Global Patient Data Hub Solutions Market - Comprehensive Data-Driven Market Analysis & Strategic Outlook

The global patient data hub solutions market in the healthcare tech sector will keep reshaping the way patient data is gathered, stored, and interpreted in the years ahead. This market will go beyond mere data storage solutions, becoming more integrated digital systems that bind hospitals, research institutions, and diagnostic centers across the globe. Since healthcare professionals will depend more on real-time insights from data, the global patient data hub solutions market will revolutionize patient care from reactive cure to preventive care, giving medical practitioners the complete picture of a patient's life.

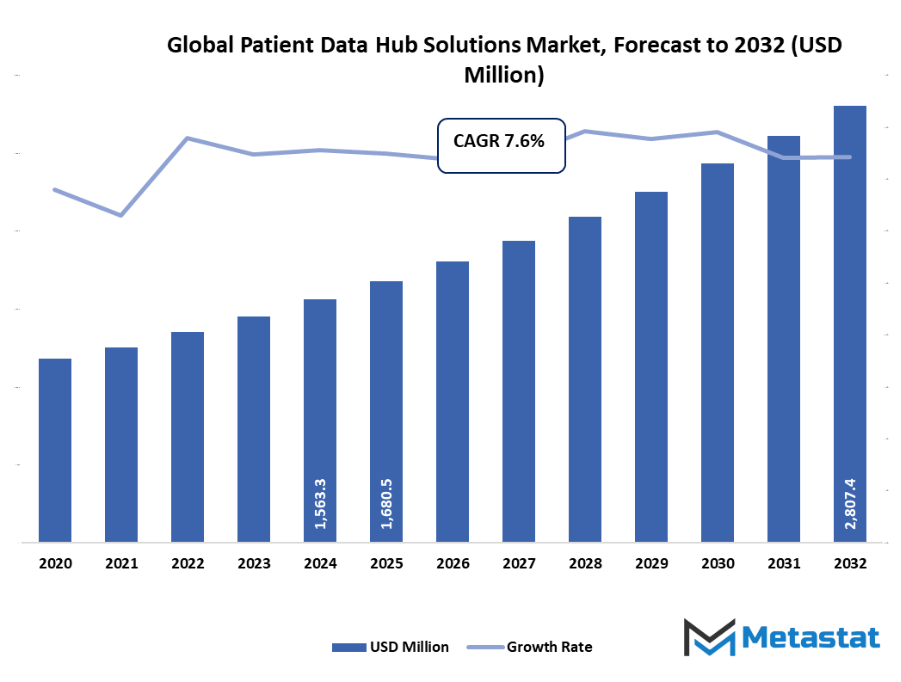

- Global patient data hub solutions market valued at approximately USD 1680.5 million in 2025, growing at a CAGR of around 7.6% through 2032, with potential to exceed USD 2807.4 million.

- Health Data Apps & AI Solutions account for nearly 29.8% market revenues, driving innovation and expanding applications through intense research.

- Key trends driving growth: Growing adoption of electronic health records (EHRs) and healthcare data interoperability standards., Rising demand for data-driven healthcare insights and personalized medicine.

- Opportunities include Expansion of AI and cloud-based analytics to enhance predictive healthcare and population health management.

- Key insight: The market is set to grow exponentially in value over the next decade, highlighting significant growth opportunities.

What impact will the growing demand for real-time patient information have on the evolution of healthcare data management? Will the combining of AI with interoperability standards shake up the conventional patient data systems and offer fresh competitive advantages? Moreover, if data privacy concerns keep getting stronger, will changes in regulations speed up or slow down the worldwide use of patient data hubs?

Outside its customary domain, the market will open up into such domains as predictive medicine and personalized medicine. Data centers will not only track patient data but also allow for healthcare systems to foresee future medical requirements, predict disease trends, and detect early warning signs of risk. This proactive strategy will facilitate closing the extended communication divides among medical departments, with an ease of exchanging vital data, leading to improved diagnostic output and treatment planning.

Market Segmentation Analysis

The global patient data hub solutions market is mainly classified based on Solution Type, Deployment Mode, End-use.

By Solution Type is further segmented into:

- Health Data Apps & AI Solutions:

The global patient data hub solutions market will be characterized by the rapid spread of the use of health data apps, AI-powered solutions that facilitate patient data management. By deploying such devices, the organizations will be able to analyze effectively, improve care decisions, and provide extended patient monitoring due to automation, predictive modeling, and real-time insights that involved healthcare systems seamlessly.

- Data Integration Solutions:

The coming time of the market is going to rely heavily on efficient data integration platforms that gather info from diverse medical sources. Such systems will bring about better data consistency, lessening data duplication and promotion of smooth interaction among digital health networks, thus creating the possibility of excellent clinical and operational outcomes.

- Patient 360 View Platforms:

The demand for the complete 360-degree patient view platform in the market will increase further. These platforms will provide healthcare establishments with the ability to access extensive and updated patient records instantly for tailoring treatments, risk identification at an early stage, and improving the communication of healthcare departments.

The other solution types in the global patient data hub solutions market will be those specialized in advanced analytics, the management of interoperability, and secure exchange of patient data. By debarring these new solutions, healthcare will become versatile and the use of data will be more adaptable across various digital ecosystems, thus driving innovations in healthcare.

By Deployment Mode the market is divided into:

- Cloud-based: The global patient data hub solutions market will experience growing adoption of cloud-based deployment models because they are cost-effective and scalable. These platforms will render patient data more accessible and facilitate secure collaboration among stakeholders as well as continuous system updates without requiring massive infrastructure investments.

- On-premises: In the global patient data hub solutions market, on-premises deployment will remain the option of choice for institutions that value having complete control and greater security of patient data stored within. The arrangement will be the best fit for organizations dealing with sensitive information, providing customizable platforms attuned to strict compliance and privacy guidelines.

By End-use the market is further divided into:

- Healthcare Companies:

A global patient data hub solutions market will represent an opportunity of great value for companies in the healthcare sector who seek to improve product development, enhance research quality, and cut down on data management expenses. To top that, pharma and biotech industries leveraging such solutions will experience less demanding regulatory compliance as well as increased data-driven innovation.

The implementation of patient hub systems in the global patient data hub solutions market will be a great avenue through which healthcare providers can not only drive clinical efficiency and care coordination but also facilitate them. Centrally available patient data will assist in diagnostics, hence there will be fewer medical errors and data-driven decision-making will be enabled leading to enhanced patient experiences and health outcomes.

Healthcare payers in the market are anticipated to adopt the utilization of advanced data hub systems in order to streamline claims administration, detect cases of fraud, and increase the accuracy of risk assessment. These platforms will verify the completeness of patient records which in turn will facilitate policy management to be more precise and create the conditions for the availability of effective healthcare financing.

- Others (Include CRO, CDMO, etc.):

Other end-users such as Contract Research Organizations (CROs) and the Contract Development and Manufacturing Organizations (CDMOs) are poised to gain tremendously from the global patient data hub solutions market. These entities will utilize data hub systems for better research collaboration, faster regulatory submissions, and improved clinical data accuracy- all leading to the next medical advancements.

|

Forecast Period

|

2025-2032

|

|

Market Size in 2025

|

$1680.5 Million

|

|

Market Size by 2032

|

$2807.4 Million

|

|

Growth Rate from 2025 to 2032

|

7.6%

|

|

Base Year

|

2024

|

|

Regions Covered

|

North America, Europe, Asia-Pacific, South America, Middle East & Africa

|

Geographic Dynamics

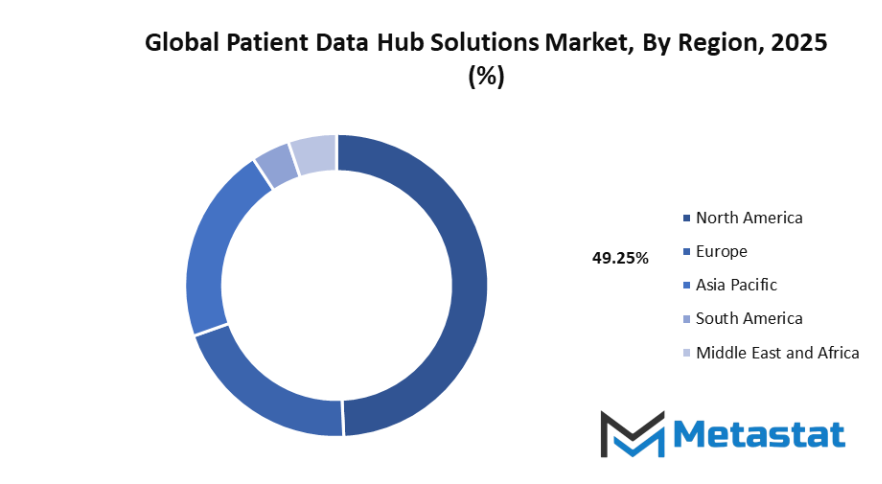

Based on geography, the global patient data hub solutions market is divided into North America, Europe, Asia-Pacific, South America, and Middle East & Africa. North America is further divided in the U.S., Canada, and Mexico, whereas Europe consists of the UK, Germany, France, Italy, and Rest of Europe. Asia-Pacific is segmented into India, China, Japan, South Korea, and Rest of Asia-Pacific. The South America region includes Brazil, Argentina, and the Rest of South America, while the Middle East & Africa is categorized into GCC Countries, Egypt, South Africa, and Rest of Middle East & Africa.

Competitive Landscape & Strategic Insights

The global patient data hub solutions market has been progressively gaining significance as healthcare organizations embrace digital transformation and connected data systems. As the increasing need for handling vast amounts of patient data securely and efficiently, hospitals, research centers, and health providers are implementing sophisticated data management systems. These devices allow for smoother data exchange between different departments and higher quality clinical decisions that are supported by accurate and up-to-the-minute data. As healthcare continues to be heavily reliant on data-driven strategies, the demand for reliable patient data hub solutions will be the main driver of connected and personalized care in the future.

The market is crowded with global industry giants on one side and fast-growing regional players on the other who are both competing for a position in the market by innovation and technology. Some of the biggest names in the industry include Beghou Consulting, Capgemini (LiquidHub), Equipo Health Inc., Informatica, IntegriChain Incorporated, IQVIA, Inc., NXGN Management, LLC. (NextGen Healthcare, Inc.), Optum (UnitedHealth Group), Veeva Systems, WellSky, and ZS are among the most notable contributors to this change. These organizations are developing the platform that focuses on data integration, analytics, and patient engagement which in turn allows healthcare professionals to have easy access to exhaustive patient insights from a single source. Their continuous effort to promote data accuracy and interoperability is paving the road for new standards throughout the healthcare sector.

As the healthcare systems around the world are struggling with unconnected and decentralized patient data base, these companies are committed to providing unified solutions that not only increase clinical effectiveness but also improve patient outcomes. These centers' cloud-based technologies, artificial intelligence, and machine learning will make it possible for them to have predictive analytics, early diagnosis, and enhanced care coordination. The transition to smarter data management is supposed to make healthcare more proactive than reactive, thus providers and patients will both benefit from it.

Moreover, telemedicine along with value-based care will be the main factors that will continue to fuel the patient data hub solution adoption. Healthcare organizations are becoming more and more aware of the requirements for a central hub which would have the ability to capture and make sense of patient information coming from different sources such as electronic health records, wearables, and diagnostic equipment. By having this data integrated in a way that is available in one hub, the errors will not only be reduced to a minimum but the treatment plans will also be optimized and the patient experience will be elevated.

Going forward, the global patient data hub solutions market will keep expanding as technology becomes an integral part of contemporary healthcare. Both established organizations and new players will be working to provide improved and more secure platforms, and the sector will see ongoing innovation. The partnership between providers, software engineers, and analysts will shape the future of digital health, and patient data would be not only retained but also utilized appropriately in saving lives and enhancing medical outcomes globally.

Market Risks & Opportunities

Restraints & Challenges:

Healthcare organizations' high implementation and integration expenses: The global patient data hub solutions market will be challenged by the high setup and system integration costs. Healthcare organizations of large scales will generally necessitate huge expenditures on infrastructures, skilled professionals, and software compatibility. Less equipped hospitals will hardly be able to afford such sophisticated systems and as a result, the overall rate of adoption will be postponed.

Data privacy, security, and regulatory compliance issues arising from sharing patient information:

The global patient data hub solutions market is destined to have continual problems with data privacy and regulatory compliance. The processing of large volumes of sensitive patient data will make the patients' data the most attractive targets for breaches and misuses. Meeting global data protection regulations will require advanced encryption technologies and also continuous monitoring in order to maintain trust.

Opportunities:

Wider use of AI and cloud-based analytics to facilitate predictive healthcare and population health management:

The global patient data hub solutions market is set to increase through the incorporation of AI and cloud-based solutions. These technologies will turn patient data into valuable insights, thereby, diagnostic accuracy and treatment planning will be personalized and made more efficient. Predictive analytics will also serve population health management and the process of healthcare provision will become more informed.

Forecast & Future Outlook

- Short-Term (1–2 Years): Recovery from COVID-19 disruptions with renewed testing demand as healthcare providers emphasize metabolic risk monitoring.

- Mid-Term (3–5 Years): Greater automation and multiplex assay adoption improve throughput and cost efficiency, increasing clinical adoption.

- Long-Term (6–10 Years): Potential integration into routine metabolic screening programs globally, supported by replacement of conventional tests with advanced biomarker panels.

Market size is forecast to rise from USD 1680.5 million in 2025 to over USD 2807.4 million by 2032. Patient Data Hub Solutions will maintain dominance but face growing competition from emerging formats.

The global patient data hub solutions market will also spread its wings over telehealth integration, facilitating virtual consultations with accurate, data-driven insights. The technology will combine clinical data, wearable device metrics, and genetic data to create a holistic digital identity of every patient. As healthcare organizations will be looking to do better on interoperability, these data hubs will be the starting point for a more integrated global health network.

In the end, the future of the market will not only be in information management but how it revolutionizes enabling decision-making. It will redefine healthcare by translating cumbersome datasets into actionable intelligence that produces a more responsive, efficient, and patient-oriented care ecosystem globally.

Report Coverage

This research report categorizes the global patient data hub solutions market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the global patient data hub solutions market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the global patient data hub solutions market.

Patient Data Hub Solutions Market Key Segments:

By Solution Type

- Health Data Apps & AI Solutions

- Data Integration Solutions

- Patient 360 View Platforms

- Others

By Deployment Mode

By End-use

- Healthcare Companies

- Healthcare Providers

- Healthcare Payers

- Others (Include CRO, CDMO, etc.)

Key Global Patient Data Hub Solutions Industry Players

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential