MARKET OVERVIEW

Rocket propulsion refers to the process of generating thrust through the expulsion of exhaust gases at high velocities to propel rockets forward. It is usually achieved by the combustion of chemical propellants that generate the forces pushing the rocket against gravity into motion. The principle behind this is Newton's Third Law of Motion, which states that for any action, there is an equal and opposite reaction. If a rocket expels gases in one direction, then it will move in the other direction. This simple yet mighty concept forms the basis for modern space exploration and myriad related applications.

Rocket propulsion plays a critical role in advancing human understanding of space. It has helped scientists and engineers launch satellites into orbit so that there could be communications, weather forecasting, and global positioning systems useful in everyday life. Additionally, it propels manned missions into space with the moon landing, and planning for future missions to Mars and beyond. These all point to rocket propulsion systems which need to be continually developed to become more efficient, reliable, and safe.

The military also employs rocket propulsion in many applications. Missiles with rocket propulsion are the critical ingredient of national defense and give what is considered the greatest degree of precision and range imaginable. Rocket technology is also used to support atmospheric studies in launching instruments that help acquire critical data on the pattern of weather and changes in the environment.

Rocket propulsion has been quite remarkable but presents challenges that need to be met. Chemical propellants have proven effective, but there is a negative environmental effect of the gases produced when launched. Further, building and maintaining these systems requires resources and technological know-how. The search for alternatives in the propulsion system continues, like electric and nuclear propulsion, that could mitigate these challenges and take the rockets further into space.

The propulsion rocket signifies the creativity and will of humankind in making impossible things possible. It has changed how people see their position in space with the opening of new frontiers and the practical use of space technology on Earth. This makes further innovation limitless because its challenges are being tackled through technology refinement.

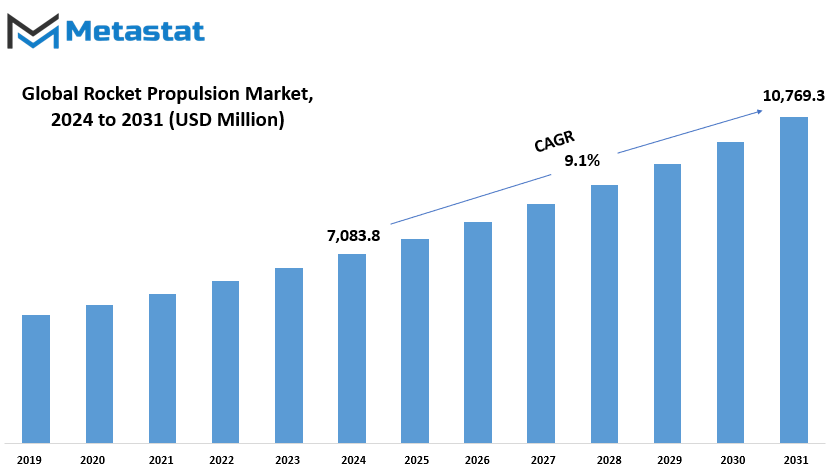

Global Rocket Propulsion market is estimated to reach $10,769.3 Million by 2031; growing at a CAGR of 9.1% from 2024 to 2031.

GROWTH FACTORS

The rocket propulsion market has been highly influenced by the increasing demand for satellite deployment for communication and defense. Satellites have become an essential tool in global communication networks, weather monitoring, navigation, and defense applications. The need for greater connectivity and enhanced national security measures has pushed the requirements for advanced rocket propulsion systems. In addition to that, increased investments in the exploration of space and commercialized space ventures have been seen as a significant factor towards speeding up the growth of this market. Governments and firms are investing heavily in exploring new technologies, which leaves room for healthy competition and evolution in the space sector.

Development and launching of a rocket propulsion system is expensive operations. This is one among the major challenges that many organizations will face. Such systems require high material inputs, intense research, and expert manpower, which imposes enormous financial costs. The same might limit the participation of smaller companies or developing countries from entering the market, hence reducing the overall level of participation. Additionally, rigid regulatory regimes and safety concerns also make rocket launches complicated. International standards compliance and the maintenance of safety during launches are crucial but can prolong projects and raise operating costs.

Despite these challenges, the reusable rocket technology is one of the most promising solutions to many of these challenges. Companies can cut the cost of launches drastically by reusing rockets. This innovation has already started changing the industry, opening up the doors for new players to join in and to further advance in space technology. With more focus on reusability, the approach aligns perfectly with sustainability goals, mitigating the growing concerns about space activities' environmental impact.

Through technological advancements and increased interest in the exploration of space, over the next few years, great opportunities are likely to develop for the rocket propulsion market. The industry is sure to expand its capabilities if all efforts are continually made in overcoming cost and regulatory challenges towards a wider range of applications. The integration of reusable technology and other innovations will not only reduce barriers but also inspire further investment and exploration, ensuring that the market continues to grow and adapt to evolving needs.

MARKET SEGMENTATION

By Propulsion Type

Propulsion is one of the main heavy dependency areas in space exploration and satellite deployment, as a propulsion system is necessary to overcome Earth's gravitational pull for spacecraft to make it away from Earth or to maneuver in space. The propulsion type is an important part of aerospace engineering, itself subdivided into categories with their specific advantages depending on the mission in view. These categories are chemical propulsion, electric propulsion, thermal propulsion, and advanced propulsion technologies.

The most traditional and widely used method is chemical propulsion. Chemical reactions are used to produce thrust, which usually delivers the high power required for launches and orbital adjustments. It has been used in many important missions, so it remains a reliable choice for most space agencies. However, chemical propulsion systems tend to have limitations in efficiency, especially when dealing with extended missions or deep-space exploration.

It is also distinguished with the easier fueling ability. The electric propulsion does not rely on chemical reactions, but it is actually propelled using electrically accelerated ions as a form of thrust generation. It is especially ideal for missions that call for gradual adjustments or long duration because it can save fuel during incremental acceleration of spacecraft. Although it cannot match the power output instantaneous as with chemical propulsion, its fueling makes it increasingly popular among satellites and interplanetary missions.

Thermal propulsion is a type where heating propellants to give thrust is integrated. Here, the heat from such sources as nuclear reactors or solar energy is applied to expand gases, forcing a spacecraft forward by the force generated. Thermal propulsion systems are one of the most promising propulsion systems that could be used in upcoming missions where energy efficiency is crucial. As this technology expands, it will be on the forefront of space traveling.

Advanced propulsion technologies represent the best efforts to push the boundaries of space exploration. These systems are designed to overcome the limitations of traditional methods, exploring new approaches, such as solar sails, fusion-based propulsion, or even antimatter. Many of these technologies are still in experimental stages, but they promise to revolutionize the way humanity approaches space exploration, making long-duration missions and interstellar travel possible.

Each propulsion type caters to a different need, so the preference will be for mission requirements such as distance, payload, and duration. As these systems continue to evolve and be perfected, the possibilities of reaching new vistas in space exploration are brightened to include potential discoveries thought previously impossible.

By Application

Satellites are now part of modern life. They offer crucial services, including communication, navigation, weather forecasting, and Earth observation. From real-time global communication to environmental change monitoring, satellites influence most aspects of daily living and decision-making. The industry is still growing because more countries and private organizations are investing in the latest satellite systems, with emphasis on efficiency and coverage.

Launch vehicles-the tools for sending payloads into orbit-form another very important category in the market. This has seen very significant technology advancements, hence making launching into space even cheaper and more efficient. Reusable launch vehicles have been some of the prominent ones, with their implementation bringing costs way down and encouraging more missions. This speaks to the industry's focus on innovation and sustainability.

Interplanetary missions, though still underdevelopment for most countries, stand as a symbol of what humanity can achieve. More than that, however, they are part of an effort to further research another planet and the possibilities of living matter. Such missions provide vital insight into science and technology for science and technology. Increased interest in missions among space agencies, research institutions, and private enterprises underlines this important aspect.

Space exploration, related closely to interplanetary missions, involves the study of space to understand the universe. The areas of space research include studying celestial bodies, resource searches, and the study of origins. This area of research has lately received public attention and investment, fueling further innovations.

The final, defense and military applications comprise a substantial part of the space market. Increasingly, countries apply space-based technologies to national security through surveillance, communication, and navigation systems. Such technologies boost defenses and form a key function in international security.

The market of space-related applications is fundamentally driven by innovation and collaboration between multiple sectors. It has been through the combined efforts of governments, private companies, and research organizations that continue to advance boundaries and bring new possibilities closer to reality, solidifying the role of space in defining the future.

By Component

The market, through its components, is divided into some major elements that are key to its functionality and evolution. These are thrusters, combustion chambers, propellant tanks, nozzles, and ignition systems. All of these have different but critical functions to ensure the general operation of the system in effective means and for its set purposes.

Thrusters are responsible for producing the thrust needed to push systems forward. They give the push needed to overcome resistance and provide motion. Thrusters' design and efficiency greatly affect performance; for this reason, they remain one of the key areas to innovate and seek improvement in. In contrast, combustion chambers are the heart where the fuel and oxidizer mixture takes place to create controlled explosions that generate the power to power the system. Combustion chambers are another critical aspect, as they have to tolerate high temperatures and pressures during combustion.

The propellant tanks are just as crucial because they carry and distribute the fuel necessary for operation. The material and construction of these tanks must be able to withstand the stresses of storage while minimizing weight to optimize performance. Nozzles, another vital component, play a role in directing the exhaust gases generated in the combustion chamber. Their shape and structure are carefully engineered to maximize the efficiency of the propulsion system by directing the gases in a controlled manner.

Ignition systems complete the series and start combustion. Therefore, if these are faulty, the entire system goes down. Such systems, therefore, need to have precision and reliability for optimal operation. These ignite the fuel just in time for peak performance.

Breaking down the market into all these segments can easily reveal points where improvement is possible and specific areas where correction may be needed. Each component has specific needs that require particular materials, technologies, and expertise to satisfy these needs. Together, they form a coherent system powering advancements and supporting the market's general objectives. Such segmentation not only emphasizes the value of each part but also provides a clear framework for research, development, and investment. It is through understanding and optimizing these components that the market continues to evolve and adapt to the demands of modern technology and applications.

By End-User

The rocket propulsion global market is influenced by various end-users who are creating a highly dynamic world on the theme of sending civilians into space, developing it for national defense, and fostering commercial ventures. Classified by end-user, the market comprises government space agencies, commercial space companies, and defense organizations.

The rocket propulsion market is primarily dominated by government space agencies, such as NASA, ESA, and ISRO. These agencies are concerned with research, development, and carrying out large-scale mission projects in pursuit of the boundaries of human knowledge. Such projects may involve very complex technologies, which require considerable investment and international cooperation. Government agencies also lead initiatives aimed at examining distant planets, understanding space phenomena, and launching satellites that help in communication, navigation, and scientific purposes. Such agencies also drive technological improvements that benefit other industries such as telecommunications and weather forecasting.

Commercial space companies have risen to become the most important contributors to the rocket propulsion market. Such firms include SpaceX, Blue Origin, and Rocket Lab, which have transformed the industry by posing an affordable solution and innovative technology. Such commercial players have opened up access to service in space because of their goals, including reusable rockets, private satellite launches, and space tourism. Their efforts have reduced the cost of launching payloads into orbit besides encouraging other industries to venture into space opportunities. Commercial companies' participation has introduced competition, fostering a more dynamic market which benefits from faster development cycles and creative solutions.

Defense organizations constitute another vital sector of the rocket propulsion market. Military agencies worldwide have significant investments in rocket technology for the improvement of national security. This encompasses missile, launch vehicle, and other aerospace systems designed for strategic defense and surveillance. The developments in propulsion systems allow defense organizations to achieve higher levels of accuracy, speed, and range, which are very important for modern warfare. Many innovations in rocket propulsion that begin in military research eventually find use in civilian projects, creating a crossover of technology.

Together, these end-users help shape the diversified growth of the rocket propulsion market. Together with innovation, collaboration, and competition, they mold its future. Their roles ensure this market remains an important constituent in technological development and economic progress, shaping the progress of a large number of industries and applications.

|

Report Coverage

|

Details

|

|

Forecast Period

|

2024-2031

|

|

Market Size in 2024

|

$7,083.8 million

|

|

Market Size by 2031

|

$10,769.3 Million

|

|

Growth Rate from 2024 to 2031

|

9.1%

|

|

Base Year

|

2022

|

|

Regions Covered

|

North America, Europe, Asia-Pacific Green, South America, Middle East & Africa

|

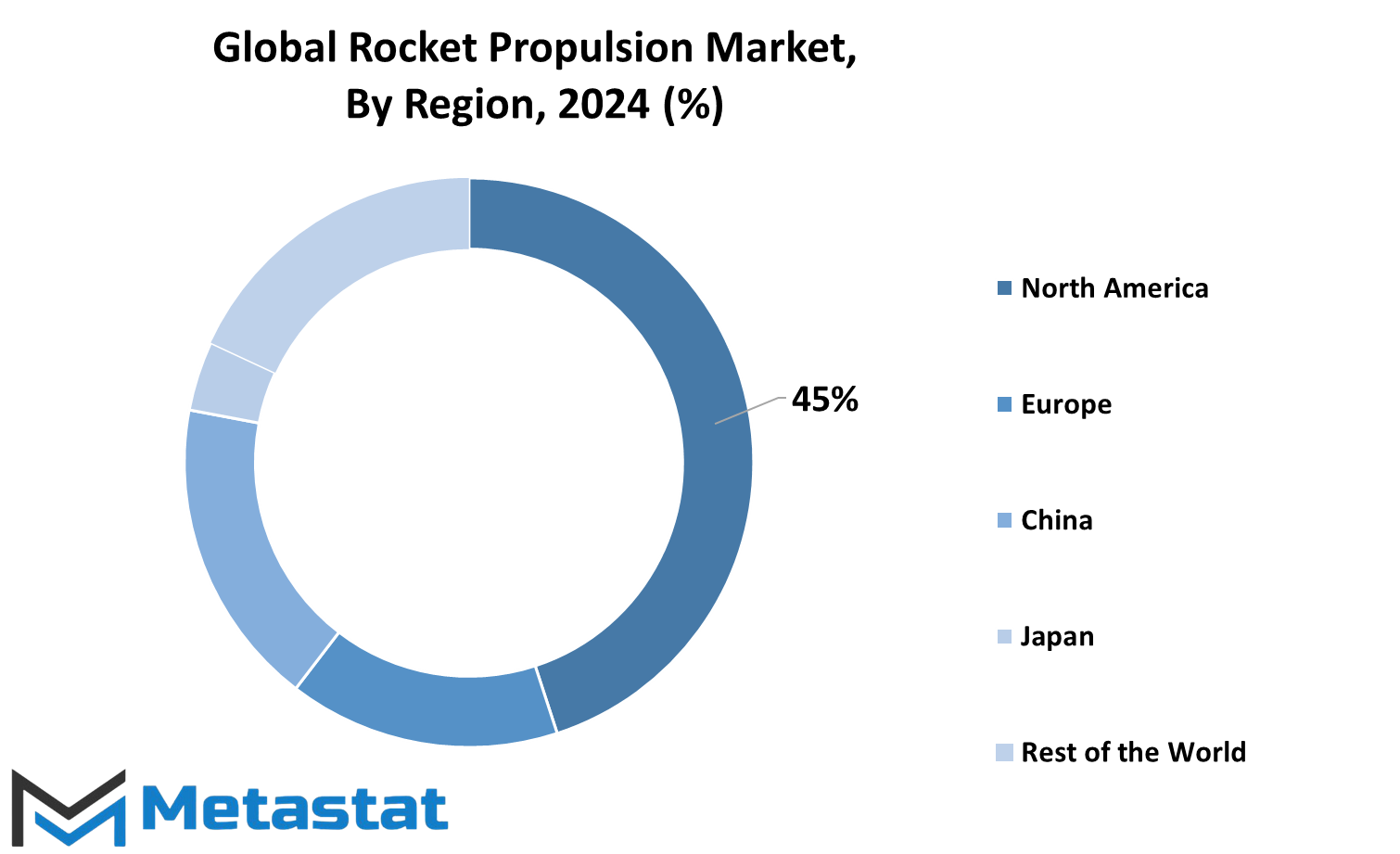

REGIONAL SEGEMENTATION

Global rocket propulsion market analysis is based on the geographical divisions, where some major differences in the market size and growth rates across various regions are seen. North America held a leading position in 2018, with a market size of 1,871.9 million US dollars, and is projected to reach 3,491.1 million US dollars by 2025. This growth reflects a compound annual growth rate (CAGR) of 9.4% from 2019 to 2025. Within North America, the market is further segmented into the United States, Canada, and Mexico, with the U.S. playing a dominant role due to its advanced technological developments and increased investments in space exploration and defense projects.

The European region is the other significant player for the rocket propulsion market. Major economies in the region include countries like the United Kingdom, Germany, France, Italy, and the Rest of Europe. Countries in this region are keenly involved with the research and development associated with aerospace advancement. Agencies, including ESA, advance innovation and increase collaboration between member states for such efforts. Germany and France, for instance, continue to commit resources to researching and developing within the aerospace industry.

Asia-Pacific is among the rapidly growing markets. The Asia-Pacific market encompasses India, China, Japan, South Korea, and the Rest of Asia-Pacific. Countries like China and India are seeing excellent growth in their space programs. In Japan and South Korea, aerospace capabilities are increasing continuously. In this region, governments are constantly increasing their initiatives and private participation in space-related activities is increasing.

In South America, the rocket propulsion market encompasses Brazil, Argentina, and Rest of South America. Brazil dominates with its aerospace sector going under expansion and modernization. Efforts are undertaken for improving satellite launches and the technologies related to it and provide opportunities for growth in this region.

Middle East and Africa would be categorized into GCC Countries, Egypt, South Africa, and the Rest of Middle East and Africa. The region has been slowly developing aerospace infrastructure. Countries such as the United Arab Emirates are making significant strides in space-related exploration.

Each of these regions contributes uniquely to the rocket propulsion market, driven by factors such as technological innovation, government funding, and the growing demand for efficient propulsion systems. This global segmentation underscores the varying degrees of growth and potential within the industry.

MARKET LEADERS

The rocket propulsion industry has witnessed great strides due to the efforts of key players that are shaping its future. They are at the heart of many innovative technologies advancing space exploration and satellite deployment, defense technologies included. Amongst these, Antrix is the commercial arm of the Indian Space Research Organisation (ISRO), specialized in satellite launching and associated services. Aerojet Rocketdyne, LLC, a subsidiary of L3Harris Technologies, Inc., specializes in innovative propulsion systems for defense and space missions. Similarly, Mitsubishi Heavy Industries contributes to launch vehicle technology, emphasizing reliability and efficiency. Northrop Grumman and Boeing are leaders in the space exploration and defense field. Northrop Grumman has developed systems for interplanetary missions, and Boeing has been a key contributor in designing crewed spacecraft and heavy-lift rockets. Sierra Nevada Corporation (SNC) and Safran S.A. have also emerged as critical contributors, with SNC focused on space transportation systems and Safran producing propulsion systems for commercial and military use.

SpaceX and Blue Origin have redefined the industry through the introduction of reusable rocket technologies. SpaceX, founded by Elon Musk, is famous for making history with its first flight of the Falcon and its latest series, Starship. Blue Origin, founded by Jeff Bezos, focuses on human space travel and making space more accessible to humanity. Virgin Galactic has also made efforts in advancing commercial space tourism to make space accessible to more civilians.

Japanese companies such as IHI and JSC Kuznetsov, besides Ukrainian manufacturer Yuzhmash, are leaders in propulsion technologies, offering systems for a variety of rockets. Another more advanced type of propulsion technology is offered by the Ad Astra Rocket Company (AARC), which is working on Variable Specific Impulse Magnetoplasma Rocket (VASIMR) with long-duration travel in space in mind. Rocket Lab, one of the new entrants in the field, focused on sending small satellites to orbit by its Electron rocket.

These companies, in cooperation, are forming the future of rocket propulsion. Innovations include reusable systems and advanced propulsion technologies in order to fulfill different needs that exist within space exploration and satellite deployment. Such an effort not only extends the humanity reach into space but also promotes international collaboration and technological progress within the sector.

Rocket Propulsion Market Key Segments:

By Propulsion Type

- Chemical Propulsion

- Electric Propulsion

- Thermal Propulsion

- Advanced Propulsion

By Application

- Satellites

- Launch Vehicles

- Interplanetary Missions

- Space Exploration

- Defense and Military Applications

By Component

- Thrusters

- Combustion Chambers

- Propellant Tanks

- Nozzles

- Ignition Systems

By End-User

- Government Space Agencies

- Commercial Space Companies

- Defense Organizations

Key Global Rocket Propulsion Industry Players

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential