Food Quality and Safety Testing Market Size, Share, By Type (Microbiological Testing, Allergen Testing, Chemical Contaminants Testing, Pesticide Residue Testing, Veterinary Drug, Antibiotic Residue Testing, Mycotoxin Testing, Heavy Metals Testing, GMO Testing, Nutritional, Label Claim Verification Testing, and Others), By End User (Food Manufacturers, Beverage Manufacturers, Dairy Processors, Meat Poultry, Seafood Processors, Bakery, Confectionery Producers, Infant Nutrition, Specialized Nutrition Producers, Ingredient, Additive Suppliers, Retailers, Private Label Brand Owners, Foodservice Chains and Central Kitchens, Government, Regulatory Agencies, Certification Bodies, and Audit Firms, and Others), By Food Type (Meat, Poultry, Seafood, Dairy Products, Processed Foods, Fruits, Vegetables, and Others), By Technology (Traditional and Rapid), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4632

Published

April 16, 2026

Pages

324 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

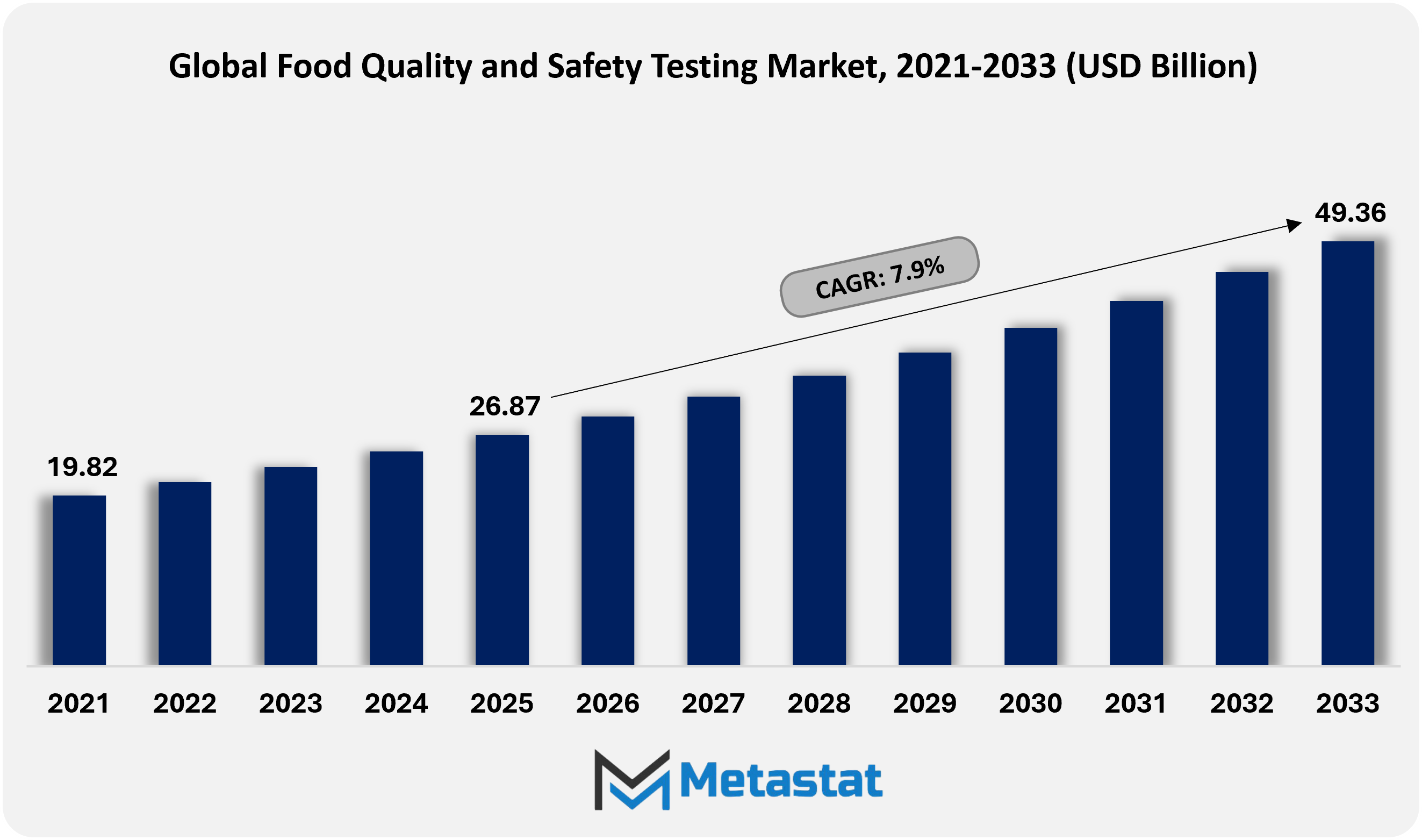

The global Food Quality and Safety Testing market size was valued at USD 26.9 billion in 2025 and is projected to grow at a CAGR of 7.9% during 2026 to 2033, reaching USD 49.4 billion by 2033.

Global Food Quality and Safety Testing Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

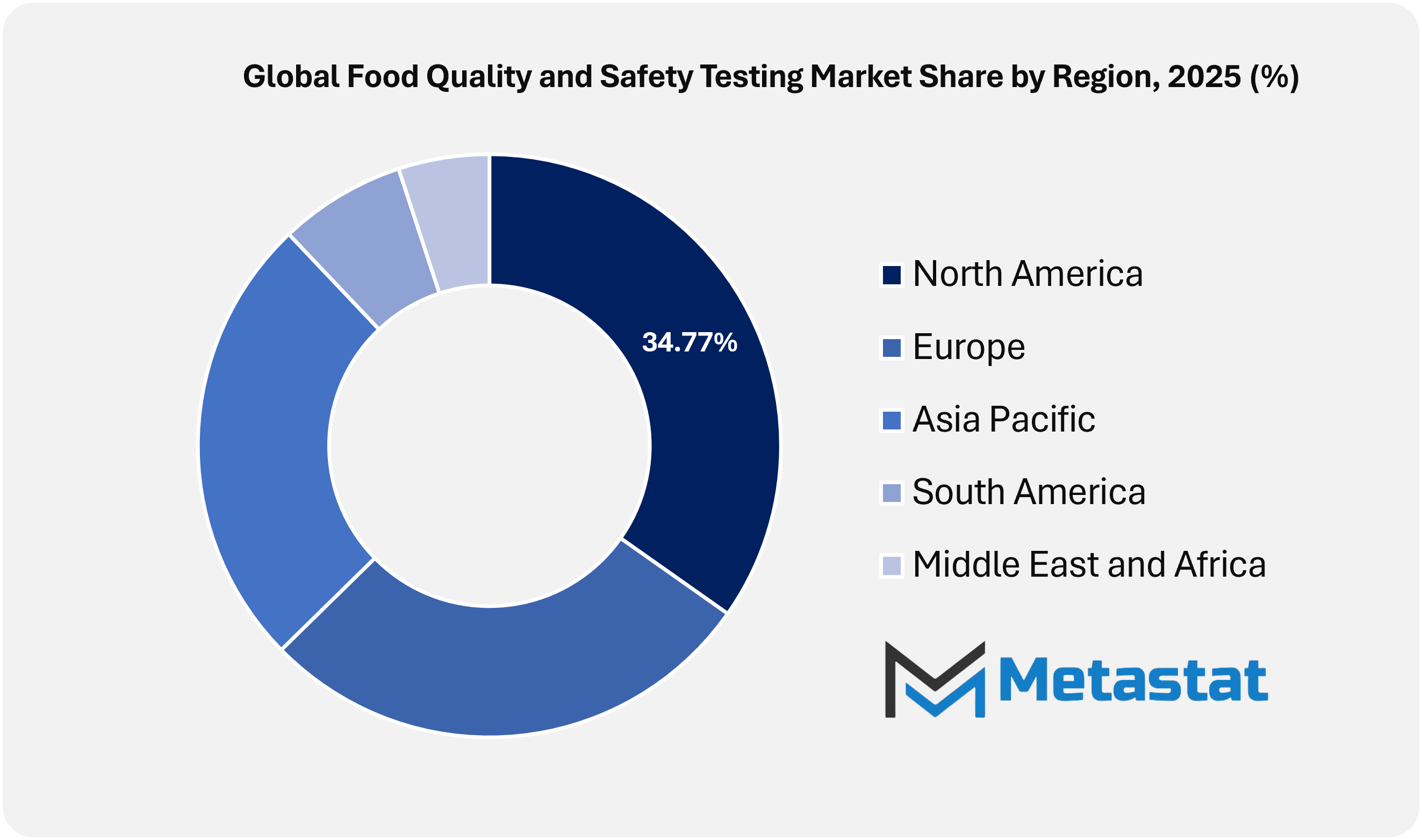

North America accounted for 34.8% in 2025, led by the United States.

Key trends driving growth include escalating foodborne illness incidents heightening regulatory scrutiny across supply chains and expansion of global food trade increasing demand for standardized testing protocols.

Key insight: Stricter regulations and globalized food supply networks are transforming food quality and safety testing into a compliance-driven, technology-intensive market.

The global food quality and safety testing industry is moving beyond laboratory verification into a phase where assurance will be embedded throughout food value chains rather than distributed at isolated checkpoints. Testing activity increasingly serves as a continuous intelligence layer, shaping decisions from raw material sourcing to post-consumption monitoring. Data reliability will become the central currency, with testing results expected to influence procurement contracts, insurance frameworks, and cross-border trade negotiations rather than serving compliance purposes alone.

Future operations will be shaped by the convergence between analytical science and digital traceability. Testing providers will integrate genomic screening, chemical fingerprinting and predictive analytics into integrated validation systems, allowing contamination risks to be predicted rather than discovered retrospectively. Laboratories no longer function as passive service units. They will act as custodians of trusted datasets that manufacturers, regulators, and retailers rely on for rapid intervention and dispute resolution. The industry will align testing protocols more closely with real-world consumption patterns, addressing cumulative exposure and interaction effects rather than individual limits.

Market Dynamics

Growth Drivers:

Escalating foodborne illness incidents heightening regulatory scrutiny across supply chains.

Rising cases of contamination and food-related health concerns will intensify oversight across production, processing, and distribution networks. Regulatory authorities are likely to implement stricter compliance norms, prompting sustained investment in advanced verification techniques. Such pressure strengthens the role of the global Food Quality and Safety Testing market in risk mitigation and consumer protection.

Expansion of global food trade increasing demand for standardized testing protocols.

Global food trade continues to expand, supported by diversified sourcing and cross-border consumption patterns. Harmonized quality benchmarks gain significance in reducing trade disputes and shipment rejections. Standardized testing frameworks will register higher adoption, strengthening the global Food Quality and Safety Testing market through harmonized certification and consistent analytical validation.

Restraints and Challenges:

High testing costs limiting adoption among small and mid-sized food processors.

Advanced laboratory infrastructure, habitual compliance audits, and sophisticated analytical equipment will generate economic strain for smaller processors. Budget constraints will restrict frequent testing cycles, reducing penetration levels within cost-sensitive segments. Such obstacles will moderate short-term expansion, particularly across developing economies with fragmented food manufacturing ecosystems.

Limited skilled laboratory professionals slowing turnaround times in emerging regions.

The shortage of trained analysts and laboratory technicians will continue to impact operational efficiency. Delays in sample processing and result verification will reduce responsiveness across the food supply network. Emerging regions will face additional pressure to build technical expertise, without which testing scalability and service reliability will be hampered.

Opportunities:

Accelerated adoption of rapid testing kits and automation improving speed and accuracy.

Developments in technology will facilitate broader adoption of rapid diagnostic kits, sensors, and automated systems, supporting detection of pathogens and contamination risks across food products. This shall facilitate decision-making in different supply chains. Efficiency will create pathways of growth in the food quality and safety testing market.

Market Segmentation Analysis

The Global Food Quality and Safety Testing market is classified based on Type, End User, Food Type, and Technology.

By Type, the market is further segmented into:

Microbiological Testing

Microbiological Testing segment is estimated at USD 8.1 billion in 2026 and is projected to reach USD 13.5 billion by 2033, at a CAGR of 7.6% during the forecast period.

Microbiological testing in the global Food Quality and Safety Testing market benefits from increased relevance, owing to rising pathogen surveillance expectations across global supply networks. Advanced detection systems will aid early identification of bacterial infection, give a boost to preventive controls, and make stronger compliance alignment. Laboratory automation and data-driven reporting will raise consistency, accuracy, and traceability throughout meals categories.

Allergen Testing

Allergen Testing segment is estimated at USD 3.6 billion in 2026 and is projected to reach USD 6.5 billion by 2033, at a CAGR of 9% during the forecast period.

Allergen testing remains important for protecting consumer health and addressing brand risk in regulated food environments. Expanding allergen labelling mandates will encourage broader analytical coverage. Future testing frameworks will emphasize rapid validation, cross-contact prevention, and stronger sensitivity to protect vulnerable populations while supporting transparent ingredient disclosure across global markets.

Chemical Contaminants Testing

Chemical Contaminants Testing segment is estimated at USD 4 billion in 2026 and is projected to reach USD 6.8 billion by 2033, at a CAGR of 7.6% during the forecast period.

Chemical contaminants testing will register steady demand expansion, owing to industrial exposure, environmental residue concerns, and packaging interactions. Analytical platforms will support the detection of solvents, components, and processing by-products. Predictive monitoring fashions will assist food operators in retaining chemical thresholds while enhancing long-term compliance and product integrity.

Pesticide Residue Testing

Pesticide Residue Testing segment is estimated at USD 2.9 billion in 2026 and is projected to reach USD 5 billion by 2033, at a CAGR of 8% during the forecast period.

Pesticide residue testing will expand as global agricultural intensification and cross-border food trade increase. Regulatory tolerance limits will pressure consistent testing adoption across all product categories. High-throughput screening strategies will enhance identity accuracy at the same time as supporting sustainable farming verification, export readiness, and residue transparency in farmed food structures.

Veterinary Drug and Antibiotic Residue Testing

Veterinary Drug and Antibiotic Residue Testing segment is estimated at USD 2.6 billion in 2026 and is projected to reach USD 4.6 billion by 2033, at a CAGR of 8.4% during the forecast period.

Veterinary drug and antibiotic residue testing beef up food safety governance inside animal-derived product chains. Regulatory scrutiny tied to antimicrobial resistance will increase testing frequency. Advanced residue profiling will guide accountable farm animal practices, enhance export eligibility, and improve acceptance in protein-based meals distribution channels.

Mycotoxin Testing

Mycotoxin Testing segment is estimated at USD 2.3 billion in 2026 and is projected to reach USD 3.9 billion by 2033, at a CAGR of 7.7% during the forecast period.

The relevance of mycotoxin testing increases due to climate variability affecting fungal contamination patterns. The grain, nut, and feed segments will adopt expanded monitoring protocols. Predictive contamination modelling combined with sensitive analytical tests will support preventive risk management and quality assurance in climate-impacted food supply sectors.

Heavy Metals Testing

Heavy Metals Testing segment is estimated at USD 1.7 billion in 2026 and is projected to reach USD 2.8 billion by 2033, at a CAGR of 7.3% during the forecast period.

Heavy metals testing remains a priority due to the risks of soil erosion, water pollution, and industrial proximity. Testing laboratories will expand capabilities to detect lead, mercury, cadmium, and arsenic. Regulatory alignment and consumer awareness will support continued adoption across staple foods and processed product portfolios.

GMO Testing

GMO Testing segment is estimated at USD 1.4 billion in 2026 and is projected to reach USD 2.2 billion by 2033, at a CAGR of 6.6% during the forecast period.

GMO Testing continues to support regulatory disclosure and business compliance across various jurisdictions. Non-GMO labelling policies expand adoption across multiple food sectors. Molecular testing advances will increase identification accuracy while supporting seed traceability, product differentiation, and agricultural transparency in genetically monitored food systems.

Nutritional and Label Claim Verification Testing

Nutritional and Label Claim Verification Testing segment is estimated at USD 1.5 billion in 2026 and is projected to reach USD 2.6 billion by 2033, at a CAGR of 8.6% during the forecast period.

Nutrition and label claim verification testing will continue to grow due to the increasing demand for nutritional accuracy and functional food transparency. Analytical validation will support protein, vitamin, mineral and calorie claims. Regulatory oversight will encourage accurate nutrient quantification while strengthening consumer confidence and marketing accountability.

Others

Others segment is estimated at USD 0.9 billion in 2026 and is projected to reach USD 1.4 billion by 2033, at a CAGR of 7.5% during the forecast period.

Additional test categories address emerging contaminants, packaging migration risks, and novel ingredient safety validation. Innovation-driven food formats will require adaptive testing frameworks. Laboratories will expand the service portfolio to keep pace with emerging dietary trends, alternative proteins, and regulatory foresight initiatives.

By End User, the market is divided into:

Food Manufacturers

Food Manufacturers segment is projected to reach USD 13.5 billion by 2033, at a CAGR of 7.6% during the forecast period.

Food manufacturers represent sustained demand drivers, owing to complex processing operations and multi-ingredient formulations. Preventive trying out techniques may be incorporated into manufacturing cycles. Digital quality management systems will support continuous compliance, batch verification, and risk prediction across global manufacturing footprints.

Beverage Manufacturers

Beverage Manufacturers segment is projected to reach USD 5.7 billion by 2033, at a CAGR of 7.5% during the forecast period.

Beverage producers prioritize trying out related to water quality, additive stability, and microbial safety. Product diversification into functional and fortified drinks will increase analytical monitoring. Rapid testing integration will support shelf-life validation, export compliance, and flavour consistency management.

Dairy Processors

Dairy Processors segment is projected to reach USD 4.7 billion by 2033, at a CAGR of 7.3% during the forecast period.

Dairy processors will depend on pathogen control, tracking for antibiotic residues, and widespread testing for nutritional consistency. Cold-chain sensitivity will encourage real-time exceptional verification. Advanced trying out workflows will support product safety in the liquid milk, fermented products, and powdered dairy segments.

Meat Poultry and Seafood Processors

Meat Poultry and Seafood Processors segment is projected to reach USD 6 billion by 2033, at a CAGR of 8% during the forecast period.

Meat, poultry, and seafood processors will face increased testing requirements, owing to higher contamination risk exposure. Pathogen detection and residue evaluation will dominate safety priorities. Automation-pushed laboratories will help with faster turnaround, regulatory alignment, and export certification reliability.

Bakery and Confectionery Producers

Bakery and Confectionery Producers segment is projected to reach USD 3.8 billion by 2033, at a CAGR of 7.4% during the forecast period.

Bakery and confectionery producers will emphasize allergen verification and ingredient balance, trying out. Complex formulations and cross-contact risks will increase analytical oversight. Shelf-balance evaluation and labelling accuracy will assist compliance in extensive manufacturing environments.

Infant Nutrition and Specialized Nutrition Producers

Infant Nutrition and Specialized Nutrition Producers segment is projected to reach USD 3.3 billion by 2033, at a CAGR of 9.2% during the forecast period.

Owing to sensitive consumer groups, infant nutrition and specialty nutrition producers will maintain stringent testing standards. Nutritional precision and exclusion of contaminants will remain central priorities. Advanced analytical validation will support regulatory approval and caregiver confidence in specific feeding solutions.

Ingredient and Additive Suppliers

Ingredient and Additive Suppliers segment is projected to reach USD 4 billion by 2033, at a CAGR of 8.2% during the forecast period.

Ingredient and additive suppliers will invest in purity testing and functional validation. Supply chain transparency requirements will intensify analytical documentation. Testing integration will support formulation compatibility, traceability assurance, and long-term supplier reliability across manufacturing partnerships.

Retailers and Private Label Brand Owners

Retailers and Private Label Brand Owners segment is projected to reach USD 3.7 billion by 2033, at a CAGR of 8.6% during the forecast period.

Retailers and private label brand owners will expand testing oversight to protect brand reputation and regulatory accountability. Independent verification programs will support sourcing integrity. Data-backed quality assurance will enhance consumer confidence in a diverse private label portfolio.

Foodservice Chains and Central Kitchens

Foodservice Chains and Central Kitchens segment is projected to reach USD 2.6 billion by 2033, at a CAGR of 8.4% during the forecast period.

Foodservice chains and central kitchens will adopt regular testing protocols to manage centralized production risks. Menu consistency verification will support standardization. Adoption of rapid testing will strengthen food safety governance in high-volume preparation environments.

Others (Government, Regulatory Agencies, Certification Bodies, Audit Firms, etc.) segment is projected to reach USD 2.1 billion by 2033, at a CAGR of 8.5% during the forecast period.

Government bodies, regulatory agencies, certification organizations, and audit firms will influence testing standards through compliance enforcement. Policy development will strengthen standards alignment. Independent verification frameworks will strengthen food safety governance in public and private sector operations.

By Food Type, the market is further divided into:

Meat, Poultry & Seafood

Meat, Poultry & Seafood segment is projected to reach USD 14.4 billion by 2033.

Meat, poultry and seafood categories will require extensive safety testing due to biological vulnerabilities. Dependence on cold storage will increase the intensity of surveillance. Advanced testing platforms will support contamination prevention, residue compliance and export certification sustainability.

Dairy Products

Dairy Products segment is projected to reach USD 8.6 billion by 2033.

Dairy products will demand extensive microbiological and nutritional testing due to concerns about spoilage. Processing variability will encourage repeated verification. Adoption of quality-centric testing will support regulatory acceptance and consumer assurance across the dairy supply ecosystem.

Processed Foods

Processed Foods segment is projected to reach USD 12.5 billion by 2033.

Processed foods will involve multistage testing due to ingredient diversity and extended shelf life. Additional verification and contaminant monitoring will be expedited. Integrated quality frameworks will support compliance across large-scale production networks.

Fruits & Vegetables

Fruits & Vegetables segment is projected to reach USD 10.3 billion by 2033.

Fruits and vegetables will be subject to pesticide residue and microbial testing driven by fresh consumption trends. Traceability verification will support agricultural transparency. Rapid testing methods will enhance supply chain response and export readiness.

Others

Others segment is projected to reach USD 3.5 billion by 2033.

Additional food categories will require adapted testing protocols to suit emerging consumption patterns. Alternative food formats will drive adaptive analytical innovation. Flexible testing services will assist in developing dietary preferences and regulatory preparedness.

By Technology, the Global Food Quality and Safety Testing market is divided as:

Traditional

Traditional segment is projected to grow at a CAGR of 6.4% during the forecast period.

Traditional testing methods will remain relevant due to reliability and regulatory familiarity. Established laboratory techniques will support confirmatory analysis. Continued modernization will increase efficiency while preserving analytical reliability recognized in compliance-driven testing environments.

Rapid

Rapid segment is projected to grow at a CAGR of 9.8% during the forecast period.

Time-sensitive security requirements will accelerate the adoption of rapid testing technologies. On-site identification and real-time analysis will assist in immediate decision making. Innovation investments will enhance sensitivity, scalability and integration into a future-ready food quality ecosystem.

By Region:

Based on geography, the Global Food Quality and Safety Testing market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Food Quality and Safety Testing Market is set to expand at a CAGR of 7.9% during 2026 to 2033, reaching a market size (TAM) of USD 16.2 billion by the end of 2033.

North America is experiencing continued demand for food quality and safety testing due to stringent regulatory oversight, frequent product recalls, and increased consumer scrutiny of packaged foods.

North America sees rapid adoption of testing, supported by advanced laboratory infrastructure, high consumption of processed food, and strong enforcement of compliance standards.

Asia Pacific presents strong growth opportunities through expanding food exports, growing middle-class awareness of food safety, and increasing alignment with international testing protocols.

Asia Pacific offers market expansion potential, supported by rapid urbanization, the growth of the organized retail sector, and increasing investment in modern food testing facilities.

The Middle East, Africa, and South America show gradual market growth in size driven by improvements in food regulations, increased import dependence, and increasing emphasis on contamination control in supply chains.

Competitive Landscape and Strategic Insights

The global food safety and quality testing market plays a critical role in protecting public health across food supply chains. Quality testing has become embedded across everyday food production, owing to rising consumer awareness, strict food regulations, and frequent product recalls. Companies across the enterprise focus on detecting contaminants, verifying components, and ensuring compliance with nearby and worldwide standards. As food systems become extra complicated and global change expands, reliable testing stays central to maintaining sustainability, transparency, and self-belief from farm to desk. Technology has become a strong pillar of progress across food quality and safety testing. Advanced analytical instruments, rapid testing kits, and digital monitoring tools are supporting laboratories in delivering faster and more accurate outcomes. Automation and data integration will continue to reduce turnaround times while improving traceability. These upgrades support food manufacturers, retailers, and regulators who depend on well-timed insights to make choices, control risks, and mitigate large-scale food safety incidents. The competitive landscape of the Global Food Quality and Safety Testing market has major competitors including Agilent Technologies, ALS Limited, AsureQuality Ltd, bioMérieux, Bio-Rad Laboratories, Inc, Bruker, Bureau Veritas, Campden BRI, Charm Sciences, Cotecna, Deibel Laboratories, DEKRA, Eurofins Scientific SE, FoodChain ID, FOSS, Hygiena, Intertek Group PLC, Mérieux NutriSciences, Mettler-Toledo, Microbac Laboratories, Neogen, NSF, QIMA, R-Biopharm, Revvity, Romer Labs, SGS SA, Shimadzu Corporation, Tentamus Group, Thermo Fisher Scientific Inc, TÜV Rheinland, and TÜV SÜD. Competition inside the market continues to intensify as businesses amplify their geographic reach and services. Strategic partnerships, laboratory expansions, and investment in faster trying out strategies will shape future boom. Players that stability accuracy, velocity, and regulatory alignment are anticipated to boom their marketplace function. Over time, the Global Food Quality and Safety Testing market continue to be a foundation for more secure meals structures, assisting both patrons properly-being and long-time period industry stability.

Forecast and Future Outlook

Market size is forecast to rise from USD 26.9 billion in 2025 to USD 49.4 billion by 2033.

Over time, the global food quality and safety testing market will support the shift towards an accountability ecosystem where transparency, auditability and scientific rigor will define the competitive position. The industry will expand its role in foresight, enabling food systems to respond to emerging risks associated with climate stress, innovative ingredients, and changes in dietary behaviour with precision and confidence rather than reaction.

Food Quality and Safety Testing Market Key Segments:

By Type:

Microbiological Testing

Allergen Testing

Chemical Contaminants Testing

Pesticide Residue Testing

Veterinary Drug and Antibiotic Residue Testing

Mycotoxin Testing

Heavy Metals Testing

GMO Testing

Nutritional and Label Claim Verification Testing

Others

By End User:

Food Manufacturers

Beverage Manufacturers

Dairy Processors

Meat Poultry and Seafood Processors

Bakery and Confectionery Producers

Infant Nutrition and Specialized Nutrition Producers

This research report categorizes the Food Quality and Safety Testing market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Food Quality and Safety Testing market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Food Quality and Safety Testing market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 7.9% from 2026 to 2033

Revenue Unit

USD billion

Segmentation

By Type, End User, Food Type, Technology, and Region

Europe (By Type, End User, Food Type, Technology, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of the Europe

Asia Pacific (By Type, End User, Food Type, Technology, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Type, End User, Food Type, Technology, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Type, End User, Food Type, Technology, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share and Revenue

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, Ongoing, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Emerging Segments and Regional Growth Potential

Key Strategic Recommendations

Competitive Benchmarking

Digitalization of Food Quality Assessment and Smart Laboratory Workflows

AI-Driven Inspection and Automated Defect Detection in Food Processing

Computer Vision Enabled Inline Quality Control and Foreign Matter Screening

Connected Sensors and IIoT-based Monitoring for Cold Chain and Storage integrity

Real-time Analytics Dashboards for Quality KPIs and Multi-site Standardization

Blockchain and Track and Trace Platforms Enabling End-to-end Supply Chain Transparency

Digital Product Passports and interoperable Data Standards for Food Traceability

Regulatory Compliance Trends Across FSMA, EU Food Law, HACCP, ISO 22000, BRCGS, and FSSC 22000

Kazakhstan Frozen Potato Products market size is valued at USD 26.4 million in 2025 and is projected to reach USD 53.0 million in 2033, at a CAGR of 9.0% from 2026 to 2033.

Switzerland Poke Food market size is valued at USD 29.2 million in 2025 and is projected to reach USD 44.5 million in 2033, at a CAGR of 5.5% from 2026 to 2033.

Netherlands Food and Beverages QA, QC, and Compliance Software Solutions Market Size, Share, Trends, 2033

Netherlands F&B QA, QC, and Compliance Software Solutions market size is valued at USD 272.5 million in 2025 and is projected to reach USD 421.3 million in 2033, at a CAGR of 5.6% from 2026 to 2033.

Netherlands F&B QA, QC, and Compliance Software Solutions Market, Netherlands F&B QA, QC, and Compliance Software Solutions Market Size, Netherlands F&B QA, QC, and Compliance Software Solutions Market Share, Netherlands F&B QA, QC, and Compliance Software Solutions Market Analysis, Netherlands F&B QA, QC, and Compliance Software Solutions Market Growth, Netherlands F&B QA, QC, and Compliance Software Solutions Market Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market Research Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Forecast, Netherlands F&B QA, QC, and Compliance Software Solutions, Netherlands F&B QA, QC, and Compliance Software Solutions Market Research, Netherlands F&B QA, QC, and Compliance Software Solutions Industry, Netherlands F&B QA, QC, and Compliance Software Solutions Industry Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Data, Netherlands F&B QA, QC, and Compliance Software Solutions Statistics, Netherlands F&B QA, QC, and Compliance Software Solutions Market Statistics, Netherlands F&B QA, QC, and Compliance Software Solutions Industry Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market News, Netherlands F&B QA, QC, and Compliance Software Solutions Forecasts, Netherlands F&B QA, QC, and Compliance Software Solutions Market Intelligence Report

Global Antibiotic-Free Pork market size is valued at USD 25,430.6 million in 2025 and is projected to reach USD 42,528 million in 2033, at a CAGR of 6.6% from 2026 to 2033