Meat Substitute Market Size, Share, By Source (Plant-based Protein, Mycoprotein, Soy-based, and Others (Pea Protein, Wheat Protein)), By Product Type (Burgers, Patties, Strips, Nuggets, Sausages, and Others (Ground, Meatballs)), By Storage Outlook (Frozen, Refrigerated, and Shelf Stable), By Distribution Channel (On-Trade and Off-Trade), Industry Analysis, Growth, Trends, and Forecasts, 2026-2033

Report ID

MSI-4536

Published

February 17, 2026

Pages

312 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Market Overview

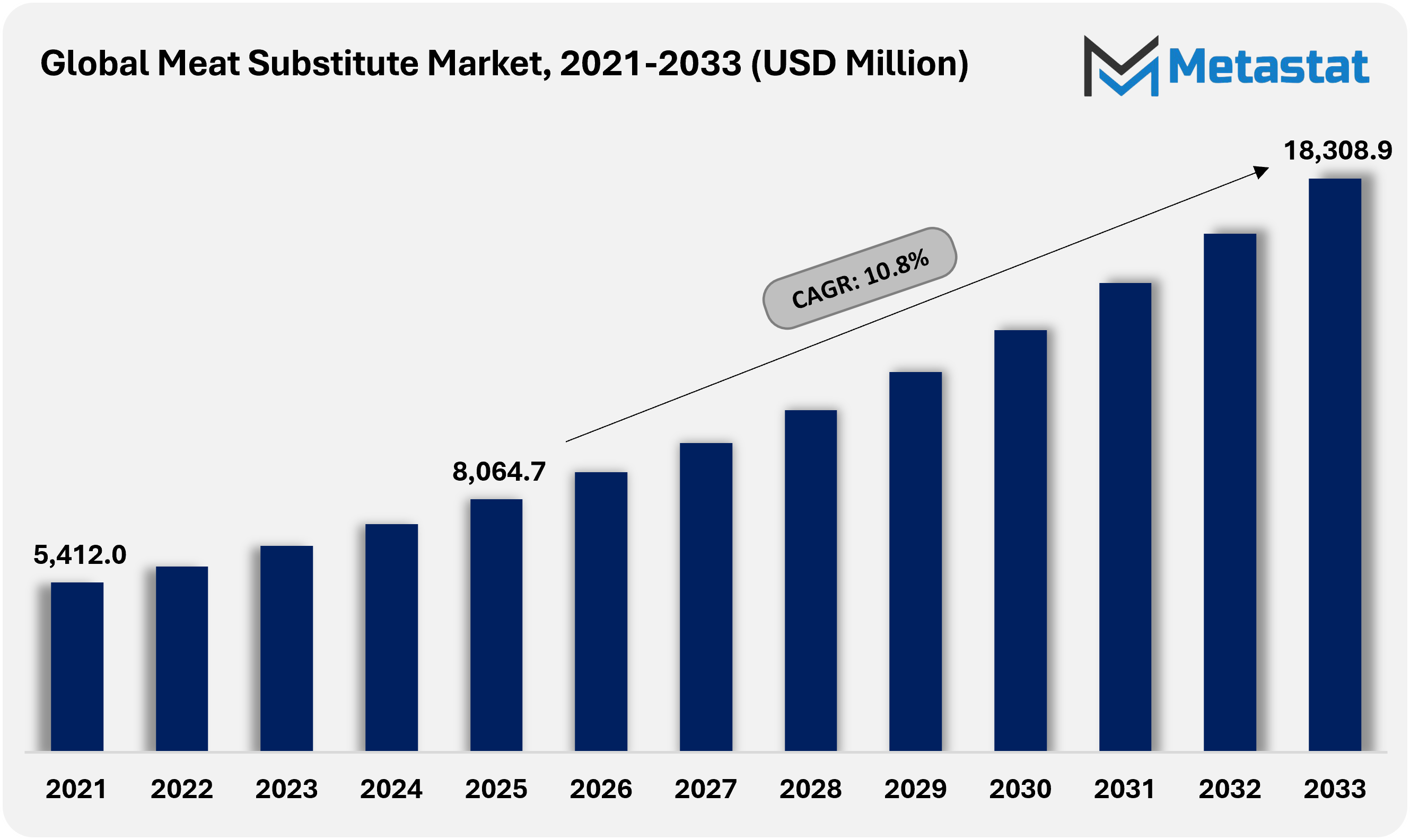

The global Meat Substitute market size was valued at USD 8,064.7 million in 2025. The market is projected to grow from USD 8,927.2 million in 2026 to USD 18,308.9 million by 2033, exhibiting a CAGR of 10.8% during the forecast period.

The Meat Substitute market has recorded strong expansion, supported by rising consumer awareness of health, sustainability, and animal welfare. Meat substitutes are products designed to replicate the taste, texture, and nutritional profile of traditional meat, typically made from plant-based proteins (soy, pea, wheat), mycoprotein, or cultured meat. The increasing demand for vegan, vegetarian, and flexitarian diets has accelerated product innovation, leading to a range of formats, including burgers, nuggets, strips, sausages, and ready-to-eat meals.

The meat substitute industry has transitioned from early rapid adoption into a more evaluation-driven phase, with broader product variety and more selective consumer repeat purchase patterns across key markets. Industry trackers estimate global retail sales of plant-based foods at around USD 28.6 billion in 2024, spanning plant-based meat, seafood, dairy alternatives, and related categories, with mid-single-digit annual growth.

Trends in ingredient sourcing and formulation show measurable changes. Wheat gluten, soy protein isolate, pea protein, and fava bean protein predominate in formulations, according to government-linked food safety dossiers and product specification sheets. Wheat gluten products used in meat substitutes such as vital wheat gluten, typically contain a very high protein content on a dry basis around 75-82% which enables strong texture and meat-like functionality in seitan and textured wheat gluten formulations.

Global Meat Substitute Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global Meat Substitute market was valued at USD 8,064.7 million in 2025 and is projected to reach USD 18,308.9 million by 2033, reflecting a CAGR of 10.8% during 2026-2033.

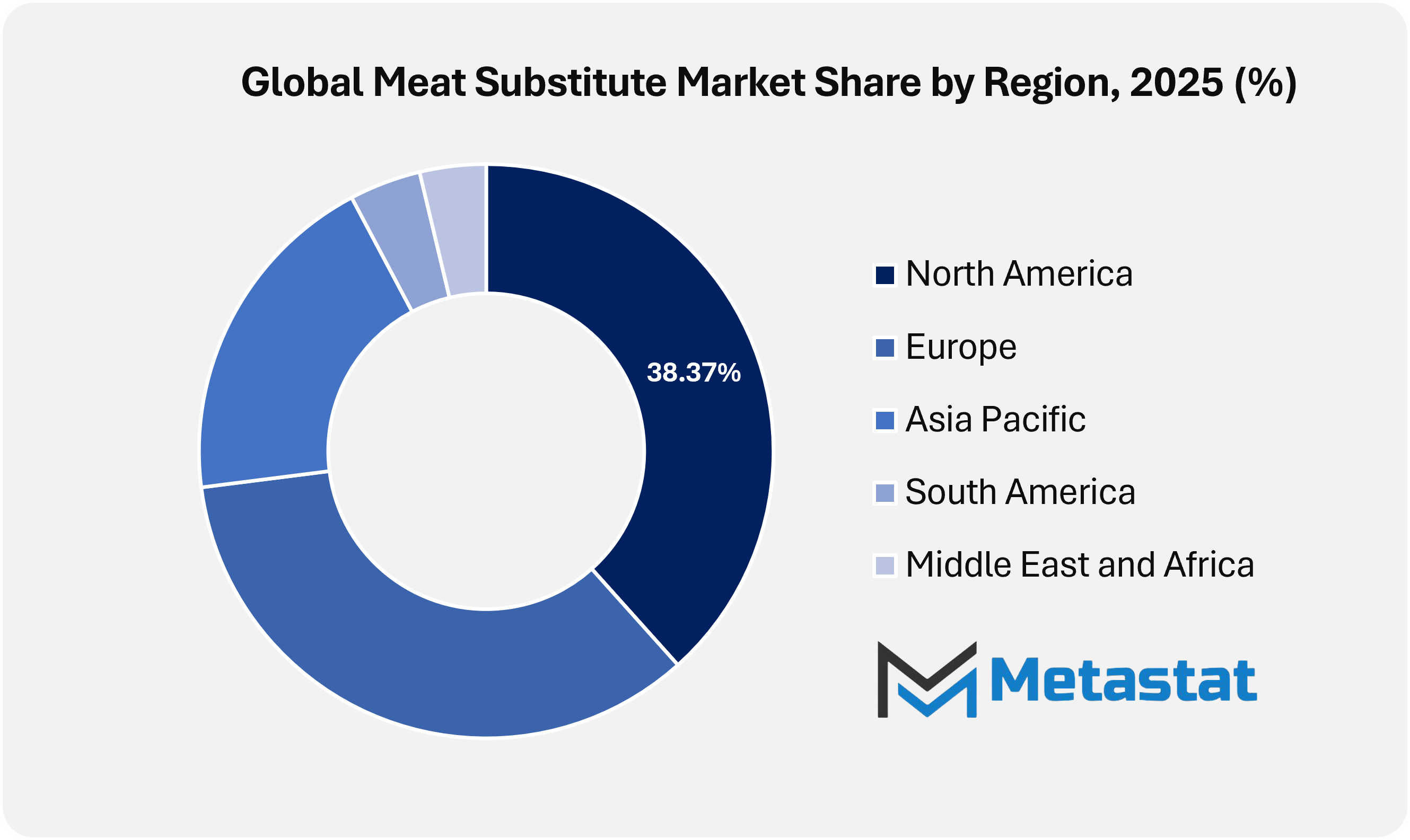

North America accounted for 38.4% of global revenue in 2025, with the United States representing the largest country-level share.

Plant-Based Protein segment accounted for 50.3% revenue share in 2025, supported by ongoing formulation innovation and portfolio expansion.

Key trends driving growth: Rising consumer health and nutrition awareness encouraging demand for high‑protein, lower‑saturated‑fat alternatives and growing ethical and environmental concerns driving consumers toward more sustainable protein sources.

Opportunities include expansion into foodservice partnerships and broader distribution channels to increase market penetration.

Key insight: The Meat Substitute market is rapidly expanding as consumers seek healthier, sustainable, and plant-based alternatives to traditional meat.

Market Dynamics

Growth Drivers:

Rising consumer health and nutrition awareness encouraging demand for high‑protein, lower‑saturated‑fat alternatives.

Consumers are increasingly attentive to food choices, supporting adoption of dietary patterns that help lower incidences of heart disease, obesity, diabetes, etc. Such diets are more likely to incorporate meat substitutes. Many meat substitute products offer comparable protein content and, in several formulations, lower saturated fat and no cholesterol. Retail pricing often remains above conventional meat, which moderates frequency of purchase. Public health guidance increasingly supports plant-forward dietary patterns for cardiometabolic outcomes, which reinforces interest in alternative proteins within flexitarian eating habits. This shift has supported wider consideration of meat substitute products, resulting in a consistent demand for the meat substitute product line.

Growing ethical and environmental concerns driving consumers toward more sustainable protein sources.

There is a growing impact of concern for animal welfare and the environmental impact of meat production. Life-cycle assessments from academic and public agencies report higher greenhouse gas emissions and land use intensity for beef and other ruminant meats versus plant-based proteins. Ethical and sustainability considerations are motivating consumers especially younger and urban demographics to choose products perceived as environmentally friendly and cruelty-free, supporting the meat substitute market’s expansion.

Restraints & Challenges:

Higher production and retail costs

Manufacturing plant-based and other alternative proteins requires specialized ingredients, extrusion technologies, and sometimes complex supply chains. As a result, retail prices for meat substitutes are higher than conventional meat equivalents. For price-sensitive consumers, this cost differential acts as a barrier to regular adoption, limiting penetration in mass-market segments.

Taste, texture, and flavor perception challenges limiting broader adoption.

Despite technological advances, many consumers still perceive plant-based meats as inferior in flavor or mouthfeel compared with traditional meat. Academic and industry research indicates texture, juiciness, and flavor parity remain inconsistent across products, which reduces trial-to-repeat conversion among conventional meat consumers. These gaps also limit repeat purchase and slow foodservice re-listing when initial consumer feedback is mixed.

Opportunities:

Expansion into foodservice partnerships

Restaurants, cafeterias, and quick-service chains offer opportunities to expose new consumers to meat substitutes in prepared meals. The institutional and chain adoption helps overcome initial taste hesitation, drives trial, and educates consumers on product versatility. This channel can also generate higher-volume sales than retail alone, providing operational efficiency and brand visibility.

Product Innovation and Taste Improvement

Product innovation and taste improvement represent a major opportunity in the meat substitute market, as consumer acceptance is strongly influenced by flavor, texture, and mouthfeel. Advances in food processing technologies such as extrusion, fermentation, and fat structuring help replicate the juiciness and bite of animal meat more closely. Improved formulations also reduce off-flavors commonly associated with plant proteins. As products become more comparable to conventional meat, they attract flexitarian and mainstream consumers, driving repeat purchases and long-term meat substitute market growth.

Market Segmentation Analysis

The global Meat Substitute market is mainly classified based on Source, Product Type, Storage Outlook, and Distribution Channel.

By Source, the market is segmented into:

Plant-based Protein

Plant-based Protein includes grains, oilseeds, and legumes, owing to its widespread availability, simpler production process, and familiarity with consumers, it leads the market. Plant-based proteins are widely used in processed meat substitutes for their functional and nutritional benefits.

Mycoprotein

Fungi-based biomass is fermented to make mycoprotein. It is a good substitute for whole-cut beef owing to its high protein content and fibrous texture. Adoption is growing, though regulatory approvals and higher production costs limit rapid scaling.

Soy-based

Soy protein is one of the earliest and most established sources used in meat substitutes. It provides high protein content and strong texturizing properties at relatively low cost. However, allergen concerns and GMO perceptions in some regions have slowed growth.

Others (Pea Protein, Wheat Protein, etc.)

The other segment includes blended proteins, wheat, fava beans, and peas. Wheat protein is prized for its exceptional flexibility and texture, while pea protein is becoming more popular owing to its allergen-friendly orientation. Blends are increasingly used to balance taste, nutrition, and cost.

By Product Type the market is divided into:

Burgers/Patties

Burgers and patties represent the most established product category, driven by early foodservice adoption and consumer familiarity. They serve as an entry point for new consumers experimenting with meat substitutes.

Strips & Nuggets

Strips and nuggets are gaining popularity due to their versatility in ready meals and quick-service menus. Their bite-sized format allows easier replication of meat texture and flavor. These products perform well in both retail and foodservice channels.

Sausages

Plant-based sausages benefit from seasoning-heavy formulations that help mask protein off-flavors. They are widely consumed in breakfast and grill formats. Demand is supported by cultural acceptance of processed sausage products across regions.

Others (Ground, Meatballs, etc.)

Other segment includes minced alternatives, meatballs, and crumble formats used in home cooking and foodservice. These products are easier to formulate and integrate into existing recipes. Growth is supported by increasing use in institutional and bulk catering.

By Storage Outlook the market is further divided into:

Frozen

Frozen meat substitutes products have longer shelf life and reduced spoilage risk. This format supports international trade and foodservice supply chains. Frozen products also retain texture and quality during storage and transport.

Refrigerated

Refrigerated products are positioned as fresher and closer to conventional meat. They appeal to consumers seeking premium or minimally processed options. However, shorter shelf life increases logistical complexity and retail shrink.

Shelf Stable

Shelf-stable products include canned, dried, or ambient formulations. While still a smaller segment, they are gaining attention for emergency food supplies and regions with limited cold-chain infrastructure.

By Distribution Channel the global Meat Substitute market is divided as:

On-Trade

The on-trade channel includes restaurants, cafes, and institutional foodservice. It plays a key role in consumer trial and awareness, particularly through menu integration. Partnerships with foodservice operators help normalize meat substitutes.

Off-Trade

Off-trade includes supermarkets, specialty stores, and online retail. It accounts for the majority of sales volume, driven by household consumption. Product variety, pricing strategies, and in-store placement significantly influence purchasing behaviour.

By Region:

Based on geography, the global Meat Substitute market is divided into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America Meat Substitute market is projected to expand during 2026-2033, reaching a market size of USD 6,995.8 million by 2033.

In North America, rising incidence of lifestyle-related conditions such as cardiovascular disease and obesity has accelerated interest in alternative proteins. Public dietary guidelines and advocacy from health organizations increasingly emphasize reduced saturated fat intake and diversified protein sources, reinforcing demand for plant-based meat substitutes among flexitarian and health-conscious consumers. The region benefits from a mature food innovation landscape, supported by venture funding, food-tech incubators, and collaboration between startups and large food manufacturers. This ecosystem has enabled rapid product development, branding, and retail penetration, making North America a launchpad for new meat substitute formats and formulations.

Asia Pacific presents strong opportunities linked to urbanization, income growth, and protein diversification initiatives across major economies. Governments and food organizations in countries such as China, India, and Southeast Asia are encouraging protein diversification to improve food security, creating favorable conditions for plant-based and alternative protein adoption alongside traditional diets. Many Asia Pacific cuisines already incorporate tofu, tempeh, wheat gluten, and legume-based proteins. This cultural familiarity reduces the behavioral barrier to meat substitutes and allows manufacturers to localize products more effectively. The opportunity lies in modernizing traditional formats into convenient, branded meat substitute products for urban consumers.

Across Europe, regulatory focus on sustainability, carbon reduction, and food labeling has positioned meat substitutes as part of broader climate and agricultural policy discussions. Public procurement initiatives and emissions-reduction targets are supporting adoption in institutional catering, even as consumer scrutiny around ultra-processed foods moderates retail growth. In the Middle East, demand is emerging primarily from urban, expatriate, and tourism-driven foodservice sectors. Import dependence for protein and interest in food security have led governments to explore alternative proteins, though higher prices and limited local manufacturing constrain mass adoption.

Competitive Landscape & Strategic Insights

The competitive landscape of the meat substitute market is characterized by a mix of early innovators, diversified global food corporations, ingredient specialists, and regionally focused brands. Beyond Meat, Impossible Foods, and Quorn Foods are widely regarded as category leaders owing to their early market entry, strong brand recognition, and continuous investment in product innovation, particularly in improving taste, texture, and nutritional profiles. These companies have played a central role in shaping consumer awareness and establishing plant-based meat as a mainstream retail and foodservice category.

Large multinational food companies such as Nestlé, Unilever Group, Maple Leaf Foods, JBS SA, and Kellanova have strengthened the competitive intensity by leveraging existing manufacturing scale, supply chains, and distribution networks. The Vegetarian Butcher, Garden (Gardein), MorningStar Farms, Lightlife Foods, and Yves Veggie Cuisine are getting benefit from this backing, enabling broader geographic reach and portfolio expansion across multiple product formats.

Ingredient and upstream specialists including Roquette Frères, PURIS, BENEO GmbH, and Axiom Foods plays a critical role in the value chain by supplying plant-based proteins such as pea, rice, and functional carbohydrate ingredients. These companies influence product performance, cost structure, and clean-label positioning, and are increasingly collaborating with consumer-facing brands to develop customized protein solutions.

Regionally focused and challenger brands such as VBites Foods, Like Meat, Meatless Farm, Cauldron, Tofoo, Tofurky, Trader Joe’s, and Amy’s Kitchen emphasize differentiated positioning through clean-label claims, organic sourcing, private-label strategies, or traditional plant-based formats. Their strength lies in niche consumer loyalty and strong presence in select retail or foodservice channels.

Emerging and high-growth players from developing markets, including Greenovative Foods Pvt Ltd., Gooddot, Imagine Meats, and Greenest, are expanding rapidly by targeting price-sensitive consumers and adapting products to local taste preferences. These companies are contributing to market diversification, particularly in Asia, by offering accessible and culturally relevant meat substitute options.

Forecast & Future Outlook

Market size is forecast to rise from USD 8,064.7 million in 2025 to over USD 18,308.9 million by 2033.

The future outlook of the meat substitute market will be driven by gradual improvements in taste, texture, and affordability rather than rapid category expansion. Advances in ingredient science, protein blending, and processing technologies are expected to enhance product quality and cost efficiency. Growing institutional demand from foodservice, corporate cafeterias, and public procurement programs will support steady volumes. In Asia Pacific, population growth and protein diversification initiatives will create incremental opportunities, while in mature markets innovation will focus on cleaner labels and targeted use cases.

This research report categorizes the Meat Substitute market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Meat Substitute market. Recent market developments and competitive strategies such as expansion, product launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Meat Substitute market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 10.8% from 2026 to 2033

Revenue Unit

USD million

Sales Volume Unit

Kilotons

Segmentation

By Source, Product Type, Storage Outlook, Distribution Channel, and Region

By Source

Plant-based Protein

Mycoprotein

Soy-based

Others (Pea Protein, Wheat Protein, etc.)

By Product Type

Burgers/Patties

Strips & Nuggets

Sausages

Others (Ground, Meatballs, etc.)

By Storage Outlook

Frozen

Refrigerated

Shelf Stable

By Distribution Channel

On-Trade

Off-Trade

By Region

North America (By Source, Product Type, Storage Outlook, Distribution Channel, and Country)

United States

Canada

Mexico

Europe (By Source, Product Type, Storage Outlook, Distribution Channel, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Source, Product Type, Storage Outlook, Distribution Channel, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Source, Product Type, Storage Outlook, Distribution Channel, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Source, Product Type, Storage Outlook, Distribution Channel, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Full in-depth analysis of the parent Industry

Important changes in market and its dynamics

Segmentation details of the market

Historical, on-going, and projected market analysis in terms of volume and value

Kazakhstan Frozen Potato Products market size is valued at USD 26.4 million in 2025 and is projected to reach USD 53.0 million in 2033, at a CAGR of 9.0% from 2026 to 2033.

Switzerland Poke Food market size is valued at USD 29.2 million in 2025 and is projected to reach USD 44.5 million in 2033, at a CAGR of 5.5% from 2026 to 2033.

Netherlands Food and Beverages QA, QC, and Compliance Software Solutions Market Size, Share, Trends, 2033

Netherlands F&B QA, QC, and Compliance Software Solutions market size is valued at USD 272.5 million in 2025 and is projected to reach USD 421.3 million in 2033, at a CAGR of 5.6% from 2026 to 2033.

Netherlands F&B QA, QC, and Compliance Software Solutions Market, Netherlands F&B QA, QC, and Compliance Software Solutions Market Size, Netherlands F&B QA, QC, and Compliance Software Solutions Market Share, Netherlands F&B QA, QC, and Compliance Software Solutions Market Analysis, Netherlands F&B QA, QC, and Compliance Software Solutions Market Growth, Netherlands F&B QA, QC, and Compliance Software Solutions Market Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market Research Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Forecast, Netherlands F&B QA, QC, and Compliance Software Solutions, Netherlands F&B QA, QC, and Compliance Software Solutions Market Research, Netherlands F&B QA, QC, and Compliance Software Solutions Industry, Netherlands F&B QA, QC, and Compliance Software Solutions Industry Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Data, Netherlands F&B QA, QC, and Compliance Software Solutions Statistics, Netherlands F&B QA, QC, and Compliance Software Solutions Market Statistics, Netherlands F&B QA, QC, and Compliance Software Solutions Industry Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market News, Netherlands F&B QA, QC, and Compliance Software Solutions Forecasts, Netherlands F&B QA, QC, and Compliance Software Solutions Market Intelligence Report

Global Antibiotic-Free Pork market size is valued at USD 25,430.6 million in 2025 and is projected to reach USD 42,528 million in 2033, at a CAGR of 6.6% from 2026 to 2033