India Affordable Housing Finance Market Size, Share, By Providers (Government, Private Builders, and Public-Private Partnership ), By Income Category (EWS, LIG, and MIG), By Location (Metro and Non-Metro), By Population (Slum Population and Non-Slum Population), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4638

Published

April 17, 2026

Pages

320 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

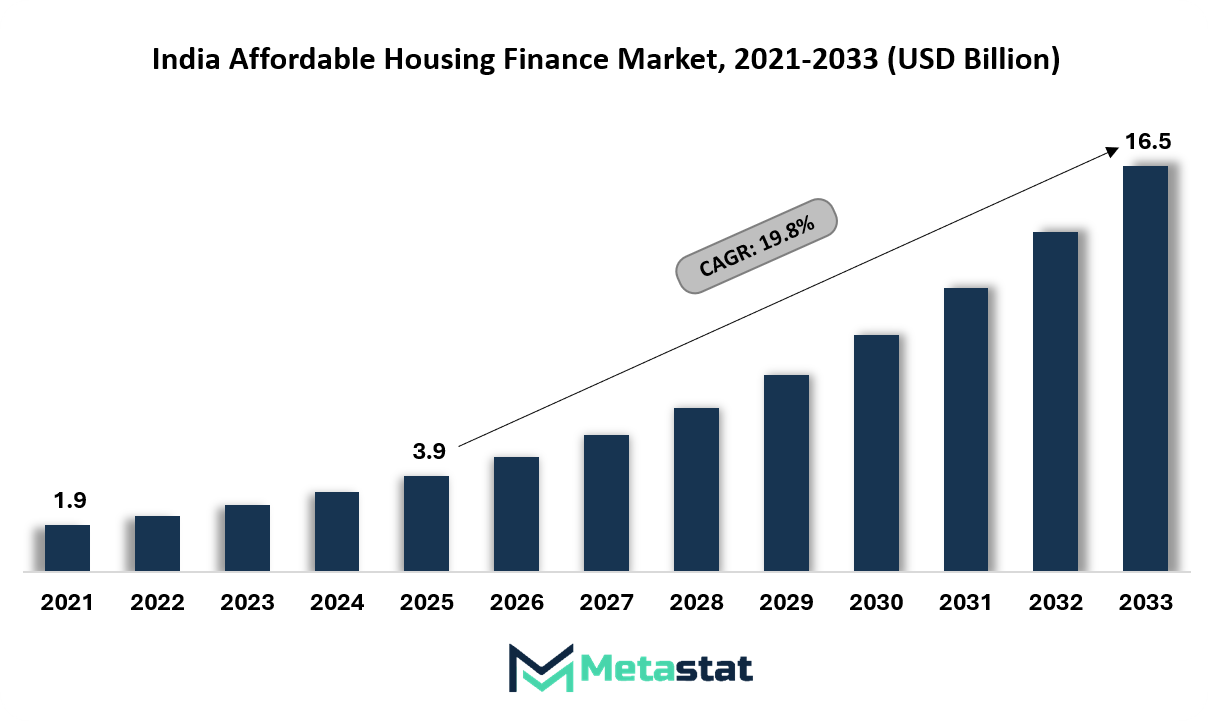

India Affordable Housing Finance market size is valued at USD 3.9 billion in 2025 and projected to grow at a CAGR of 19.8% during the forecast period, reaching USD 16.5 billion by 2033.

India Affordable Housing Finance Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Government segment accounted for 36.0% of the India Affordable Housing Finance market in 2025.

Key trends driving growth: Government-backed subsidies and housing schemes increasing access to low-cost home financing, Rapid urbanization and rising housing demand among middle- and lower-income populations.

Opportunities include expansion of digital lending platforms and fintech integration improving credit access and underwriting efficiency.

Key insight: India Affordable Housing Finance market is expanding rapidly on the back of urban migration, policy-backed credit support, and rising demand from low- and middle-income households, with the segment already accounting for nearly one-third of total housing loans.

India Affordable Housing Finance market is witnessing steady expansion supported by policy-led lending initiatives, rising housing demand among low- and middle-income households, and stronger participation from specialized housing finance institutions. The market is advancing through structured credit frameworks designed to improve home ownership across urban, semi-urban, and emerging residential locations. Government subsidy programs and targeted affordable housing schemes are improving access to formal financing, particularly for economically weaker sections and lower-income borrowers. Lenders are refining loan products in line with borrower affordability, supporting wider mortgage penetration across underserved customer groups.

Urban population expansion, continued migration toward employment hubs, and stronger financial inclusion efforts are reshaping demand across the India Affordable Housing Finance market. Credit-linked support programs, digital onboarding models, and improved borrower assessment tools are strengthening loan accessibility and supporting faster disbursement cycles. The market is also moving toward a broader lending ecosystem in which digital verification, alternative credit evaluation, and data-led underwriting are improving access for borrowers with informal or variable income patterns.

Market Dynamics

Growth Drivers:

Government-backed subsidies and housing schemes increasing access to low-cost home financing.

India Affordable Housing Finance market will maintain strong momentum supported by subsidy-linked housing programs and policy measures focused on expanding home ownership among economically weaker and lower-income households. These initiatives are improving affordability, strengthening borrower confidence, and encouraging deeper participation from housing finance companies and banks. Continued institutional support is helping formal credit reach semi-urban and rural markets with greater consistency.

Rapid urbanization and rising housing demand among middle- and lower-income populations

India Affordable Housing Finance market will expand steadily with continued urbanization and increasing housing demand from middle- and lower-income households. Rising aspirations for home ownership, combined with the expansion of affordable residential supply, are supporting first-time borrowing activity across major and emerging cities. Lenders are aligning products with evolving income patterns and repayment capacity, which is improving accessibility across wider borrower categories.

Restraints and Challenges:

High credit risk and informal income structures limiting borrower eligibility

India Affordable Housing Finance market continues to face pressure from high credit risk linked to informal income patterns and limited financial documentation among target borrowers. Credit assessment remains challenging in customer groups with variable cash flows, thin credit histories, and lower formal banking penetration. These conditions restrict loan eligibility and keep approval rates uneven across several borrower segments.

Regulatory complexities and lengthy approval processes impacting loan disbursement

India Affordable Housing Finance market is also affected by documentation intensity, regulatory compliance requirements, and lengthy approval procedures that slow the lending cycle. Extended processing timelines reduce borrower convenience and create operational inefficiencies for financial institutions. Faster execution and streamlined approval systems remain important for improving customer experience and sustaining competitive loan origination.

Opportunities:

Expansion of digital lending platforms and fintech integration improving credit access and underwriting efficiency

India Affordable Housing Finance market holds strong opportunity through the expansion of digital lending platforms, fintech partnerships, and technology-led underwriting systems. Digital verification tools, analytics-based credit screening, and alternative data assessment models are improving lender efficiency and supporting broader borrower inclusion. These capabilities are particularly valuable in serving applicants with informal income profiles and limited traditional credit records.

Market Segmentation Analysis

The India Affordable Housing Finance market is classified based on Providers, Income Category, Location, and Population.

By Providers, the market is further segmented into:

Government

Government segment is valued at USD 1.7 billion in 2026 and is projected to reach USD 5.5 billion by 2033, at a CAGR of 18.4% during the forecast period.

Government segment in India Affordable Housing Finance market is strengthening through interest subsidy programs, credit-linked support measures, and policy-backed housing initiatives aimed at improving access to formal home financing. Public support mechanisms are helping lower the effective borrowing burden for economically weaker and lower-income households. Continued focus on affordable housing development is supporting wider mortgage adoption across urban and semi-urban locations.

Private Builders

Private Builders segment is valued at USD 1.9 billion in 2026 and is projected to reach USD 7.3 billion by 2033, at a CAGR of 20.9% during the forecast period.

Private Builders segment in India Affordable Housing Finance market is gaining importance through the expansion of developer-led affordable projects, compact housing formats, and financing alignment with end-user affordability. Collaboration between private developers and lenders is supporting smoother home purchase financing and improving access for first-time buyers. Growing project activity in emerging residential clusters is also supporting segment expansion.

Public-Private Partnership

Public-Private Partnership segment is valued at USD 1 billion in 2026 and is projected to reach USD 3.7 billion by 2033, at a CAGR of 19.9% during the forecast period.

Public-Private Partnership segment in India Affordable Housing Finance market is developing through shared investment structures that combine public policy support with private sector execution. These models improve project feasibility, support affordable housing supply creation, and strengthen financing access across income-sensitive borrower groups. Greater coordination between government agencies, developers, and lenders is helping accelerate delivery across high-demand housing corridors.

By Income Category, the market is divided into:

EWS

EWS segment is projected to reach USD 5.7 billion by 2033, at a CAGR of 21.9% during the forecast period.

EWS segment is advancing through targeted subsidy support, lower-ticket home loans, and inclusion-focused financing initiatives designed for economically weaker households. Simplified eligibility assessment and focused housing schemes are improving access to ownership-based financing for low-income borrowers. Expansion of formal credit access in this segment is supporting higher participation across dense urban and peripheral housing markets.

LIG

LIG segment is projected to reach USD 7.3 billion by 2033, at a CAGR of 19.5% during the forecast period.

LIG segment is recording steady progression supported by improving credit awareness, structured repayment options, and increased availability of affordable housing units. Financial institutions are broadening loan accessibility through longer tenures, flexible installment structures, and competitive interest offerings. Strong borrower demand from salaried and semi-formal working households is supporting this segment across urban and semi-urban regions.

MIG

MIG segment is projected to reach USD 3.6 billion by 2033, at a CAGR of 17.6% during the forecast period.

MIG segment is expanding through rising disposable income, growing preference for formal housing finance, and wider adoption of digital loan processing systems. Competitive mortgage offerings and improved credit evaluation practices are supporting both new home purchases and housing upgrades within middle-income communities. Stronger lender competition in organized housing finance is also improving service quality for this segment.

By Location, the market is further divided into:

Metro

Metro segment is projected to reach USD 8.6 billion by 2033.

Metro segment is witnessing structured growth supported by high population density, sustained housing demand, and the continued expansion of vertical residential development. Financing activity remains strong in metropolitan centers where property demand, employment concentration, and formal credit access are well established. Lenders are increasingly using digital processing and faster evaluation systems to manage volume-intensive mortgage demand in these cities.

Non-Metro

Non-Metro segment is projected to reach USD 7.9 billion by 2033.

Non-Metro segment is gaining traction with improving infrastructure, rising regional connectivity, and relatively lower residential property prices. Expansion of housing finance networks beyond major cities is supporting wider borrower access and encouraging first-time ownership across tier 2 and tier 3 locations. Affordable project development and stronger local lending presence are supporting long-term growth across these markets.

By Population, the India Affordable Housing Finance market is divided as:

Slum Population

Slum Population segment is projected to grow at a CAGR of 21.3% during the forecast period.

Slum Population segment is influenced by rehabilitation schemes, formal housing transition programs, and targeted financial inclusion efforts aimed at improving residential stability. Structured lending support linked with redevelopment and subsidized housing initiatives is helping move households toward formal ownership opportunities. Financing models in this segment are increasingly tied to social housing programs and government-backed redevelopment mechanisms.

Non-Slum Population

Non-Slum Population segment is projected to grow at a CAGR of 19.2% during the forecast period.

Non-Slum Population segment continues to expand with stronger housing awareness, improving access to organized mortgage products, and rising preference for planned residential ownership. Stable employment patterns and better financial literacy are supporting loan adoption across a broader borrower base. Continued project availability and lender outreach are strengthening growth across this segment in both urban and non-metro markets.

Competitive Landscape and Strategic Insights

India Affordable Housing Finance market will continue to expand steadily, supported by rising urban housing demand and a stronger focus on financial inclusion. A large number of households are seeking access to formal housing credit across semi-urban and rural areas, where conventional banking penetration has remained limited. Lenders are responding by simplifying loan processes, strengthening distribution reach, and designing products aligned with the income patterns of first-time homebuyers. This shift is supporting the movement from informal borrowing toward structured financing, improving stability for both borrowers and lending institutions.

A major feature shaping the competitive landscape is the presence of housing finance companies serving diverse borrower categories across the country. Large institutions and specialized lenders are both expanding their presence to capture underserved demand. Companies such as LIC Housing Finance Limited and Bajaj Housing Finance Limited will retain strength through scale and brand credibility, while Aavas Financiers Limited and Aptus Value Housing Finance India Limited will strengthen their position in underpenetrated markets. Piramal Capital & Housing Finance Limited and PNB Housing Finance Limited will refine their portfolios to maintain a balanced approach toward risk and growth.

Other important participants, including Tata Capital Housing Finance Limited, Can Fin Homes Limited, and Aditya Birla Housing Finance Limited, will continue to support market competitiveness through pricing discipline and service quality. Institutions such as ICICI Home Finance Company Limited and IIFL Home Finance Limited will strengthen their digital capabilities, making loan approvals faster and more accessible. In parallel, Aadhar Housing Finance Limited and Home First Finance Company India Limited will maintain focus on borrowers with limited credit history, supporting broader participation in organized housing finance.

Emerging and region-focused lenders such as India Shelter Finance Corporation Limited, Shubham Housing Development Finance Company Limited, and Grihum Housing Finance Limited will strengthen their presence through localized expansion strategies. Mahindra Rural Housing Finance Limited, MAS Rural Housing & Mortgage Finance Limited, and Vastu Housing Finance Corporation Limited will continue to focus on rural and lower-income borrower groups. At the same time, Muthoot Homefin India Limited, Hinduja Housing Finance Limited, India Home Loan Limited, Niwas Housing Finance Limited, SAVE Housing Finance Limited, IKF Home Finance Limited, and Easy Home Finance Limited will continue to build niche strength through targeted product offerings and region-specific outreach.

Forecast and Future Outlook

Market size is forecast to rise from USD 3.9 billion in 2025 to over USD 16.5 billion by 2033.

India Affordable Housing Finance market is set for sustained expansion, supported by policy-led housing promotion, wider adoption of digital lending infrastructure, and continued improvement in borrower inclusion. Financial institutions are expected to strengthen underwriting systems to better serve applicants with informal income profiles and limited credit histories. Expansion of affordable housing supply, combined with improving credit delivery mechanisms, will continue to support long-term market development across diverse income categories.

Affordable Housing Finance Market Key Segments:

By Providers:

Government

Private Builders

Public-Private Partnership

By Income Category:

EWS

LIG

MIG

By Location:

Metro

Non-Metro

By Population:

Slum Population

Non-Slum Population

Key India Affordable Housing Finance Industry Players

This research report categorizes the India Affordable Housing Finance market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the India Affordable Housing Finance market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the India Affordable Housing Finance market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 19.8% from 2026 to 2033

Revenue Unit

USD billion

Segmentation

By Providers, Income Category, Location and Population

By Providers

Government

Private Builders

Public-Private Partnership

By Income Category

EWS

LIG

MIG

By Location

Metro

Non-Metro

By Population

Slum Population

Non-Slum Population

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Prepositions of Leading Market Players

Australia Parametric Insurance Market Size, Share, Trends, 2033

Australia Parametric Insurance market size is valued at USD 286.4 million in 2025 and is projected to reach USD 720.9 million in 2033, at a CAGR of 12.2% from 2026 to 2033.

Australia Parametric Insurance Market, Australia Parametric Insurance Market Size, Australia Parametric Insurance Market Share, Australia Parametric Insurance Market Analysis, Australia Parametric Insurance Market Growth, Australia Parametric Insurance Market Trends, Australia Parametric Insurance Market Research Report, Australia Parametric Insurance Market Forecast, Australia Parametric Insurance, Australia Parametric Insurance Market Research, Australia Parametric Insurance Industry, Australia Parametric Insurance Industry Report, Australia Parametric Insurance Market Data, Australia Parametric Insurance Statistics, Australia Parametric Insurance Market Statistics, Australia Parametric Insurance Industry Trends, Australia Parametric Insurance Market Report, Australia Parametric Insurance Market Trends, Australia Parametric Insurance Market News, Australia Parametric Insurance Forecasts, Australia Parametric Insurance Market Intelligence Report

Merchant Banking Services market size is valued at USD 68.3 billion in 2025 and is projected to reach USD 260.7 billion in 2033, at a CAGR of 18.3% from 2026 to 2033.

Global Debt Management Solutions market size is valued at USD 41.8 billion in 2025 and is projected to reach USD 72.8 billion in 2033, at a CAGR of 7.2% from 2026 to 2033

The Global Affordable Housing Finance market size was USD 347.7 billion in 2025 and is projected to reach USD 653.2 billion in 2033, at a CAGR of 8.2% from 2026 to 2033