Cathodic Protection Market Size, Share, By Type (Galvanic (Sacrificial Anodes) Cathodic Protection, and Impressed Current Cathodic Protection), By Component (Anodes, Power Supplies, Reference Electrodes, Cables, Monitoring Systems, and Others), By Service (Design, Engineering, Installation, Construction, Inspection, Monitoring, Maintenance, and Repair), By Application (Oil Transmission Pipelines, Gas Transmission Pipelines, Storage Facilities, Processing Plants, Water, Wastewater, Transportation, Bridges, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4716

Published

May 4, 2026

Pages

315 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

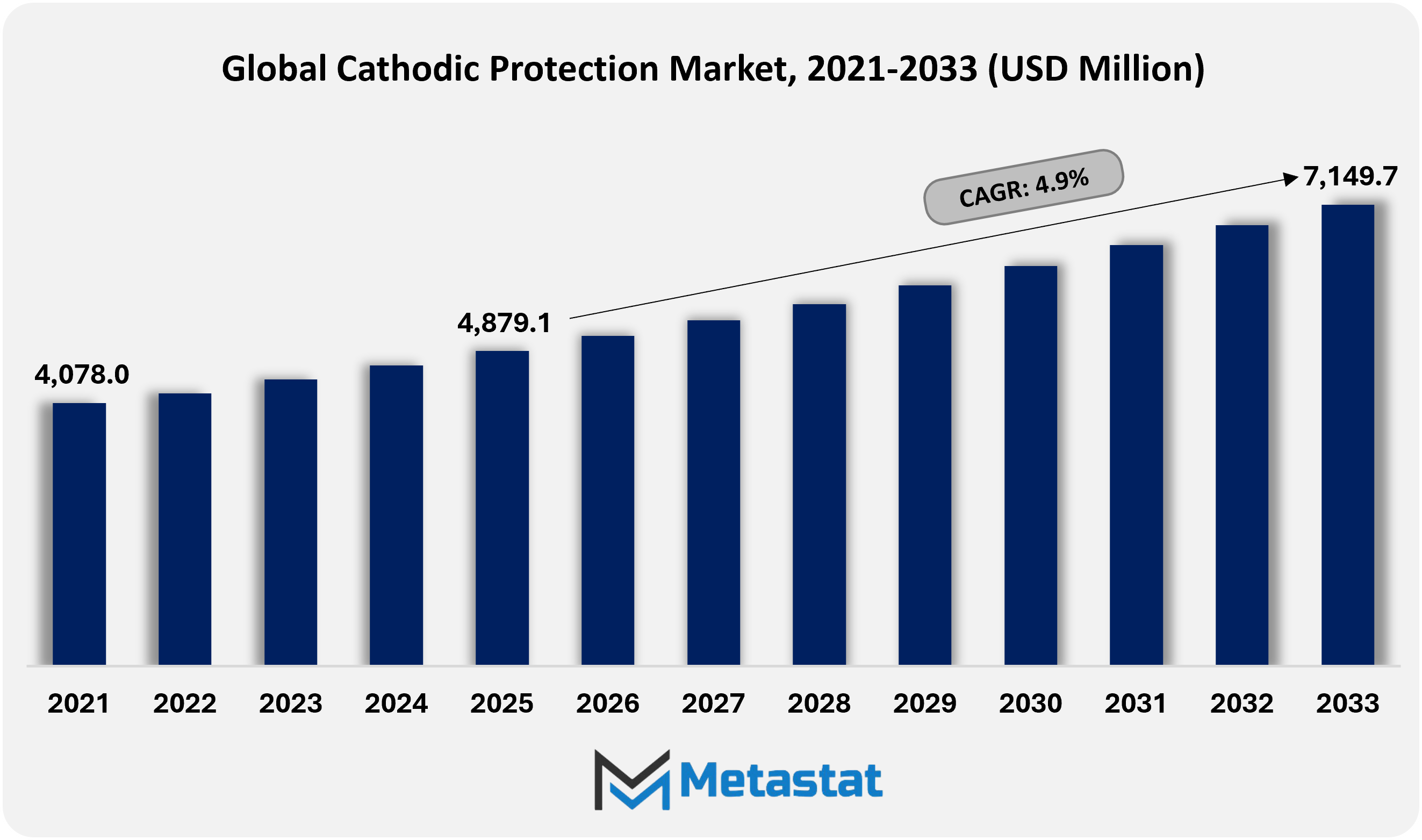

Global Cathodic Protection market size is valued at USD 4,879.1 million in 2025 and projected to grow at a CAGR of 4.9% during the forecast period, reaching USD 7,149.7 million by 2033.

Global Cathodic Protection Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

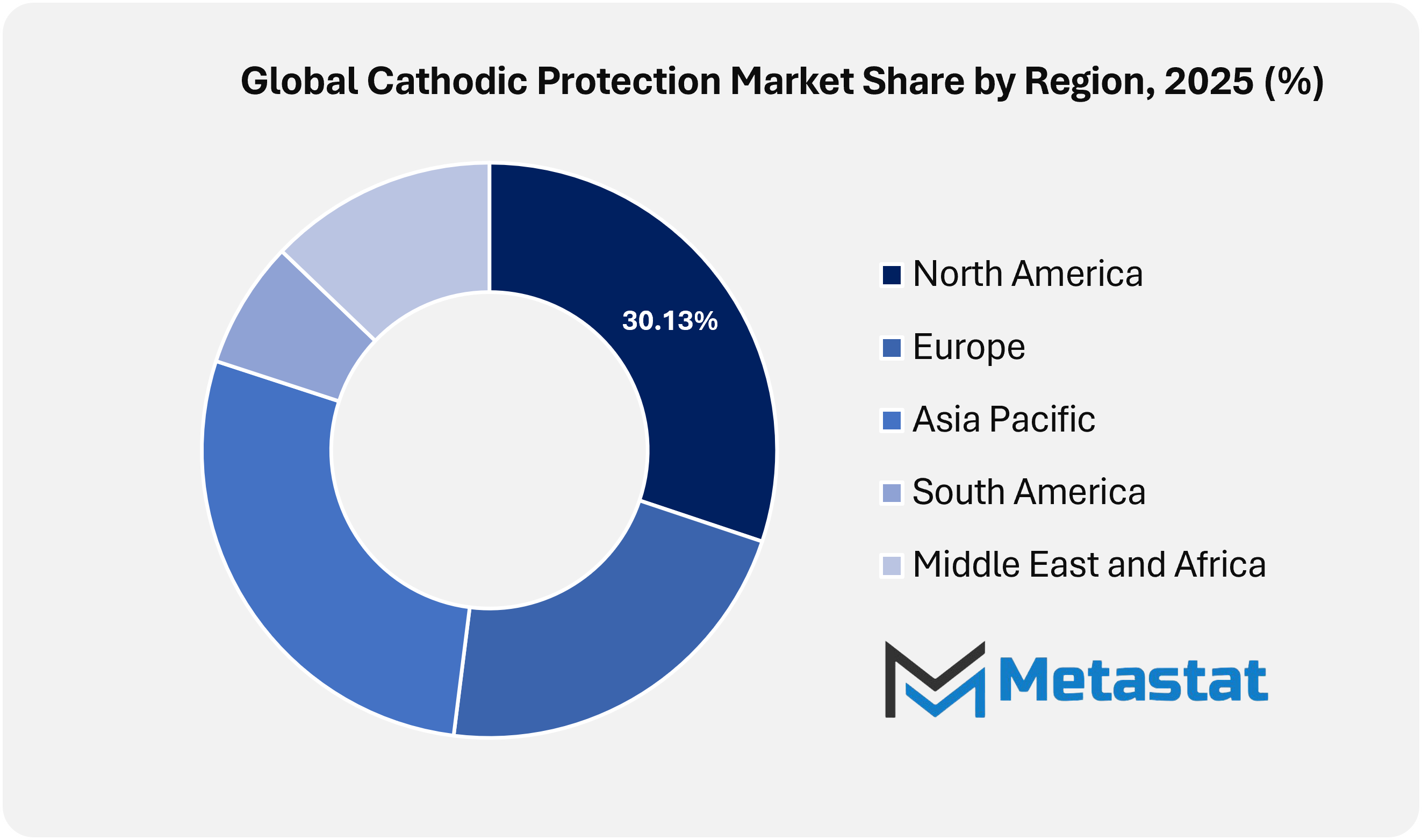

North America holds 30.1% of the global market in 2025, with the U.S. leading the regional market.

Galvanic (Sacrificial Anodes) Cathodic Protection segment accounts for a 41.9% market share in 2025.

Key trends driving growth include increasing investments in infrastructure maintenance and aging asset integrity programs, along with stringent government regulations and industry standards mandating corrosion prevention across oil & gas, water, and utilities.

Opportunities include integration of digital monitoring, remote IoT-based inspection solutions, and predictive analytics in cathodic protection offers new avenues for enhanced operational efficiency, cost-effective maintenance, and real-time corrosion management.

Key insight: Global Cathodic Protection Market is gaining momentum through rising demand for infrastructure longevity and expanding energy networks across oil & gas, marine, and utilities sectors.

Global Cathodic Protection Market will expand beyond conventional pipeline and offshore asset protection, reshaping how long-term infrastructure durability is planned across critical industries. The market is shifting from reactive maintenance toward predictive corrosion management supported by sensor-based monitoring across steel, concrete, and composite structures. Engineers are increasingly combining real-time potential measurements with cloud-based monitoring dashboards, enabling remote calibration of rectifiers and sacrificial anode systems with improved efficiency and reduced field service requirements.

Urban infrastructure projects will adopt cathodic protection systems at a broader scale across bridges, metro tunnels, desalination plants, and underground utility networks. Asset owners are prioritizing lifecycle optimization, which is shifting procurement models toward performance-based service contracts focused on long-term structural durability. In parallel, autonomous inspection drones and robotic crawlers are improving evaluation of coating degradation, stray current interference, and polarization efficiency, enabling maintenance cycles to be scheduled with data-backed precision.

Market Dynamics

Growth Drivers:

Increasing investments in infrastructure maintenance and aging asset integrity requirements motivate the adoption of cathodic protection solutions as owners seek long-term corrosion mitigation and regulatory compliance.

Rising investment in infrastructure maintenance and aging asset integrity programs is supporting steady expansion of the Global Cathodic Protection Market. Large transportation networks, pipelines, storage tanks, and utility grids require corrosion control systems that extend service life and protect long-term capital investment. Asset owners are increasingly adopting structured asset integrity frameworks to reduce failure risk, lower liability exposure, and maintain operational continuity.

Stringent government regulations and industry standards mandating corrosion prevention in critical sectors such as oil & gas, water, and utilities prompt higher adoption of cathodic protection systems.

Stringent government regulations and industry standards governing corrosion prevention across oil & gas, water, and utilities are accelerating adoption of cathodic protection systems and reinforcing compliance-driven market growth. Regulatory authorities continue to enforce stricter inspection cycles and documentation requirements, compelling operators to implement certified corrosion mitigation programs. Industrial operators are aligning infrastructure strategies with evolving safety benchmarks to avoid penalties and sustain long-term project approvals.

Restraints and Challenges:

High upfront installation and ongoing maintenance costs for cathodic protection systems, especially for large and complex infrastructure projects, can deter potential buyers and slow market growth.

High upfront installation and ongoing maintenance costs remain a major challenge for cathodic protection system deployment, particularly across large and complex infrastructure projects. Capital-intensive requirements involving deep-ground anodes, rectifiers, cables, and monitoring equipment can place pressure on project budgets. Smaller operators will delay system upgrades or limit deployment scope owing to funding constraints and extended payback periods.

Shortages of skilled professionals and technical expertise in designing, implementing, and maintaining CP systems limit widespread adoption and effective deployment.

Limited availability of skilled professionals with expertise in corrosion engineering, system design, and field calibration can restrict effective deployment of cathodic protection systems. Technical capability gaps often affect installation quality, monitoring accuracy, and long-term performance. Stronger training programs and certification standards remain important for reliable system implementation across industrial applications.

Opportunities:

Integration of digital monitoring, remote IoT-based inspection solutions, and predictive analytics in cathodic protection offers new avenues for enhanced operational efficiency, cost-effective maintenance, and real-time corrosion management.

Integration of digital monitoring, remote IoT-based inspection, and predictive analytics is creating strong growth opportunities in the Global Cathodic Protection Market. Advanced sensors, connected dashboards, and automated alerts enable continuous asset monitoring and faster fault detection. These capabilities support cost-effective maintenance planning, reduced unplanned shutdowns, and improved long-term infrastructure resilience.

Market Segmentation Analysis

The Global Cathodic Protection market is classified based on Type, Component, Service, and Application.

By Type, the market is further segmented into:

Galvanic (Sacrificial Anodes) Cathodic Protection

Galvanic (Sacrificial Anodes) Cathodic Protection segment is valued at USD 2,143.4 million in 2026 and is projected to reach USD 2,779.8 million by 2033, at a CAGR of 3.8% during the forecast period.

Galvanic cathodic protection systems will maintain strong adoption across aging infrastructure networks owing to their simple configuration and limited dependence on external power sources. Pipeline replacement programs and asset rehabilitation projects are supporting demand across both developed and emerging markets. Cost-effective corrosion control across remote and distributed sites will continue to strengthen use of sacrificial anode systems.

Impressed Current Cathodic Protection

Impressed Current Cathodic Protection segment is valued at USD 2,969.7 million in 2026 and is projected to reach USD 4,369.9 million by 2033, at a CAGR of 5.7% during the forecast period.

Impressed Current Cathodic Protection systems will witness stronger deployment across large-scale industrial assets that require controlled and continuous protection levels. Advances in rectifier technology and remote monitoring are improving system precision and operating efficiency. High-value assets such as offshore platforms, storage terminals, and long-distance pipelines will continue to support demand for impressed current solutions.

By Component, the market is divided into:

Anodes

Anodes segment is projected to reach USD 2,112.7 million by 2033, at a CAGR of 4.5% during the forecast period.

Anodes will remain a core component of cathodic protection systems, with material innovation improving durability, current output, and service life. Mixed metal oxide and high-silicon cast iron variants are gaining wider use across demanding operating environments. Infrastructure rehabilitation and new installation activity will continue to support steady demand for anode products across multiple end-use sectors.

Power Supplies

Power Supplies segment is projected to reach USD 1,096.8 million by 2033, at a CAGR of 5.4% during the forecast period.

Power supplies will advance through the adoption of energy-efficient rectifiers, automated controls, and smart monitoring features. These systems play a critical role in maintaining stable output across impressed current applications. Growing emphasis on system efficiency and remote supervision is supporting integration of intelligent power management solutions across industrial assets.

Reference Electrodes

Reference Electrodes segment is projected to reach USD 5,48.4 million by 2033, at a CAGR of 4.3% during the forecast period.

Reference electrodes remain essential for accurate potential measurement and performance verification in cathodic protection systems. Continuous monitoring requirements are supporting demand for reliable, long-life electrode materials across pipelines, tanks, and reinforced concrete structures. Greater focus on compliance and asset integrity is increasing the importance of precise voltage assessment tools.

Cables

Cables segment is projected to reach USD 697.1 million by 2033, at a CAGR of 4.3% during the forecast period.

Cables are evolving with better insulation strength, mechanical durability, and resistance to harsh environmental conditions, supporting reliable current distribution across cathodic protection systems. Growth in offshore, underground, and industrial infrastructure is increasing installation requirements. Long operational life and dependable field performance will remain key purchase criteria.

Monitoring Systems

Monitoring Systems segment is projected to reach USD 1,017.4 million by 2033, at a CAGR of 7.1% during the forecast period.

Monitoring systems are emerging as a high-growth component segment owing to rising adoption of digital sensors, cloud connectivity, and predictive analytics. These solutions improve visibility into corrosion performance and support faster operational decisions. Expansion of remote infrastructure networks is further supporting demand for real-time monitoring capabilities.

Others

Others segment is projected to reach USD 1,677.3 million by 2033, at a CAGR of 4.4% during the forecast period.

Auxiliary components such as junction boxes, test stations, connectors, and related accessories remain important for overall system reliability and performance. Standardization efforts are improving product quality across supply chains and supporting more efficient installation practices. Continued focus on simplified maintenance and long-term operational continuity will support this segment.

By Service, the market is further divided into:

Design & Engineering

Design & Engineering segment is projected to reach USD 1,500 million by 2033.

Design and engineering services will expand through greater use of customized corrosion modeling, site assessment, and risk-based planning frameworks. Infrastructure modernization and asset integrity programs require detailed technical evaluation before system deployment. These services support better lifecycle cost control and stronger compliance alignment.

Installation & Construction

Installation & Construction segment is projected to reach USD 2,307.2 million by 2033.

Installation and construction services will grow with pipeline expansion, storage facility development, and utility infrastructure upgrades. Execution quality, project scheduling, and skilled labor availability remain critical to successful deployment. Large-scale capital projects will continue to support steady service demand across this segment.

Inspection & Monitoring

Inspection & Monitoring segment is projected to reach USD 1,690.2 million by 2033.

Inspection and monitoring services are shifting toward data-driven assessment supported by digital reporting, remote diagnostics, and condition-based analysis. Regulated industries are placing greater emphasis on compliance audits and performance validation. These trends will sustain demand for ongoing system evaluation and asset integrity assurance.

Maintenance & Repair

Maintenance & Repair segment is projected to reach USD 1,652.3 million by 2033.

Maintenance and repair services remain essential for extending infrastructure life through timely component replacement, recalibration, and corrective intervention. Preventive maintenance strategies help reduce long-term corrosion risk and improve system effectiveness. Stable recurring demand is expected through service contracts tied to critical infrastructure assets.

By Application, the Global Cathodic Protection market is divided as:

Oil and Gas Transmission Pipelines

Oil and Gas Transmission Pipelines segment is projected to grow at a CAGR of 4.6% during the forecast period.

Oil and gas transmission pipelines represent a major application area owing to continuous corrosion exposure across extensive network systems. Expansion of cross-border energy infrastructure and stricter integrity requirements are supporting system deployment. Cathodic protection remains critical for reducing leakage risk, improving safety, and maintaining regulatory compliance.

Storage Facilities

Storage Facilities segment is projected to grow at a CAGR of 4.4% during the forecast period.

Storage facilities, including tanks and terminals, require reliable corrosion mitigation to reduce contamination risk, protect structural integrity, and prevent environmental incidents. Rising investment in fuel, chemical, and bulk liquid storage capacity is supporting system installation. Modernization of storage infrastructure will continue to drive demand in this application segment.

Processing Plants

Processing Plants segment is projected to grow at a CAGR of 4% during the forecast period.

Processing plants require advanced corrosion control systems to protect operational continuity across chemically aggressive and high-temperature environments. Refineries, chemical plants, and industrial processing units are adopting stronger protection measures to reduce maintenance risk and unplanned downtime. Ongoing industrial expansion will support steady demand across this segment.

Water and Wastewater segment is projected to grow at a CAGR of 5.4% during the forecast period.

Water and wastewater infrastructure will see stronger adoption of cathodic protection systems owing to modernization of treatment plants, pipelines, and underground utility networks. Municipal investment programs focused on leakage reduction and infrastructure reliability are supporting deployment. Corrosion control is becoming increasingly important for long-term service continuity and asset performance.

Transportation

Transportation segment is projected to grow at a CAGR of 4.2% during the forecast period.

Transportation infrastructure, including rail systems, transit assets, and related structural networks, requires effective corrosion protection to maintain long-term reliability and safety. Urban expansion and mobility infrastructure upgrades are supporting new installation activity. Adoption is also increasing alongside smart city programs focused on durable public assets.

Bridges

Bridges segment is projected to grow at a CAGR of 6.3% during the forecast period.

Bridges represent a high-potential application segment owing to continuous exposure to moisture, salts, and heavy load stress. Government investment in infrastructure renewal and structural rehabilitation is supporting adoption of cathodic protection systems across steel and reinforced concrete assets. Long-term durability requirements will sustain deployment across this segment.

Others

Others segment is projected to grow at a CAGR of 6.3% during the forecast period.

Additional application areas such as marine structures, ports, harbor assets, and industrial foundations are broadening the use of cathodic protection technologies. Climate resilience planning and asset preservation strategies are increasing focus on corrosion mitigation across diverse infrastructure classes. This is supporting wider market diversification.

By Region:

Based on geography, the Global Cathodic Protection market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Cathodic Protection Market is set to expand at a CAGR of 4.9% within the forecast period, reaching a market size (TAM) of USD 2,019.8 million by the end of 2033.

In North America, ageing oil & gas pipelines and massive offshore infrastructure create sustained demand for advanced cathodic protection structures.

In North America, stringent regulatory requirements for corrosion manipulate across utilities and transportation networks accelerate adoption of cathodic safety answers.

In Europe, aging transport, marine, and utility infrastructure, combined with strict safety and environmental regulations, is supporting consistent demand for cathodic protection systems.

In Asia Pacific, fast expansion of business centers and go-border pipeline projects provides strong increase possibilities for cathodic safety providers.

In Asia Pacific, growing investments in marine ports, refineries, and concrete infrastructure aid new installations of cathodic protection technologies.

Across the Middle East, Africa, and South America, increasing oil manufacturing belongings, mining activities, and lengthy-distance pipeline networks pressure regular integration of cathodic safety systems to guard crucial infrastructure.

Competitive Landscape and Strategic Insights

The Global Cathodic Protection Market continues to gain steady traction as industries increase focus on protecting critical infrastructure from corrosion-related damage. Pipelines, storage tanks, marine systems, water treatment facilities, and reinforced concrete structures remain exposed to harsh operating environments, making corrosion prevention a strategic priority. Rising energy demand, expansion of oil and gas networks, and modernization of water and wastewater systems will support market growth across key regions.

Public and private infrastructure investment is playing an important role in shaping market expansion. Governments are upgrading aging pipeline networks and reinforcing bridges, ports, and industrial facilities to meet higher safety standards. At the same time, stricter inspection requirements are encouraging adoption of monitoring technologies that provide real-time performance visibility and improve compliance management.

Competition remains diverse, with specialized engineering firms and technology providers offering tailored corrosion control solutions across installation, maintenance, monitoring, and technical services. Companies such as Allied Corrosion Industries, Inc., Corrosion Service Company, Cor-Pro Systems, Inc., Farwest Corrosion Control Company, and SESCO focus on system deployment and field service capabilities. Product manufacturers including Cathtect USA, Inc., Galvotec Alloys, Inc., Houston Anodes, Inc., Jennings Anodes, Inc., and Borin Manufacturing, Inc. support the market through supply of anodes, monitoring equipment, and related components. Firms such as American Innovations, Ltd., OmniMetrix, LLC, and Mobiltex Data Ltd. strengthen the market through remote monitoring and asset performance solutions, while larger participants including Acuren Corporation, Mears Group, Inc., Xylem Inc., Industrie De Nora S.p.A., Lindsay Corporation, Azuria, and Nippon Corrosion Industry Co., Ltd. continue expanding through service integration and geographic reach.

Additional participants such as Tinker & Rasor, M. C. Miller Co., Inc., BAC Corrosion Control Ltd, Deepwater Corrosion Services, Inc., NIXUS International, Inc., Interprovincial Corrosion Control Company Ltd., General Transformer Corporation, Eastcom Associates, Inc., Vector Corrosion Technologies, Underground Testing & Response Services, Inc., CMP Europe, and Harger Lightning & Grounding strengthen the competitive environment through inspection tools, testing equipment, engineering design, and specialized solutions. As infrastructure networks expand and maintenance budgets receive higher priority, long-term contracts, performance-based service models, and digital diagnostics will shape competitive positioning across the market.

Forecast and Future Outlook

Market size is forecast to rise from USD 4,879.1 million in 2025 to over USD 7,149.7 million by 2033.

Academic institutions and technology startups will collaborate on corrosion modeling algorithms that simulate long-term electrochemical degradation with higher accuracy. Through digitization, sustainability initiatives, and performance-based contracting, the Global Cathodic Protection Market will reshape how long-term structural resilience is engineered and financed across global infrastructure ecosystems.

Cathodic Protection Market Key Segments:

By Type:

Galvanic (Sacrificial Anodes) Cathodic Protection

Impressed Current Cathodic Protection

By Component:

Anodes

Power Supplies

Reference Electrodes

Cables

Monitoring Systems

Others

By Service:

Design & Engineering

Installation & Construction

Inspection & Monitoring

Maintenance & Repair

By Application:

Oil and Gas Transmission Pipelines

Storage Facilities

Processing Plants

Water and Wastewater

Transportation

Bridges

Others

Key Global Cathodic Protection Industry Players

Allied Corrosion Industries, Inc.

Corrosion Service Company

Cor-Pro Systems, Inc.

Farwest Corrosion Control Company

SESCO (Schmoldt Engineering Services Company)

Cathtect USA, Inc.

Lindsay Corporation

Azuria

Acuren Corporation

Mears Group, Inc.

American Innovations, Ltd.

OmniMetrix, LLC

Mobiltex Data Ltd.

Xylem Inc.

Tinker & Rasor

M. C. Miller Co., Inc.

Galvotec Alloys, Inc.

Houston Anodes, Inc.

Jennings Anodes, Inc.

BAC Corrosion Control Ltd

Borin Manufacturing, Inc.

Industrie De Nora S.p.A.

Harger Lightning & Grounding

Deepwater Corrosion Services, Inc.

NIXUS International, Inc.

Interprovincial Corrosion Control Company Ltd.

General Transformer Corporation

Eastcom Associates, Inc.

Vector Corrosion Technologies

Underground Testing & Response Services, Inc.

CMP Europe

Nippon Corrosion Industry Co., Ltd

Report Coverage

This research report categorizes the Cathodic Protection market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Cathodic Protection market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Cathodic Protection market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 4.9% from 2026 to 2033

Revenue Unit

USD million

Segmentation

By Type, Component, Service, Application, and Region

By Region

North America (By Type, Component, Service, Application, and Country)

United States

Canada

Mexico

Europe (By Type, Component, Service, Application, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Type, Component, Service, Application, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Type, Component, Service, Application, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Type, Component, Service, Application, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Emerging Segments and Regional Growth Potential

Key Strategic Recommendations

Competitive Benchmarking

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

Top players operating in the Cathodic Protection industry include Allied Corrosion Industries, Inc., Corrosion Service Company, Cor-Pro Systems, Inc., Farwest Corrosion Control Company, SESCO (Schmoldt Engineering Services Company), and Cathtect USA, Inc.

High upfront installation and ongoing maintenance costs for cathodic protection systems, especially for large and complex infrastructure projects, can deter potential buyers and slow market growth. will hamper the market growth within the forecast period.

North America region dominates the market.

Global Cathodic Protection market is estimated to reach USD 7,149.7 million by 2033.

Increasing investments in infrastructure maintenance and aging asset integrity requirements motivate the adoption of cathodic protection solutions as owners seek long-term corrosion mitigation and regulatory compliance. and Stringent government regulations and industry standards mandating corrosion prevention in critical sectors such as oil & gas, water, and utilities prompt higher adoption of cathodic protection systems. are key driving factors, boosting the market.

The Impressed Current Cathodic Protection is the leading type segment in the Global market.

The Metastat Insights analysis shows that the North America Cathodic Protection market size is estimated to be USD 2,019.8 million by 2033.

The Metastat Insights study shows that the Global Cathodic Protection market size was USD 4,879.1 million in 2025.

The Global Cathodic Protection market is expected to grow at a CAGR of 4.9% over the forecast period (2026-2033).

Lubricants Manufacturing market size is valued at USD 151.1 billion in 2025 and projected to reach USD 208.4 billion by 2033, growing at a CAGR of 4.1%.

Vapor Degreasing Solvent market size is valued at USD 1,004.1 million in 2025 and projected to reach USD 1,576.4 million by 2033, growing at a CAGR of 5.8%.

Bangladesh Flavours and Fragrances Market Size, Share, Trends, 2033

Bangladesh Flavours and Fragrances market size is valued at USD 793.9 million in 2025 and is projected to reach USD 1,447.9 million in 2033, at a CAGR of 7.8% from 2026 to 2033

Bangladesh Flavours and Fragrances Market, Bangladesh Flavours and Fragrances Market Size, Bangladesh Flavours and Fragrances Market Share, Bangladesh Flavours and Fragrances Market Analysis, Bangladesh Flavours and Fragrances Market Growth, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market Research Report, Bangladesh Flavours and Fragrances Market Forecast, Bangladesh Flavours and Fragrances, Bangladesh Flavours and Fragrances Market Research, Bangladesh Flavours and Fragrances Industry, Bangladesh Flavours and Fragrances Industry Report, Bangladesh Flavours and Fragrances Market Data, Bangladesh Flavours and Fragrances Statistics, Bangladesh Flavours and Fragrances Market Statistics, Bangladesh Flavours and Fragrances Industry Trends, Bangladesh Flavours and Fragrances Market Report, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market News, Bangladesh Flavours and Fragrances Forecasts, Bangladesh Flavours and Fragrances Market Intelligence Report

Biocatalysis and Enzyme Biocatalysts Market Size, Share, Trends, 2033

Biocatalysis and Enzyme Biocatalysts market size is valued at USD 737.8 million in 2025 and is projected to reach USD 1,221.0 million in 2033, at a CAGR of 6.5% from 2026 to 2033.

Biocatalysis and Enzyme Biocatalysts Market, Biocatalysis and Enzyme Biocatalysts Market Size, Biocatalysis and Enzyme Biocatalysts Market Share, Biocatalysis and Enzyme Biocatalysts Market Analysis, Biocatalysis and Enzyme Biocatalysts Market Growth, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market Research Report, Biocatalysis and Enzyme Biocatalysts Market Forecast, Biocatalysis and Enzyme Biocatalysts, Biocatalysis and Enzyme Biocatalysts Market Research, Biocatalysis and Enzyme Biocatalysts Industry, Biocatalysis and Enzyme Biocatalysts Industry Report, Biocatalysis and Enzyme Biocatalysts Market Data, Biocatalysis and Enzyme Biocatalysts Statistics, Biocatalysis and Enzyme Biocatalysts Market Statistics, Biocatalysis and Enzyme Biocatalysts Industry Trends, Biocatalysis and Enzyme Biocatalysts Market Report, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market News, Biocatalysis and Enzyme Biocatalysts Forecasts, Biocatalysis and Enzyme Biocatalysts Market Intelligence Report