MARKET OVERVIEW

The global vision testing devices market, which falls under the umbrella of the larger medical diagnostic equipment sector, will remain a work in progress as eye care grows more relevant across clinical and non-clinical environments. The industry comprises specialized devices designed to test and quantify visual acuity, peripheral vision, depth perception, and other visual function in many environments, ranging from hospitals and eye care facilities to mobile locations and optical retail settings. Instead of being confined to conventional eye charts and refractive instruments, this market will spread into more advanced technologies, such as portable electronic vision screeners, autorefractors, and high-performance retinal imaging systems.

In contrast to general medical devices that are used to treat a general variety of conditions, vision testing instruments will continue to be specifically designed for ophthalmologists, optometrists, and general practitioners who work with eye and neurological illnesses. The global vision testing devices market will expand over time-both in the sense of numbers sold and incorporation of artificial intelligence and automated analytics for diagnostic support. However, in its overall perspective, this market would not be defined by innovations or technology alone, but a reflection of regional disparities in eye care infrastructure, professional expertise, and the demographics of the population.

One of the key areas distinguishing this market from surrounding diagnostic categories is the crossover of clinical and lifestyle. Products in this category are not only employed for diagnosing disease conditions such as cataract or glaucoma but also will find application in school screenings, driver's license assessments, and occupational health programs. This double use will influence both the business and regulatory dynamics of the global vision testing devices market, rendering it distinct within the diagnostic paradigm.

What will distinguish future advancements is how these devices change to address issues like digital eye strain and growing screen time, both of which are impacting younger generations at an earlier age. Answers will not be limited to traditional testing rooms; mobile and app-based devices will become the norm, particularly in regions where access to eye care professionals is still limited. Even with increasing interest in such innovations, the market will need to overcome issues regarding accuracy, data protection, and clinical validation of newer test formats.

It's important to keep in mind that the global vision testing devices market will not extend to treatment solutions such as eyeglasses or contact lenses, nor will it touch on surgical devices applied in correction procedures. Its focus will remain on detecting and monitoring visual function and abnormalities. Therefore, any overlap with corrective devices or therapeutic platforms will be peripheral rather than central to this particular market's direction.

In the future, the global vision testing devices market will experience both opportunity and restraint via regulation updates, healthcare policy changes, and public awareness campaigns. Nevertheless, it will stay concentrated on providing solutions that enhance early detection and ongoing monitoring of eyesight. Although the market is not independent of overall medical technology trends, it will maintain its unique character as a preventive diagnostics-oriented market.

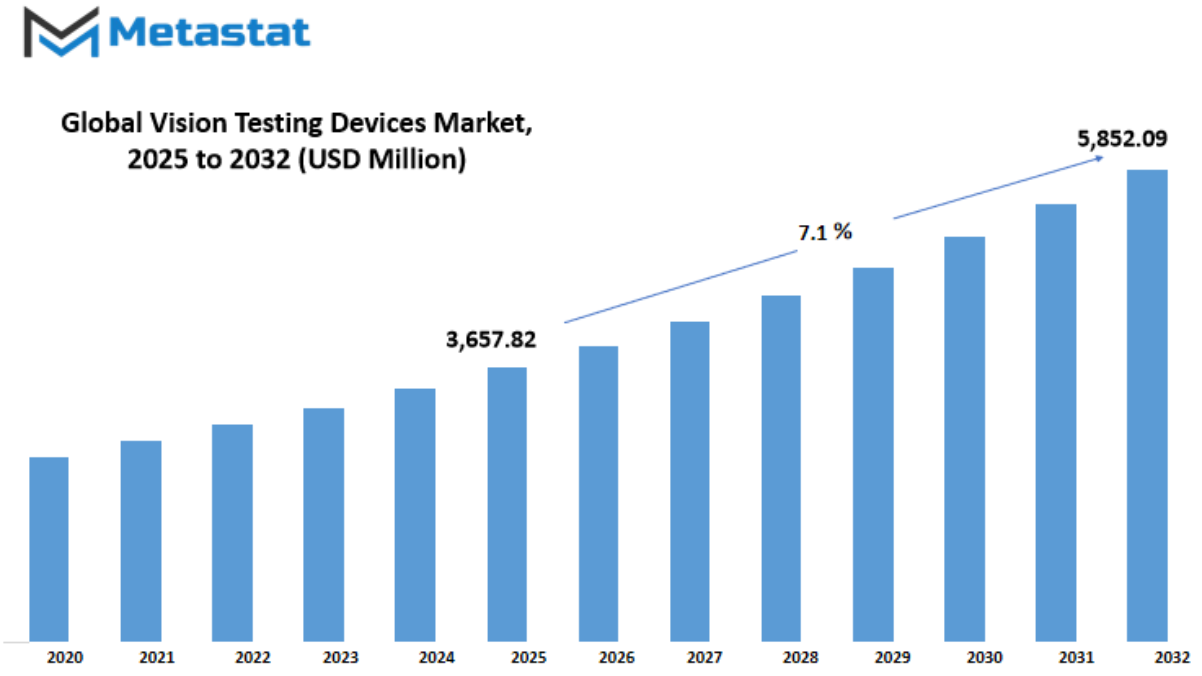

Global vision testing devices market is estimated to reach $5,852.09 Million by 2032; growing at a CAGR of 7.1% from 2025 to 2032.

GROWTH FACTORS

The global vision testing devices market is anticipated to grow steadily in the future because of growing concern about eyesight and the increased number of individuals suffering from vision ailments. As more individuals worldwide become accessible for medical care, periodic eye check-ups are becoming increasingly popular. This trend is most visible in the developing world where healthcare facilities are improving incrementally. Consequently, the demand for accurate and precise vision testing equipment is expected to increase. Technological innovations are also defining the future of this sector.

New equipment is becoming increasingly user-friendly, portable, and efficient at giving quick results. These developments are not only improving doctors' services but are also making it feasible for tests to occur outside traditional clinics. Devices that are equipped with features such as digital screens, remote data transfer, and compatibility with other health systems are likely to become popular. These advancements are contributing to the growth of the global vision testing devices market by availing vision care to individuals in both urban and rural settings. The rising population is one of the primary drivers of growth. As individuals age, they tend to develop vision disorders like cataracts, glaucoma, and age-related macular degeneration.

This is resulting in a consistent increase in the population that needs regular eye exams. Another reason is the growing use of digital devices by every age group. Prolonged use of digital media is leading to eye strain and other eye-related problems, even among children. This is fueling the demand for frequent eye tests and trustworthy testing equipment. Though, certain difficulties may hinder the market. The cost of sophisticated machines being too high and unavailability of trained personnel in some areas may prevent their usage on a large scale. There are also issues regarding accuracy and maintenance of the machines, particularly in off-places or underdeveloped areas. These may be deterrents to growth.

In spite of these challenges, the future is still very promising. Increased use of telemedicine, backing from health organizations, and increased investment in health technology may pave the way for new opportunities. Public health systems partnering with private firms may also bring low-cost solutions to more people.

Later, this will more likely result in more precise, quicker, and easier-to-use products entering the global vision testing devices market, providing improved results for patients and new potential for growth.

MARKET SEGMENTATION

By Product Type

The global vision testing devices market is steadily increasing, driven by increasing awareness of eye health and the increasing demand for early detection of vision issues. Because individuals are living longer and spending more time staring at digital screens, there is a growing demand for precise and effective vision testing equipment. This market consists of various devices that are meant to test various aspects of eye health and the clarity of vision. Every type of device contributes to enabling experts to identify problems early and make the optimal decision regarding correction or treatment. In the future, more sophisticated and easier-to-use tools will define this industry.

By product type, there are quite a few important categories in the global vision testing devices market. Visual Acuity Test Devices assist in measuring the level to which an individual can see at different distances. Such devices are usually incorporated in simple eye examinations and play a critical role in identifying vision changes. Color Vision Test Devices assist in screening for color blindness or deficiency, which may influence one's daily activities as well as certain job specifications. Refraction Test Devices assist in finding the correct prescription for glasses or contacts by measuring how light bends as it enters the eye. Retinoscopes are small instruments that are used to direct light into the eyes to examine how it bounces off of the retina, giving important information for prescribing lenses, particularly for children or individuals who might not do well with other tests.

Autorefractors and Keratometers are computerized machines that rapidly measure the way in which light is altered by the eye and the corneal shape, which is useful for detecting abnormalities and enhancing the fitting of contact lenses.

Other equipment within this category can consist of instruments utilized for more advanced tests or dual purposes to accelerate testing and make it more efficient. In the near future, the global vision testing devices market will most probably move toward more portable, connected, and AI-assisted devices that are able to provide results quickly and with high accuracy. Such upgrades will not only enable professionals to provide improved care, but even make eye testing available to those living in rural or underdeveloped regions.

With the drive for smarter healthcare systems and early intervention, there will be robust investment and innovation in the area. Generally, the market will continue to evolve to cater to an increasing population requiring sound eye health monitoring in an age of technology.

By Application

The global vision testing devices market is expected to see strong growth in the coming years. As eye health continues to gain attention worldwide, more people will seek regular eye check-ups and early diagnosis of vision problems. One of the main drivers behind this growth is the rising demand for routine eye examinations. These basic tests, often done in clinics or optical stores, help detect early signs of vision loss or other eye-related conditions. As awareness of eye health increases, especially among older adults and children, the need for such routine testing will grow steadily.

Another key area is clinical diagnosis. In this segment, professionals use specialized devices to identify specific eye conditions such as glaucoma, cataracts, or macular degeneration. As technology becomes more advanced, devices will become more accurate and efficient, allowing eye care professionals to diagnose problems faster and with more precision. This means that patients can get the right treatment sooner, which can greatly improve outcomes and prevent further vision loss. Hospitals and eye clinics will continue to invest in better diagnostic equipment, which will support the market's growth.

Surgical evaluation is also an important part of the global vision testing devices market. Before undergoing eye surgery, patients must go through a detailed assessment to determine the best course of action. Vision testing devices are vital in this process. They help measure eye structure and function so that surgeons can plan and perform procedures with confidence. As eye surgeries become safer and more common, especially procedures like LASIK or cataract removal, the need for accurate testing tools will continue to rise. These tools will support both the safety and success of surgeries.

Vision screening, especially in schools, workplaces, and community centers, is expected to play a bigger role in the future. Early detection of vision problems in children can lead to better learning outcomes, while screening in adults can help catch issues before they become serious. Portable and easy-to-use vision testing devices will likely become more widespread, helping reach people in both cities and rural areas.

Looking ahead, the global vision testing devices market will benefit from continued improvements in technology, growing awareness of eye health, and stronger healthcare infrastructure in developing regions. As more people prioritize clear vision and early detection, the use of these devices will expand across all application types making them a key part of future healthcare solutions.

By End User

The global vision testing devices market will continue to grow as eye health becomes a greater priority across the world. In the future, rising awareness about early diagnosis of vision problems will drive more people to seek regular eye check-ups. As technology keeps advancing, these devices will likely become more accurate, user-friendly, and accessible to both healthcare professionals and patients. By end user, this market is divided into hospitals, eye clinics, ambulatory surgical centers, research and academic institutes, and optical stores each of which plays a key role in supporting the growth and improvement of eye care services.

Hospitals will likely continue being major users of these devices, especially for diagnosing more complex vision issues. As healthcare systems expand, particularly in developing countries, hospitals will need more advanced and reliable tools to provide better eye care. Eye clinics, on the other hand, focus specifically on eye health, and they often serve a large number of patients who come in for regular vision screenings. This means they will always rely on updated devices that offer quicker results without compromising accuracy.

Ambulatory surgical centers are also expected to increase their use of vision testing tools. These centers provide eye surgeries and pre-operative checks that require precise measurements, making high-quality testing devices essential. Since these centers are designed for quicker services with shorter patient stays, they benefit from devices that are fast and efficient.

Research and academic institutes will keep pushing the boundaries of innovation in the vision testing field. These institutions not only train future eye care professionals but also explore new testing methods and technologies. Their work helps improve the overall quality of the tools used across the industry. As the need for more personalized and advanced eye care grows, their role in shaping the future of vision testing becomes more important.

Optical stores also have a steady demand for vision testing devices, especially those used for standard eye exams before selling prescription glasses or lenses. As more people seek convenience and quicker services, optical stores are likely to upgrade to better and smarter devices that make the process smoother.

Overall, the global vision testing devices market will move toward smarter, faster, and more connected solutions that fit the changing needs of each end user. As more attention is given to eye health, these devices will play a bigger role in both early detection and treatment, making eye care more effective and accessible to people everywhere.

|

Forecast Period |

2025-2032 |

|

Market Size in 2025 |

$3,657.82 million |

|

Market Size by 2032 |

$5,852.09 Million |

|

Growth Rate from 2025 to 2032 |

7.1% |

|

Base Year |

2024 |

|

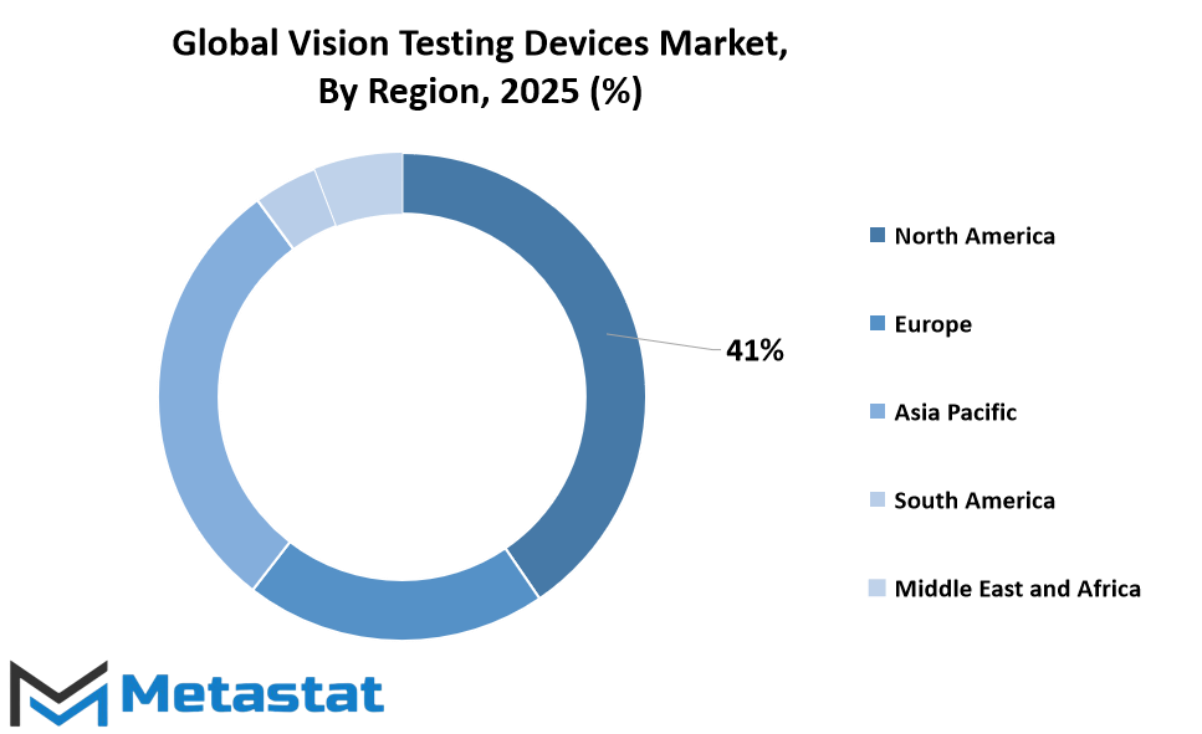

Regions Covered |

North America, Europe, Asia-Pacific Green, South America, Middle East & Africa |

REGIONAL ANALYSIS

The global vision testing devices market is expected to grow steadily as more people become aware of the importance of regular eye check-ups and early diagnosis of eye problems. As technology keeps moving forward, these devices are becoming more accurate, portable, and user-friendly. Countries across different regions are beginning to adopt smarter healthcare systems, and this is making room for better and faster vision testing. Based on geography, this market is spread across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Each of these regions has its own pace of development and unique healthcare priorities, but all are moving in the same direction toward better eye health supported by improved testing tools.

In North America, which includes the U.S., Canada, and Mexico, the market is growing fast due to strong healthcare infrastructure and quick adoption of advanced technologies. The U.S. in particular is seeing an increased demand for early diagnosis tools, especially as more people face eye strain from digital screens. Europe is not far behind, with countries like the UK, Germany, France, and Italy pushing forward with healthcare reforms and digital upgrades. The rest of Europe is catching up, helped by better access to modern devices and government support for public health initiatives.

Asia-Pacific is another key region, with countries like India, China, Japan, and South Korea leading the way in making healthcare more accessible. Rapid population growth and increasing awareness about eye health are driving the need for updated testing systems. In rural and remote parts of the region, portable and mobile vision testing devices are becoming especially useful. The South America region, which includes Brazil and Argentina, is also seeing progress, although the pace may be slightly slower. Efforts are being made to make vision care more available to everyone, even in less developed areas.

In the Middle East & Africa, which includes GCC Countries, Egypt, and South Africa, demand is rising as health awareness grows and public and private sectors start to invest more in modern equipment. This trend will likely continue, opening up new opportunities for companies focused on improving eye care. As time goes on, the global vision testing devices market will likely become even more important as people live longer and screen time increases, making eye health a growing concern worldwide.

COMPETITIVE PLAYERS

The global vision testing devices market is expected to grow steadily in the coming years, driven by advancements in eye care technology and an increased awareness of vision health across the world. As populations age and digital screen time continues to rise, more people are experiencing vision-related issues, which creates a higher demand for accurate and efficient diagnostic tools. This growing need will lead to stronger competition among companies that produce these devices, as each brand works to offer better performance, quicker testing methods, and more reliable results.

Several major players are already shaping the direction of the global vision testing devices market. Companies like Carl Zeiss Meditec AG and Topcon Corporation are well-known for their constant push to develop better optical equipment. Their research and development efforts will likely continue to bring forward smarter devices that not only check vision but also support early detection of eye conditions. NIDEK Co., Ltd. and EssilorLuxottica also play a strong role by combining technology with ease of use, aiming to reach both professionals and patients in all kinds of healthcare environments. These companies are not only focusing on improvements in hospitals and clinics but are also working to expand access in underserved areas.

Alcon Inc. and Canon Inc. bring innovation from their experience in medical and imaging devices, which allows them to create more advanced vision testing solutions. Their efforts will push the market forward, especially as demand increases for mobile and portable vision testing options. Heidelberg Engineering GmbH, Kowa Company Ltd., and Righton Limited are also contributing to this shift, designing tools that give precise results with minimal discomfort for patients. The move toward more user-friendly and automated devices will make vision testing faster and more accessible.

Other notable contributors include Tomey Corporation, Visionix Ltd., and Takagi Seiko Co., Ltd., all of whom focus on refining equipment that can meet the changing expectations of healthcare providers. Smaller but equally ambitious players like Adaptica Srl and Coburn Technologies are likely to challenge the larger companies by offering specialized tools for specific testing needs. AMETEK Inc. (Reichert Technologies) and OCULUS Optikgeräte GmbH also add to the competitive landscape, aiming to create long-term value through technology and reliability. In the future, the global vision testing devices market will be shaped by a mix of established leaders and newer innovators, all trying to meet the growing need for accurate and efficient eye care solutions.

Vision Testing Devices Market Key Segments:

By Product Type

- Visual Acuity Test Devices

- Color Vision Test Devices

- Refraction Test Devices

- Retinoscopes

- Autorefractors and Keratometers

- Other

By Application

- Routine Eye Examination

- Clinical Diagnosis

- Surgical Evaluation

- Vision Screening

By End User

- Hospitals

- Eye Clinics

- Ambulatory Surgical Centers

- Research and Academic Institutes

- Optical Stores

Key Global Vision Testing Devices Industry Players

- Carl Zeiss Meditec AG

- Topcon Corporation

- NIDEK Co., Ltd.

- EssilorLuxottica

- Alcon Inc.

- Canon Inc.

- Heidelberg Engineering GmbH

- Kowa Company Ltd.

- Righton Limited

- Tomey Corporation

- Visionix Ltd.

- Takagi Seiko Co., Ltd.

- Coburn Technologies

- Adaptica Srl

- AMETEK Inc. (Reichert Technologies)

- OCULUS Optikgeräte GmbH

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential

US: +1 3023308252

US: +1 3023308252