and long-term performance.

The Global Physical Vapor Deposition market will heavily connect with segments that require materials innovation at the surface level. With manufacturing trends now emphasizing precision, repeatability, and performance under extreme conditions, unattended PVD will remain the technology of choice for companies investing in durability and efficiency across production environments.

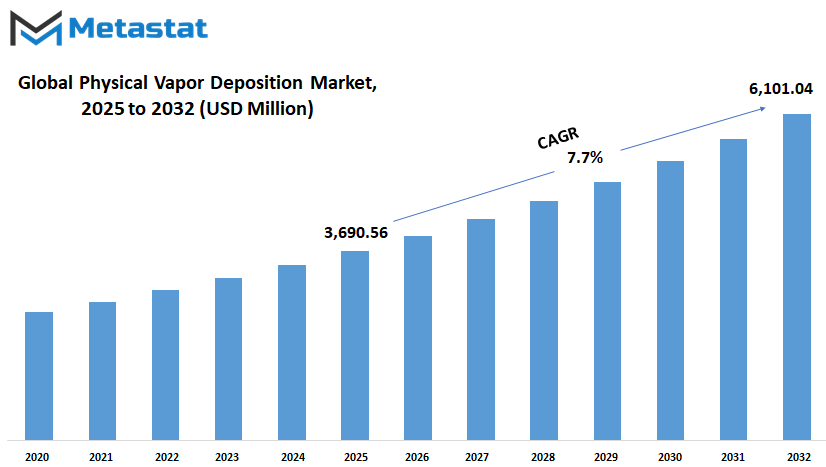

Global Physical Vapor Deposition market is estimated to reach $6,101.04 Million by 2032; growing at a CAGR of 7.7% from 2025 to 2032.

GROWTH FACTORS

The Global Physical Vapor Deposition market is likely to grow steadily in the coming years due to various factors that shall induce its growth. Innovations stimulate industries to demand more efficient, reliable, and high-performance coating solutions. Physical Vapor Deposition, widely adopted for thin films and coatings, met demands across different industries: electronics, aerospace, automotive, and healthcare. Such growing demand for surface treatments improvement will boost demand for these methods. Manufacturing industries are striving to improve product durability, functionality, and aesthetics as Physical Vapor Deposition would help achieve them without the harm of high-embedded processes.

As new devices and tools become smaller and more complex, the importance of precise coatings increases. This market is also boosted by increasing investments in research and development, as businesses strive to create advanced coatings from their performance perspective. Manufacturers are switching from the established methodologies for coatings to cleaner alternatives in the meantime in awareness for less environmental impact. The market is expected to gain from this.

However, the Global Physical Vapor Deposition market is not bereft of challenges. The cost of the equipment along with the complex setup required for installation and operation may slow down such adoption, especially concerning smaller businesses. Also, the dependency on trained professionals for the operation and maintenance of systems might prove a critical bottleneck in the way, since not all companies can avail of such technical expertise. These barriers might affect market expansion rates, then.

However, there are some promising opportunities expected in the future despite these challenges. As more industries move toward automation and digital manufacturing, the demand for high-quality coatings will increase. The rise of electric vehicles, smart devices, and renewable energy systems may spur new demand for sophisticated coating solutions. Materials science and nanotechnology innovations could also lead to new avenues that will enhance the efficiency and applicability of Physical Vapor Deposition methods.

The Global Physical Vapor Deposition market, in other words, is expected to reap the benefits from its push for cleaner technology, reliable products that could be used in making longer-lasting materials. Negative impacts and obstacles will definitely slow the speed, but the overall trend is positive. The future holds a lot as continuous innovation and rising demand across multiple sectors indicate that this market is likely to remain a key component of the manufacturing landscape in the future.

MARKET SEGMENTATION

By Category

There are innovations and precision in future requirements of advanced surface coating technologies, which are needed to develop PVD. This market is expected to grow consistently as industries need reliable ways of improving their products' performance and longevity. The main reason for this lies in the fact that it serves a range of categories that have specific industrial needs.

PVD Equipment is made up of the machines and tools used in the process of deposition. As production methods improve, the equipment will also become much more refined, energy efficient, and simple to operate. Industries dependent on fine coatings like electronics and automotive manufacturing will find benefit from the machines that allow more precise control over the process. These machines will allow companies to expand their scale without compromising quality, driving a steady market demand.

PVD Materials are additionally a significant portion of this market. These are the materials used during the coating process in the formation of thin films on the surface of various products. Manufacturers will increasingly pursue greener and more efficient ways of converting goods; hence, their capabilities would adapt with those of PVD materials. Future developments will increasingly lead to the adoption of new materials with superior wear resistance, long life, and stronger bonding abilities. These factors make them ideal for applications in affecting industries such as aerospace, medical tooling, and precision instruments.

There are also PVD Services covering application and customization-in fact, exclusive providers of coatings that are applied or even customized. Not all companies operate their own equipment, so many general ones still turn to outside sources for PVD expertise. This segment is only expected to become more relevant in that direction as companies try to lower their initial costs but still avail themselves of the use of top-coated options. Given that markets abound with extreme temperatures for fast turnarounds and very specific qualities in coating properties, demand will increase for tailored needs.

Clearly, tomorrow's Global Physical Vapor Deposition market is about supporting industries that require durable and advanced coatings in the progressive search for producing methods that are more efficient. Appropriately, this market is shaped by and the drive of needs such as reduced environmental practices and more willingness for reliable surface appendages. With an ever-growing need for quality and sustainability in the two aspects, equipment, materials, and services would continue to grow steadily, tuning to the changing demands of industries.

By Application

The Global Physical Vapor Deposition market is likely to follow a consistent trend of growth in the years to come as industries shift to advanced coating technologies to enhance performance and durability. Applications and uses of this method for producing very thin films or coatings are becoming numerous, each with its specific drivers of demand. From data storage to medical equipment, all continue to be influenced by increasingly demanding requirements for efficient, reliable, and durable solutions.

The corresponding demand for compactness and faster storage continues to rise with data storage. Improve performance and stability of devices using coatings through Physical Vapor Deposition. The more businesses rely on data-driven systems, the more they need solutions for improved storage as the amount of digital content continues to increase; therefore, this segment will not run out of impetus to push forward. Every next generation storage product brings with it demands for better efficiencies, hence advanced coatings are becoming even more valuable for that endless cycle.

Microelectronics is an equally vibrant growth area for the Global Physical Vapor Deposition market. The increasing demand for miniaturization of electronic devices calls for coatings to support miniaturized components while maintaining quality and function. As these items keep getting smaller and smarter, the need for precision and reliability of coatings will continue to be critical. This is where Physical Vapor Deposition comes into play because it is a controlled and clean process that fosters innovation in electronic design.

The rest would create a larger market share for the solar product segment. There are then rising interests in improving the durability and performance of solar panels as the world moves from fossil fuels toward renewable energy. The enhancement of sunlight absorption and protective coatings afforded through Physical Vapor Deposition will prove beneficial. Investing and improving technology in this application section is expected to grow in the future with popularization and cost-effectiveness of solar energy.

Cutting tools benefit from these coatings' wear resistance. In industries where precision and strength such as the manufacturing industry and the automotive production industry, coated tools last longer and outperform their peers. The same can be said for medical equipment, where safety and hygiene are crucial. The smooth and clean surface generated by this process uphold sterile conditions and prolongs the instruments' life.

Numerous applications continue to find value in this technology, and demand will continue to swell as more and more sectors realize the benefits it offers. Technology advancement being what it is, the Global Physical Vapor Deposition market will also grow as many more industries find practical applications of the technology.

|

Forecast Period

|

2025-2032

|

|

Market Size in 2025

|

$3,690.56 million

|

|

Market Size by 2032

|

$6,101.04 Million

|

|

Growth Rate from 2025 to 2032

|

7.7%

|

|

Base Year

|

2024

|

|

Regions Covered

|

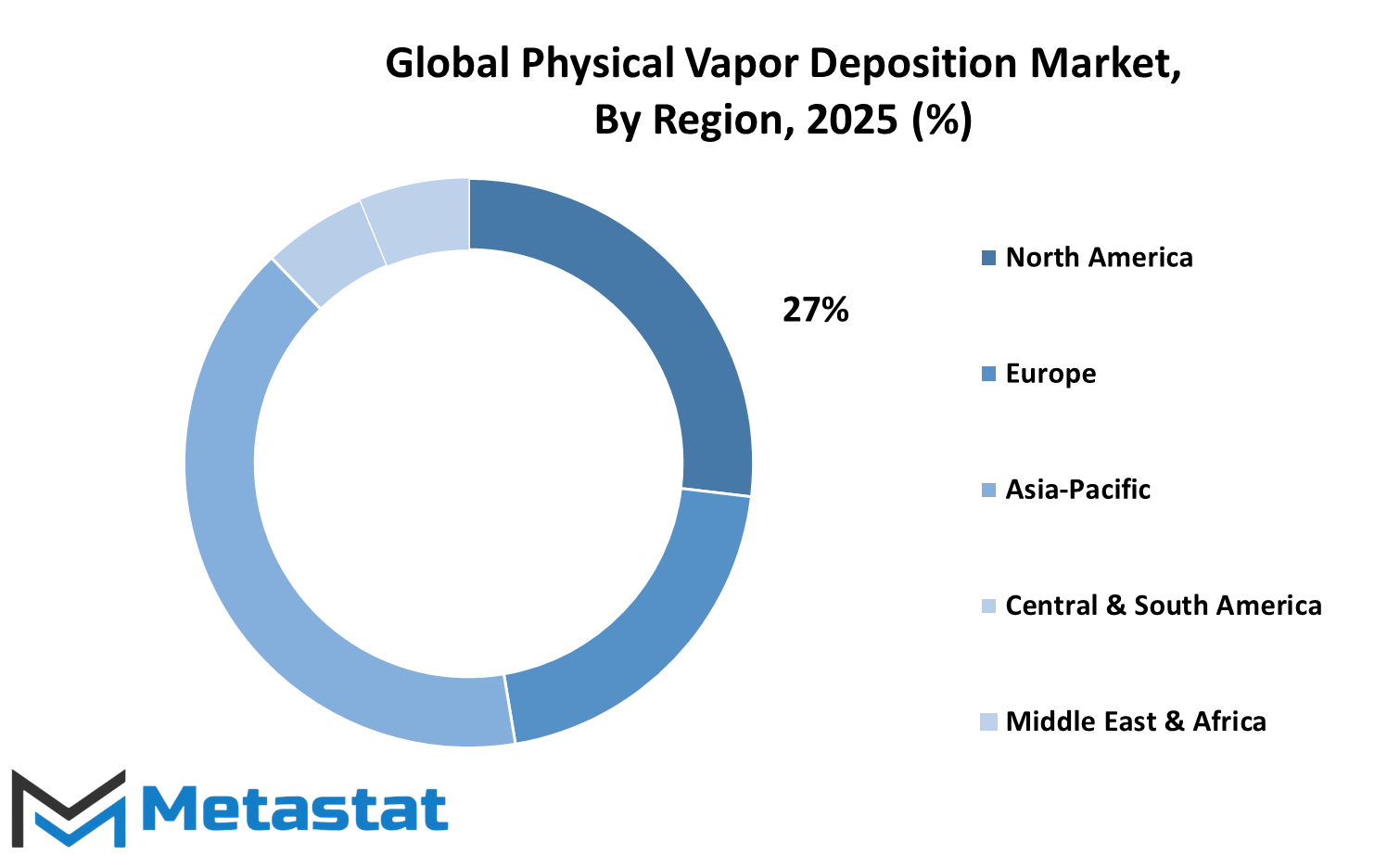

North America, Europe, Asia-Pacific, South America, Middle East & Africa

|

REGIONAL ANALYSIS

It is reported that the Global Physical Vapor Deposition market is poised to grow continuously different regions around the globe. Each of these regions has its own pace and direction to growth. The division of this market on a geographical basis helps in understanding patterns of demand and progress in a clearer way. North America, in this regard, stands out as one of the major contributors, with the United States, Canada, and Mexico at the stage now driving the action. The advanced technological base coupled with an increased investment in the industrial process strengthens a foothold in this space. North America will likely continue to be a major player in this market as more industries adopt newer tools and coating technologies.

In contrast, Europe has always combined a cocktail of new innovations and regulatory support for market growth. Industrial frameworks have already been established, with countries like Germany, the UK, France, and Italy that have been mainstream but are now gradually moving towards greener and cleaner alternative methods of production. This shift will allow greater use of PVD techniques. Such a market development will combine with significant future preparations of European industries focusing on sustainability. All these will keep driving the adoption of such methods, particularly in manufacturing and electronics, because of the push for compliance with the environment throughout Europe.

Asia-Pacific is fast shaping into one of the fastest growing regions. Leading countries like India, China, Japan, and South Korea taking this region into a whole new level of production and innovation. All this sums up to an increase in demands for electronics nowadays accompanied by expanding automotive industries and rapid urban developments that will contribute to this growth. By encouraging local production and industrial improvements, governments in the region have put these into part and parcel along with better standards in place for all this growth and capability. If the progress keeps going, Asia-Pacific may even set trends in the use of these technologies.

South America and the Middle East & Africa are a little behind in their pace but are not that far off. Countries that include Brazil and Argentina have witnessed a rise in interests that are aimed at improving their manufacturing setups. The possibilities of growth exist robustly with a better infrastructure coupled with stronger industrial policies. Likewise, countries in the Middle East and Africa, such as South Africa, Egypt, and the GCC countries, are beginning to see the possibilities that such technologies can offer. As time goes by, market presence will gradually develop in these areas and prepare itself for global expansion.

COMPETITIVE PLAYERS

The Global Physical Vapor Deposition (PVD) market has a bright future characterized by uninterrupted innovations. It originates from the strategic choices made by established players impacting the applicability of this technology across different industries. These companies are also anticipating erosion of obsolescence by collectively acting on all the cues like energy-efficient, high-precision manufacturing. In this market competition is not about the best equipment but about providing the right solutions for long-term value in the next industrial wave.

Applied Materials Inc., Veeco Instruments Inc., and Oerlikon Balzers seem to invest extensively in research to design tools and systems that comply with stricter environmental regulations and give them higher efficiency. Their focus has been on providing coatings that enhance the performance and life of drills, electronics, and medical devices. Their view toward innovation is that future demand will not only be speed- and cost- driven, but will also consider issues of reliability, environmental effect, and customizability. Therefore, when industries gravitate toward cleaner processes and more durable materials, the leaders of the Global Physical Vapor Deposition market are swaying towards innovative and flexible systems.

ULVAC Technologies Inc., IHI Hauzer Techno Coating B.V., and AJA International Inc. are upgrading production capabilities to meet the needs of expanded aerospace, automotive, and semiconductor industries. The latter sectors will still demand a higher level of performance and resistance to some advanced coating techniques against extreme environments. Besides increasing production capacity, these companies are also investing time improving customer service and technical support because they believe future growth hinges on partnership just as much as product quality.

Unlike many of their competitors, AgLnstrom Engineering Inc., Impact Coatings AB, and Semicore Equipment Inc. are introducing speed-to-market agility by designing easy-to-integrate, compact, and custom-designed systems, capable of being incorporated into a diverse array of manufacturing settings. As more companies consider bringing coating in-house, these players are giving solutions that make it possible without heavy overhead costs and infrastructure support. In the coming years, the Global Physical Vapor Deposition market will be mainly pulled in this direction of flexible systems that will give small and medium companies a fair chance of utilizing this technology.

Even more, with the long view, the participants in the said market do not compete against one another to shape the long-term agenda thereby sustaining long-term impacts. With advances in materials sciences and the rising demand for sustainable manufacturing, the Global Physical Vapor Deposition market will remain a space of discussion as the innovation mania and competition will just keep pushing the boundaries further.

Physical Vapor Deposition Market Key Segments:

By Category

- PVD Equipment

- PVD Materials

- PVD Services

By Application

- Data Storage

- Microelectronics

- Solar Products

- Cutting Tools

- Medical Equipment

- Others

Key Global Physical Vapor Deposition Industry Players

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential