MARKET OVERVIEW

The Global Radiology As A Service market and industry will transform the way healthcare providers deliver diagnostic imaging services in the near future. As healthcare systems around the world are increasingly being squeezed to make healthcare more efficient, cost-effective, and outcomes-focused, radiology as a service is emerging as an important strategic response. Such a model shall allow health systems to outsource radiologic services through external online radiology service delivery platforms to obtain access to cutting-edge technology, higher quality talent, and scalable solutions.

The market for radiology-as-a-service will shift all of its demands drastically, and it will be an inevitable component of the healthcare sector. Hospitals and clinics will not have to maintain costly equipment, such as imaging tools, and specialized staff in-house anymore. Instead, they will opt for service providers that offer on-demand access to advanced diagnostic tools and highly skilled radiologists. This transformation will not only reduce the operational costs but also make the diagnostic services accessible to underrepresented regions and small healthcare facilities.

The Global Radiology As A Service market shall bring about a new era of innovativeness for imaging in medicine. Effective standard imaging practices shall yield to newer, advanced AI -powered technologies. The integration of artificial intelligence into radiology workflows will automate routine tasks, thereby increasing the accuracy and speed of diagnoses. Radiologists will be able to focus more on complex cases and patient interaction. AI-powered tools will improve the efficiency of early detection of diseases such as cancer, heart conditions, and neurological disorders, thereby saving lives through quicker interventions.

Telemedicine services will also be integrated with the radiology services in this model. Health care providers can, therefore, perform remote consultations to patients in good time, especially in remote or rural areas. Radiology services are hence made available online and on demand through secure sites, empowering the patient to have access to any care they might need without the need to travel long distances. This will be highly beneficial in those countries where healthcare infrastructure is not easily accessible and helps fill the gap in healthcare delivery.

Regulatory frameworks will evolve as the Global Radiology As A Service market evolves, focusing on protection of patient data and proper accreditation of service providers. Stricter standards on privacy will be set up in order to avoid data breaches and ensure that health records are kept safely on the digital platforms. Compliance with the regulations of local and international communities will be important for companies that will venture into this area, to make sure that they meet medical as well as technological standards.

Collaboration will continue to rise in the Global Radiology As A Service market, including among health service providers, tech companies, and governmental bodies. Their cooperation will increase the pace and efficiency with which new imaging technology is designed and delivered and enhance affordability and access. Through all this, quality of diagnosis for the patient improves while being executed on the fastest time frames possible for treatment and healing.

The Global Radiology As A Service market is going to transform the future of healthcare delivery by healthcare organizations in the years to come. Its potential to reduce costs, improve access to services, and facilitate the integration of AI and telemedicine will make it a key element in the future of healthcare delivery and allow patients to receive better care in a more efficient manner.

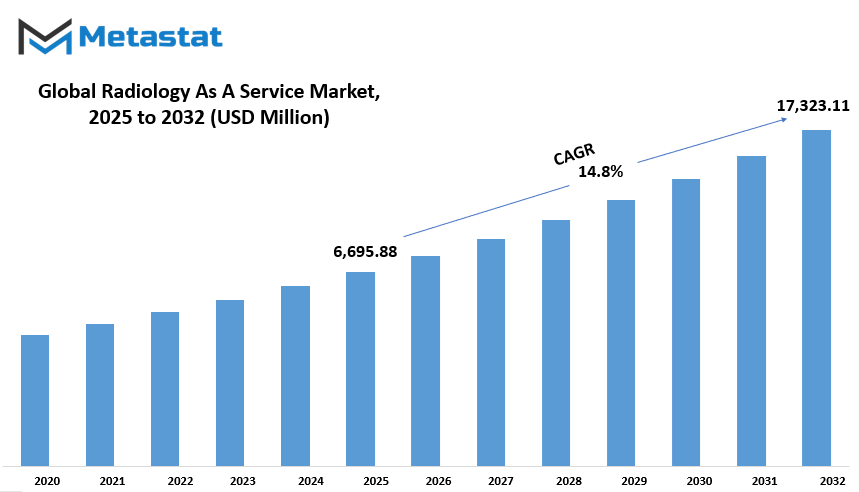

Global Radiology As A Service market is estimated to reach $17,323.11 Million by 2032; growing at a CAGR of 14.8% from 2025 to 2032.

GROWTH FACTORS

This has been growing in the Global Radiology As A Service Market over the years and is driven by several factors, which influence the development of the market and will shape its future. The high demand for remote diagnostics and teleradiology is one such factor. Due to the pursuit of more accessible and convenient ways of medical care by healthcare providers and patients, teleradiology offers the solution of remotely interpreting images. This enables radiologists to offer services from any location, thus enhancing the delivery of healthcare, especially in rural or underserved areas. As a result, the increasing dependence on remote diagnostics is forcing healthcare providers to begin using advanced radiology solutions, thereby creating an expansion avenue for the market.

The adoption of AI-based and cloud-based imaging solutions is another important growth driver for the market. Artificial intelligence is a revolution in radiology, enhancing analysis of images, reducing workload in radiologists, and making quicker and more precise diagnoses. AI-based systems allow for the analysis of thousands of medical images, and abnormalities might be detected that the human eye cannot see. So, AI becomes an essential tool in modern radiology. Cloud-based imaging solutions are also becoming popular, as they offer safe storage, easy access, and sharing of medical images. These technologies together improve the efficiency of radiology services and drive market growth.

However, despite the numerous opportunities, the market is constrained by a few limitations. High initial investment and infrastructure costs continue to be major barriers for healthcare providers, particularly in developing countries or smaller healthcare facilities. Advanced imaging technologies often require large sums of money for infrastructure support, which can act as a deterring factor in adopting the service. Another area that the industry is still to overcome is related to data security and regulatory compliance issues. As much sensitive patient information is involved in this, ensuring protection of this information and strictly adhering to HIPAA and GDPR is complicated and costly.

The market also provides several growth opportunities. One of the most promising is the expansion of healthcare services in emerging markets. As healthcare systems in these regions improve and healthcare access increases, the demand for radiology services will grow, creating a significant opportunity for radiology as a service. In addition, the integration of AI for enhanced image analysis and workflow automation presents another opportunity. The potential for streamlining radiology workflows, reducing errors, and enhancing image interpretation with AI will make this segment a key differentiator in the industry, allowing businesses that invest in these technologies to lead the pack in a competitive market. These opportunities will shape the future of the Global Radiology As A Service Market and contribute to its continued growth.

MARKET SEGMENTATION

By Service

The Global Radiology As A Service market is fast-growing, given the increasing healthcare service demand and the advancement in medical imaging technologies. Radiology, being an essential part of healthcare, has been keeping pace with growing needs of hospitals, clinics, and patients around the world. This market is divided into several key service categories, catering to specific requirements within the healthcare system.

One of the major segments of the Radiology As A Service market is Tele-radiology Reading Platform Services, which is estimated at $2,306.55 million. This service enables radiologists to send images of radiological studies to remote specialists for interpretation. Tele-radiology has become an essential component of healthcare because it offers a cost-effective means of overcoming the shortage of radiologists in many areas, especially in remote or underserved regions. It allows for access to specialized opinions instantly, without the need to wait on an in-person visit of a specialist.

Remote Scanning Services is another integral service in this market. Advanced imaging technology helps healthcare providers to deliver diagnostic imaging services to patients from their locations without physically visiting healthcare facilities. It adds to the convenience and reduces the load on patients, especially in areas that are rurally located or remote. It also ensures that the radiologists and medical staff are able to view images without being in the same physical location as the patient, thereby making the process faster and more efficient.

Consulting services help healthcare organizations find the right way to use and optimize radiology services. Consulting services improve the general workflow, the quality of images, and compliance with medical regulations. Consulting services assist healthcare providers in achieving maximum effectiveness of their radiology systems, ensuring high-quality diagnostic imaging for patients.

Staffing Services is another significant segment in the Global Radiology As A Service market. Staffing services help healthcare organizations source the right professionals, such as radiologists, technicians, and support staff. With an increase in demand for radiology services, staffing services are essential to enable healthcare providers to have skilled personnel in all departments of radiology.

Last, the category of "Other" consists of various services involved in the execution of radiology services, ranging from equipment servicing, software application solutions, to training. These service support the functions and quality operations of radiology within healthcare delivery systems.

In conclusion, the Global Radiology As A Service market is growing steadily with the diverse services that address the challenges faced by healthcare providers. With innovations in tele-radiology, remote scanning, consulting, staffing, and other services, the sector is well-positioned to meet the evolving needs of modern healthcare.

By Location

The Global Radiology As A Service market is getting progressively segmented along geographical locations, that are of significant help in formulating the growth aspects of the industry. Divided into three broad categories, this market can be primarily classified into inshore, offshore, and in-house. The categories signify the locations at which radiology services are offered, and each category has its own strengths and weaknesses that govern expansion.

Inshore radiology services refer to the provision of radiology services within a country or region. The service model, therefore, based on location is useful since it ensures better control over the quality and accessibility of the services. Healthcare providers can, with inshore radiology, ensure that the services provided comply with the requirements of the local regulation and meet the specific needs of the population. This would also mean better integration with local healthcare systems, thus making it easier for the patients to access and use the offered services. However, there may be some instances wherein such a model has limitations, usually in terms of the cost and availability of resource capabilities.

The 'offshore' radiology services would provide services from another country or region where labor costs are typically much lower. Offshore services enable healthcare providers to reduce costs while still offering high-quality radiology support. This model has gained popularity due to the global reach of healthcare providers and the advancements in telemedicine and communication technologies. Offshore radiology can offer the opportunity to get access to the expertise of experts in areas where such services are not readily available locally. Even though offshore radiology has several advantages, there are some drawbacks, including differences in time zones, communication, and data security and confidentiality issues.

Those services which are given in-house, meaning within healthcare facilities, such as hospitals and clinics, are considered in-house. It integrates directly into the healthcare setting, providing instant access to radiology support. The in-house model allows for high control over the service quality because the radiology professionals work with the same team of physicians in treating these patients, which often leads to faster decision-making and hence better patient outcomes. One main drawback of in-house services is that it costs more to operate because healthcare facilities need to maintain their radiology departments and personnel.

Each location-based model has different advantages and disadvantages in the Global Radiology As A Service market, and healthcare providers should examine these factors before determining the best service model for their needs. Because of this, the market will continue to evolve with regards to changing technologies, cost pressures, and patient demands of service models in the future.

By Modality

The Global Radiology as a Service RaaS market growth has been tremendous. Enhanced healthcare technology and growing demand for diagnostic imaging services are a few reasons for this growth. The increasing requirement for accessible yet affordable radiology services across the world is perhaps the primary reason for this growth. RaaS also provides the advantages of offering demand-based imaging service access to medical providers without burdening them by heavy investments on equipment and infrastructures. Smaller clinics, hospitals, especially within regions where only limited advanced access to medical technologies is possible will find it appropriate.

The market is also categorized based on modality. There are various categories of diagnostic imaging techniques. This includes X-ray, CT, MRI, Ultrasound, Mammography, and PET-CT. Each one has an important role in the diagnostic process and offers specific advantages depending on the condition being diagnosed.

X-ray still holds the largest application of the imaging techniques available. It has extensive use for bone fractures, infection diagnosis, and many cancers. Relatively inexpensive than the other imaging apparatuses, an X-ray machine remains a part of the various setups in healthcare facilities. Advancements in digital X-rays improved the quality of the images considerably.

CT scans are able to produce clearer images of the body compared to X-rays, especially concerning soft tissue and organs. This is especially useful for conditions such as tumors, internal injuries, and neurological disorders. More precise planning for surgery and treatments is possible by allowing 3D images to be obtained. It will produce images in the body and organs through a combination of radio waves and magnetic fields. Diagnosis is mostly common to conditions involving the brain, the spinal cord, muscles, and joints.

Ultrasound imaging makes images through high-intensity sound waves, though the common utilization is producing images for pregnancy and monitoring or diagnosing diseases like heart, liver, and kidney. This form of imaging technique is non-invasive, relatively safe, and not too costly. Mammography still has the utmost relevance to screening a breast for cancers. Last but not least, PET-CT merges functional imaging provided by PET with the anatomical images provided by CT, such that cancer, cardiovascular diseases, and neurological disorders will be more sensitive to detect.

As demand in radiology is increasing, all these imaging modalities will contribute to an expansive role of RaaS, hence providing health-care providers flexible as well as effective solutions to the diagnosis and treatments of numerous health conditions.

By End-use

The RaaS global market is highly developing and revolutionizing the ways through which healthcare service providers are delivering radiology services. It is an outsourced service, where specialized service providers carry out radiology work, hence giving it a more flexible and efficient approach. It is categorized on different end-use sectors, where every sector has different needs of radiology services. These include hospitals, diagnostic imaging centers, radiology clinics, physician offices, and nursing homes.

Hospitals are among the primary end-users of radiology services. Given their size and range of services, hospitals need consistent, high-quality radiology solutions to take care of patients. The institutions use radiology services to diagnose a wide range of conditions, from fractures to more complex diseases. The demand for accurate imaging results and quick turnaround times is critical in providing timely treatment.

Diagnostic imaging centers is the second largest segment in the Radiology As A Service market. They emphasize the technologies they use to image, including X-rays, CT scans, MRI scans, and ultrasounds. These diagnostic centers are of utmost importance to both primary care providers and specialists as they offer referred patients the services that diagnose them. As the requirement for advanced diagnostic tools is on the rise, RaaS is being applied by diagnostic imaging centers to modernize technological structure and face increasing demand from patients.

Radiology clinics are similar in concept to a diagnostic imaging center, but they focus on providing imaging services and are normally smaller operations. Many clinics cater specifically to certain types of patients who require specific imaging studies. Clinics benefit from models of Radiology As A Service by being able to have access to the latest generation of imaging technologies without the massive capital expenditures in purchasing and maintaining expensive equipment.

Physician offices are another area where Radiology As A Service is gaining prominence. Small healthcare practices, especially in rural or underserved areas, cannot afford to invest in their own radiology equipment. RaaS allows these offices to provide radiology services to their patients by outsourcing the tasks to third-party providers, thereby improving patient care without the cost of equipment.

Finally, nursing homes are embracing Radiology As A Service to provide better care to elderly residents. Most nursing homes lack the resources for on-site radiology. Outsourcing of these services would ensure that patients have access to essential diagnostic tools. This is important, especially in identifying health issues that might not be very apparent, such as bone fractures or respiratory conditions.

In a nutshell, the global Radiology As A Service market caters to a myriad number of sectors, each with benefits consisting of flexibility, cost efficiency, and advanced technology offered by the service model. These sectors include the hospital, offices for physicians, and nursing homes, which now rely on RaaS for optimum patient care at reduced costs.

|

Forecast Period

|

2025-2032

|

|

Market Size in 2025

|

$6,695.88 million

|

|

Market Size by 2032

|

$17,323.11 Million

|

|

Growth Rate from 2024 to 2031

|

14.8%

|

|

Base Year

|

2024

|

|

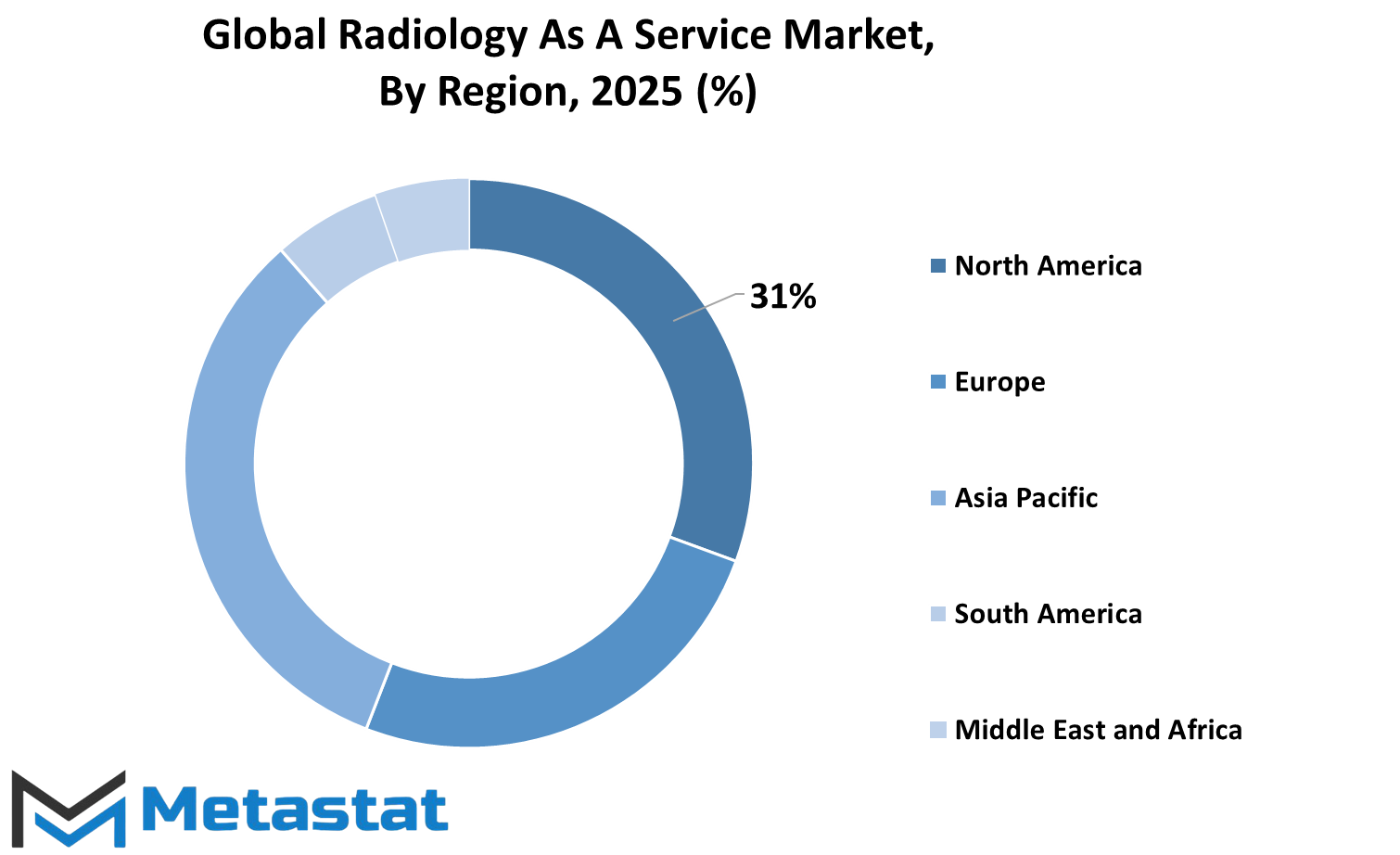

Regions Covered

|

North America, Europe, Asia-Pacific, South America, Middle East & Africa

|

REGIONAL ANALYSIS

The global Radiology As A Service (RaaS) market is further segmented based on geography, wherein the various regions are contributing heavily to its growth. These include North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. North America further comprises the U.S., Canada, and Mexico, with all of them having different market dynamics. Europe consists of such major countries as the UK, Germany, France, and Italy, with other regions within the continent that are less prominent but contribute toward the market landscape of this continent. Asia-Pacific is such a major player in this market, as this continent is comprised of countries like India and China, Japan, and South Korea, forming key areas of concentration.

Each of these countries represents a different set of challenges and opportunities for the radiology services sector. In addition to the above major countries, the region consists of other areas which are classified together under the title "Rest of Asia-Pacific" regions such as those countries which have demand for the services of radiology but are not currently market leaders but more promising for future growth. Another region of interest is the South American market.

The region is largely dominated by Brazil and Argentina, countries that have seen advancements in healthcare technology, including radiology services. Other nations in the continent are included in the "Rest of South America" category and contribute to the overall regional market but at a smaller scale compared to the leading countries. The last is the Middle East & Africa region, which again is broken down into subcategories-including GCC countries, Egypt, South Africa, and the rest of the Middle East & Africa.

Of these, the GCC countries lead with their growing health infrastructure. Meanwhile, nations like Egypt and South Africa also contribute to the expansion of radiology services within the region, while other countries in the Middle East & Africa show promise for future growth as healthcare needs continue to rise. In sum, the global Radiology As A Service market is spread and diversified.

All the regions, in fact, offer their unique challenges and opportunities, from the North American to the European, Asia-Pacific, South American, and Middle East & African ones. The future of radiology services will be shaped by all these regions, and the market will keep growing along with the rising demand for health care and technological development in radiology.

COMPETITIVE PLAYERS

Global Radiology As A Service (RaaS) market is expanding fast due to the rising need for operational efficiency and patient care from healthcare providers.This service enables cloud-based medical imaging, thus negating the need for in-house radiologists and complex infrastructure like that found in traditional imaging centers. By outsourcing their radiology services, healthcare providers can cut down on costs while increasing efficiency and the quality of care given to patients.

Key players in the Radiology As A Service industry are firms such as Siemens Healthineers, TRG-The Radiology Group, and Philips Healthcare, which have been in operation for years. These firms drive innovation and expand radiology services around the world. For example, Siemens Healthineers offers an extended range of imaging solutions, which healthcare facilities can access around the world. TRG - The Radiology Group, on the other hand, offers specialist services catering to multiple medical practices within both accessible and isolated regions. The firm of Philips Healthcare offers comprehensive, advanced, and superior quality imaging and diagnostics to clinics and hospitals all around the world due to its sound infrastructure.

In addition to these big companies, there are several innovative companies like DeepHealth, DeepTek Inc, and Cloudex Radiology Solutions, which are working to make access to radiology services much easier and efficient. All of these companies are using artificial intelligence and machine learning to enhance the accuracy of diagnoses, automate workflow processes, and ensure faster return of results to clinicians.

ONRAD, Inc., Teleradiology Solutions, Everlight Radiology, RadNet, Inc., and Virtual Radiologic (vRad) are some other major players in the market. They are offering teleradiology services so that radiology images with reports can be access with distant healthcare providers. It is particularly useful in short supply of local radiologists or when immediate consultations outside working hours are required. Medica Group PLC is another company offering comprehensive radiology services through advanced technology, further advancing the reach and scope of the industry.

Overall, the Global Radiology As A Service market is characterized by the presence of leading companies with high-quality services that are primarily aimed at improving the outcomes of the patients while making health care more accessible and cost-effective. The market is expected to continue growing as the healthcare providers understand the benefits associated with the use of radiology services.

Radiology As A Service Market Key Segments:

By Service

- Tele-radiology Reading Platform Services

- Remote Scanning Services

- Consulting Services

- Staffing Services

- Other

By Location

- Inshore

- Offshore

- In-house

By Modality

- X-ray

- CT

- MRI

- Ultrasound

- Mammography

- PET-CT

By End-use

- Hospitals

- Diagnostic Imaging Centers

- Radiology Clinics

- Physician Offices

- Nursing Homes

Key Global Radiology As A Service Industry Players

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential