MARKET OVERVIEW

The global carbon fiber market is expected to continue shaping the industrial landscape abruptly, ranging far beyond its traditional frontiers. This industry is consistent in properties of producing light yet highly strong materials, yet it is going beyond the aerospace or automotive sectors. This will be an influence that branches out into former domains that were considered unrelated or impractical for application of carbon fiber. There is a technology that has made the strength-to-weight ratio of carbon fiber attractive for planes and race cars, and this will be a door opening where performance, efficiency, and design flexibility are critical.

Soon, the architecture and construction sectors will also find out that carbon fiber can address structural reinforcement and aesthetic expression. The bulkiness won't always appeal to engineers and architects if cities thrive and sustainability proves to be more than just a buzzword for attention. With its excellent resistance to corrosion and the ability to support heavy loads without deformation, carbon fiber will soon become a material of choice for bridges, towers, and possibly even houses. The global carbon fiber market will increasingly attract companies that are into long-term cost savings and low-maintenance infrastructure.

Another major change is expected in the domain of consumer electronics. Devices will continue to evolve in terms of growing slimmer, lighter, and more mobile, but functions of robustness will soon be more engraved on the products by the manufacturers. By then, carbon fiber would be the metal and plastic alternative that one might find, especially in premium phones, laptops, and wearables. The tactile graces and sleek profile of carbon fiber would smother such creations with a rich touch, a very new vernacular for brands to speak with their audiences. The global carbon fiber market will not just quietly enter into daily life as a utility material but also becomes a signature in terms of design.

Another surprising contribution to furthering this market, medical technology, will provide thin prosthetics and orthopedic implants made almost exclusively from carbon fiber for its contribution to comfort and strength. Hospitals and rehabilitation centers will view the pre-made product as custom equipment, carbon composites, which aim at improving mobility and decreasing recovery times. Including tools and devices, carbon fiber will make surgical instruments reduce surgeon fatigue since they are much lighter and balanced in handling.

As industries become more digitally connected, the energy sector will also experiment with carbon fiber-based components in wind turbines and underwater pipelines. Due to its flexibility under pressure and varying temperatures, it performs in hostile environments. Thus, the global carbon fiber market will slowly start growing a reputation in the renewable energy infrastructure that requires such efficient and long-lasting materials to address environmental objectives.

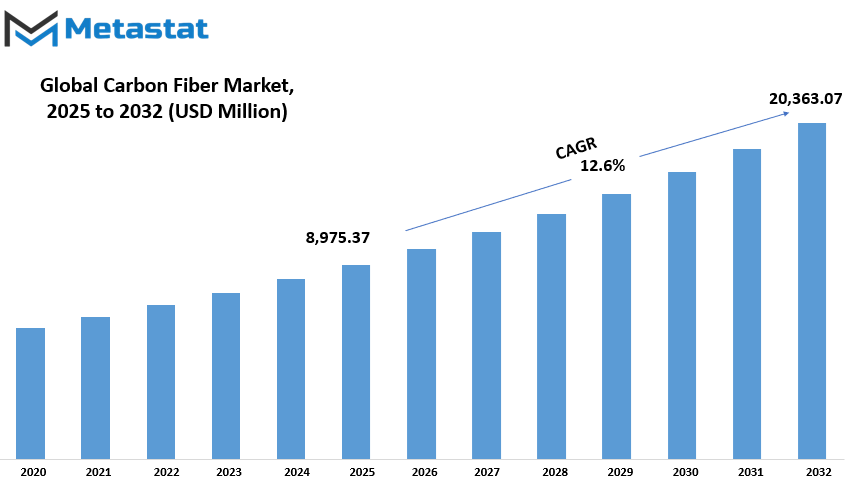

Global carbon fiber market is estimated to reach $20,363.07 Million by 2032; growing at a CAGR of 12.6% from 2025 to 2032.

GROWTH FACTORS

Two principal causes define the burgeoning global carbon fiber market. First, there is an upsurge in demand for lightweight, fuel-efficient materials in the aerospace and automotive industries. These industries are constantly trying to reduce weight as that directly translates to lowered fuel consumption and better overall performance. Carbon fiber thus suits it due to its lightness and strength. Secondly, there is an increase in the use of carbon fiber in renewable energy, with wind turbines being the major focus. Wind turbine blades need to be strong but also light and durable; carbon fiber has all these properties. The demand for carbon fiber is also rising in the domain as investments in green energy are made by more and more countries.

The huge potential notwithstanding, there are pockets of impediments that have slowed the full growth of the industry. One of these challenges is the high production cost of carbon fiber. High energy and time costs for production make carbon fiber expensive. For industries where low cost is of utmost importance, general manufacturing or consumer goods, these prices become a problem. So high carbon fiber prices often mean that performance-advantaged options often come up against stiff resistance in areas like aerospace with a very low level of price tolerance: Carbon fiber is still an option in many cases; less likely to be included." Another item of concern is carbon fiber's hard recycling. Metals are easy to recycle, and plastics are not that difficult; carbon fiber has complex procedures that require breaking down and recycling. These pose problems for companies trying to comply with environmental and sustainable targets because they need to look for means to deal with waste that is hardly manageable.

But with these hurdles comes some rays of hope. Researchers and companies are now developing low-cost, environmentally friendly carbon fiber and recycling processes. If they achieve success, carbon fiber may become more available to a wider variety of industries. This will boost the market for carbon fiber and provide long-term benefits for the environment. The prospect of recycling carbon fiber for end-use in products such as sports goods, automotive parts, and construction materials represents another avenue for expansion. With the development of these technologies, the market is expected to flourish with both demands and better solutions in the coming years.

MARKET SEGMENTATION

By Raw Material

The global carbon fiber market is gaining steadily since it can be utilized increasingly in various industries. One of the major driving factors for the market is the need for strong yet lightweight materials. This is exactly what carbon fiber is and thus becomes an important material considering industries such as aerospace, automotive, construction, and sports equipment. Manufacturers will find an answer to concerns over strength without heavy weight, so preference for using carbon fiber comes up naturally. This will help save energy, improve efficiency, and overall performance, particularly in vehicles and aircraft when lighter means less fuel consumption.

The quality and application of Carbon Fiber majorly depend on the type of raw material used for its production. The global carbon fiber market is divided into PAN Based Carbon Fiber, Pitch Based Carbon Fiber and Rayon Carbon Fiber. Among these, PAN Based Carbon Fiber has the lion's share with a market value of $8,284.90 million. This is because it is preferred as a high strength and stiff material. PAN or polyacrylonitrile allows a much more controlled manufacturing process, leading to better consistency and reliability of the end product. Pitch Based Carbon Fiber is also used mainly in applications requiring high thermal conductivity, such as heat-resistant materials or some aerospace components. On the other hand, Rayon Carbon Fiber is currently not much used but is still there in some specialized fields. However, such strands are not significant regarding the market size.

Carbon fiber is also believed to be an enabling material for sustainability. That is, it helps to make lighter vehicles other than the complementary elements in the car that have also seen reduced weight. These developments are forcing industries to shift from conventional forms of operation into more eco-friendly approaches. In fact, this redirection has initiated heightened consideration over carbon fiber not only in matured countries but also from developing economies where industries are expanding and modernizing. In addition, continuous invention in manufacturing and technology of carbon fiber should lower the prices over time, thereby benefiting from the viability.

In a nutshell, the global carbon fiber market will always remain optimistic as industries across the world are investing more in such materials for strength and durability while also keeping weight to a minimum. The market will become innovative as well as more widely used in years to come, with PAN Based Carbon Fiber leading the way.

By Tow Size

The global carbon fiber market classification is of course best understood using tow size. Tow does refer to the number of filaments that are bundled together along the strand of carbon fiber. Based on tow size, the market can be classified into small tow and large tow. Generally, small tow represents those having up to 24,000 filaments and tends to be high performance. These are mainly used for the applications where strength and stiffness come into great importance, such as aerospace, automotive parts, and high-end sporting goods. Due to small-tow carbon fiber, a certain degree of exactness and reproducibility is maintained when quality and reliability can never be compromised. When dealing with industries where stringent specifications are set, manufacturers favor this kind of carbon fiber because of its control and performance under stress.

Conversely, large tow refers to bundles having more than 24,000 filaments and finds application in processes requiring high volume but not necessarily the utmost strength. It finds application in areas where cost saving and mass production are heavier considerations than premium performance: wind energy, civil construction, and infrastructure. The one key attribute of large-tow carbon fiber is offering lower cost per unit, allowing larger projects to consider it or larger components that do not need extremely high precision. Allowing for faster production speeds and therefore helping to meet the increased demand in these sectors.

Broadly, tow sizes will have their unique strengths and selected according to end product requirements. While small tow means a very attractive mechanical property, large tow opens a path for mass production with cost savings precedence. Demand for both segments is growing with increased applications for carbon fiber in enterprising fields. As different industries continue to seek lighter, stronger, and more energy-efficient materials, both small and large tow options become more significant. The call for reducing weights while retaining durability has made the material carbon fiber widely acceptable, while understanding tow size helps many industries select the right applicable variety for their particular utility.

Market trends appear to forecast growth for both tow sizes, with each being propelled by specific industry demands. As the industrial disposition and manufacturing processes improve, it is also expected that large tow quality would scale up and catch up in some respects with small tow. This balance of performance and cost would shape the overall trajectory for the global carbon fiber market over the coming years.

By Application

The global carbon fiber market exhibited remarkable growth because of varied applications in several industries. One prominent driver for this growth is the increasing demand for materials that are strong yet lightweight. Carbon fiber fits right into this criterion in several industries such as automotive and aerospace because of its excellent strength-to-weight ratio. The accent regarding the carbon fiber application has been toward reducing vehicle weight in recent years for improved fuel consumption and less emission. Lighter cars accelerate faster and exert lesser strain on the engine, which is gaining prominence considering the strict environmental demands and fuel-consumption standards weighing on industry.

Carbon fiber is used in the aerospace and defense industry for parts required to handle considerable pressure and stress with minimal weight. It serves well to fabricate aircraft components like wings, tails, and fuselage sections. Given that aircraft need to be reasonably strong yet extremely light if they are to fly efficiently, carbon fiber fits the bill. Added strength translates to safety, while durability means less maintenance.

A major area that is now being increasingly opened up for carbon fiber application manufacturing is wind energy. Long, light, and strong turbine blades ensure good functional performance and long lifetimes in the field under severe weather conditions. Wind turbine performance in terms of above-mentioned functional stipulations would have an incentive if carbon fiber is extensively used since the world is currently driving towards cleaner energy.

The main application for carbon fiber in aerospace and defense includes other leisure implements such as bicycle, tennis rackets, and golf clubs. Lightweight, easy to handle, and strong enough for everyday use - it is precisely for these reasons that athletes prefer carbon fiber. Construction has also utilized carbon fiber to a large extent, particularly in designing bridges and buildings that require lightweight, yet strong components. Repair and strengthening of the older buildings, plus assist renovation, are on various applications of carbon fiber.

Molding and compound applications use carbon fiber due to its workability and ductility, creating custom designs possibly adapted into different tools and product parts. In pressure vessels, carbon fiber is also in use; these are containers that hold any gas or liquid under high pressures. These vessels require a material that cannot easily chip off or leak, which is exactly what the safety and reliability of carbon fiber prove to support.

The applications of carbon fiber continue to broaden in parallel with new industries discovering carbon fiber benefits. Any industry with great demand for strength without an increase in weight finds carbon fiber at the top of their list.

|

Forecast Period

|

2025-2032

|

|

Market Size in 2025

|

USD 8,975.37 Million

|

|

Market Size by 2032

|

USD 20,363.07 Million

|

|

Growth Rate from 2025 to 2032

|

12.6%

|

|

Base Year

|

2024

|

|

Regions Covered

|

North America, Europe, Asia-Pacific, South America, Middle East & Africa

|

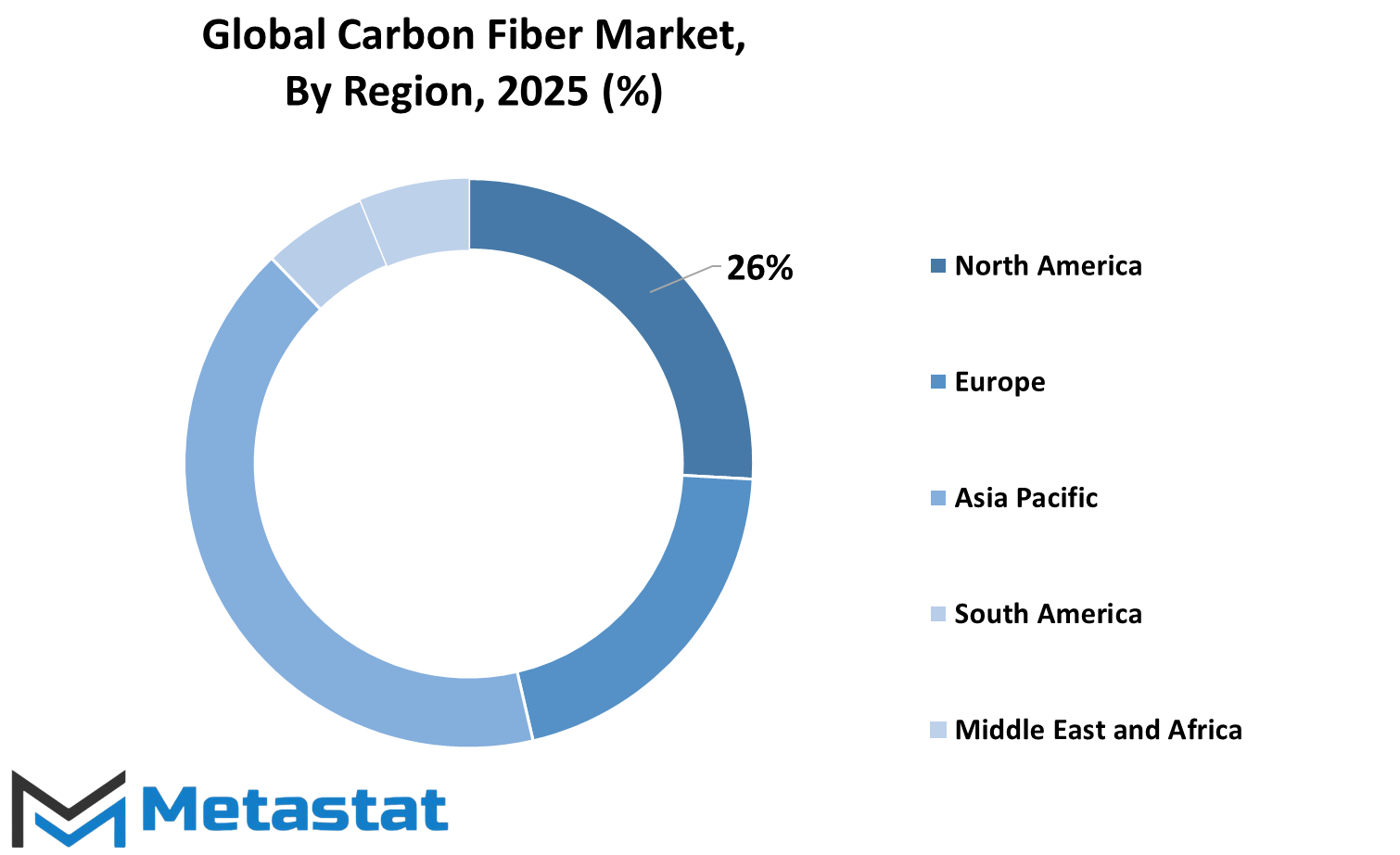

REGIONAL ANALYSIS

Geographically, the global carbon fiber market is divided into five major regions, namely North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Each region contributes uniquely to its growth and applications in consideration of its industrial growth, technological improvement, and demand from different sectors. Included in the North American region are the United States, Canada, and Mexico. Being a leader in aerospace and defense, the U.S. tops the list of potential markets for carbon fiber due to its high consumption for aircraft and automotive product manufacturing.

The European markets consist of the UK, Germany, France, Italy, and the Rest of Europe. Germany and the UK possess strong automotive and, therefore, construction sectors, continuously increasing the demand for carbon fiber materials. Demand is further sustained by Germany's engineering know-how and investment in research. Likewise, helping the demand are the traditional industries of France and Italy in transportation and sports equipment.

The group encompasses India, China, Japan, South Korea, and the Rest of Asia-Pacific. Demand for carbon fibers has seen some of the highest growth rates on account of the advent of electric vehicles, aerospace development, and renewable energy projects. Well, China and Japan come first because of their strong manufacturing bases and considerable investment in new developments. India is fast catching up with more government support and increasing demand in the wind energy and automobile sectors. Research is also moving ahead in the use of carbon fiber in electronics and infrastructure in South Korea.

There are Brazil, Argentina, and the Remaining Set of South America. This region is still very much emerging in terms of carbon fiber application use; however, Brazil is becoming a significant player as it begins to catch developing interest in clean energy and industrial applications. Argentina has potential but has a small market compared with Brazil.

In the Middle East and Africa, the region is divided into GCC Countries, Egypt, South Africa, and the Rest of the Middle East and Africa. The GCC countries are forging ahead with plans catalyzed by efforts to diversify their economies into advanced materials. Egypt and South Africa are slowly but steadily exploring the application of carbon fiber in the construction and transportation sector. Each region in its unique way is contributing to the increasing usage and development of carbon fiber.

COMPETITIVE PLAYERS

One of the major reasons why this has led to increased demand is the application in electric vehicles. Cleansed energy of the world leads one to rely on the lighter and energy-efficient EVs, which make any possible use of materials like carbon fiber beneficial for the efficiency of energy usage in batteries and better overall performance.

Wind energy generation is yet another feature where carbon fiber plays its magic. Wind energy extraction using lighter and longer life turbine blades made of carbon fiber becomes more efficient in terms of energy thrifts. More and more countries are investing towards upgrading their new renewable sources of power, hence, the demand for materials such as carbon fiber is expected to increase for applications ranging from automotive engineering all the way to housebuilding.

These properties will engage carbon fiber with many industries as it provides them mechanical advantages, durability, and corrosion resistance so as to make the life of products significantly better. All these facts present carbon fiber as an excellent option for almost all sectors that strive for most durable and reliable raw materials. It can be quoted here that it can be costly as compared to conventional materials like steel or aluminum, yet in the long run, advantages outweigh the cost for many organizations.

Those companies and many other global names will play a major role in the global carbon fiber market. Some of the eminent ones that have to do with the carbon fiber market include Syensqo, DowAksa USA LLC, Formosa Plastics Corporation, Hexcel Corporation, Holding company Composite, Hyosung Advanced Materials, Jiangsu Hengshen Co. Ltd., Mitsubishi Chemical Corporation, Nippon Graphite Fiber Co. Ltd., SGL Carbon, Solvay, Teijin Limited, Toray Industries Inc., and Zhongfu Shenying Carbon Fiber Co. Ltd. These companies keep investing their resources in research and development to bring forth improved quality and applications of carbon fiber in several areas. Thus, costs for carbon fiber will keep declining for most applications as production becomes more efficient along with the advancement in technology.

A bright future is there for the global carbon fiber market. Initiatives for sustainability and higher performances most likely imply that carbon fibers will be part of the critical features of modern manufacturing and innovation in several industries together with other numerous bright materials.

Carbon Fiber Market Key Segments:

By Raw Material

- PAN Based Carbon Fiber

- Pitch Based Carbon Fiber

- Rayon Carbon Fiber

By Tow Size

By Application

- Automotive

- Aerospace & Defense

- Wind Turbines

- Sports/Leisure

- Molding & Compound

- Construction

- Pressure Vessel

- Others

Key Global Carbon Fiber Industry Players

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential