Fin and Tube Heat Exchanger Market Size, Share, By Type (Air-Cooled Fin & Tube Heat Exchangers, Water-Cooled Fin & Tube Heat Exchangers, and Refrigerant-Cooled Fin & Tube Heat Exchangers), By Material (Aluminum, Stainless Steel, and Copper), By Application (Cooling Systems, Heating Systems, and Condensation Systems), By End User (HVAC, Automotive, Industrial Processes, and Power Generation), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-3304

Published

January 31, 2025

Pages

262 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

MARKET OVERVIEW

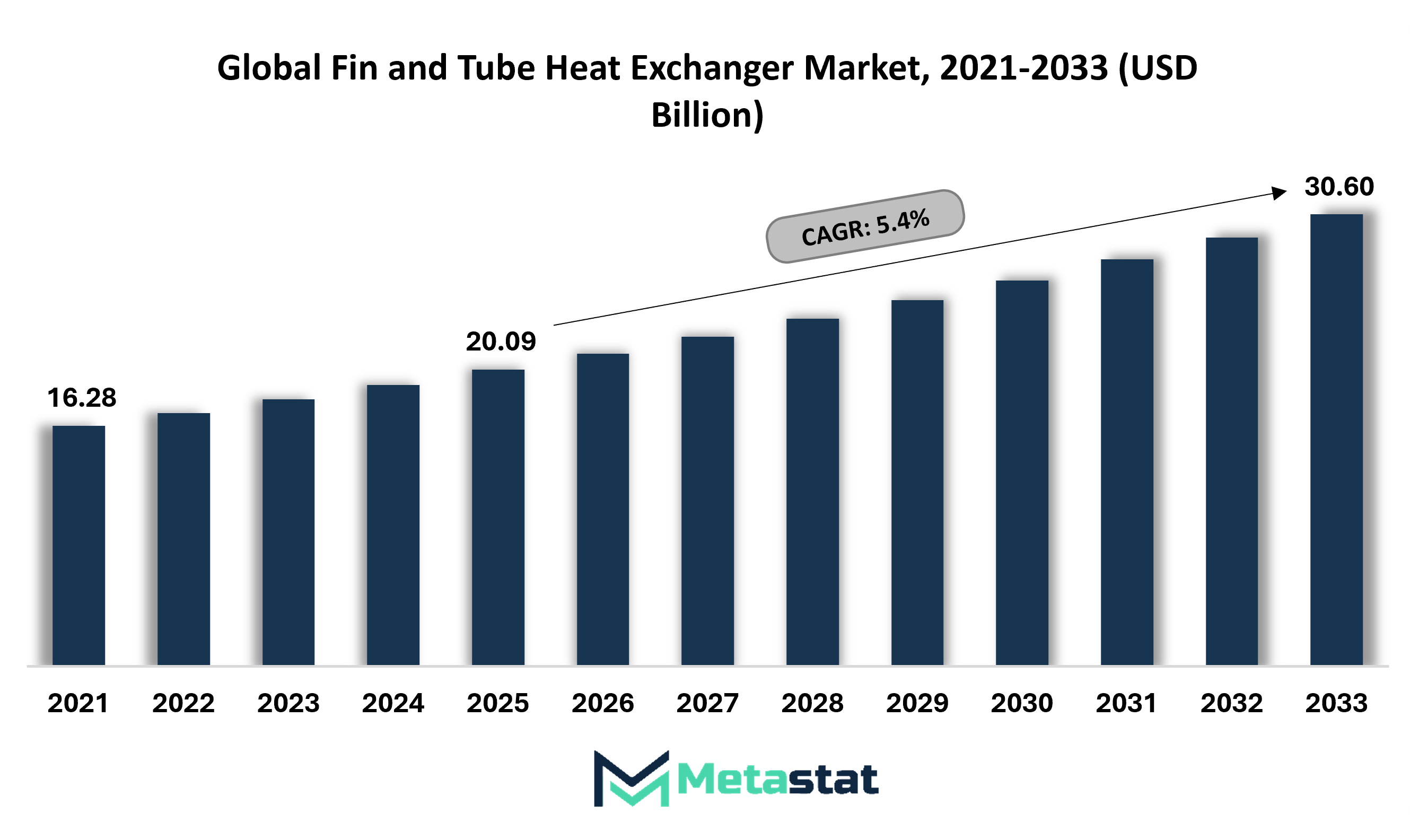

Global Fin and Tube Heat Exchanger market size is valued at USD 20.1 billion in 2025 and projected to grow at a CAGR of 5.4% during the forecast period, reaching USD 30.6 billion by 2033.

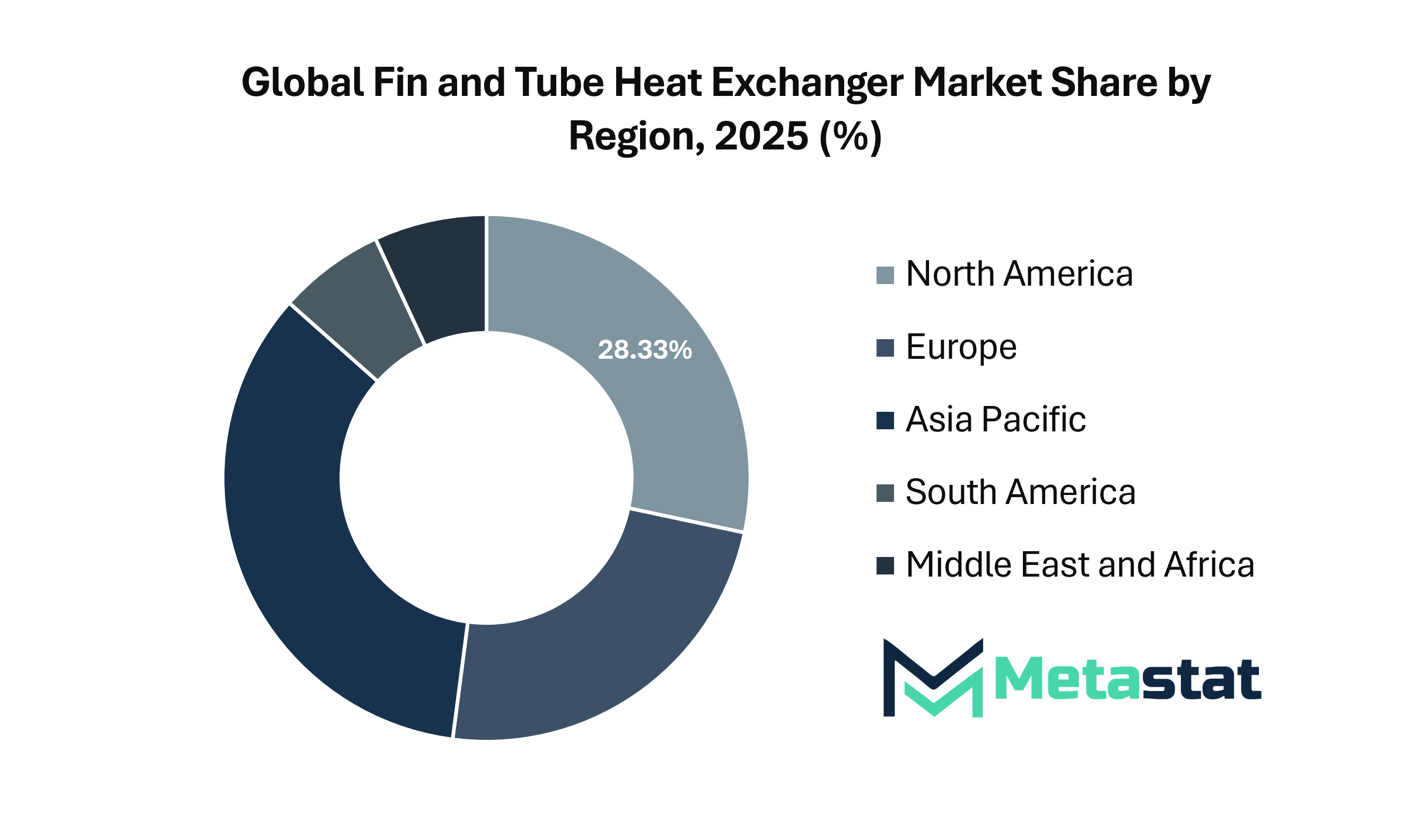

North America holds 28.3% in 2025 with US leading the market share in 2026.

The Global Fin & Tube Heat Exchanger market and its industry will be a vital segment in the thermal management solution space, particularly in the quest to meet increased demands for efficient heat transfer across the applications. As industries continue to grow, and technology progresses to redefine efficiency in operations, this market is going to grapple with increasing complexity from innovation, regulatory shifts, and changes in material sciences. Beyond the common uses, this industry's direction will represent an evolution in terms of energy consumption, production technologies, and considerations of sustainability.

Developments in materials science will reshape the efficiency and durability of fin and tube heat exchangers. Emerging alloys and composite materials will replace traditional metals, offering enhanced thermal conductivity while reducing corrosion risks. These advancements will enable manufacturers to optimize exchanger performance in extreme environments, where heat dissipation remains a significant challenge. The integration of advanced coatings will further enhance longevity and efficiency, minimizing energy losses and operational downtimes.

The second major defining shift in this market will be the digitalization of industrial processes. Integration of sensors and smart monitoring systems into heat exchangers will enable real-time performance tracking, predictive maintenance, and automatic adjustment of operational conditions. This will not only increase efficiency but also fit into the broader push toward Industry 4.0, where interconnected systems lead to cost reduction and operational reliability.

Future strategies will take the cue from the regulatory landscapes and in which manner governments or environmental agencies will effectively ensure that energy consumption and emissions are curtailed. Through this, there will be more pressure on manufacturers to innovate concerning design and functionality. With energy efficiency fast becoming a global need, alternative refrigerants and eco-friendly heat transfer fluids will take more precedence. This regulatory framework will propel research and development efforts toward solution requirements that balance performance with environmental responsibility.

Specialization in the Global Fin & Tube Heat Exchanger market will be driven further by the rising complexity of industrial applications. In the future, manufacturers will instead design application-specific exchangers suited to niche industries rather than developing one-size-fits-all solutions. Aerospace, data centers, and renewable energy will demand customized solutions that maximize efficiency in unique operational settings. Research collaborations and partnerships between industry leaders and academic institutions will shape the next generation of heat exchanger designs.

Geographical shifts beyond the traditional manufacturing hubs will influence the direction of the market. Emerging economies will define future production and consumption patterns. Rapid industrialization and infrastructure development are expected to raise demands for thermal management efficiency, thereby bringing new localized manufacturing and supply chain realignments in this regard. This shift will require strategic investments in regional production facility investments that address logistical challenges and cost efficiencies.

The competitive scenario will also transform as new participants use technological change to upset market equilibrium. There will be some startups focused on nanotechnology, additive manufacturing, and computational fluid dynamics that introduce innovation in design and make newer solutions challenging against the traditional. This would call for continuous changes in offerings and make the established players work and innovate more to come out on top in the markets.While the Global Fin & Tube Heat Exchanger will continue to meet the needs of core industrial markets, its trajectory into the future will far outweigh its present range.

It is going to transform its operational model at the interface of material innovations, digitalization, regulatory constraints, and industry's demand-shift. The next generation of heat exchangers will not only target efficiency but also seamlessly interface with the bigger technological landscape, making thermal management solutions at the forefront of industrial progress.

GROWTH FACTORS

The Global Fin & Tube Heat Exchanger market is observing a tremendous growth due to the increasing requirement of efficient coolings in HVAC as well as industrial applications. These heat exchangers are crucial in sustaining the ideal temperature in many systems, for which they are now required even in diversified industries. Their demand is also on an increase scale in the automotive industry, where efficient thermal management is necessary for efficient vehicle performance and energy efficiency. Similarly, power generation industries rely on these systems to regulate heat in turbines and other equipment, ensuring smooth operations and prolonged equipment lifespan. Despite their growing popularity, some challenges could affect market expansion.

One major issue is the high maintenance required to keep these systems functioning efficiently. Over time, they become prone to fouling, which can reduce heat transfer efficiency and lead to higher operational costs. In addition, the fluctuating prices of raw materials directly influence the manufacturing costs, which do not allow for stable production cost. These can slow down the adoption of fin and tube heat exchangers in some applications where cost-sensitive solutions are preferred.

On the bright side, advancements in materials and new design concepts will overcome these problems. Engineers and researchers are continuously improving the durability and efficiency of heat exchangers so that they can stand harsh operating conditions but with high performance. Introducing corrosion-resistant materials and improving the design of heat transfer is likely to enhance their reliability and make them more attractive for industries that are seeking long-term solutions.

The market will offer promising opportunities ahead as industries are still focusing on energy efficiency and environmental sustainability.The companies are investing in research and development of heat exchangers which minimize energy consumption and contribute to making the entire system efficient.

As the carbon footprint comes under the increasing scanner for reduction, industry processes need to be optimized. Therefore, advancements in cooling solutions are going to see a hike in demand. With the current pace of innovation in the area of heat exchangers and the rising requirement for thermal management efficiency in the industries, this market is bound to experience stable growth in the coming years.

MARKET SEGMENTATION

By Type

Air-Cooled Fin & Tube Heat Exchangers segment is valued at USD 10.5 billion in 2026 and is projected to reach USD 15 billion by 2033, at a CAGR of 5.1% during the forecast period.

The Global Fin & Tube Heat Exchanger market is growing due to the demand from various sectors. These are heat exchangers capable of transferring heat easily from one fluid to the other. With applications in HVAC systems, power plants, chemical industries, and refrigeration, the demand for these heat exchangers is on the rise. As energy efficiency and reduced costs become inevitable for the industries, the demand for more advanced exchangers increases.

One of the major drivers in market growth is increased demand for cooling solutions in manufacturing and processing industries. Technological advancements have led companies to design improved performance with more compact models. Enhanced use of these exchangers can now be seen in automotive applications, which calls for a highly efficient cooling system to uphold the engine's performance and fuel efficiency requirements of modern vehicles. Some more industries for maintaining optimal operation depend largely on heat exchangers: the food and beverages sector, the pharmaceutical industry, and even in power generation. It has been classified under type with $9,765.53 million attributed to Air-Cooled Fin & Tube Heat Exchangers.

Water-Cooled Fin & Tube Heat Exchangers and Refrigerant-Cooled Fin & Tube Heat Exchangers also go into the contribution list of demand within the market. Each type has its usage, depending upon the source available for cooling- air-cooled machines are in vogue wherever sources of water are scarce. Water-cooled variants have usually been used where considerable industrial requirements for cooling had to be achieved to ensure high-speed heat transfer from the fluid flow.

The third variant refrigerant-cooled finds extensive applications where refrigeration or air-conditioning is required. The increasing focus on environmental sustainability has led to the adoption of energy-efficient heat exchangers. Governments and regulatory bodies are encouraging industries to use environmentally friendly cooling solutions, which has further propelled market growth.

Additionally, the integration of smart technologies in these systems allows for real-time monitoring and improved efficiency, reducing operational costs for businesses. Although the future looks bright, there are still some drawbacks. The investment cost for the advanced heat exchangers is high, which makes them less favorable to smaller companies. Maintenance and operating costs may also be a concern for some industries. However, the long-term benefits include energy savings and better performance.

With an ongoing drive in technology, it can be projected that the global market for Fin & Tube Heat Exchanger is looking at sustained growth and increase with a more substantial requirement by the industry in relation to the availability of cooling, more energy efficient and sustainable options.

By Material

Stainless Steel segment is projected to reach USD 5.6 billion by 2033, at a CAGR of 5.6% during the forecast period.

The Global Fin & Tube Heat Exchanger market is divided by material, and three major categories in this area include aluminum, stainless steel, and copper. It is through these materials that the efficiency, durability, and cost-effectiveness of heat exchangers are largely determined. Among the most used material is aluminum. This is mainly due to the lightweight nature, excellent thermal conductivity, and making it suitable for industries that have to have heat transfer efficiently with a minimal weight.

Stainless steel is preferred in environments exposed to moisture, chemicals, and extreme temperatures because of its corrosion resistance and strength. Copper is used because of its superior heat conductivity and resistance to corrosion in applications where maximum heat transfer is essential. Increased demands are witnessed, mainly in areas that consider fin and tube heat exchangers to help industries save cost and conserve more energy.

These devices are critical in HVAC, power generation, automotive, and chemical processing, where temperature must be controlled to function at an optimum level. Companies invest in research and development to improve the design of heat exchangers, seeking to enhance efficiency and minimize energy consumption. In this regard, material selection plays a very significant role in the achievement of these objectives, since each material has different benefits that may be suitable for specific applications. Markets are increasingly opting for lightweight aluminum heat exchangers as well, mainly due to lightweight characteristics and cost-effectiveness.

More and more industries optimise performance without increasing manufacturing and operating costs by opting for the aluminum-based models. Nevertheless, in areas where harsh conditions and durability are involved, stainless steel is a preferred choice. Copper, with its highly efficient heat transfer capabilities, finds use in specialized applications wherein these benefits are well worth the expenditure.

Environmental issues and concerns over sustainability are also aspects that shape the market dynamics. The demand is now more geared towards companies obtaining environmentally friendly material and designs as they work toward minimizing carbon emissions without losing high efficiency. Such improvements in production processes enhance performance and longer lifespan heat exchangers both in economic and environmental aspects.

The competitive landscape involves major companies that continue investing in enhanced technologies so that their market share is not at risk. Innovation through strategic alliances, mergers, and acquisitions results in expanded product portfolios as they respond to the changing requirements of industries that utilize heat exchangers. Companies tend to individualize their products, which enables them to match a specific requirement of different industries so their needs are met.

Overall, the Global Fin & Tube Heat Exchanger market is in a continuous evolution process due to improvements in materials, efficiency, and sustainability. The growing concern for energy conservation and performance optimization has increased the demand for high-quality heat exchangers, further emphasizing their use in different industries across the globe.

By Application

Heating Systems segment is projected to reach USD 6.6 billion by 2033.

The Global Fin & Tube Heat Exchanger market is experiencing steady growth due to its wide application in various industries. These exchangers are critical in transferring heat efficiently and, therefore, form a very essential part of several systems. The increasing trend in the demand for energy efficiency and cost-effectiveness will see an increase in the demand for these heat exchangers.

The primary driver in this market would be the requirement for effective temperature regulation in most sectors. Temperature regulation is considered a critical necessity in industrial processes, power plants, and HVAC. Fin & Tube Heat Exchangers are so widely used in the industry because it enhances heat transfer while minimizing the consumption of energy. Their design, which comprises fins for increasing surface area and tubes for fluid movement, makes them ideal for effective heat exchange, hence popular across industries.

By application, the market is further divided into Cooling Systems, Heating Systems, and Condensation Systems. Cooling systems rely on these exchangers to dissipate heat and maintain stable temperatures in industrial machinery, refrigeration units, and air conditioning systems. Without efficient cooling, equipment performance can decline, leading to increased maintenance costs and potential failures.

Heating systems, on the other hand, use these exchangers to generate and distribute warmth in residential, commercial, and industrial settings. They help improve energy efficiency by ensuring heat is transferred effectively with minimal losses. These heat exchangers support the condensation system as this will allow vapor transformation to liquid states in various kinds of power-generation industries and chemicals industries.

Expanding on its thrust toward new renewable energy products is also driving the increase in the industry's growth because environmental concerns keep intensifying under current stricter restrictions while the energy costs skyrocket. These align with these goals in providing high thermal performance with minimal energy consumption. Material advancements and improved manufacturing processes have also driven the growth of this market as companies come up with exchangers with improved durability, corrosion resistance, and higher heat transfer capability.

The future for the Fin & Tube Heat Exchanger market appears to be promising as technology improves and is adopted in various industries. The increasing demand for efficient heating, cooling, and condensation solutions will always require these heat exchangers as essential parts of the application. They continue to find their place in this sustainable world with emphasis on energy efficiency and performance.

By End User

Industrial Processes segment is projected to grow at a CAGR of 5.4% during the forecast period.

Global Fin & Tube Heat Exchanger market is in substantial growth now, finding its importance in the recent times with major businesses, which feel a vital need for effective heat transfer systems. The exchangers constitute an important component in several sectors that help in controlling temperatures, increasing the process of energy efficiency, and improving overall system performance. Industries that focus on sustainability, energy conservation, and improving operational efficiency prefer adopting exchangers.

The most significant area of application for Fin & Tube Heat Exchangers is HVAC systems. All applications in heating, ventilation, and air conditioning need effective heat transfer solutions for maintaining comfortable indoor temperatures with optimal use of energy. In light of the increasing demand for energy-efficient buildings, advanced heat exchangers have a high potential to grow in demand because they help in generating lesser overall power consumption without any compromise on performance.

The automotive industry is also dependent on these heat exchangers. The cooling systems of vehicles are designed to ensure that they do not overheat; thus, engine performance is optimized, and several parts' life span is enhanced. From the cooling of engines to air conditioning, Fin & Tube Heat Exchangers play an important role in the smooth operation of vehicles. With the rising trend of electric vehicles, attention towards innovative cooling solutions for the management of temperatures in batteries will continue to grow, thus boosting market demand.

Many manufacturing applications are high-temperature applications, and thus, industrial processes have a lot of benefits derived from these heat exchangers. Chemical processing, food production, and metal fabrication require reliable heat exchange solutions to maintain efficiency and safety. These industries rely on well-designed systems to handle the heat loads without the risk of equipment failure. So, Fin & Tube Heat Exchangers are an essential component of these industries.

Majorly, these exchangers are applied in the sector of power generation. In thermal power plants, nuclear facilities, and renewable energy systems, effective heat transfer is required in maintaining efficiency and preventing energy loss. Heat exchangers help provide optimization in performance for steam turbines, condensers, or other critical systems to ensure constant power production. With a continued trend toward cleaner sources of energy, improvement in sustainable technologies is expected to be enhanced using advanced heat exchanger technologies.

Since energy efficiency remains an important element for most developing industries, Fin & Tube Heat Exchangers are in constant demand. Materials and designs have been developing and changing so much that many business companies achieve low costs alongside complying with governmental standards. Fin & Tube Heat Exchangers, being among the most diverse application of heat exchangers with great importance nowadays, will continue playing an important role in the realization of smarter, sustainable energy globally.

REGIONAL ANALYSIS

Geographical region is also one of the main influencing factors in the global fin & tube heat exchanger market, and the markets are divided into five main geographies: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. All of them have their different economic and industrial characteristics, therefore influencing the demand for fin and tube heat exchangers and growth.

North America includes the U.S., Canada, and Mexico. The U.S. is the technological leader and industrial user. Therefore, the U.S. market is a significant one for these exchangers. Canada and Mexico also contribute to the demand due to their developing industrial and energy sectors. Europe includes the UK, Germany, France, Italy, and the Rest of Europe. Germany is the largest contributor in terms of engineering and manufacturing, making the demand for efficient heat exchange solutions very high. The UK, France, and Italy also contribute to this demand, mainly because of their focus on sustainable energy and industrial growth.

The Asia-Pacific is another significant region, with India, China, Japan, South Korea, and the Rest of Asia-Pacific being key contributors. China and India have fast-growing industrial sectors, which increase the demand for heat exchangers in manufacturing, power generation, and HVAC applications. Japan and South Korea, known for their advanced technology and engineering expertise, further strengthen the market in this region. The Rest of Asia-Pacific also sees steady growth due to infrastructural developments and increasing energy needs.

In South America, Brazil and Argentina are key markets; besides them, there also has potential for Rest of South America. Fin and tube heat exchanger is gaining the demands by their industrial sectors where Argentina targets efficiency with respect to energy use. Indicating increasing growth of industry for proper thermal management solution as the entire region undergoes the impact.

The Middle East & Africa region can be broadly classified into GCC Countries, Egypt, South Africa, and the Rest of the Middle East & Africa. GCC Countries, specifically Saudi Arabia and the UAE, host strong energy and industrial sectors that necessitate efficient heat exchange systems. Egypt and South Africa also contribute to market growth by increasing their investments in infrastructure and energy projects. The demand in the broader region is driven by the expansion of industries and their focus on energy efficiency.

In general, the market for fin and tube heat exchangers continues to grow across these regions due to industrial expansion, technological advancements, and the increasing need for energy-efficient solutions. Each region's unique economic landscape influences the adoption and development of heat exchange technologies, shaping the industry's future growth.

COMPETITIVE PLAYERS

The global fin and tube heat exchanger market is growing at a steady pace because of growing demand from all kinds of industries, such as HVAC, refrigeration, automobile, and power generation. As the heat transfer between fluids enables efficient energy management, these types of heat exchangers play a crucial role in many applications. With industry trends focusing more on sustainability and reducing costs, there is a significant demand for heat exchange solutions that are efficient and effective.

Energy conservation is one of the main reasons that fuel the market. Companies and industries are continuously looking for ways to curtail energy consumption, and fin and tube heat exchangers provide the best-suited solution. These systems enhance thermal performance by minimizing energy loss, making them a commonly recommended choice by manufacturers. Moreover, government regulations aimed at energy efficiency are also propelling companies to invest in advanced heat exchanger technology.

With regard to industrialized sectors, both manufacturing and chemical processing expand their markets. To ensure the most efficient cooling or heating processes possible, finned and tube type heat exchangers are usually used in reliable applications. From the automotive view, they support the cooling and heating of all engines, also air conditioning unit and transmission fluid applications, thus leading to better vehicles performance and prolongation.

The production of electric and hybrid vehicles will be on the rise, hence increasing the demand for advanced heat exchangers. Advancements in technology also contribute to the market, as the design of exchangers has been improved by manufacturers to provide higher thermal transfer efficiency and longer lifetimes. Aluminium and stainless steel are some of the materials frequently employed to get superior performance and better life for these exchangers. Advances have been made through compact and lightweight designs that can now be applied in data centers and renewable energy systems.

Despite the positive outlook, certain challenges exist. High initial costs associated with advanced heat exchanger technology can be a limiting factor for smaller businesses. Additionally, fluctuating raw material prices impact production costs, affecting overall market growth. However, substantial research and development is conducted on this field to resolve those problems for making fin and tube heat exchangers economical.

Some of the major players in the fin and tube heat exchanger market are Alfa Laval AB, Kelvion Holding GmbH, Danfoss A/S, Modine Manufacturing Company, Thermofin GmbH, Evapco Inc., Johnson Controls International, Shanghai Shenglin M&E Technology Co., Ltd., Boyd Corporation, and Kaori Heat Treatment Co., Ltd. The companies are actively involved in investing in product innovation and strategic partnerships for a better market position.As industrialization increases, with growth in technological advancements and energy efficiency, the global fin and tube heat exchanger market will grow into the next years.

Fin & Tube Heat Exchanger Market Key Segments:

By Type

Air-Cooled Fin & Tube Heat Exchangers

Water-Cooled Fin & Tube Heat Exchangers

Refrigerant-Cooled Fin & Tube Heat Exchangers

By Material

Aluminum

Stainless Steel

Copper

By Application

Cooling Systems

Heating Systems

Condensation Systems

By End User

HVAC

Automotive

Industrial Processes

Power Generation

Key Global Fin & Tube Heat Exchanger Industry Players

Bangladesh Flavours and Fragrances Market Size, Share, Trends, 2033

Bangladesh Flavours and Fragrances market size is valued at USD 793.9 million in 2025 and is projected to reach USD 1,447.9 million in 2033, at a CAGR of 7.8% from 2026 to 2033

Bangladesh Flavours and Fragrances Market, Bangladesh Flavours and Fragrances Market Size, Bangladesh Flavours and Fragrances Market Share, Bangladesh Flavours and Fragrances Market Analysis, Bangladesh Flavours and Fragrances Market Growth, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market Research Report, Bangladesh Flavours and Fragrances Market Forecast, Bangladesh Flavours and Fragrances, Bangladesh Flavours and Fragrances Market Research, Bangladesh Flavours and Fragrances Industry, Bangladesh Flavours and Fragrances Industry Report, Bangladesh Flavours and Fragrances Market Data, Bangladesh Flavours and Fragrances Statistics, Bangladesh Flavours and Fragrances Market Statistics, Bangladesh Flavours and Fragrances Industry Trends, Bangladesh Flavours and Fragrances Market Report, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market News, Bangladesh Flavours and Fragrances Forecasts, Bangladesh Flavours and Fragrances Market Intelligence Report

Biocatalysis and Enzyme Biocatalysts Market Size, Share, Trends, 2033

Biocatalysis and Enzyme Biocatalysts market size is valued at USD 737.8 million in 2025 and is projected to reach USD 1,221.0 million in 2033, at a CAGR of 6.5% from 2026 to 2033.

Biocatalysis and Enzyme Biocatalysts Market, Biocatalysis and Enzyme Biocatalysts Market Size, Biocatalysis and Enzyme Biocatalysts Market Share, Biocatalysis and Enzyme Biocatalysts Market Analysis, Biocatalysis and Enzyme Biocatalysts Market Growth, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market Research Report, Biocatalysis and Enzyme Biocatalysts Market Forecast, Biocatalysis and Enzyme Biocatalysts, Biocatalysis and Enzyme Biocatalysts Market Research, Biocatalysis and Enzyme Biocatalysts Industry, Biocatalysis and Enzyme Biocatalysts Industry Report, Biocatalysis and Enzyme Biocatalysts Market Data, Biocatalysis and Enzyme Biocatalysts Statistics, Biocatalysis and Enzyme Biocatalysts Market Statistics, Biocatalysis and Enzyme Biocatalysts Industry Trends, Biocatalysis and Enzyme Biocatalysts Market Report, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market News, Biocatalysis and Enzyme Biocatalysts Forecasts, Biocatalysis and Enzyme Biocatalysts Market Intelligence Report

Malaysia Tyre Pyrolysis Products Market Size, Share, Trends, 2033

Malaysia Tyre Pyrolysis Products market size is valued at USD 205.9 million in 2025 and is projected to reach USD 421.8 million in 2033, at a CAGR of 9.3% from 2026 to 2033.

Malaysia Tyre Pyrolysis Products Market, Malaysia Tyre Pyrolysis Products Market Size, Malaysia Tyre Pyrolysis Products Market Share, Malaysia Tyre Pyrolysis Products Market Analysis, Malaysia Tyre Pyrolysis Products Market Growth, Malaysia Tyre Pyrolysis Products Market Trends, Malaysia Tyre Pyrolysis Products Market Research Report, Malaysia Tyre Pyrolysis Products Market Forecast, Malaysia Tyre Pyrolysis Products, Malaysia Tyre Pyrolysis Products Market Research, Malaysia Tyre Pyrolysis Products Industry, Malaysia Tyre Pyrolysis Products Industry Report, Malaysia Tyre Pyrolysis Products Market Data, Malaysia Tyre Pyrolysis Products Statistics, Malaysia Tyre Pyrolysis Products Market Statistics, Malaysia Tyre Pyrolysis Products Industry Trends, Malaysia Tyre Pyrolysis Products Market Report, Malaysia Tyre Pyrolysis Products Market Trends, Malaysia Tyre Pyrolysis Products Market News, Malaysia Tyre Pyrolysis Products Forecasts, Malaysia Tyre Pyrolysis Products Market Intelligence Report

Near Infrared (NIR) Analyzer Market Size, Share, Trends, 2033

Near Infrared (NIR) Analyzer market size is valued at USD 855.3 million in 2025 and is projected to reach USD 1,813.6 million in 2033, at a CAGR of 9.9% from 2026 to 2033.

Near Infrared (NIR) Analyzer Market, Near Infrared (NIR) Analyzer Market Size, Near Infrared (NIR) Analyzer Market Share, Near Infrared (NIR) Analyzer Market Analysis, Near Infrared (NIR) Analyzer Market Growth, Near Infrared (NIR) Analyzer Market Trends, Near Infrared (NIR) Analyzer Market Research Report, Near Infrared (NIR) Analyzer Market Forecast, Near Infrared (NIR) Analyzer, Near Infrared (NIR) Analyzer Market Research, Near Infrared (NIR) Analyzer Industry, Near Infrared (NIR) Analyzer Industry Report, Near Infrared (NIR) Analyzer Market Data, Near Infrared (NIR) Analyzer Statistics, Near Infrared (NIR) Analyzer Market Statistics, Near Infrared (NIR) Analyzer Industry Trends, Near Infrared (NIR) Analyzer Market Report, Near Infrared (NIR) Analyzer Market Trends, Near Infrared (NIR) Analyzer Market News, Near Infrared (NIR) Analyzer Forecasts, Near Infrared (NIR) Analyzer Market Intelligence Report