Global Draught Beer Market - Comprehensive Data-Driven Market Analysis & Strategic Outlook

Could the global draught beer market redefine customer reviews as shifting existence and premiumization trends reshape drinking conduct, or will traditional choices sluggish down this transformation? How might technological improvements in storage and dispensing disrupt the industry, and what uncertainties should rising health-aware selections create for its lengthy-term boom?

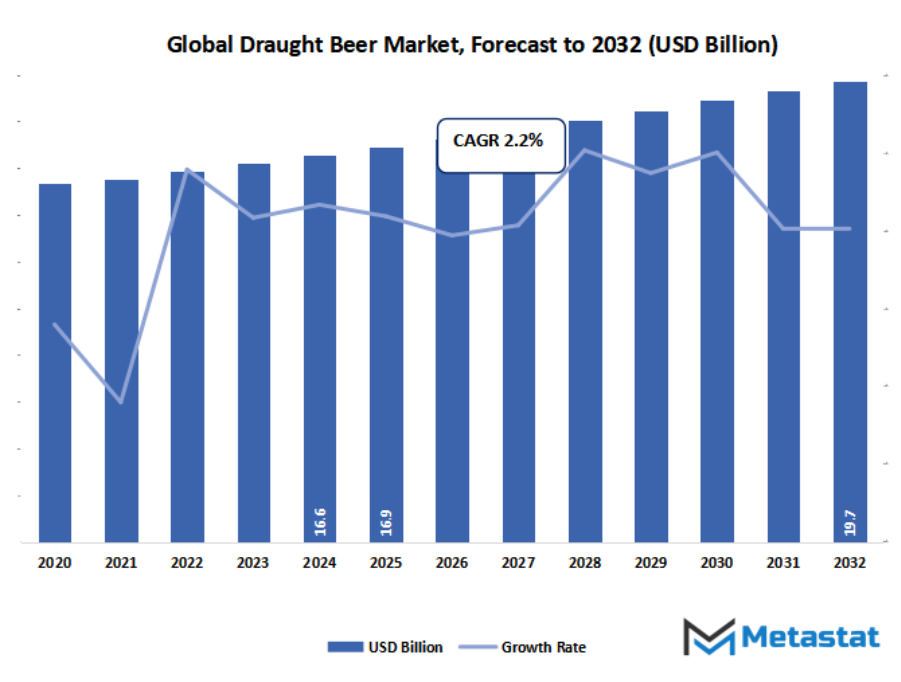

- Global draught beer market valued at approximately USD 16.9 Billion in 2025, growing at a CAGR of around 2.2% through 2032, with potential to exceed USD 19.7 Billion.

- Keg Beer account for nearly 93.5% market revenues, driving innovation and expanding applications through intense research.

- Key trends driving growth: Consumer preference for premium, fresh-tasting beer experiences in bars and restaurants., Higher profit margins for retailers compared to bottled/canned beer.

- Opportunities include Growth of home draught systems and craft beer subscriptions.

- Key insight: The market is set to grow exponentially in value over the next decade, highlighting significant growth opportunities.

The global draught beer market and industry will be watched not just for its own rich heritage but for how it will evolve away from expectations. What the focus will be in the years to come is not just how consumption patterns and regional tastes will influence the market, but how draught beer will be framed as part of larger cultural and social experiences. This market will be accompanied by the push of local breweries to be creative and international players redefining distribution outlets, setting the stage where beer will no longer just be a drink—it will be an identity and lifestyle statement.

What will differentiate the global draught beer market in the future is how it will overcome traditional boundaries. Beer faucets will serve up not only familiar lagers or ales, but also creative hybrids that will redefine the concept of draught beer. Customers will increasingly demand not only freshness, but authenticity of flavour, which will compel both small and established breweries alike to re-examine their brewing processes and packaging. The focus will increasingly be on tradition and innovation as the link to what this market will be appealing to worldwide consumers.

Market Segmentation Analysis

The global draught beer market is mainly classified based on Type, Category, Production, End User.

By Type is further segmented into:

- Keg Beer - The global draught beer market will continue to see robust adoption of keg beer, particularly because of the ease with which it can be stored and transported. Future consumption will further be based on more automated systems in restaurants and pubs, promoting freshness and uniform quality. Increased demand from urban areas will further bolster the position of keg beer.

- Cask Beer - In the global draught beer market, cask beer will continue to hold relevance among customers looking for authentic brewing styles. The growth will be complimented by craft-oriented outlets that value authenticity and natural fermentation. In the coming years, the category will remain robust in markets that appreciate artisan quality, albeit if manufacturing continues to remain relatively smaller in scale compared to kegs.

By Category the market is divided into:

- Super Premium - The global draught beer market will experience increasing appeal for super premium offerings as customer tastes lean towards luxury experiences. Increasing disposable incomes and the desire for exclusivity will make breweries produce limited-edition draught types. The premiumization movement will enable brands to build stronger identities and increase market share.

- Premium - Premium products in the global draught beer market will continue to be a top option for a wide consumer base. This segment finds a balance between cost and quality, remaining affordable yet providing an upscale taste. In the future, premium draught products will continue to grow across established and emerging regions of consumers.

- Regular - The global draught beer market will maintain steady demand for regular draught beer, led chiefly by mass consumption in social environments. This segment offers affordability and availability, making it largely accessible. Regular variants, in the years to come, will remain a staple for breweries, backing volume growth through varied geographies.

By Production the market is further divided into:

- Macro Breweries - Macro breweries will continue to be important to the global draught beer market, providing large-scale distribution and standardized production. Their function in addressing global demand will become increasingly significant as consumption increases throughout developing economies. Technological incorporation and efficiency gains will assist macro breweries in sustaining competitive strengths in expansions to come.

- Microbreweries - Microbreweries will define a creative corner in the global draught beer market by testing out different flavors and local ingredients. Future demand from consumers will be towards small-batch and personalized production. The segment will be unique for innovation, attracting enthusiasts hungry for variety, and increasing the overall richness of the market.

By End User the global draught beer market is divided as:

- Commercial - Commercial outlets will continue to be the greatest contributors to the global draught beer market. Growth will be helped by growing hospitality industries, such as pubs, bars, and restaurants, in both developed and emerging economies. In the future, these establishments will make greater use of new dispensing technologies to provide consistent quality and service efficiency.

- Home - The World Draught Beer Market will experience growing demand for home consumption as lifestyle trends evolve. Improvements in portable dispensing systems and mini-kegs will provide the draught experience in households. This trend will open new opportunities for breweries to focus on individual consumers looking for convenience and enjoyment in coming years.

|

Forecast Period |

2025-2032 |

|

Market Size in 2025 |

$16.9 Billion |

|

Market Size by 2032 |

$19.7 Billion |

|

Growth Rate from 2025 to 2032 |

2.2% |

|

Base Year |

2024 |

|

Regions Covered |

North America, Europe, Asia-Pacific, South America, Middle East & Africa |

Geographic Dynamics

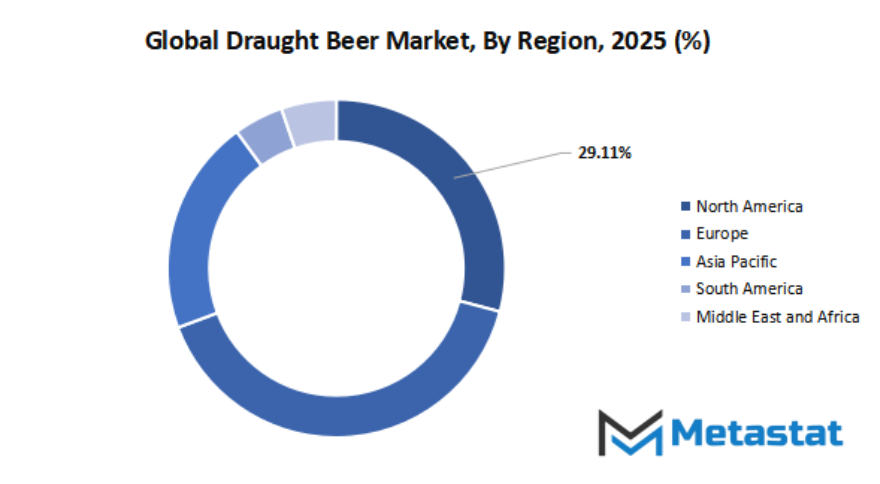

Based on geography, the global market is divided into North America, Europe, Asia-Pacific, South America, and Middle East & Africa. North America is further divided in the U.S., Canada, and Mexico, whereas Europe consists of the UK, Germany, France, Italy, and Rest of Europe. Asia-Pacific is segmented into India, China, Japan, South Korea, and Rest of Asia-Pacific. The South America region includes Brazil, Argentina, and the Rest of South America, while the Middle East & Africa is categorized into GCC Countries, Egypt, South Africa, and Rest of Middle East & Africa.

Competitive Landscape & Strategic Insights

The global draught beer market is an embodiment of tradition and innovation where there is a marriage between established global players and vibrant regional brewers. As greater consumers are looking for clean and wonderful beer, draught stays fairly appealing across a huge patron base. In contrast to bottled or canned options, the draught beer offers a completely unique taste and experience that many believe represents authenticity and socializing. This preference has sustained the market, with breweries global making an investment in upgrading their merchandise whilst keeping their initial appeal.

The market is prompted via the presence of top worldwide manufacturers in addition to increasing regional gamers. Some of the pinnacle players consist of Anheuser-Busch InBev, Boston Beer Company, and Heineken International B.V., which have developed substantial distribution networks and consumer loyalty through the years. Along with them, players consisting of Anadolu Efes, Asahi Group Holdings, Ltd., and Molson Coors Beverage Company introduce extra opposition through different portfolios and a worldwide presence. Regional players such as China Resources Snow Breweries and New Belgium Brewing Company offer diversification through the potential to play properly in local markets while additionally establishing a presence in global markets.

The competitive panorama is not distinctive to traditional giants however additionally includes smaller and mid-sized breweries increasingly more shaping consumer behavior. Terms like Castel Frères and Constellation Brands, Inc. show how regional forces are consistently becoming prominent by emphasizing niche segments, distinctive brewing culture, and greater interaction with customers. This fusion of international scope and localized creativity preserves the market for draught beer as a draw for investors and consumers alike, looking for diversity.

In the destiny, the global draught beer market is expected to grow as purchaser desire turns towards top class reports. With the present gamers and new entrants continuously innovating in terms of flavour, packaging, and distribution, the marketplace is probably to be dynamic. The existence of established global players and emerging players makes sure that the draught beer segment will not only maintain its cultural relevance but also tighten its position in the broader beverage industry.

Market Risks & Opportunities

Restraints & Challenges:

- Complex logistics and maintenance requirements for dispensing systems. - Sophisticated logistics and maintenance needs for dispensing systems will continue to pose impediments to growth. Specialized handling, equipment maintenance, and regular supply chain coordination needs will require more investment. In the absence of effective solutions, mass distribution may suffer delays, and this could curtail growth in both commercial establishments and new market entries.

- Short shelf life and spoilage risk if not managed properly. - Short shelf life and risk of spoilage if not handled appropriately will be another urgent issue. Draught beer requires strict conditions of garage, and mild deviations in temperature or hygiene will bring about lack of quality. The destiny advancement will rely upon technological strides that keep freshness and minimize wastage in all breweries, vendors, and retailers.

Opportunities:

Growth of home draught systems and craft beer subscriptions. - Consumer need for customized experiences and new flavours will drive demand beyond restaurants and bars. Innovative, space-saving, and simple-to-use systems will enable households to duplicate pub-like experiences, transforming the market in favour of direct-to-home models. Craft beer subscription expansion will enable new channels for consumer interaction. Novel tastes, rotating options, and hand-crafted packs shipped at regular periods will reimagine convenience and variety. With increasing digital channels and web orders, subscription-based sales will facilitate draught beer more conveniently, ensuring wider access and greater customer loyalty.

Forecast & Future Outlook

- Short-Term (1–2 Years): Recovery from COVID-19 disruptions with renewed testing demand as healthcare providers emphasize metabolic risk monitoring.

- Mid-Term (3–5 Years): Greater automation and multiplex assay adoption improve throughput and cost efficiency, increasing clinical adoption.

- Long-Term (6–10 Years): Potential integration into routine metabolic screening programs globally, supported by replacement of conventional tests with advanced biomarker panels.

Market size is forecast to rise from USD 16.9 Billion in 2025 to over USD 19.7 Billion by 2032. Draught Beer will maintain dominance but face growing competition from emerging formats.

As much as it has been commercially broad, the global draught beer market will also indirectly affect tourism, social events, and even art collaborations. Festivals and brewpubs will be venues where individuals will not only consume but engage with stories, craftsmanship, and community. As new dispensing and storage technologies arise, they will redefine convenience without sacrificing the integrity of the product. In that way, this market will not only grow geographically but conceptually as well, expanding into realms of culture, experience, and social identity. In the process, the global draught beer market will offer itself as more than a commercial endeavor, it will become a powerful cultural force with lasting influence.

Report Coverage

This research report categorizes the Draught Beer market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Draught Beer market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Draught Beer market.

Draught Beer Market Key Segments:

By Type

- Keg Beer

- Cask Beer

By Category

- Super Premium

- Premium

- Regular

By Production

- Macro Breweries

- Microbreweries

By End User

- Commercial

- Home

Key Global Draught Beer Industry Players

- Anheuser-Busch InBev

- Boston Beer Company

- Heineken International B.V.

- Anadolu Efes

- Asahi Group Holdings, Ltd.

- Molson Coors Beverage Company

- China Resources Snow Breweries

- Carlsberg

- New Belgium Brewing Company

- Castel Frères

- Constellation Brands, Inc.

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential

US: +1 3023308252

US: +1 3023308252