Used Cooking Oil Market Size, Share, By Source (HoReCa (Hotels, Restaurants, and Catering), Household Kitchens, and Food Processing Plants), By Application (Animal Feed, Bio Diesel, Oleochemicals, Soap and Detergent Manufacturing, Lubricants & Industrial Oils, Energy Generation, Cosmetics and Personal Care Products, and Other), By Distribution Channel (Direct Collection from Households, Aggregators, Middlemen, Waste Management Companies, Restaurants, and Commercial Contracts), By Form (Crude UCO and Filtered UCO), Industry Analysis, Growth, Trends, and Forecasts, 2026-2033

Report ID

MSI-4529

Published

January 17, 2026

Pages

260 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Market Overview

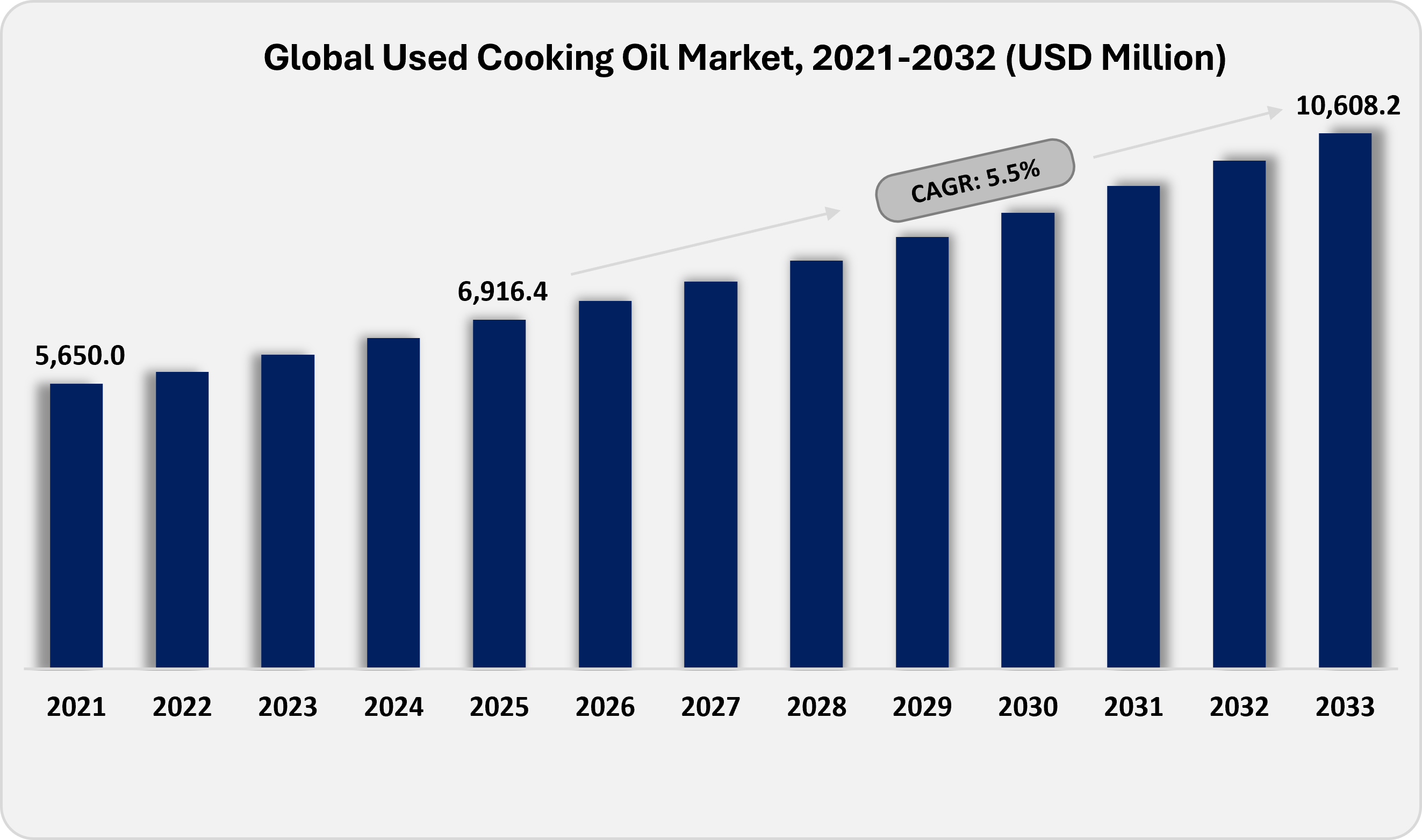

The global Used Cooking Oil market size was valued at USD 6,916.4 million in 2025. The market is projected to grow from USD 7,289.6 million in 2026 to USD 10,608.2 million by 2033, exhibiting a CAGR of 5.5% during the forecast period.

Global Used Cooking Oil Market - Comprehensive Data-Driven Market Analysis & Strategic Outlook

Global Used Cooking Oil market valued at USD 6,916.4 million in 2025, growing at a CAGR of around 5.5% through 2033, with potential to exceed USD 10,608.2 million.

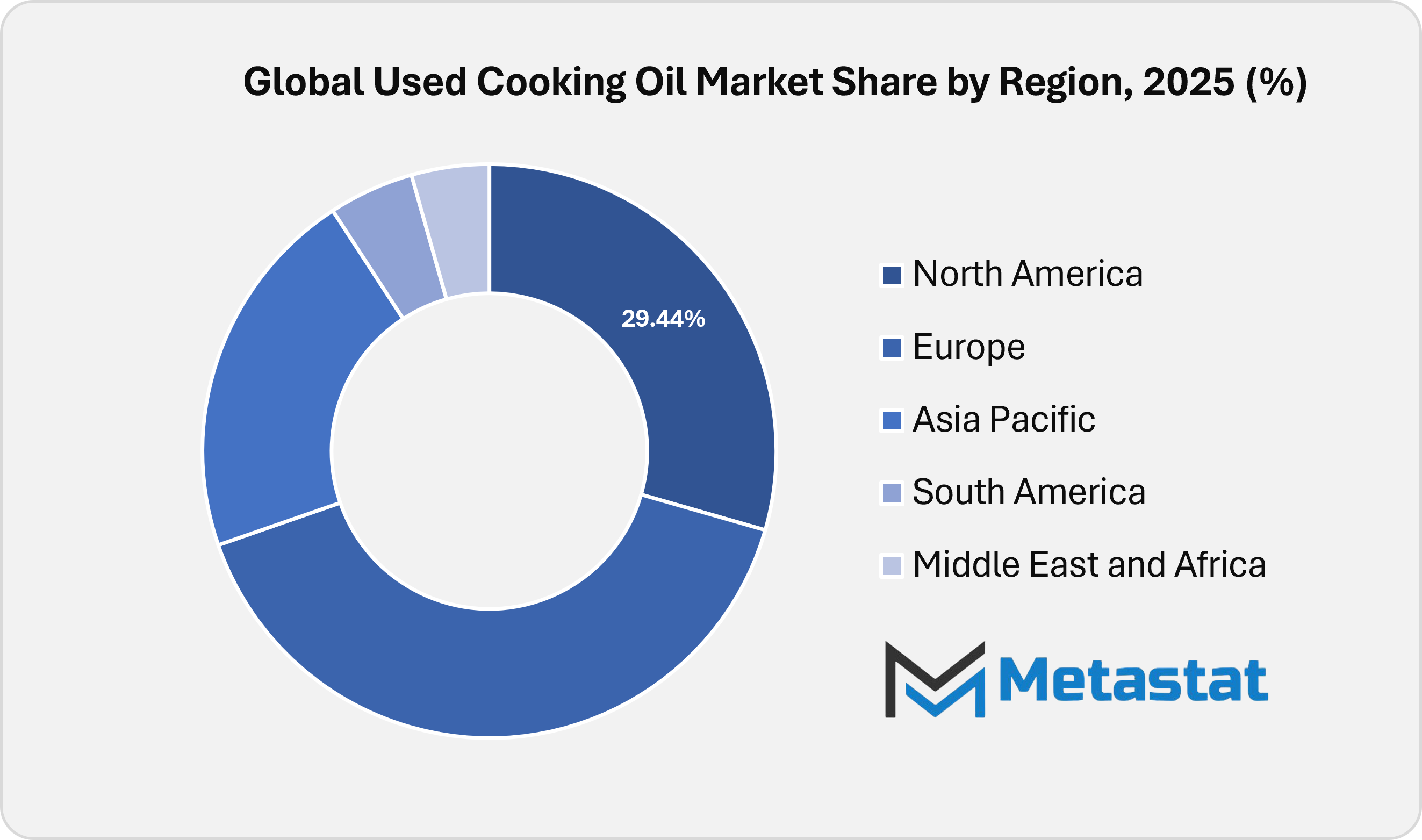

North America holds 29.6% in 2025 with US leading the market share in 2026.

HoReCa (Hotels, Restaurants, Catering) segment account for a market share of 54.3% in 2025, driven by properly separated UCO from other waste streams like water and solid food debris.

Key trends driving growth: Strong demand from the biofuel industry driven by renewable fuel mandates and corporate sustainability goals promoting waste-to-resource initiatives.

Opportunities: Increasing usage of UCO into higher value biochemicals such as bio lubricants and bio plastics.

Key insight: Urbanization and the expansion of quick-service restaurant chains in emerging economies are creating new, concentrated collection hubs and propelling the market growth.

The used cooking oil (UCO) market is primarily driven by its conversion into biodiesel and renewable diesel, fueled by global decarbonization mandates. In the European Union, where the Renewable Energy Directive sets binding targets, UCO is a key advanced feedstock. According to the European Biodiesel Board, around 1.2 million tonnes of used cooking oil (UCO) were collected domestically in 2022, with additional imports mainly from Asia to meet demand. The United States market is also policy-driven, with the Renewable Fuel Standard creating Renewable Identification Numbers (RINs) that provide an economic incentive. The United States Environmental Protection Agency found that in 2023, biomass-based diesel, including fuels from UCO, totalled approximately 10.3 million metric tonnes and UCO is becoming an increasingly bigger part of the total feedstock mix with other fats and oils.

Supply chain logistics and collection infrastructure are critical constraints of the market. The National Renderers Association states that U.S. renderers collect over 0.68 million tonnes of UCO per year from commercial sources. However, a significant amount still goes uncollected through formal channels. In economies like China and Indonesia, government initiatives are expanding formal collection networks to curb illegal diversion into animal feed, a practice banned in the EU since 2002. UCO prices are closely linked to regular vegetable oils like soybean and palm, usually running a bit cheaper to keep biodiesel blending profitable. Big players like Neste, Darling Ingredients, and Valero are all-in, locking down long-term UCO contracts for sustainable production across the years. The emphasis on building traceable and transparent supply chains which meet strict sustainability certification requirements is driving market growth in Europe and North America markets.

Market Dynamics

Growth Drivers:

Strong demand from the biofuel industry, driven by renewable fuel mandates.

The market is driven by government mandates for renewable fuel blends and steady demand. The availability of waste oils, a low-carbon feedstock is also a key catalyst in the growth landscape. Refineries are ensuring a steady supply of UCO to avoid missing of compliance targets. The collectors and processors are experiencing new growth opportunities owing to increased demand.

Companies are setting net-zero and circular economy targets to meet stakeholder expectations. Using recycled feedstocks reduces Scope 3 emissions and virgin material use, creates strategic partnerships and premium markets for waste oils, and turns a disposal cost into a sustainability asset.

Restraints & Challenges:

Complex and costly logistics for collection and purification.

Gathering waste oil from countless small sources like restaurants and factories is fragmented and inefficient process. Moreover, transporting low-density and hazardous material is expensive. The purification process which removes contaminants, requires significant energy and specialized equipment, squeezing profit margins of the processor. Waste oil collection from multiple small places like restaurants or factories is a complex process. It's scattered, inefficient, low-density, and hazardous, making transport expensive. Purifying UCO to remove contaminants hampers the process further and reduces the profit margins.

Contamination and inconsistent quality are affecting processing efficiency.

The UCO is generally not pure, it's usually mixed with water, food bits, or leftover lubricants. This factor impacts equipment and demands extra pre-treatment. Inconsistent feedstock quality hampers yield combined with refining costs will restraint the market growth.

Opportunities:

Expansion into higher value biochemicals like bio lubricants or plastics.

The specialty chemicals such as bio lubricants and bioplastics provide better opportunity owing to higher prices and better profit margins. It reduces the dependability on uncertain governments decisions on biofuels.

Market Segmentation Analysis

The global Used Cooking Oil market is mainly classified based on Source, Application, Distribution Channel, and Form.

By Source, the market is further segmented into:

HoReCa (Hotels, Restaurants, Catering)

Bigger sites are convent and biggest collection source for UCO. HoReCa sites enable efficient, quick, and scheduled pickups. The disposal rules enable businesses to co-ordinate and mange better collection across HoReCa industry. The segment is organized, with specialized renderers or biofuel companies fighting to lock down these arranged sources. Owing to disposal rules, efficient pickups, and managed collection, the segment is expected to garnet a considerable growth within the forecast period.

Household Kitchens

Individual volumes are smaller which results in increased per liter cost. Fundamental public awareness and easy drop-off points like special municipal bins are key pain points of this segment. Moreover, adulteration with water and other materials to increase the volume, is a key risk factor observed for this segment. Major collection happens through city waste programs and small recycling pilots. However, there's a huge untapped potential for this segment in the future as the key players will try to enhance and manage better operations for the collection process.

Food Processing Plants

Food Processing Plants produce big, steady batches that are often cleaner and more consistent than HoReCa industry. The collection deals are direct, long-term, and the plants appreciate having waste handled professionally. Occasionally, food processing plants get paid for their UCO instead of having to pay to dispose of it. This is the top-tier segment for collectors and biorefineries owing to easy logistics, large volumes, and clean raw materials.

By Application, the market is divided into:

Animal Feed

UCO is processed into feed-grade fats and calcium soaps for livestock. EU regulations restrict its use in feed due to contamination risks. It remains a significant market in regions with less stringent food-safety regulations such as Asia Pacific and South America. UCO competes directly with biodiesel for feedstock in these regions. Animal Feed is a lower-value outlet than fuel, offering less price support. Market demand in this segment is declining within premium and regulated markets.

Bio Diesel

UCO is a premier low-carbon feedstock for biodiesel production. It offers significant GHG savings under fuel mandates such as RFS and RED. The segmental demand is driven by policy and regulations, creating a stable, and high-volume offtake. The segments growth is directly tied to blending mandates and tax incentives.

Oleochemicals

UCO is split and processed into fatty acids, glycerin, and methyl esters. These serve as renewable building blocks for diverse industries such as oleochemicals. It offers a market diversification away from the volatile biofuels industry. Production requires consistent quality and specialized refining and commands higher margins than standard biodiesel when purified. This segment benefits from the broader shift toward increased demand for bio-based chemicals.

Soap and Detergent Manufacturing

Saponified used cooking oil is a key ingredient in industrial soaps and cleaning agents. The segment prioritizes low-cost, stable supply over sustainability credentials. It acts as a secondary market for lower-quality or contaminated UCO streams. It provides a baseline demand that absorbs supply that does not meet fuel standards. Innovation is limited, howerver, it's a traditional, volume-driven use, combined with thin and competitive margins will provide a secondary demand within the market.

Lubricants & Industrial Oils

Processed UCO is used to produce biodegradable lubricants for marine and forestry applications. It requires advanced refining and additive treatment for stability. Products command a significant price premium over petrochemical lubes. Environmental regulations in sensitive ecosystems will fuel the segment growth. It represents a strategic diversification into specialty chemicals. The segmental volume is expected growing owing to stricter ecological laws implementation.

Energy Generation

UCO can be directly burned in modified boilers for heat and power. This Application competes on cost with natural gas and other fuels. It is common for on-site waste disposal at large food processing plants. It lacks the policy-driven price support of transport fuel markets. It serves as a fallback option where collection for higher uses is not economical. It represents the lowest rung on the value ladder.

Cosmetics & Personal Care Products

Highly refined UCO derivatives, such as glycerin and fatty acids, are used in products like soaps and creams. The segment demands the highest purity and strictest safety certifications globally. The volume is lower compared to fuel markets but offers strong margins and new growth opportunities. The segment aligns with the brand's stories of natural and sustainable sourcing. Supply chains are distinct, often segregated from bulk fuel feedstock to maintain better output quality.

Other

The Others segment includes potential uses in bioplastics, asphalt additives, and animal bedding. These applications are in early-stage development and are on pilot scale. This segment represents future diversification pathways for the UCO value chain. Market viability depends on technological breakthroughs and cost competitiveness. This category highlights ongoing efforts to utilize full market potential across the globe. Current commercial impact is minimal but is expected to provide future opportunities for growth.

By Distribution Channel, the market is further divided into:

Direct Collection from Households

Collection requires significant public infrastructure, like municipal drop-off bins or curbside programs. Participation relies heavily on consumer awareness and convenience, making scaling difficult. High contamination risk from mixing with other household waste reduces the oil's value and processability. The segment represents a vast untapped supply pool. However, its unit economics are challenging owing to low volume per point and high collection costs. This channel is a long-term strategic bet on increasing total feedstock.

Aggregators / Middlemen

This segment is operated by local or regional operators which builds direct contracts with restaurants, caterers, and food processors. They provide containers, scheduled pickups, and basic filtration, acting as the first consolidation point. The segments growth hinges on dense route density and strong customer relationships. The aggregators sell collected oil to larger traders and pre-processors for better margin to enable local logistical service. This segment is highly competitive and fragmented, leading to ongoing consolidation. The segment is essential for accessing the fragmented HoReCa sector.

Waste Management Companies

Major waste management firms are adding UCO collection to their portfolios of commercial waste services. These companies provide a one-stop shop solution for businesses and creates synergies in collection routes. They can offer competitive rates by bundling services and have the scale to invest in preprocessing facilities. They typically act as large-scale aggregators, supplying directly to bio-refineries or major traders. Their involvement signifies the commoditization and professionalization of UCO as a waste stream.

By Form, the global Used Cooking Oil market is divided as:

Crude UCO

Crude UCO contains significant impurities like food solids, water, and other oils. The value of UCO is discounted for this segment owing to higher refining costs and processing risk for the buyer. Price is heavily dependent on Free Fatty Acid (FFA) content and moisture levels. Trading often occurs locally between collectors and initial aggregators and pre-processors. The crude UCO form is subject to the most significant quality inconsistencies and price volatility in the entire UCO market. It represents the base commodity before any value-added processing.

Filtered UCO

Filtered UCO undergoes physical removal of solids and water to meet basic contractual specifications. This preprocessing adds value and stabilizes quality for more extended storage and transport. It is the standard form for domestic and international trade between aggregators and large biorefineries. This segment commands a premium over crude UCO, reflecting the cost of filtration and quality assurance. The filtered UCO enables more efficient logistics and is typical feedstock for biodiesel (FAME) production. This Form establishes the benchmark price for the bulk UCO market globally.

By Region:

Based on geography, the global used cooking oil market is divided into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

North America Used Cooking Oil Market is set to expand at a CAGR of 5.5% within the forecast period, reaching a market size (TAM) of USD 3,119.9 million by the end of 2033.

The increasing demand for sustainable biofuels is driving growth in the North American Used Cooking Oil market.

The used cooking oil is increasingly being converted into biodiesel and other renewable fuels. Government incentives, carbon-reduction policies, and corporate sustainability commitments drive the collection and use of UCO, supporting demand in the energy and transportation sectors.

Increased regulatory support and waste management initiatives are expected to propel the North America market into a growth phase. The strict regulations over waste disposal and environmental compliance motivate restaurants, food processors, and households to recycle UCO rather than dispose of it improperly. This factor creates a structured collection ecosystem, improving supply availability for industrial and biofuel applications.

Expanding biodiesel and renewable energy markets are fuelling the growth in the Asia Pacific region. The rapid industrialization and growing energy demand is expected to open the drive the demand for UCO as an economical feedstock for biodiesel production. Governments renewables mandates and targets for reductions in emissions further improve adoption prospects in Asia Pacific.

Growing awareness of circular economy practices is creating new opportunities in the Asia Pacific for used cooking oil market. Consumers and businesses are increasingly aware of waste-to-value solutions which is propelling the market growth. The food service, hospitality, and industrial companies are seeking sustainable means to dispose of used cooking oil, creating opportunities for collection, processing, and resale.

South America, Middle East, and Africa regions are emerging as supply sources and consumer markets. Multiple countries in these regions have abundant UCO availability arising from high volumes of foodservice operations and street food industries. However, inadequate collection infrastructure, low awareness of recycling benefits, and logistical challenges will hamper the market growth in the near future. Investment in organized collection networks, local processing facilities, and regulatory frameworks can unlock significant growth and will help to boost the interest in renewable fuels and various sustainability initiatives across these regions. These factors will create longer-term prospects for structured UCO markets in South America, Middle East, and Africa regions.

Competitive Landscape & Strategic Insights

The global used cooking oil (UCO) market features a fragmented and dynamic competitive landscape, dominated by two primary tiers of players. Large-scale, vertically integrated aggregators and renderers such as Darling Ingredients and Baker Commodities, Inc., which leverage vast, established logistics networks to collect UCO at scale, primarily from the commercial HoReCa (Hotels, Restaurants, and Catering) sector and food processing plants.

Their competitive advantage stems from operational efficiency, long-term client contracts, and integrated waste processing capabilities. Parallelly, specialized UCO and biofuel-focused collectors like Olleco, Mahoney Environmental, and MBP Solutions compete through dense regional collection routes, value-added services, and stringent quality control to serve as critical feedstock suppliers. These players are increasingly pressured by intense demand from biofuel producers, driven by renewable fuel mandates like the U.S. RFS and the EU's RED II, which prioritize certified, traceable waste feedstocks.

The supply chain is further shaped by international traders and intermediaries such as Targray, Quatra, and Bio-Oil, which specialize in aggregating, certifying, such as ISCC EU, and transporting UCO across borders to meet demand in key bio-refining regions. Their role is crucial in ensuring sustainability compliance and managing complex logistics for UCO market. The market foundation consists of numerous regional and independent collectors, such as Eazy Grease, LLC, Lifecycle Oils, Tagaddod, and Aris BioEnergy, which possess deep local networks but often face margin pressure and consolidation. Strategic initiatives across the landscape focus on securing long-term supply agreements, investing in traceability systems to prevent fraud, and expanding into emerging high-supply regions. This environment is driving steady consolidation, as larger players acquire regional operators to secure feedstock. All key market players are expected to adapt rigorous sustainability and documentation standards set by major end-users in the renewable diesel and sustainable aviation fuel industries.

Forecast & Future Outlook

Market size is forecast to rise from USD 6,916.4 million in 2025 to over USD 10.60 billion by 2033.

Global UCO collection is forecast to grow significantly, propelled by ambitious renewable fuel mandates. The EU's Renewable Energy Directive III (RED III) maintains a high target for advanced biofuels, with UCO as a key feedstock. The U.S. Renewable Fuel Standard (RFS) and new incentives, such as the Sustainable Aviation Fuel (SAF) Tax Credits under the Inflation Reduction Act (IRA), create powerful, long-term demand pull from the renewable diesel and SAF sectors. This regulatory certainty, as outlined in government policy roadmaps, will continue to make UCO a critically scarce and sought-after commodity, supporting sustained price premiums over virgin oils.

This research report categorizes the Used Cooking Oil market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Used Cooking Oil market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Used Cooking Oil market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 5.5% from 2026 to 2033

Revenue Unit

USD million

Sales Volume Unit

Kilotons

Segmentation

By Source, Application, Distribution Channel, Form, and Region

By Source

HoReCa (Hotels, Restaurants, Catering)

Household Kitchens

Food Processing Plants

By Application

Animal Feed

Bio Diesel

Oleochemicals

Soap and Detergent Manufacturing

Lubricants & Industrial Oils

Energy Generation

Cosmetics & Personal Care Products

Other

By Distribution Channel

Direct Collection from Households

Aggregators / Middlemen

Waste Management Companies

Restaurants / Commercial Contracts

By Form

Crude UCO

Filtered UCO

By Region

North America (By Source, Application, Distribution Channel, Form, and Country)

United States

Canada

Mexico

Europe (By Source, Application, Distribution Channel, Form, and Country)

Germany

France

UK

Italy

Spain

Russia

Asia Pacific (By Source, Application, Distribution Channel, Form, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Source, Application, Distribution Channel, Form, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Source, Application, Distribution Channel, Form, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Used Cooking Oil Collection Rate (%), 2021-2025

Market Price Analysis, 2021-2025

Full in-depth analysis of the parent Industry

Important changes in market and its dynamics

Segmentation details of the market

Former, on-going, and projected market analysis in terms of volume and value

Assessment of niche industry developments

Market share analysis

Key strategies of major players

Emerging segments and regional growth potential

Market Volume in Kilotons across the regions and segments

Pricing Structure of Used Cooking Oil across various regions and countries

Key Future and Upcoming porjects within the sector

Kazakhstan Frozen Potato Products market size is valued at USD 26.4 million in 2025 and is projected to reach USD 53.0 million in 2033, at a CAGR of 9.0% from 2026 to 2033.

Switzerland Poke Food market size is valued at USD 29.2 million in 2025 and is projected to reach USD 44.5 million in 2033, at a CAGR of 5.5% from 2026 to 2033.

Netherlands Food and Beverages QA, QC, and Compliance Software Solutions Market Size, Share, Trends, 2033

Netherlands F&B QA, QC, and Compliance Software Solutions market size is valued at USD 272.5 million in 2025 and is projected to reach USD 421.3 million in 2033, at a CAGR of 5.6% from 2026 to 2033.

Netherlands F&B QA, QC, and Compliance Software Solutions Market, Netherlands F&B QA, QC, and Compliance Software Solutions Market Size, Netherlands F&B QA, QC, and Compliance Software Solutions Market Share, Netherlands F&B QA, QC, and Compliance Software Solutions Market Analysis, Netherlands F&B QA, QC, and Compliance Software Solutions Market Growth, Netherlands F&B QA, QC, and Compliance Software Solutions Market Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market Research Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Forecast, Netherlands F&B QA, QC, and Compliance Software Solutions, Netherlands F&B QA, QC, and Compliance Software Solutions Market Research, Netherlands F&B QA, QC, and Compliance Software Solutions Industry, Netherlands F&B QA, QC, and Compliance Software Solutions Industry Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Data, Netherlands F&B QA, QC, and Compliance Software Solutions Statistics, Netherlands F&B QA, QC, and Compliance Software Solutions Market Statistics, Netherlands F&B QA, QC, and Compliance Software Solutions Industry Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market News, Netherlands F&B QA, QC, and Compliance Software Solutions Forecasts, Netherlands F&B QA, QC, and Compliance Software Solutions Market Intelligence Report

Global Antibiotic-Free Pork market size is valued at USD 25,430.6 million in 2025 and is projected to reach USD 42,528 million in 2033, at a CAGR of 6.6% from 2026 to 2033