Global Radiochemical Synthesizers Market Size, Share, By Type (Benchtop Synthesizers, Console Synthesizers, Microfluidic Synthesizers, and Others), By Application (Positron Emission Tomography (PET), Single Photon Emission Computed Tomography (SPECT), and Others), By End-Use (Hospitals, Diagnostic Centers, Research Institutes, and Others), By Product Type (Fully Automated Synthesizers, Semi-Automated Synthesizers, and Manual Synthesizers), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4774

Published

May 27, 2026

Pages

315 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

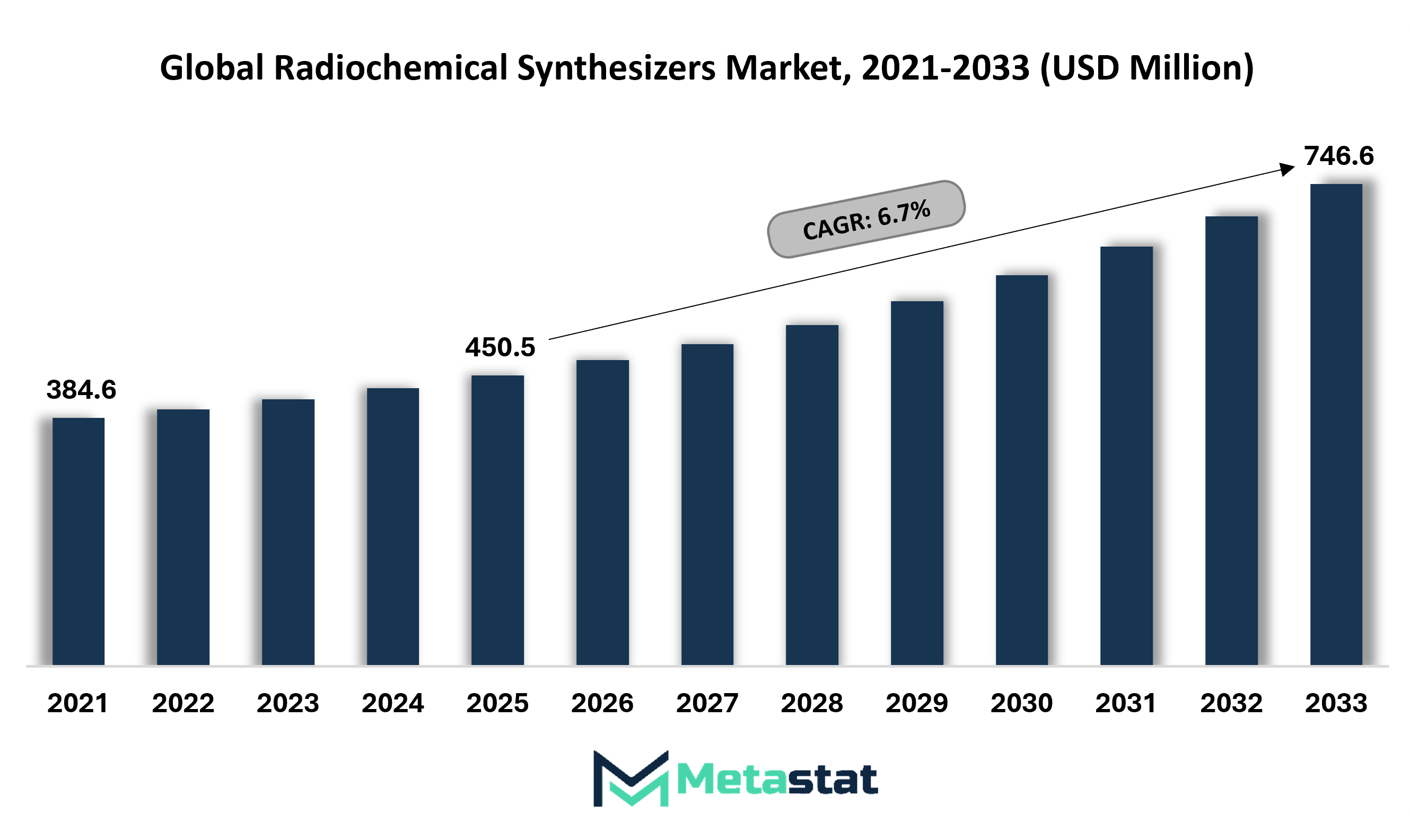

Global Radiochemical Synthesizers market size is valued at USD 450.5 million in 2025 and projected to grow at a CAGR of 6.7% during the forecast period, reaching USD 746.6 million by 2033.

Global Radiochemical Synthesizers Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

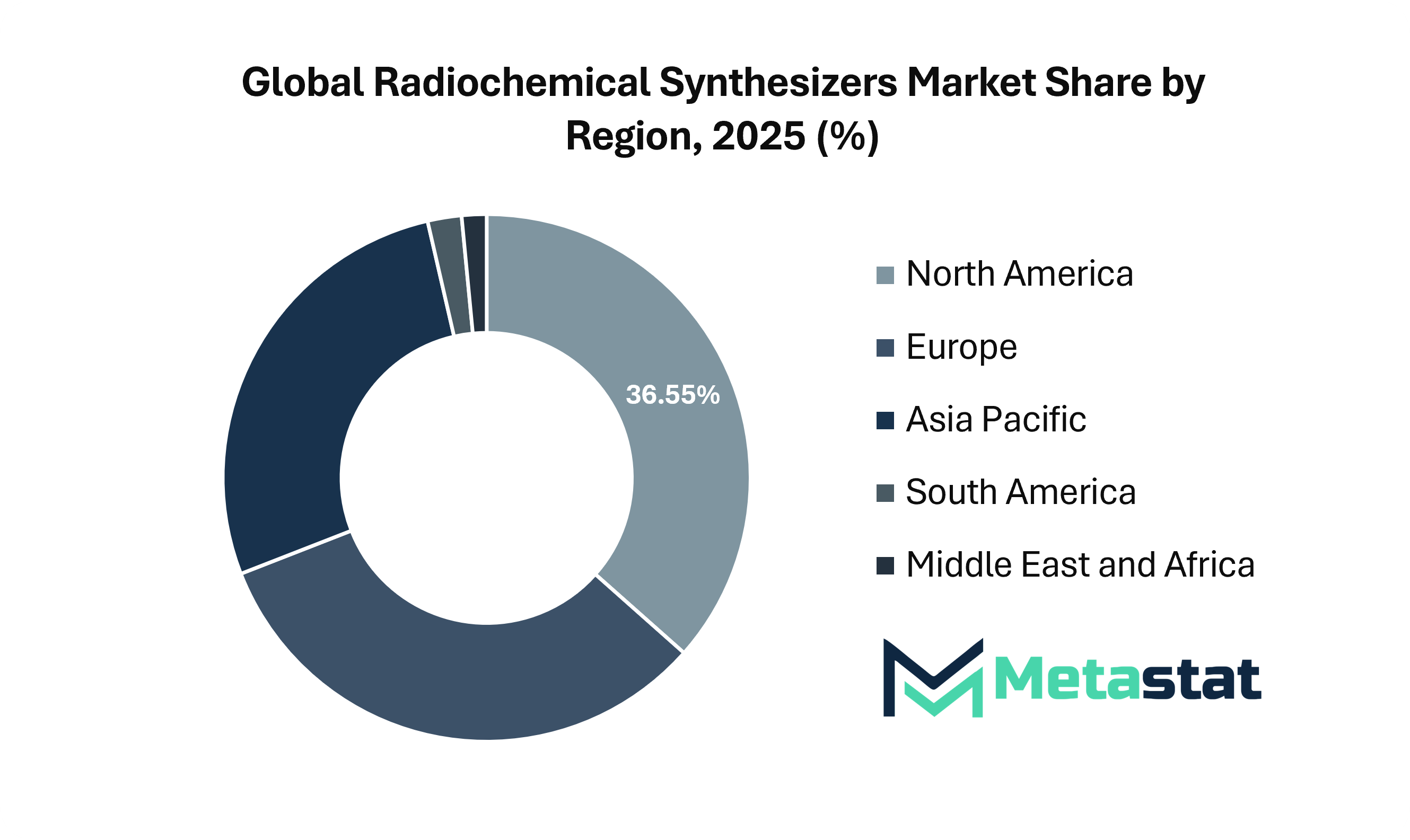

North America holds 36.6% market share in 2025, with the U.S. leading regional revenue contribution.

The benchtop synthesizers segment accounts for 39.94% market share in 2025.

Key trends driving growth: Rising incidence of cancer and neurological disorders increasing demand for diagnostic imaging and advancements in automated synthesizer technologies improving efficiency and safety.

Opportunities include expansion of targeted radionuclide therapy creating new application areas and growth in emerging markets with improving healthcare infrastructure.

Key insight: Growing reliance on nuclear imaging and targeted radiotherapy is positioning radiochemical synthesizers as critical infrastructure in modern healthcare.

The global radiochemical synthesizers market is closely linked to the expansion of nuclear medicine, where these systems are used to produce radiotracers for diagnostic imaging and targeted therapies. The market is witnessing steady growth, driven by the rising incidence of cancer, neurological disorders, and cardiovascular diseases that require advanced imaging modalities such as PET and SPECT. Hospitals, research institutes, and pharmaceutical companies form the core end-user base, with hospitals leading adoption owing to higher patient volumes and established imaging infrastructure. Technological advancement has shifted the market toward automated synthesizers that improve reproducibility, safety, and efficiency while reducing human exposure to radioactive materials and improving throughput in clinical and research settings.

From a structural standpoint, the market is supported by cyclotron-based, nuclear reactor-based, and radionuclide generator-based systems, each serving distinct production and application requirements. North America and Europe dominate owing to advanced healthcare infrastructure, strong R&D ecosystems, and favorable reimbursement policies, while Asia-Pacific is emerging as a high-growth region supported by increasing healthcare investments and rising disease burden. Competitive intensity remains high, with established players focusing on innovation and product differentiation, while newer entrants explore niche applications and cost-effective solutions. Despite strong demand, high capital investment, regulatory complexity, and operational challenges continue to influence adoption patterns across regions.

Market Dynamics

Growth Drivers:

Rising incidence of cancer and neurological disorders increasing demand for diagnostic imaging.

The increasing burden of cancer and neurological disorders across the global population continues to drive demand for advanced diagnostic imaging solutions. Greater reliance on precision diagnostics is encouraging the adoption of radiochemical synthesizers across healthcare facilities. The global radiochemical synthesizers market reflects steady expansion, supported by the need for early detection, accurate disease monitoring, and improved patient outcomes.

Advancements in automated synthesizer technologies improving efficiency and safety.

Continuous progress in automated synthesizer technology enhances operational efficiency while reducing human exposure to radioactive materials. Integration of advanced software systems supports consistent production quality and minimizes manual intervention. Healthcare providers are showing rising preference for reliable automation, creating favorable conditions for radiochemical synthesizer production and deployment across research and clinical environments.

Market Restraints:

High capital and maintenance costs limiting adoption in smaller facilities.

The significant investment required for installation and ongoing maintenance of radiochemical synthesizers creates a major barrier for smaller healthcare facilities and research institutions. Budget constraints restrict access to advanced equipment, leading to uneven adoption rates. Financial pressure influences procurement decisions, slowing penetration across emerging economies and limiting broader accessibility within diagnostic infrastructure.

Short half-life of radioisotopes creating logistical and operational constraints.

The short half-life of radioisotopes creates challenges in storage, transportation, and timely utilization. Facilities require precise coordination to ensure effective usage within limited timeframes. Delays or inefficiencies will result in material wastage and increased operational costs. Strong logistics networks remain essential to maintain consistent supply chains for radiochemical synthesis procedures.

Opportunities:

Expansion of targeted radionuclide therapy creating new application areas.

Growing focus on targeted radionuclide therapy is opening new avenues for radiochemical synthesizer applications in personalized medicine. Increased funding in precision oncology supports the development of specialized radiopharmaceuticals tailored to disease profiles. Advancements in therapeutic strategies are encouraging innovation, allowing manufacturers to explore diverse clinical applications and improve long-term growth potential across healthcare sectors.

Market Segmentation Analysis

The global radiochemical synthesizers market is classified by type, application, end user, and product type.

By Type, the market is further segmented into:

Benchtop Synthesizers

Benchtop Synthesizers segment is valued at USD 189.9 million in 2026 and is projected to reach USD 305.0 million by 2033, at a CAGR of 7% during the forecast period.

Benchtop synthesizers are witnessing steady adoption across compact laboratory environments, supported by space efficiency and operational precision. Growing demand for controlled synthesis in space-constrained infrastructure settings will support segment expansion. Integration of user-friendly interfaces and improved safety mechanisms will further enhance usability and consistent output quality.

Console Synthesizers

Console Synthesizers segment is valued at USD 161.8 million in 2026 and is projected to reach USD 247.5 million by 2033, at a CAGR of 6.3% during the forecast period.

Console synthesizers reflect strong preference for high-capacity production in advanced facilities requiring scalability. Large-scale diagnostic centers and research hubs will invest in console-based systems owing to reliability and throughput advantages. Enhanced automation features and robust shielding technologies will support safety standards and operational continuity.

Microfluidic Synthesizers

Microfluidic Synthesizers segment is valued at USD 78.8 million in 2026 and is projected to reach USD 133.5 million by 2033, at a CAGR of 7.8% during the forecast period.

Microfluidic synthesizers are gaining traction through improved reagent control and reduced waste generation. Demand for miniaturized systems will increase with rising focus on cost efficiency and faster reaction cycles. Advancements in chip-based designs will enable improved reproducibility and streamlined workflows in modern radiochemistry laboratories.

Others

Others segment is valued at USD 43.4 million in 2026 and is projected to reach USD 60.7 million by 2033, at a CAGR of 4.9% during the forecast period.

Other synthesizer types in the radiochemical synthesizers market include emerging hybrid models and customized systems designed for niche applications. Continuous research efforts will introduce adaptable configurations addressing specific synthesis requirements. Growing collaboration between technology developers and healthcare institutions will expand product range and enhance functional capabilities.

Positron Emission Tomography (PET) segment is projected to reach USD 375.0 million by 2033, at a CAGR of 7% during the forecast period.

Positron emission tomography applications will witness strong growth owing to rising demand for early disease detection and precise imaging solutions. Increasing production of PET tracers will drive synthesizer adoption. Technological advancements in radiotracer synthesis will support higher accuracy and efficiency in diagnostic imaging procedures.

Single Photon Emission Computed Tomography (SPECT)

Single Photon Emission Computed Tomography (SPECT) segment is projected to reach USD 270.1 million by 2033, at a CAGR of 6.7% during the forecast period.

Single photon emission computed tomography applications highlight consistent utilization in cardiac and neurological diagnostics. Demand for reliable radiopharmaceutical preparation will support system adoption. Enhanced synthesis protocols and strong isotope-handling techniques will contribute to improved imaging outcomes and operational safety.

Others

Others segment is projected to reach USD 101.5 million by 2033, at a CAGR of 5.6% during the forecast period.

Other applications in the radiochemical synthesizers market include therapeutic radiopharmaceutical development and experimental imaging techniques. Expansion in nuclear medicine research will increase demand for flexible synthesizer systems. Continuous innovation in compound development will create new opportunities for synthesis technologies across various clinical and scientific fields.

By End-Use, the market is further divided into:

Hospitals

Hospitals segment is projected to reach USD 334.2 million by 2033.

Hospitals in the radiochemical synthesizers market represent major end-user contributors, supported by rising adoption of in-house radiopharmaceutical preparation. Growing focus on rapid diagnostics will encourage investment in advanced synthesizer systems. Integration with hospital imaging departments will enhance workflow efficiency and patient care delivery.

Diagnostic Centers

Diagnostic Centers segment is projected to reach USD 205.0 million by 2033.

Diagnostic centers are installing compact and automated systems to meet rising imaging demand. High patient volumes will require consistent tracer availability. Technological advancements will support faster synthesis cycles, ensuring timely diagnostic procedures and improved service capabilities.

Research Institutes

Research Institutes segment is projected to reach USD 161.9 million by 2033.

Research institutes in the radiochemical synthesizers market play a crucial role in innovation and development of new radiochemical compounds. Continuous funding in nuclear medicine research will drive equipment adoption. Advanced synthesizer systems will support experimental accuracy and enable breakthroughs in imaging and therapeutic applications.

Others

Others segment is projected to reach USD 45.6 million by 2033.

Other end-user segments in the radiochemical synthesizers market include academic laboratories and specialized production centers focused on niche radiochemical applications. Expansion in academic research programs will support demand. Collaboration across industry and academia will encourage development of flexible synthesizer technologies.

By Product Type, the Global Radiochemical Synthesizers market is divided as:

Fully Automated Synthesizers

Fully Automated Synthesizers segment is projected to grow at a CAGR of 7.2% during the forecast period.

Fully automated synthesizers reflect strong demand for precision, safety, and minimal human intervention. Automation will reduce operational errors and enhance reproducibility. Growing adoption across high-throughput environments will support consistent radiopharmaceutical production and regulatory compliance.

Semi-Automated Synthesizers

Semi-Automated Synthesizers segment is projected to grow at a CAGR of 6.4% during the forecast period.

Semi-automated synthesizers provide a balance between manual control and automation, making them suitable for facilities requiring operational flexibility. Moderate investment requirements will encourage adoption in mid-scale operations. Continuous improvements in interface design will improve usability and process control.

Manual Synthesizers

Manual Synthesizers segment is projected to grow at a CAGR of 5.4% during the forecast period.

Manual synthesizers maintain relevance in low-resource settings and research-focused environments requiring customization. Skilled handling will remain essential for operation. A gradual transition toward automated solutions will occur, yet manual systems will continue serving specialized experimental needs.

By Region:

Based on geography, the Global Radiochemical Synthesizers market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America is supported by strong healthcare infrastructure, high spending on diagnostic imaging, the presence of major industry players, and advanced research capabilities.

Europe continues to hold a strong position, supported by established nuclear medicine networks, supportive regulatory frameworks, and increasing funding in radiopharmaceutical research, especially across Germany, France, and the United Kingdom.

Asia-Pacific will witness strong growth, supported by rapid healthcare infrastructure development in China and India, increasing pharmaceutical R&D investments, and expanding nuclear medicine facilities.

South America and the Middle East & Africa are witnessing gradual adoption, supported by improving healthcare access and rising awareness of advanced diagnostic techniques. However, limited infrastructure, lower diagnosis rates, and financial constraints continue to restrict large-scale deployment, creating a mixed growth outlook with selective high-potential markets.

Competitive Landscape and Strategic Insights

The global radiochemical synthesizers market has gained consistent attention owing to the growing need for accurate imaging and targeted therapy in modern healthcare. These systems play a critical role in producing radiotracers that support diagnostic procedures, especially in oncology and neurology. Hospitals and research facilities depend on these tools to improve precision, reduce human error, and maintain safety standards while handling radioactive substances. Market expansion will continue as healthcare providers seek faster and more reliable methods to prepare compounds used in advanced scans and therapies.

Technology upgrades have made these systems more compact and user-friendly, encouraging wider adoption across large clinical institutions and smaller diagnostic setups. Automation has reduced manual intervention, helping specialists focus on patient care rather than complex preparation steps. Demand will rise with growing awareness of early disease detection, where radiopharmaceuticals play a key role. Regulatory requirements have pushed manufacturers to design equipment that meets strict safety and quality standards, ensuring consistent output without compromising operator protection.

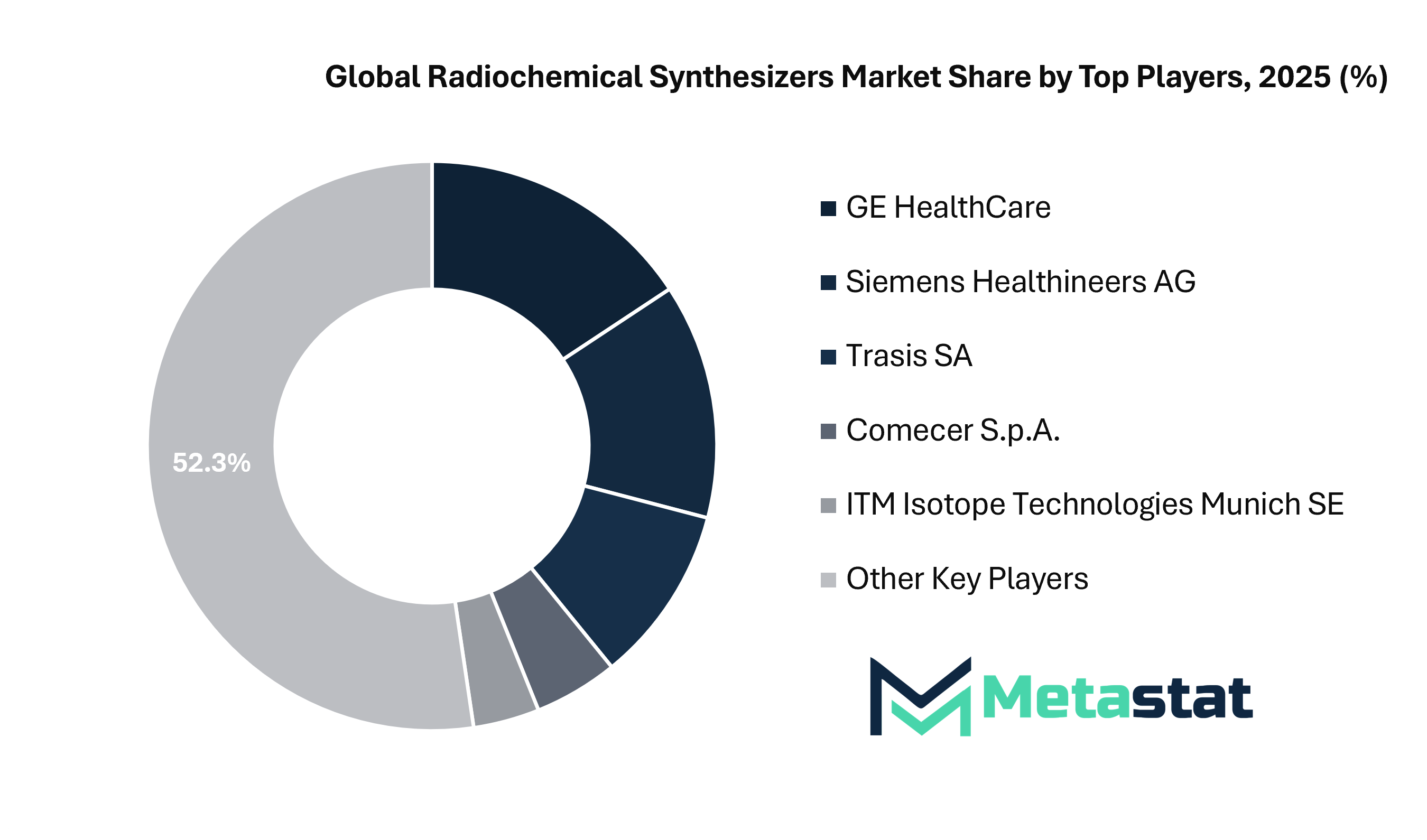

The competitive landscape includes established companies and specialized firms that continue to bring innovation into the market. Key global radiochemical synthesizers industry players include IBA Radiopharma Solutions, Eckert & Ziegler, Synthra GmbH, Siemens Healthineers AG, GE HealthCare, Trasis SA, Elysia SA, Comecer S.p.A., IPHASE technologies Pty Ltd, and ITM Isotope Technologies Munich SE. These companies focus on improving performance, reliability, and ease of use across their systems. Many players invest in research partnerships and product enhancements to stay competitive and meet changing customer requirements across regions.

Looking ahead, the market will witness further expansion, supported by rising healthcare investments and a strong shift toward personalized medicine. Increasing collaboration between research institutions and system manufacturers will support the development of new applications. While high initial costs will remain a concern for some buyers, long-term benefits such as accuracy, safety, and reduced operational effort will strengthen the investment case. With ongoing innovation and wider acceptance, the global radiochemical synthesizers market will continue to expand and support improved outcomes in medical diagnostics and therapy.

Forecast and Future Outlook

Market size is forecast to rise from USD 450.5 million in 2025 to over USD 746.6 million by 2033.

Looking ahead, the market is expected to benefit from continued advancements in radiopharmaceutical development, increasing adoption of personalized medicine, and growing government support for nuclear medicine infrastructure. Rising investment in automated synthesis platforms and targeted radionuclide therapy will further strengthen long-term market prospects.

Radiochemical Synthesizers Market Key Segments:

By Type:

Benchtop Synthesizers

Console Synthesizers

Microfluidic Synthesizers

Others

By Application:

Positron Emission Tomography (PET)

Single Photon Emission Computed Tomography (SPECT)

Others

By End-Use:

Hospitals

Diagnostic Centers

Research Institutes

Others

By Product Type:

Fully Automated Synthesizers

Semi-Automated Synthesizers

Manual Synthesizers

Key Global Radiochemical Synthesizers Industry Players

This research report categorizes the radiochemical synthesizers market based on key segments and regions, forecasts revenue growth, and analyzes trends across each submarket. The report evaluates key growth drivers, opportunities, and challenges influencing the radiochemical synthesizers market. Recent market developments and competitive strategies such as expansions, product launches, partnerships, mergers, and acquisitions have been included to present the competitive landscape.

The report strategically identifies and profiles key market players and analyzes their core competencies across each sub-segment of the radiochemical synthesizers market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 6.7% from 2026 to 2033

Revenue Unit

USD million

Sales Volume Unit

Units

Segmentation

By Type, Application, End-Use, Product Type, and Region

By Region

North America (By Type, Application, End-Use, Product Type, and Country)

United States

Canada

Mexico

Europe (By Type, Application, End-Use, Product Type, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Type, Application, End-Use, Product Type, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Type, Application, End-Use, Product Type, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Type, Application, End-Use, Product Type, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, Ongoing, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

India Maternal Health Monitoring Market Size, Share, Trends, 2033

India Maternal Health Monitoring market size is valued at USD 416.0 million in 2025 and is projected to reach USD 834.4 million in 2033, at a CAGR of 9.1% from 2026 to 2033

India Maternal Health Monitoring Market, India Maternal Health Monitoring Market Size, India Maternal Health Monitoring Market Share, India Maternal Health Monitoring Market Analysis, India Maternal Health Monitoring Market Growth, India Maternal Health Monitoring Market Trends, India Maternal Health Monitoring Market Research Report, India Maternal Health Monitoring Market Forecast, India Maternal Health Monitoring, India Maternal Health Monitoring Market Research, India Maternal Health Monitoring Industry, India Maternal Health Monitoring Industry Report, India Maternal Health Monitoring Market Data, India Maternal Health Monitoring Statistics, India Maternal Health Monitoring Market Statistics, India Maternal Health Monitoring Industry Trends, India Maternal Health Monitoring Market Report, India Maternal Health Monitoring Market Trends, India Maternal Health Monitoring Market News, India Maternal Health Monitoring Forecasts, India Maternal Health Monitoring Market Intelligence Report

Global Anaerobic Incubators market size is valued at USD 177.5 million in 2025 and is projected to reach USD 323.6 million in 2033, at a CAGR of 7.8% from 2026 to 2033

Thoracolumbar Posterior Fixation Systems Market Size, Share, Trends, 2033

Global Thoracolumbar Posterior Fixation Systems market size is valued at USD 875.8 million in 2025 and is projected to reach USD 1,526.6 million in 2033, at a CAGR of 7.2% from 2026 to 2033

Thoracolumbar Posterior Fixation Systems Market, Thoracolumbar Posterior Fixation Systems Market Size, Thoracolumbar Posterior Fixation Systems Market Share, Thoracolumbar Posterior Fixation Systems Market Analysis, Thoracolumbar Posterior Fixation Systems Market Growth, Thoracolumbar Posterior Fixation Systems Market Trends, Thoracolumbar Posterior Fixation Systems Market Research Report, Thoracolumbar Posterior Fixation Systems Market Forecast, Thoracolumbar Posterior Fixation Systems, Thoracolumbar Posterior Fixation Systems Market Research, Thoracolumbar Posterior Fixation Systems Industry, Thoracolumbar Posterior Fixation Systems Industry Report, Thoracolumbar Posterior Fixation Systems Market Data, Thoracolumbar Posterior Fixation Systems Statistics, Thoracolumbar Posterior Fixation Systems Market Statistics, Thoracolumbar Posterior Fixation Systems Industry Trends, Thoracolumbar Posterior Fixation Systems Market Report, Thoracolumbar Posterior Fixation Systems Market Trends, Thoracolumbar Posterior Fixation Systems Market News, Thoracolumbar Posterior Fixation Systems Forecasts, Thoracolumbar Posterior Fixation Systems Market Intelligence Report

Global Cranial Perforator market size is valued at USD 125.6 million in 2025 and is projected to reach USD 192.6 million in 2033, at a CAGR of 5.5% from 2026 to 2033