Surgical 3D Printing Market Size, Share, By Component (Equipment, Materials, Services & Software), By Application (External Wearable Devices, Tissue Engineering, Implants, and Clinical Study Devices), By Technology (Electronic Beam Melting (EBM), Laser Beam Melting, Photopolymerization, Droplet Deposition (DD), and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-2298

Published

February 3, 2026

Pages

312 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Definition

3D Printing medical system is based on a patient's imaging data.Medical devices that are printed at the point of care include patient-matched anatomical models, prosthetics, and surgical guides, which are used to guide surgeons during an operation.

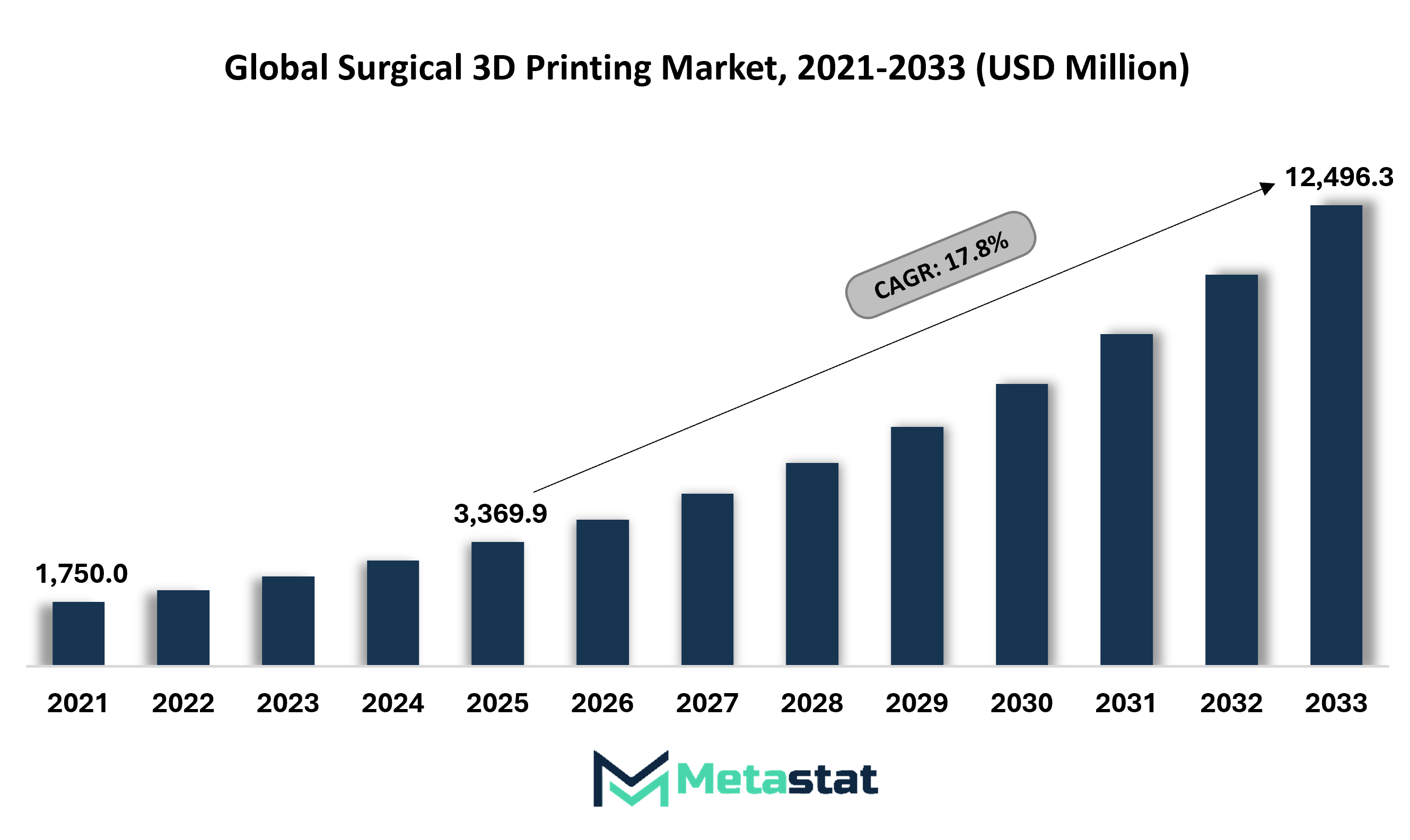

Global Surgical 3D Printing market size is valued at USD 3369.9 million in 2025 and projected to grow at a CAGR of 17.8% during the forecast period, reaching USD 12496.3 million by 2033

Market Dynamics

Technological advancements in surgical 3D printing is a key driving factor of the market. Companies are focusing on developing advanced and innovative 3D printing system for surgery. For instance, Anatomics has designed and developed world-first 3D printed titanium sternum and rib implant for the patient in suffering from cancer in the chest.The customizable implant can be adjusted to fit into the affected area and secured in place with screws. The people suffering from sarcoma use 3D printed titanium sternum and rib implant.Sarcoma cancer occurs in bone, cartilage, fat, muscle, vascular, or hematopoietic tissues. Further, TRUMPF has offered TRUMPF 3D printer to produce craniomaxillofacial implants. The surgeon use TRUMPF 3D printer to cut the craniomaxillofacial implant from perforated titanium plate during the procedure and then shape it to the size. Additionally, Renovis Surgical has introduced3D-printed Posterior Lumbar Interbody Fusion Systems. The company has received 510(k) clearance from the U.S. Food and Drug Administration (FDA) to market posterior lumbar Tesera porous titanium interbody fusion systems. However, the high cost associated with surgical 3D printing might hamper market growth. The cost of the standard 3D printing material varies by process from approximately $25 per kilogram for FDM filaments, to $50-60 per kilogram of SLA resin. Larger parts of the 3D printed system need more material and will take longer to print, which leads to increasing cost. Moreover, Rising investment and funding for surgical 3D printing would provide lucrative opportunities for the market in the coming years.

Market Segmentation

The global surgical 3D printing market is mainly classified based on technology, component, and application. Technology is further segmented into Electronic Beam Melting (EBM), Laser Beam Melting, Photopolymerization, Droplet Deposition (DD), and Others. By component, the market is divided into Equipment, Materials, and Services & Software. By application, the market is further divided into External Wearable Devices, Tissue Engineering, Implants, and Clinical Study Devices.

Equipment segment is valued at USD 688.8 million in 2026 and is projected to reach USD 2249.3 million by 2033, at a CAGR of 18.4% during the forecast period.

Based on technology, Photopolymerization was dominating the global surgical 3D printing market in 2019, owing to the widespread application of photopolymerization technology across various medical applications such as for manufacturing surgical guides including orthopedic, dental, and CMF guides; prosthetics and implants; porous scaffolds; and dental restorations.

External Wearable Devices segment is projected to reach USD 7210.4 million by 2033, at a CAGR of 16.4% during the forecast period.

The partnership between companies to extend the range of applications for surgical 3D printing system is driving the market demand. For instance, Structo, a dental 3D printing solutions provider and the manufacturer has partnered with German 3D printing materials company, pro3dure. The partnership will help Velox users gain access to pro3dure’s range of dental 3D printing materials.Velox is an all-in-one desktop 3D printer with autonomous post-processing aimed at spearheading the adoption of 3D printing in dental practices.pro3dure manufactures various photopolymer materials for dental, audiology and medical applications.

Regional Analysis

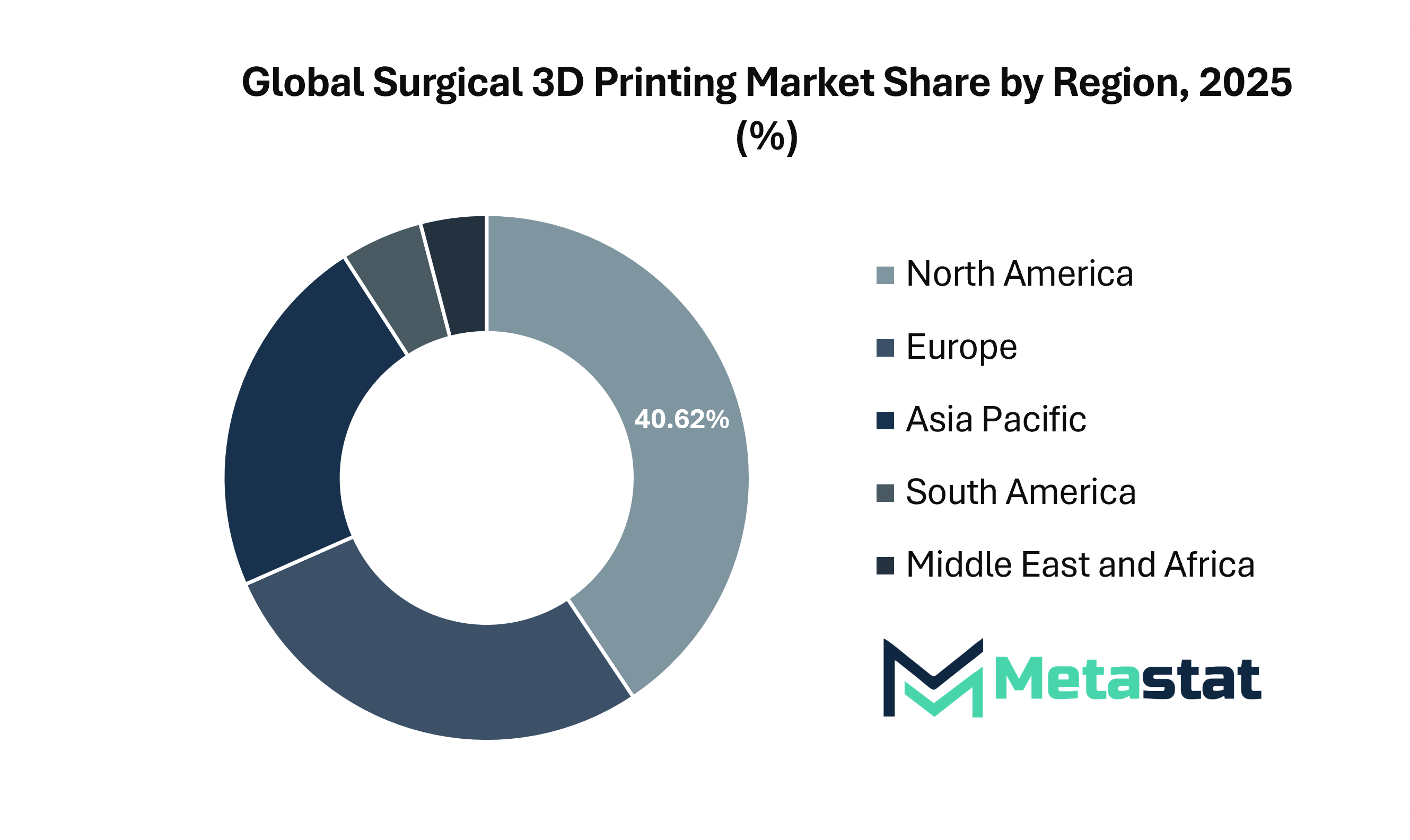

Based on geography, the global surgical 3D printing market is divided into North America, Europe, Asia-Pacific, South America, and Middle East & Africa. North America is further divided in the U.S., Canada, and Mexico, whereas Europe consists of the UK, Germany, France, Italy, and Rest of Europe. Asia-Pacific is segmented into India, China, Japan, South Korea, and Rest of Asia-Pacific. The South America region includes Brazil, Argentina, and the Rest of South America, while the Middle East & Africa is categorized into GCC Countries, Egypt, South Africa, and Rest of Middle East & Africa.

North America was dominating the global surgical 3D printing market in 2019, due to the commercialization of regulatory approved surgical 3D printing system, rising investment and expanding the development facility for the surgical 3D printing system, and strategic collaboration between companies to develop surgical 3D printing system. For instance, GE Healthcare has collaborated with Formlabs, a Massachusetts-based manufacturer of advanced 3D-printers that can help clinicians quickly print anatomical models at the point of care. These models visualize patient anatomy and disease for improved communication within the medical team, case-based teaching models and enhanced patient education.

Competitive landscape

Key players operating in the surgical 3D printing industry include 3D Systems Corporation, Stratasys Ltd., Envisiontec GmbH, Renishaw plc, Materialise NV, 3T Additive Manufacturing Ltd., Arcam AB, EOS GmbH Electro Optical Systems, Prodways Group, and Concept Laser GmbH.

The companies are commercializing technologically advanced surgical 3D printing system, the partnership between companies to develop 3D printing system for the medical industry, rising investment, facility expansion to manufacture 3D printing system for medical applications, and regulatory approval of surgical 3D printing system are some of the strategies adopted by the major companies. For instance, Materialise NV, a leading company in 3D technology solutions has received CE Marking Certification for its personalized orthopaedic and cranio-maxillofacial (CMF) solutions, which includes 3D-printed anatomical models and patient-matched surgical guides and implants. Materialise is one of the first company to acquire CE certification for personalized, 3D-printed medical device portfolio. The CE approval will make the technology more accessible for surgeons.

India Maternal Health Monitoring Market Size, Share, Trends, 2033

India Maternal Health Monitoring market size is valued at USD 416.0 million in 2025 and is projected to reach USD 834.4 million in 2033, at a CAGR of 9.1% from 2026 to 2033

India Maternal Health Monitoring Market, India Maternal Health Monitoring Market Size, India Maternal Health Monitoring Market Share, India Maternal Health Monitoring Market Analysis, India Maternal Health Monitoring Market Growth, India Maternal Health Monitoring Market Trends, India Maternal Health Monitoring Market Research Report, India Maternal Health Monitoring Market Forecast, India Maternal Health Monitoring, India Maternal Health Monitoring Market Research, India Maternal Health Monitoring Industry, India Maternal Health Monitoring Industry Report, India Maternal Health Monitoring Market Data, India Maternal Health Monitoring Statistics, India Maternal Health Monitoring Market Statistics, India Maternal Health Monitoring Industry Trends, India Maternal Health Monitoring Market Report, India Maternal Health Monitoring Market Trends, India Maternal Health Monitoring Market News, India Maternal Health Monitoring Forecasts, India Maternal Health Monitoring Market Intelligence Report

Global Anaerobic Incubators market size is valued at USD 177.5 million in 2025 and is projected to reach USD 323.6 million in 2033, at a CAGR of 7.8% from 2026 to 2033

Global Radiochemical Synthesizers market size is valued at USD 450.5 million in 2025 and is projected to reach USD 746.6 million in 2033, at a CAGR of 6.7% from 2026 to 2033.

Global Radiochemical Synthesizers Market, Global Radiochemical Synthesizers Market Size, Global Radiochemical Synthesizers Market Share, Global Radiochemical Synthesizers Market Analysis, Global Radiochemical Synthesizers Market Growth, Global Radiochemical Synthesizers Market Trends, Global Radiochemical Synthesizers Market Research Report, Global Radiochemical Synthesizers Market Forecast, Global Radiochemical Synthesizers, Global Radiochemical Synthesizers Market Research, Global Radiochemical Synthesizers Industry, Global Radiochemical Synthesizers Industry Report, Global Radiochemical Synthesizers Market Data, Global Radiochemical Synthesizers Statistics, Global Radiochemical Synthesizers Market Statistics, Global Radiochemical Synthesizers Industry Trends, Global Radiochemical Synthesizers Market Report, Global Radiochemical Synthesizers Market Trends, Global Radiochemical Synthesizers Market News, Global Radiochemical Synthesizers Forecasts, Global Radiochemical Synthesizers Market Intelligence Report

Thoracolumbar Posterior Fixation Systems Market Size, Share, Trends, 2033

Global Thoracolumbar Posterior Fixation Systems market size is valued at USD 875.8 million in 2025 and is projected to reach USD 1,526.6 million in 2033, at a CAGR of 7.2% from 2026 to 2033

Thoracolumbar Posterior Fixation Systems Market, Thoracolumbar Posterior Fixation Systems Market Size, Thoracolumbar Posterior Fixation Systems Market Share, Thoracolumbar Posterior Fixation Systems Market Analysis, Thoracolumbar Posterior Fixation Systems Market Growth, Thoracolumbar Posterior Fixation Systems Market Trends, Thoracolumbar Posterior Fixation Systems Market Research Report, Thoracolumbar Posterior Fixation Systems Market Forecast, Thoracolumbar Posterior Fixation Systems, Thoracolumbar Posterior Fixation Systems Market Research, Thoracolumbar Posterior Fixation Systems Industry, Thoracolumbar Posterior Fixation Systems Industry Report, Thoracolumbar Posterior Fixation Systems Market Data, Thoracolumbar Posterior Fixation Systems Statistics, Thoracolumbar Posterior Fixation Systems Market Statistics, Thoracolumbar Posterior Fixation Systems Industry Trends, Thoracolumbar Posterior Fixation Systems Market Report, Thoracolumbar Posterior Fixation Systems Market Trends, Thoracolumbar Posterior Fixation Systems Market News, Thoracolumbar Posterior Fixation Systems Forecasts, Thoracolumbar Posterior Fixation Systems Market Intelligence Report