Global Rigid Paper Containers Market - Comprehensive Data-Driven Market Analysis & Strategic Outlook

The global rigid paper containers market has a history dating back to the early years of contemporary packaging when companies initially started looking for strong but cost-effective substitutes for wood crates and metal tins. In its birth, the idea was straightforward: build self-supporting containers made of paperboard light enough to be mailed freely. With passage of time, printing and papermaking technologies evolved with new innovations enabling firms to produce goods not only serving purposes but also being attractive in appearance, thus making brand differentiation possible in extremely packed store shelves.

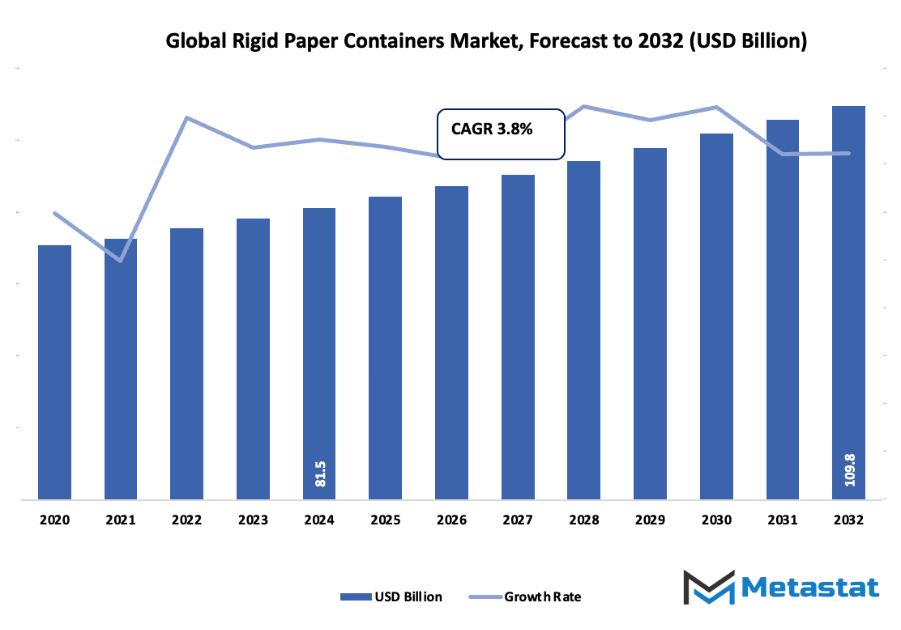

- Global rigid paper containers market of nearly USD 84.6 billion in the year 2025, expanding at a CAGR of nearly 3.8% between 2032, with the potential to reach more than USD 109.8 billion.

- Boxes command a close to 53.2% market share, fueling innovation and expanding uses through rigorous research.

- Major trends fueling growth: Rising need for sustainable and environmentally friendly packaging solutions, Expansion in e-commerce and home delivery services

- Opportunities include: Packaging design and material innovations for improved functionality and aesthetics

- Major insight: The market is projected to increase exponentially in value over the next decade, underlining dramatic growth opportunities.

Growing demand for packaged food, drinks, and domestic products compelled manufacturers to try out designs that would safeguard products from moisture and spoilage and lower costs. Paper packaging picked up speed as it could be readily expanded to fit various groups of products and tailored with intricate graphics. This trend was also backed by increasing knowledge of the environmental impact of plastics, providing paper packaging a competitive edge based on perception and function. Government evolution later provided another justification for this industry to be critical. Governments started promoting sustainable products, and compliance requirements provided further momentum to those packaging companies that had already been long-term producers of paper-based packaging. This provided the competitive context upon which firms began to bring in coated, laminated, and multi-layered paper boxes to give strength and cleanliness.

Today, therefore, the rigid paper packaging market globally is where design, efficiency, and sustainability converge. Consumer trend continues to affect the dynamics of this market, with consumers increasingly looking for functional, as much as value-oriented, packaging. The future promises even greater innovation, with digital printing, automation, and intelligent supply chains revolutionizing the manufacture and delivery of these containers.

From its early days to the current situation, the trajectory of this market shows how changes in consumer demand, technology, and regulation will continue to shape its growth. The rigid paper containers market globally will not stay the same; rather, it will continue to evolve as industries shift to meet new needs and opportunities.

Market Segments

The global rigid paper containers market is mainly classified based on Product Type, Board Type, End User, Distribution Channel.

By Product Type is further segmented into:

- Boxes will be well-placed in the global rigid paper containers market due to flexibility across a range of industries. Protection of goods and durability will guarantee boxes' long-term position. In the future, better design efficiency and advanced recycling technology will render boxes an even more cost-efficient and eco-friendly packaging option in the world.

- Tubes: Tubes will continue to grow steadily in the market, particularly in personal care and cosmetics. Convenience and good looks come with the compact form. Increased demand in the future will result from environmentally oriented consumers gravitating toward recyclable tube packaging. Design innovation and barrier protection will further enhance tube performance in applications.

- Trays: Trays will be an important part of the market with growing demand for ready-to-eat food and fresh fruits and vegetables. Trays provide strength and stackability and are convenient to use in food packaging. Developments in compostable coatings and lightweight material will increase tray usage in industries that are moving towards environmental stewardship.

- Cartons: Cartons will be growing in the market through extensive application in beverages and liquid food products. Cartons are appreciated for protection, portability, and branding. Through consistent emphasis on recyclability and minimizing plastic usage, cartons will become more powerful as industries shift to sustainable packaging to appeal to customers across the globe.

- Other: Other structures in the global rigid paper containers market, including bespoke packaging shapes, will experience incremental adoption. Those formats enable companies to differentiate themselves and cater to niche requirements. In the future, innovation in flexible yet strong material will expand uses for these types, providing functionality as well as design beauty.

By Board Type the market is divided into:

- Paperboard: Paperboard will maintain a strong role in the global rigid paper containers market, especially for lightweight packaging. Its smooth surface makes it suitable for branding and printing. As digital commerce expands, paperboard demand will rise further. Future improvements in strength and recyclability will help balance functionality with environmental goals worldwide.

- Corrugated Fibreboard: Corrugated fibreboard will see sustained demand in the market because of strength and protective quality. It will remain essential for shipping, storage, and heavy-duty applications. In future, innovation in biodegradable adhesives and improved durability will increase its importance, while sustainability initiatives will encourage broader adoption globally.

- Kraft Paper: Kraft paper will grow in use within the global rigid paper containers market due to its recyclable and biodegradable nature. Its natural look appeals to eco-conscious brands and consumers. Future adoption will strengthen as industries emphasize plastic-free packaging. Enhanced barrier coatings will expand kraft paper’s ability to protect a wider range of goods.

By End User the market is further divided into:

- Food and Beverage: Food and beverage will dominate demand in the global rigid paper containers market because of wide packaging needs. Freshness and safety will remain key. Growing consumer preference for sustainable packaging will drive adoption. Future demand will be supported by innovation in protective coatings and formats designed to extend shelf life of products.

- Personal Care and Cosmetics: Personal care and cosmetics will see rising adoption of packaging from the market. Tubes, cartons, and boxes will be preferred for compactness and branding. Sustainability and aesthetics will drive industry choices. In the future, recyclable and biodegradable packaging solutions will continue to attract companies seeking eco-friendly options.

- Pharmaceuticals: Pharmaceuticals will rely more on the market for secure and tamper-evident packaging. Boxes and cartons will dominate as they provide safety and compliance. With healthcare expansion worldwide, future demand will grow. Advancements in protective coatings and barrier properties will strengthen paper packaging for sensitive medical and health products.

- Household Products: Household products will strengthen the market with packaging that ensures durability and easy handling. Boxes and trays will dominate this segment. Future demand will rise as eco-friendly preferences grow. Development of packaging that is both functional and recyclable will align with the shift toward sustainable living.

- Industrial Goods: Industrial goods will continue to utilize the market because of corrugated fiberboard and kraft packaging. The durability and protective strength of these formats will be critical. In the future, industries will adopt advanced rigid packaging that balances heavy-duty use with recyclability, ensuring sustainability in large-scale applications.

- Other: Other end-user categories in the global rigid paper containers market, including specialty packaging for unique products, will see steady expansion. These formats provide customized solutions that standard packaging may not address. Future growth will be supported by innovation in design flexibility and the demand for unique packaging styles across industries.

By Distribution Channel the global rigid paper containers market is divided as:

- Retail Stores: Retail stores will continue to support demand in the global rigid paper containers market as visual appeal and shelf impact remain critical. Packaging will be designed for both attraction and functionality. In future, businesses will adopt recyclable designs that balance brand visibility with sustainability to appeal to eco-conscious shoppers directly.

- Online Sales: Online sales will drive rapid growth in the market as e-commerce expands worldwide. Packaging will need to be sturdy, lightweight, and protective for shipping. Future designs will focus on reducing waste while maintaining durability, making online retail a powerful driver of demand for rigid paper packaging solutions.

|

Forecast Period |

2025-2032 |

|

Market Size in 2025 |

$84.6 Billion |

|

Market Size by 2032 |

$109.8 Billion |

|

Growth Rate from 2025 to 2032 |

3.8% |

|

Base Year |

2024 |

|

Regions Covered |

North America, Europe, Asia-Pacific, South America, Middle East & Africa |

By Region:

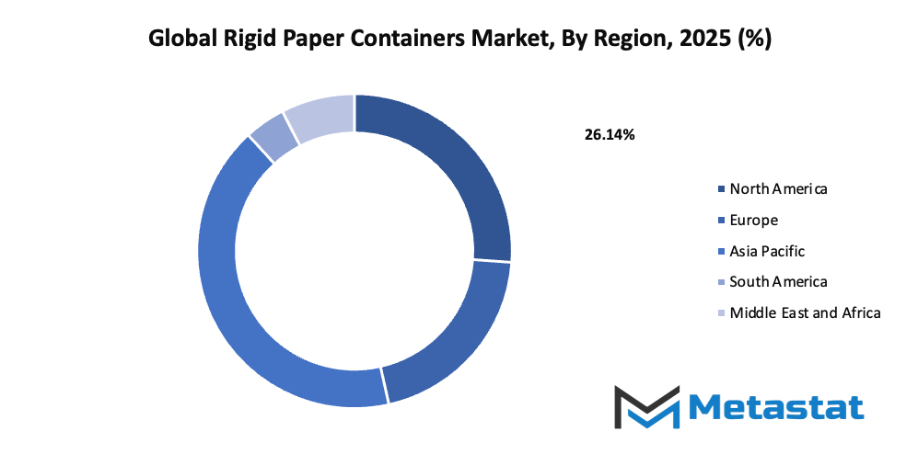

- Based on geography, the global rigid paper containers market is divided into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

- North America is further divided into the U.S., Canada, and Mexico, whereas Europe consists of the UK, Germany, France, Italy, and the Rest of Europe.

- Asia-Pacific is segmented into India, China, Japan, South Korea, and the Rest of Asia-Pacific.

- The South America region includes Brazil, Argentina, and the Rest of South America, while the Middle East & Africa is categorized into GCC Countries, Egypt, South Africa, and the Rest of the Middle East & Africa.

Growth Drivers

- Increasing demand for sustainable and eco-friendly packaging solutions: The global rigid paper containers market will benefit greatly from the rising demand for sustainable and eco-friendly packaging solutions. As consumers prefer packaging that reduces waste and protects the environment, industries will adopt these containers on a larger scale. This shift will secure growth and improve brand value for many companies.

- Growth in e-commerce and home delivery services: The market will gain momentum with the expansion of e-commerce and home delivery services. The need for durable, lightweight, and recyclable packaging is higher than ever. This packaging solution ensures safe delivery while addressing environmental concerns, making it a preferred option for online retailers and delivery businesses.

Challenges and Opportunities

- Competition from alternative packaging materials such as plastics and metals: The global rigid paper containers market will experience competition from plastics and metals, which remain widely used due to durability and cost advantages. Overcoming this challenge will require focusing on promoting environmental benefits and expanding awareness. Increased regulation against non-recyclable packaging will gradually favour rigid paper containers over alternatives.

- Fluctuations in raw material prices: The global rigid paper containers market will be impacted by fluctuations in raw material prices. Changes in pulp and paper costs affect overall production expenses, which can influence profit margins. Companies that develop efficient sourcing and recycling strategies will be better equipped to handle such shifts and maintain steady growth.

Opportunities

Innovations in packaging design and materials for enhanced functionality and aesthetics: The market will have opportunities through continuous innovation. Advancements in packaging design and material strength will enhance performance while offering aesthetic appeal. These improvements will support branding efforts, customer satisfaction, and wider adoption. Emphasis on innovation will ensure competitiveness and growth for the global rigid paper containers market.

Competitive Landscape & Strategic Insights

The global rigid paper containers market is developing into an industry that continues to attract attention from both established corporations and new regional participants. Growth in this sector is supported by changing consumer expectations, an increasing demand for sustainable packaging, and the global shift toward environmentally responsible solutions. Rigid paper containers have gained recognition because they are durable, versatile, and recyclable, making them a preferred choice across food, beverage, personal care, and household product packaging. As brands across the world prioritize eco-friendly practices, the use of paper-based containers will expand even further, reshaping packaging standards in many industries.

The market brings together large-scale corporations with decades of experience alongside smaller regional companies that are steadily building influence. The presence of well-known names such as Sonoco Products Company, Amcor plc, Smurfit Kappa, WestRock Company, International Paper Company, Mondi Group, Packaging Corporation of America, Stora Enso Oyj, Georgia-Pacific LLC, Greif, Metsa Board Corporation, Oji Holdings Corporation, Nippon Paper Industries Co., Ltd., Huhtamäki Oyj, and DS Smith plc demonstrates how the sector is shaped by both international leaders and strong competitors from local markets. These companies continue to strengthen their position by investing in technology, innovation, and supply chain efficiency, while emerging players focus on adaptability and regional advantages to secure their share of the market.

The market is moving toward an era defined by technological progress and environmentally driven production methods. Advancements in lightweight material design, printing techniques, and barrier coatings will play a major role in improving product durability while maintaining recyclability. Companies are also expected to adopt smart packaging technologies that support better tracking and improved product safety. These developments will not only benefit manufacturers but also enhance consumer trust and brand value. In the future, the integration of digital tools in packaging production will become more common, opening opportunities for customization, reduced waste, and faster turnaround times.

The market will also be influenced by policy changes and stricter environmental regulations. Governments and international organizations are pushing for reduced use of plastic and non-recyclable packaging, which is creating both challenges and opportunities for industry players. Companies that adapt quickly to these requirements by designing containers that balance strength with recyclability will maintain a competitive edge. Furthermore, the rise of e-commerce is driving increased demand for secure and sustainable packaging solutions, reinforcing the role of rigid paper containers as a reliable choice for shipping and delivery.

Market size is forecast to rise from USD 84.6 billion in 2025 to over USD 109.8 billion by 2032. Rigid Paper Containers will maintain dominance but face growing competition from emerging formats.

In the years ahead, the global rigid paper containers market will likely expand its influence across new sectors. Growing awareness among consumers about the environmental impact of packaging will fuel innovation, while technological improvements will strengthen performance and efficiency. This blend of global leadership, regional innovation, and sustainability-focused growth ensures that the industry will remain a central part of packaging solutions worldwide.

Report Coverage

This research report categorizes the market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the global rigid paper containers market.

By Product Type is further segmented into:

- Boxes

- Tubes

- Trays

- Cartons

- Other

By Board Type the market is divided into:

- Paperboard

- Corrugated Fiberboard

- Kraft Paper

By End User the market is further divided into:

- Food and Beverage

- Personal Care and Cosmetics

- Pharmaceuticals

- Household Products

- Industrial Goods

- Other

By Distribution Channel the market is divided as:

- Retail Stores

- Online Sales

Key Global Rigid Paper Containers Industry Players

- Sonoco Products Company

- Amcor plc

- Smurfit Kappa

- WestRock Company

- International Paper Company

- Mondi Group

- Packaging Corporation of America

- Stora Enso Oyj

- Georgia-Pacific LLC

- Greif

- Metsa Board Corporation

- Oji Holdings Corporation

- Nippon Paper Industries Co. Ltd.

- Huhtamäki Oyj

- DS Smith plc

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential

US: +1 3023308252

US: +1 3023308252