Global Patient Administration System Market - Comprehensive Data-Driven Market Analysis & Strategic Outlook

The global patient administration system market, situated in the healthcare information technology sector, will increasingly cross over conventional administrative divides in the next few years. With healthcare institutions aiming to integrate operations and patient files under one virtual umbrella, the market will increasingly shift away from being a software for data management to that of a central component in strategic healthcare decision-making. Its future will not be characterized by electronic recording but by how it will integrate departments, automate operations, and optimize the entire patient's journey from intake to discharge.

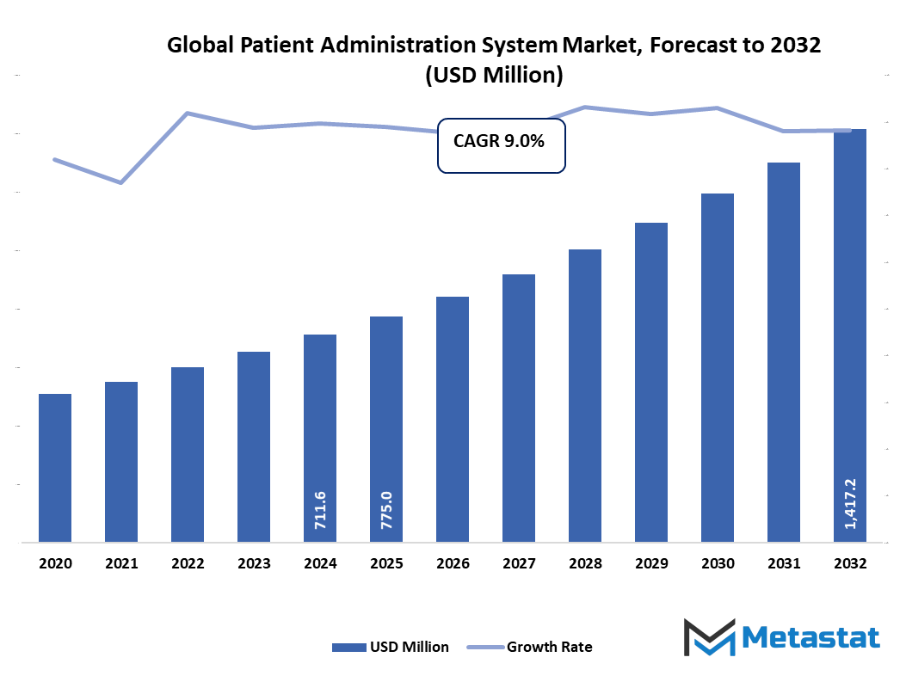

- The global patient administration system market valued at approximately USD 775 million in 2025, growing at a CAGR of around 9.0% through 2032, with potential to exceed USD 1417.2 million.

- Software account for nearly 69.9% market revenues, driving innovation and expanding applications through intense research.

- Key trends driving growth: Rising demand for digital healthcare infrastructure and hospital automation., Increasing adoption of electronic health records for efficient patient data management.

- Opportunities include Integration of PAS with AI and cloud-based platforms for enhanced operational efficiency.

- Key insight: The market is set to grow exponentially in value over the next decade, highlighting significant growth opportunities.

Is the increasing use of digital health care systems going to change the way hospitals handle patient data and make their processes more efficient? Could the use of AI and cloud technologies in patient administration systems lead to a major change in the healthcare management sector, thus making it a non-viable management model? With the continual rise of data privacy concerns, how will providers manage to keep up with the regulations and still be able to innovate in this market that is constantly evolving?

In addition to its traditional role of scheduling appointments and billing, the global patient administration system market will venture further toward predictive analysis and real-time coordination among medical and administrative staff. The systems will become more like intelligent infrastructures, increasing operational transparency and facilitating hospitals in making quicker and more informed decisions. By minimizing the need for manual intervention, healthcare professionals can spend more time enhancing the quality of patient care, further boosting institutional efficiency.

Market Segmentation Analysis

The global patient administration system market is mainly classified based on Component, Functions, Deployment, End-use.

By Component is further segmented into:

- Software: The global patient administration system market will see more emphasis on sophisticated software solutions that automate healthcare functions. These systems will make patient information more accessible, better schedule appointments, and maintain records with ease. The future will probably incorporate AI-based analytics so healthcare organizations can accomplish administrative functions with higher accuracy and efficiency.

- Services: The market will experience expansion in service offerings that facilitate software implementation, training, and maintenance. Service providers will become crucial to guaranteeing effortless system adoption and performance enhancement. Future times will witness customized service models that match the operational demands of varied healthcare environments.

By Functions the market is divided into:

- Patient Management: The global patient administration system market is set to expand via electronic platforms that efficiently handle patient data, admissions as well as discharge processes. With the help of automation, there will be fewer mistakes and better coordination among different departments, thus the time for patient service delivery will be less and the accuracy will be great in healthcare organizations.

- Outpatient Management: The market will revolve around the elimination of paper-based work in outpatient departments, from scheduling appointments to scheduling follow-ups. More interoperability between departments will also guarantee that the healthcare professionals deliver the care which is not only consistent but also timely, thus patient satisfaction as well as operating productivity will rise.

- Inventory & Procurement: The market is to be progressively inclusive of intelligent inventory and procurement systems that not only show the stocks in real-time but also reduce wastage. By automating, it will be possible to conduct predictive analysis for supply requirements, thus medical facilities will be kept at the level of optimal resource utilization and cost management.

- Revenue Management: The market will face integration of technology to make billing, insurance, and payment tracking easier. Advanced systems will allow healthcare institutions to have transparent management of finances, reduce delays, and ensure correct reimbursement, making financial stability and operations sustainable.

- Others : The global patient administration system market is going to add several new features aimed at addressing the different requirements of the medical industry. These features may include compliance monitoring, reporting, and inter-departmental communication tools that enable openness and data-driven decision-making in healthcare administration.

By Deployment the market is further divided into:

- Web & Cloud Based: The global patient administration system market is going to be increasingly dependent on web and cloud-based solutions that facilitate secure remote access to patient information. Cloud integration will give healthcare organizations the flexibility and scalability to manage multiple facilities while ensuring data protection and regulatory compliance.

- On-premises: The market is still expected to hold a share of on-premises systems, particularly in those institutions where local data control and customization are the main concerns. Such solutions will continue to offer stability and direct supervision and, thus, will attract facilities with highly stringent data governance requirements.

By End-use the global patient administration system market is divided as:

- Hospitals & Ambulatory Centers: The global patient administration system market is going to be a major part of application development in hospitals and ambulatories that require sophisticated systems with high patient volumes. These systems will streamline centralized operations, which enable faster patient handling and efficient integration of medical and administrative departments.

- Diagnostic Centers: The market is a great tool for diagnostic centers to upgrade their appointment scheduling, test tracking, and report distribution processes. Compatibility with the laboratory information system will ensure the fast turnaround of the tests and improve the communication between the physician and diagnostic team.

- Other Healthcare Institutions: The market will extend its usage to different healthcare institutions like medical care facilities and clinics. Such organizations will receive the benefits of efficient data management systems that reduce record errors, increase resource utilization, and make the coordination of patient care delivery easier.

|

Forecast Period

|

2025-2032

|

|

Market Size in 2025

|

$775 Million

|

|

Market Size by 2032

|

$1417.2 Million

|

|

Growth Rate from 2025 to 2032

|

9.0%

|

|

Base Year

|

2024

|

|

Regions Covered

|

North America, Europe, Asia-Pacific, South America, Middle East & Africa

|

Geographic Dynamics

Based on geography, the global patient administration system market is divided into North America, Europe, Asia-Pacific, South America, and Middle East & Africa. North America is further divided in the U.S., Canada, and Mexico, whereas Europe consists of the UK, Germany, France, Italy, and Rest of Europe. Asia-Pacific is segmented into India, China, Japan, South Korea, and Rest of Asia-Pacific. The South America region includes Brazil, Argentina, and the Rest of South America, while the Middle East & Africa is categorized into GCC Countries, Egypt, South Africa, and Rest of Middle East & Africa.

Competitive Landscape & Strategic Insights

The global patient administration system market is also experiencing tremendous growth with healthcare institutions all over the globe continuing to update their operations. The systems are developed to make hospital management easier, eliminate administrative mistakes, and enhance efficiency in handling patients. As clinics and hospitals try to deliver quicker and more correct services, demand for efficient digital administration tools will keep on rising. The market comprises a mix of world industry titans and local innovators who all strive to create high-end solutions that enhance the transparency and accessibility of patient data management.

Such major corporations as Abbott Laboratories, Access Group, Alcidion, Dedalus Brisbane, Getinge AB, Global Health Limited, Honeywell International, Inc., IMS MAXIMS, IQVIA Holdings, Inc., and Koninklijke Philips N.V. constitute a sizable portion of this market. In order to meet the changing demands of healthcare providers, they have been incessantly retooling their architectures. Their platforms generally bring together patient data, billing, scheduling, and resource management in one place, thus simplifying the work both of medical and administrative personnel. By focusing on automation and instant data retrieval, these companies are liberating the medical staff from the paperwork burden and allowing them to devote more time to patient care.

Also, new entrants and domestic players such as Nervecentre Software Ltd., NEXTGEN HEALTHCARE, INC. (Thoma Bravo), Oracle Corporation, RIOMED LTD., Siemens Healthineers AG (Siemens AG), System C., TPP Ltd., and Veradigm LLC are molding the market landscape. They deliver innovative solutions that are tailored precisely to local needs and are in compliance with regulations, thus small healthcare providers find it easy to implement patient administration technologies. By being affordable and customization-oriented, they are able to challenge the big corporations and thus facilitate a balance between global innovation and local availability.

While the healthcare industry is undergoing digital transformation, the market will be expanding for sure. The implementation of cloud computing, artificial intelligence, and advanced analytics will be the main factors that drive the improvement in data security and decision-making capability. Moreover, these upgrades will facilitate hospital systems interoperability that will make sharing patient information safer and quicker. The upcoming patient administration solutions will not only be of great help in managing hospitals but will also foster the advent of a more interconnected and responsive healthcare environment worldwide.

Overall, the development of the industry indicates a definitive trend towards technology-powered care. With constant innovation from firms like Abbott Laboratories, Oracle Corporation, and Siemens Healthineers AG, the global patient administration system market is destined to stay at the center of healthcare infrastructure in the future. This digital trend is changing the standards for precision, efficiency, and patient satisfaction, defining the practice of care in hospitals for decades ahead.

Market Risks & Opportunities

Restraints & Challenges

Excessive setup and maintenance expenses of sophisticated healthcare IT systems

The advanced healthcare IT infrastructure installation and maintenance cost will pose a major challenge to the global patient administration system market. Small-sized healthcare institutions will not be able to install modern systems due to a large financial outlay for the setup, upgrading, and training of workers. The constant maintenance will also increase operational costs and, thus, limit most institutions in the implementation of automation of administrative functions. The costs will slow the spread of such technology in particular in the developing world, where health budgets are limited, and technological adoption is slow.

Data privacy and security issues surrounding patient data

The global patient administration system market is going to face data protection and cybersecurity challenges on a large scale. As patient information is stored in electronic formats, healthcare professionals will need to deliver strong security measures so that data breaches and unauthorized use are avoided. Authorities and standardizing entities will demand strict adherence to security regulations for the protection of sensitive data. There might be a few entities which, because of the apprehension of data breaches, will be hesitant to fully discard paper files and shift to electronic patient administration systems. Although striving for transparency, confidentiality of patient records will pose a challenge for technology in the sector.

Opportunities

PAS integration with AI and cloud-based solutions to enhance operational efficiency

The integration between artificial intelligence and cloud computing will open immense opportunities for the global patient administration system market. AI-powered analytics will assist in simplifying administrative tasks, procedural tasks will be automated, and errors by humans will be reduced. Cloud-based solutions will facilitate real-time patient record access, which will be beneficial for the coordination not only between the different departments but also between healthcare facilities. This digital revolution will lead to quicker decision-making, enhanced patient care, and increased resource use. As healthcare systems progressively move towards digital efficiency, the adoption of AI and cloud-integrated PAS solutions will change the global operations standards.

Forecast & Future Outlook

- Short-Term (1–2 Years): Recovery from COVID-19 disruptions with renewed testing demand as healthcare providers emphasize metabolic risk monitoring.

- Mid-Term (3–5 Years): Greater automation and multiplex assay adoption improve throughput and cost efficiency, increasing clinical adoption.

- Long-Term (6–10 Years): Potential integration into routine metabolic screening programs globally, supported by replacement of conventional tests with advanced biomarker panels.

Market size is forecast to rise from USD 775 million in 2025 to over USD 1417.2 million by 2032. Patient Administration System will maintain dominance but face growing competition from emerging formats.

Cloud-based systems and interoperability with other medical software will transform the process of accessing and sharing patient information in the future. The market will tend to promote interoperability so that health networks can operate as integral ecosystems and not in silos. As regulatory and patient expectations keep changing, the market will move towards secure, scalable, and adaptive solutions that can satisfy international benchmarks. Eventually, the move away from conventional administrative tasks will establish a new chapter in healthcare administration, where patient administration systems will be the electronic backbone of delivering healthcare in the future.

Report Coverage

This research report categorizes the global patient administration system market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the global patient administration system market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the global patient administration system market.

Patient Administration System Market Key Segments:

By Component

By Functions

- Patient Management

- Outpatient Management

- Inventory & Procurement

- Revenue Management

- Others

By Deployment

- Web & Cloud Based

- On-premise

By End-use

- Hospitals & Ambulatory Centers

- Diagnostic Centers

- Other Healthcare Institutions

Key Global Patient Administration System Industry Players

- Abbott Laboratories

- Access Group

- Alcidion

- Dedalus Brisbane

- Getinge AB

- Global Health Limited

- Honeywell International, Inc.

- IMS MAXIMS

- IQVIA Holdings, Inc.

- Koninklijke Philips N.V.

- Medtronic PLC

- Nervecentre Software Ltd

- NEXTGEN HEALTHCARE, INC. (Thoma Bravo)

- Oracle Corporation

- RIOMED LTD.

- Siemens Healthineers AG (Siemens AG)

- System C.

- TPP Ltd.

- Veradigm LLC

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential