United States Medical Device Contract Manufacturing Market

United States Medical Device Contract Manufacturing Market Size, Share, By Device Class (Class I, Class II, and Class III), By Service Type (Device Development, Manufacturing, Quality Management, Packaging, Assembly Services, and Others), By Therapeutic Area (Cardiovascular Devices, Orthopedic Devices, Ophthalmic Devices, Diagnostic Devices, Respiratory Devices, Surgical Instruments, Dental, and Others), By End User (Original Equipment Manufacturers (OEMs), Pharmaceutical, Biopharmaceutical Companies, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4600

Published

April 13, 2026

Pages

320 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

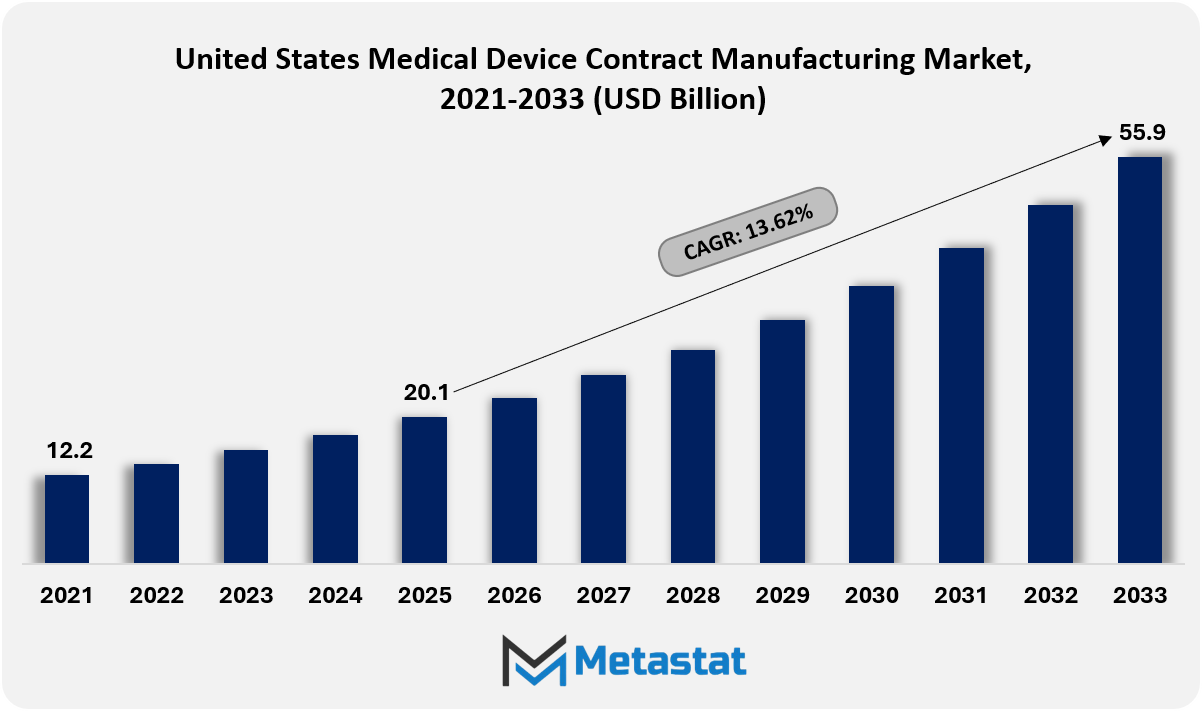

United States Medical Device Contract Manufacturing market size is valued at USD 20.1 billion in 2025 and projected to grow at a CAGR of 13.6% during the forecast period, reaching USD 55.9 billion by 2033.

United States Medical Device Contract Manufacturing Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Key trends driving growth: Rising demand for cost optimization and operational efficiency is driving OEMs to outsource production to specialized contract manufacturers, along with increasing complexity of medical devices (miniaturization, combination products, advanced materials) is accelerating reliance on technically capable MDCM partners.

Opportunities include growing demand for minimally invasive, wearable, and implantable devices presents high-value outsourcing opportunities for technologically advanced contract manufacturers.

Key insight: Strategic outsourcing and regulatory rigor shape growth trajectory in the United States Medical Device Contract Manufacturing market.

The United States Medical Device Contract Manufacturing market is evolving beyond traditional build-to-print manufacturing and is increasingly serving as a strategic extension of original equipment manufacturers. Contract partners are participating earlier in product conceptualization by offering integrated design transfer, digital prototyping, and regulatory documentation support well before commercial launch. Rather than limiting engagement to component fabrication, manufacturers are also supporting human factors validation, material traceability systems, and pre-submission documentation to streamline interactions with the U.S. Food and Drug Administration.

Advanced automation is being deployed not only to improve efficiency but also to ensure reproducibility across multi-site production ecosystems. Cloud-connected manufacturing execution systems enable OEM clients to monitor batch genealogy, calibration cycles, and deviation management in real time. Cleanroom environments are increasingly designed with modular scalability so that emerging device categories such as combination products and minimally invasive platforms can move from pilot builds to scaled output without extensive facility redesign.

Market Dynamics

Growth Drivers:

Rising demand for cost optimization and operational efficiency is driving OEMs to outsource production to specialized contract manufacturers.

Rising cost pressure across the healthcare value chain is encouraging OEMs to outsource production to specialized contract manufacturers. This model helps reduce capital expenditure, improve asset utilization, and support faster commercialization without the need to build large in-house production networks. Contract manufacturing partners that offer integrated services across development, assembly, packaging, and quality support are becoming increasingly valuable to medical device companies operating in the United States.

Increasing complexity of medical devices (miniaturization, combination products, advanced materials) is accelerating reliance on technically capable MDCM partners.

Medical devices are becoming more sophisticated with growing use of miniaturized components, advanced biomaterials, embedded electronics, and combination product designs. These technical requirements are increasing reliance on contract manufacturers with precision engineering expertise, cleanroom capabilities, and strong quality systems. Providers that can support complex builds while maintaining regulatory discipline are likely to gain stronger positions across the United States Medical Device Contract Manufacturing market.

Restraints and Challenges:

Stringent regulatory compliance requirements and evolving global quality standards increase operational burden and validation costs.

Regulatory compliance remains a major operational challenge in the United States Medical Device Contract Manufacturing market. Manufacturers must maintain strict documentation, validation protocols, quality management systems, and traceability frameworks to meet evolving requirements. These obligations increase operating costs, extend project timelines, and require continuous investment in compliance infrastructure, audit preparedness, and process control.

Supply chain disruptions and dependency on single-source suppliers create production risks and margin pressure.

Supply chain instability continues to create production risks across the United States Medical Device Contract Manufacturing market. Dependence on specialized materials, electronic components, and single-source suppliers can affect production continuity, delivery schedules, and pricing stability. Contract manufacturers are therefore placing greater emphasis on supplier diversification, domestic sourcing strategies, and stronger inventory planning to improve resilience and protect margins.

Opportunities:

Growing demand for minimally invasive, wearable, and implantable devices presents high-value outsourcing opportunities for technologically advanced contract manufacturers.

Expanding use of minimally invasive, wearable, and implantable devices is opening attractive outsourcing opportunities across the United States Medical Device Contract Manufacturing market. These products require advanced capabilities in micro-assembly, precision molding, sterile manufacturing, and material handling. Contract manufacturers with strong technical depth and validated production environments are well positioned to capture higher-value programs in these fast-evolving device categories.

Market Segmentation Analysis

The United States Medical Device Contract Manufacturing market is classified based on Device Class, Service Type, Therapeutic Area, and End User.

By Device Class, the market is further segmented into:

Class I

Class I segment is valued at USD 6.1 billion in 2026 and is projected to reach USD 15.1 billion by 2033, at a CAGR of 13.7% during the forecast period.

Class I devices hold a stable position in the United States Medical Device Contract Manufacturing market, supported by ongoing demand for low-risk consumables, disposables, and basic medical instruments. Manufacturing activity in this segment benefits from standardized production processes, efficient assembly systems, and cost-focused supply models. Contract manufacturers with strong volume management and quality consistency are expected to maintain a solid presence in this category.

Class II

Class II segment is valued at USD 10.2 billion in 2026 and is projected to reach USD 24.8 billion by 2033, at a CAGR of 13.6% during the forecast period.

Class II devices represent a major portion of the United States Medical Device Contract Manufacturing market owing to their broad use across diagnostic, monitoring, and therapeutic applications. This segment requires stronger validation, tighter quality control, and greater engineering precision than lower-risk categories. Contract manufacturers with expertise in precision molding, electronics integration, and regulated assembly are likely to benefit from sustained outsourcing demand in Class II programs.

Class III

Class III segment is valued at USD 6.5 billion in 2026 and is projected to reach USD 16 billion by 2033, at a CAGR of 13.7% during the forecast period.

Class III devices occupy the highest-value end of the United States Medical Device Contract Manufacturing market and require stringent manufacturing controls, advanced material expertise, and robust regulatory alignment. These products include life-sustaining and implantable technologies where quality assurance and process validation are critical. Long-term collaboration between OEMs and contract manufacturers is especially important in this segment to support commercialization, patient safety, and supply reliability.

By Service Type, the market is divided into:

Device Development and Manufacturing

Device Development and Manufacturing segment is projected to reach USD 29 billion by 2033, at a CAGR of 13.6% during the forecast period.

Device Development and Manufacturing remains the core service category within the United States Medical Device Contract Manufacturing market. OEMs increasingly prefer partners that can support concept refinement, prototyping, process optimization, scale-up, and full commercial production within a unified operating model. This integrated approach helps shorten development timelines, improve manufacturing readiness, and strengthen operational continuity across the product lifecycle.

Quality Management

Quality Management segment is projected to reach USD 14.1 billion by 2033, at a CAGR of 13.4% during the forecast period.

Quality Management is a critical service area across the United States Medical Device Contract Manufacturing market. Manufacturers are investing in digital documentation systems, automated inspection technologies, process validation, and audit readiness to meet strict compliance requirements. Service providers with strong quality infrastructure and consistent regulatory performance are better positioned to build long-term customer relationships and manage higher-complexity programs.

Packaging and Assembly Services

Packaging and Assembly Services segment is projected to reach USD 8.9 billion by 2033, at a CAGR of 13.8% during the forecast period.

Packaging and Assembly Services play an essential role in supporting product integrity, sterility, labeling compliance, and shipment efficiency. In the United States Medical Device Contract Manufacturing market, customers are increasingly seeking partners that can provide automated assembly, sterile barrier packaging, serialization, and traceability-enabled labeling. Providers that combine regulatory discipline with scalable operations are likely to strengthen their position in this service segment.

Others

Others segment is projected to reach USD 3.8 billion by 2033, at a CAGR of 14.6% during the forecast period.

Other services include supply chain coordination, regulatory support, inventory management, and lifecycle assistance. These capabilities are gaining importance with OEMs seeking fewer vendors and broader operating support from manufacturing partners. Contract manufacturers with diversified service portfolios are increasingly moving from transactional supply roles to strategic partnership models.

By Therapeutic Area, the market is further divided into:

Cardiovascular Devices

Cardiovascular Devices segment is projected to reach USD 13.5 billion by 2033.

Cardiovascular devices represent a significant therapeutic area within the United States Medical Device Contract Manufacturing market. The segment benefits from continued product development in catheters, implantable systems, monitoring technologies, and minimally invasive treatment devices. Contract manufacturers with capabilities in precision components, advanced materials, and validated cleanroom production are well placed to support the demanding requirements of cardiovascular programs.

Orthopedic Devices

Orthopedic Devices segment is projected to reach USD 10.2 billion by 2033.

Orthopedic devices remain a major source of outsourcing activity in the United States Medical Device Contract Manufacturing market. The segment includes implants, fixation products, and surgical tools that often require high-precision machining, advanced biomaterials, and strong production consistency. Contract manufacturers that support complex geometries, scalable output, and regulated quality systems are likely to maintain strong relevance in orthopedic manufacturing.

Ophthalmic Devices

Ophthalmic Devices segment is projected to reach USD 5.9 billion by 2033.

Ophthalmic devices contribute to specialized manufacturing demand across the United States Medical Device Contract Manufacturing market. These products require fine tolerances, precision optics integration, and highly controlled assembly processes. Contract manufacturers with expertise in micro-scale production and quality-sensitive fabrication are well positioned to support innovation across diagnostic, corrective, and surgical ophthalmic applications.

Diagnostic Devices

Diagnostic Devices segment is projected to reach USD 8.7 billion by 2033.

Diagnostic devices represent an important growth area in the United States Medical Device Contract Manufacturing market. Expanding use of point-of-care systems, laboratory instruments, biosensors, and portable testing platforms is increasing the need for flexible, high-precision manufacturing support. Contract manufacturers that can scale output efficiently while maintaining validation and compliance standards are expected to remain in strong demand across this category.

Respiratory Devices

Respiratory Devices segment is projected to reach USD 4.6 billion by 2033.

Respiratory devices continue to create steady manufacturing demand across the United States Medical Device Contract Manufacturing market. Products in this segment require dependable sourcing, sterile assembly, reliable component quality, and responsive production capacity. Contract manufacturers with adaptable operations and stable quality systems are likely to remain important partners for respiratory device OEMs and healthcare-focused technology developers.

Surgical Instruments

Surgical Instruments segment is projected to reach USD 6 billion by 2033.

Surgical Instruments maintain a steady position within the United States Medical Device Contract Manufacturing market, supported by ongoing procedural demand and the need for durable, precision-engineered tools. Manufacturing in this area requires strong capabilities in machining, finishing, sterilization support, and quality control. Contract manufacturers that deliver consistent workmanship and compliance-focused production are expected to preserve strong relationships in this segment.

Dental

Dental segment is projected to reach USD 2.9 billion by 2033.

Dental devices are gaining traction in the United States Medical Device Contract Manufacturing market with increasing use of digital workflows, customized components, and biocompatible materials. The segment requires detailed fabrication, efficient production turnaround, and high repeatability across product batches. Contract manufacturers that support flexible production and application-specific engineering are likely to benefit from continued expansion in dental technology.

Others

Others segment is projected to reach USD 4 billion by 2033.

Other therapeutic areas in the United States Medical Device Contract Manufacturing market include neurology, wound care, drug delivery, and specialty intervention devices. These categories often require mixed material expertise, application-specific engineering, and flexible manufacturing support. Contract manufacturers with adaptable infrastructure and broad technical capabilities are likely to capture opportunities across these emerging and niche device segments.

By End User, the United States Medical Device Contract Manufacturing market is divided as:

Original Equipment Manufacturers (OEMs)

Original Equipment Manufacturers (OEMs) segment is projected to grow at a CAGR of 13.6% during the forecast period.

Original Equipment Manufacturers remain the primary end users in the United States Medical Device Contract Manufacturing market. Many OEMs are increasing outsourcing activity to reduce fixed manufacturing costs, accelerate product launch timelines, and focus internal resources on innovation, branding, and commercialization. This shift is strengthening the strategic importance of contract manufacturing partnerships across the medical device value chain.

Pharmaceutical & Biopharmaceutical Companies

Pharmaceutical & Biopharmaceutical Companies segment is projected to grow at a CAGR of 14% during the forecast period.

Pharmaceutical and biopharmaceutical companies are becoming increasingly important end users in the United States Medical Device Contract Manufacturing market, particularly for drug delivery systems, combination products, and specialized packaging formats. These applications require sterile production, process validation, and close regulatory coordination. Contract manufacturers that support both device-related and therapy-linked requirements are likely to see rising engagement from this customer group.

Others

Others segment is projected to grow at a CAGR of 13.1% during the forecast period.

Other end users in the United States Medical Device Contract Manufacturing market include research institutions, start-ups, and emerging medical technology companies. These organizations often require pilot-scale manufacturing, engineering support, and flexible production arrangements before full commercialization. Contract manufacturers offering technical guidance and scalable operating models are well positioned to serve this end-user segment.

Competitive Landscape and Strategic Insights

The United States Medical Device Contract Manufacturing market is expanding steadily owing to rising demand for advanced healthcare products, cost pressure on original equipment manufacturers, and the need for faster product launches. Medical device companies are focusing more on research, branding, and distribution, while outsourcing manufacturing to specialized contract manufacturers. This shift is expected to continue as it helps device innovators reduce capital investment, improve operational efficiency, and scale production without building large in-house facilities. Contract manufacturers are strengthening capabilities in precision machining, micro molding, cleanroom assembly, and regulatory support to meet strict industry standards.

Technology development is playing a central role in shaping the market. Rising demand for minimally invasive devices, diagnostic tools, wearable monitoring systems, and implantable components is pushing manufacturers to adopt advanced automation, robotics, and quality inspection systems. Regulatory compliance in the United States remains stringent, and manufacturers must meet standards set by the Food and Drug Administration. Companies that can ensure traceability, validation, and consistent quality control are securing long-term partnerships with leading medical device manufacturers. Many service providers are also investing in design support and early-stage engineering to become strategic partners rather than only manufacturing vendors.

The aggressive landscape includes numerous competitors with vast technical knowledge and nationwide manufacturing footprints. Key members in the market encompass Integer Holdings Corporation, Viant Medical, Inc., Cirtec Medical Corporation, Phillips-Medisize, LLC, Jabil Inc., Sanmina Corporation, Plexus Corp., Benchmark Electronics, Inc., Kimball Electronics, Inc., Nortech Systems, Incorporated, SigmaTron International, Inc., Key Tronic Corporation, TTM Technologies, Inc., SMC Ltd., Cadence, Inc., Tecomet, Inc., Orchid Orthopedic Solutions, Tegra Medical, Paragon Medical, Inc., Quasar Medical, LLC, Heraeus Medevio, Spectrum Plastics Group, Aptyx, Inc., Seisa Medical, Inc., Elevaris Medical Devices Inc., Sterling Industries, Inc., Medical Murray, Inc., Tessy Plastics Corporation, Kaysun Corporation, Accumold, LLC, PTI Engineered Plastics, Inc., Westfall Technik, LLC, Natech Plastics, Inc., MME Group, Inc., and ARCH Medical Solutions Corp. These organizations consciousness on product development support, issue manufacturing, very last assembly, and supply chain management for a wide range of clinical applications.

Mergers, acquisitions, and capacity expansion are expected to remain important strategic moves across the United States Medical Device Contract Manufacturing market. Many companies are increasing domestic manufacturing presence to improve supply security, shorten lead times, and align with customer preference for U.S. based production.

Forecast and Future Outlook

Market size is forecast to rise from USD 20.1 billion in 2025 to over USD 55.9 billion by 2033.

The United States Medical Device Contract Manufacturing market is expected to move further toward an integrated partnership model over the forecast period. Contract manufacturers will increasingly support early-stage engineering, regulatory planning, digital production visibility, and lifecycle management alongside core manufacturing services. Providers that invest in advanced production technologies, compliance infrastructure, and broader service capabilities are likely to strengthen their long-term competitive position in the market.

Medical Device Contract Manufacturing Market Key Segments:

By Device Class:

Class I

Class II

Class III

By Service Type:

Device Development and Manufacturing

Quality Management

Packaging and Assembly Services

Others

By Therapeutic Area:

Cardiovascular Devices

Orthopedic Devices

Ophthalmic Devices

Diagnostic Devices

Respiratory Devices

Surgical Instruments

Dental

Others

By End User:

Original Equipment Manufacturers (OEMs)

Pharmaceutical & Biopharmaceutical Companies

Others

Key United States Medical Device Contract Manufacturing Industry Players

This research report categorizes the United States Medical Device Contract Manufacturing market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Medical Device Contract Manufacturing market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Medical Device Contract Manufacturing market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 13.6% from 2026 to 2033

Revenue Unit

USD billion

Sales Volume Unit

Thousand Units

Segmentation

By Device Class, Service Type, Therapeutic Area, End User, and Region

By Device Class

Class I

Class II

Class III

By Service Type

Device Development and Manufacturing

Quality Management

Packaging and Assembly Services

Others

By Therapeutic Area

Cardiovascular Devices

Orthopedic Devices

Ophthalmic Devices

Diagnostic Devices

Respiratory Devices

Surgical Instruments

Dental

Others

By End User

Original Equipment Manufacturers (OEMs)

Pharmaceutical & Biopharmaceutical Companies

Others

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

India Maternal Health Monitoring Market Size, Share, Trends, 2033

India Maternal Health Monitoring market size is valued at USD 416.0 million in 2025 and is projected to reach USD 834.4 million in 2033, at a CAGR of 9.1% from 2026 to 2033

India Maternal Health Monitoring Market, India Maternal Health Monitoring Market Size, India Maternal Health Monitoring Market Share, India Maternal Health Monitoring Market Analysis, India Maternal Health Monitoring Market Growth, India Maternal Health Monitoring Market Trends, India Maternal Health Monitoring Market Research Report, India Maternal Health Monitoring Market Forecast, India Maternal Health Monitoring, India Maternal Health Monitoring Market Research, India Maternal Health Monitoring Industry, India Maternal Health Monitoring Industry Report, India Maternal Health Monitoring Market Data, India Maternal Health Monitoring Statistics, India Maternal Health Monitoring Market Statistics, India Maternal Health Monitoring Industry Trends, India Maternal Health Monitoring Market Report, India Maternal Health Monitoring Market Trends, India Maternal Health Monitoring Market News, India Maternal Health Monitoring Forecasts, India Maternal Health Monitoring Market Intelligence Report

Global Anaerobic Incubators market size is valued at USD 177.5 million in 2025 and is projected to reach USD 323.6 million in 2033, at a CAGR of 7.8% from 2026 to 2033

Global Radiochemical Synthesizers market size is valued at USD 450.5 million in 2025 and is projected to reach USD 746.6 million in 2033, at a CAGR of 6.7% from 2026 to 2033.

Global Radiochemical Synthesizers Market, Global Radiochemical Synthesizers Market Size, Global Radiochemical Synthesizers Market Share, Global Radiochemical Synthesizers Market Analysis, Global Radiochemical Synthesizers Market Growth, Global Radiochemical Synthesizers Market Trends, Global Radiochemical Synthesizers Market Research Report, Global Radiochemical Synthesizers Market Forecast, Global Radiochemical Synthesizers, Global Radiochemical Synthesizers Market Research, Global Radiochemical Synthesizers Industry, Global Radiochemical Synthesizers Industry Report, Global Radiochemical Synthesizers Market Data, Global Radiochemical Synthesizers Statistics, Global Radiochemical Synthesizers Market Statistics, Global Radiochemical Synthesizers Industry Trends, Global Radiochemical Synthesizers Market Report, Global Radiochemical Synthesizers Market Trends, Global Radiochemical Synthesizers Market News, Global Radiochemical Synthesizers Forecasts, Global Radiochemical Synthesizers Market Intelligence Report

Thoracolumbar Posterior Fixation Systems Market Size, Share, Trends, 2033

Global Thoracolumbar Posterior Fixation Systems market size is valued at USD 875.8 million in 2025 and is projected to reach USD 1,526.6 million in 2033, at a CAGR of 7.2% from 2026 to 2033

Thoracolumbar Posterior Fixation Systems Market, Thoracolumbar Posterior Fixation Systems Market Size, Thoracolumbar Posterior Fixation Systems Market Share, Thoracolumbar Posterior Fixation Systems Market Analysis, Thoracolumbar Posterior Fixation Systems Market Growth, Thoracolumbar Posterior Fixation Systems Market Trends, Thoracolumbar Posterior Fixation Systems Market Research Report, Thoracolumbar Posterior Fixation Systems Market Forecast, Thoracolumbar Posterior Fixation Systems, Thoracolumbar Posterior Fixation Systems Market Research, Thoracolumbar Posterior Fixation Systems Industry, Thoracolumbar Posterior Fixation Systems Industry Report, Thoracolumbar Posterior Fixation Systems Market Data, Thoracolumbar Posterior Fixation Systems Statistics, Thoracolumbar Posterior Fixation Systems Market Statistics, Thoracolumbar Posterior Fixation Systems Industry Trends, Thoracolumbar Posterior Fixation Systems Market Report, Thoracolumbar Posterior Fixation Systems Market Trends, Thoracolumbar Posterior Fixation Systems Market News, Thoracolumbar Posterior Fixation Systems Forecasts, Thoracolumbar Posterior Fixation Systems Market Intelligence Report