Home Equity Lending Market By Type (Home Equity Loans and Home Equity Lines of Credit (HELOCs), By Interest Rate Type (Fixed-rate Loans and Variable-rate Loans), By Loan Duration (Short-term Loans and Long-term Loans), By End Users (Residential Property Owners and Commercial Property Owners), Industry Analysis, Size, Share, Growth, Trends, and Forecast, 2025-2032

Report ID

MSI-3347

Published

January 25, 2026

Pages

255 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

MARKET OVERVIEW

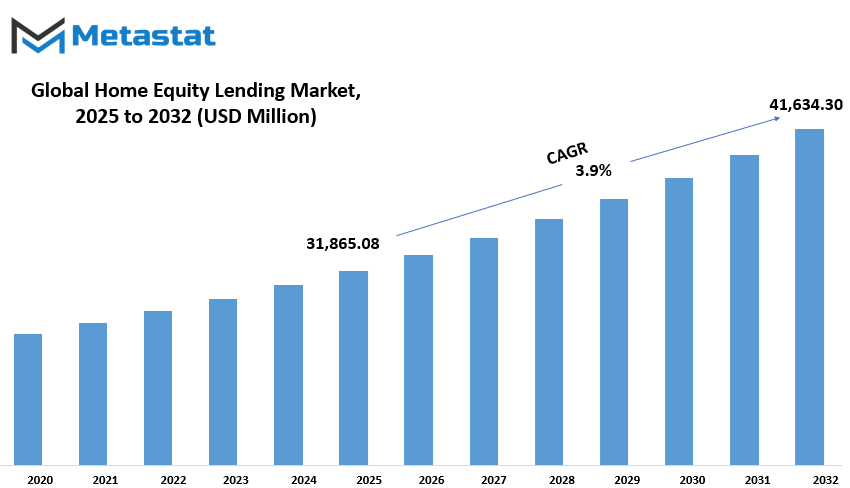

Global Home Equity Lending market is estimated to reach $41,634.30 Million by 2032; growing at a CAGR of 3.9% from 2025 to 2032.

The Global Home Equity Lending market and its industry continue to reshape financial landscapes, offering homeowners avenues to leverage property value for diverse financial needs. While much discussion revolves around interest rates, borrowing limits, and regulatory frameworks, there is a broader spectrum that remains unexplored. The market extends far beyond traditional loan structures, influencing economic patterns, consumer behavior, and technological advancements that redefine lending practices.

With constantly changing financial tools, the relevance of home equity lending extends to less researched fields. Global economic trends and the role of equity-based borrowing remain an area of interest as fluctuating real estate values and the economy change the access to such financial tools. Emerging economies, once considered second-tier players, are now influencing the direction, thereby changing traditional lending models.

Improving access to a wider population, alternative methods of credit scoring are gaining importance as financial institutions explore new markets. Technology has transformed lending mechanisms as well. Digital lending platforms are no longer restricted to personal or business loans but now also incorporate home equity lending.

Risk assessment and loan approval processes incorporate artificial intelligence, blockchain, and machine learning. As a result, reliance on traditional credit evaluations decreases. The application processing time will decrease, while transparency and security will improve for financial institutions.

Shifting societal trends further influence lending patterns. Changes in homeownership demographics, especially among younger generations, will change the dynamics of equity-based borrowing. Unlike previous generations who considered property as a lifelong asset, contemporary homeowners may use home equity in innovative ways, from funding entrepreneurial ventures to navigating financial uncertainty.

As financial literacy grows, borrowers will likely adopt strategic approaches to home equity utilization, emphasizing wealth-building rather than short-term liquidity.The regulatory framework, viewed by many as straitjacketing, is likely to evolve as regulators acknowledge the changing dynamics of lending.

International regulatory agencies will cooperate in formulating regulations that strike a balance between consumer protection and financial market fluidity. The consequences of such regulations will not only determine borrowing patterns but also dictate investor confidence in mortgage-backed securities and lending institutions. It will shift the financial sector towards sustainability and lead to innovative lending models that are in line with the goals of environmental and social responsibility.

Beyond economic implications, the Global Home Equity Lending market contributes to broader financial stability discussions. As housing markets fluctuate, lenders and policymakers will examine the correlation between equity borrowing and long-term economic resilience. Strategic home equity management may emerge as a critical component of financial planning, encouraging borrowers to consider long-term wealth preservation alongside immediate financial needs.

The extension of this market goes to far-flung lands, intertwined with investment strategy and financial planning that goes beyond simple lending structures. The interlinkage between the evolution of financial technology, changes in regulations, and changes in consumer behavior will define the course of the future for home equity lending. Much of the discussions are based on the quantitatively based metrics such as valuation of markets and interest rate moves, but this financial instrument truly has much deeper potential with the adaptability to changing financial environments.

GROWTH FACTORS

The Global Home Equity Lending market has become very promising owing to the reason that home appreciation offers more available equity for more borrowing. All these increased levels of available equities have seen a significant motivation among people, thus forcing more to take equity loans for considerable expense like major home improvements or to pay college costs. Low interest rate environments add to the attractiveness of these loans in the sense that borrowing is less expensive and more appealing in taking into funds by homeowners. It saves homeowners from accessing high-interest credit options.

Despite the promising opportunities of this market, there are challenges that might limit it. Among the critical areas of concern is stringent lending regulation and credit requirements that make some borrowers difficult to qualify for home equity loans. Usually, lenders apply quite strict criteria that may lock out some individuals because they may not meet the threshold credit score or income level required. This usually limits the opportunities for homeowners who would otherwise make good use of their home equity.

Other main factors that form the home equity lending landscape involve economic uncertainties. During unstable conditions, consumers take fewer risks over borrowing against the house. If there is no job security or inflation, besides the possibility of a downturn in the economy, people are discouraged from taking a loan even with much equity locked in the property. This also slows down growth in the markets as fewer choose to take loans during uncertain economic times.

Though such challenges may face the demand, the rising demand for home renovation finance is expected to open new market opportunities. Increasingly, homeowners are choosing to invest in property upgrades, whether for enhancing the living space or increasing the resale value. Going forward with modernization as key factors in housing markets, the need for accessible financing options will presumably continue growing. Home equity loans are one of the possible ways to fund renovations, so they are always attractive for people who want to improve their homes without taking unsecured debt.

In the near future, home equity lending is expected to undergo changes in line with economic and regulatory factors. Although tighter rules may continue to restrict access to some borrowers, the overall demand for home equity financing is likely to remain in place. The balance of risk versus opportunities will vary the shape the market will take, and interest rates, housing prices, and consumer confidence will play a big part in shaping the outcome. When economic stability has increased and lending policies become more accessible, the opportunity to drive growth further through homeowners taking advantage of available equity could only increase.

MARKET SEGMENTATION

By Type

The Global Home Equity Lending market is constantly growing with more homeowners seeking financial flexibility. The market is broadly categorized into two major types: Home Equity Loans, worth $18,593.74 million, and Home Equity Lines of Credit, commonly known as HELOCs. These are a group of financial products that assist homeowners in accessing funds which can be utilized based on the home's equity. As housing prices fluctuate and interest rates shift, borrowers explore these options to manage expenses, fund renovations, or consolidate debts. Home Equity Loans offer a lump sum with a fixed interest rate, making them an attractive choice for individuals who prefer predictable payments.

Since the borrower gets the full loan amount upfront, he can spend it on large projects or unforeseen expenses without worrying about the future borrowing limits. In contrast, HELOCs are a type of revolving credit. As such, the homeowner gets to withdraw as much money as is needed within their established limit. This option has more flexibility provided over ongoing expenses, though interest rates depend on market terms. Economic stability, value of the properties, and interest rates all determine demand for home equity lending. Homeowners borrow more as house prices rise due to increased equity in their property.

When the interest rates decline, it lowers the cost of borrowing and thereby makes home equity lending more appealing. In case of economic down turns, home equity lending can be restricted by imposing higher criteria, as this helps reduce risks for lenders. Financial institutions continue to perfect their lending practices to meet the demands of the market. Borrowers have to sift through different lending terms, repayment options, and eligibility criteria to find the best fit for their financial situation. Credit scores, income stability, and debt-to-income ratios are significant factors in approval processes, so it is important for borrowers to assess their financial health before applying.

Technology also contributed to this market. The borrowing process becomes much easier for homeowners through online applications and digital tools. One can easily compare options, estimate the loan amount, and apply online. Technology has been embraced by lenders as well to improve approval processes, reduce paperwork, and enhance the customer experience.

Thus, one must not use home equity as collateral without due precaution and caution. Either funds are mismanaged or unforeseen economic uncertainties can cause financial stress. Responsible borrowing, proper planning, and understanding of loan terms mean that an informed financial decision is made.

As the market grows and changes, home equity lending will forever remain one of the most valuable financial instruments available to homeowners. It is through careful decision-making and proper financial planning that individuals can make the most of these options while still maintaining long-term stability.

By Interest Rate Type

Several factors influence the global home equity lending market, with interest rate types among the most important factors determining how such loans are structured. Generally, the market is divided into two categories based on the type of interest rate used: fixed-rate loans and variable-rate loans. The two types of loans both offer different advantages to borrowers under different needs and financial conditions.

A fixed rate loan is so structured that it has an unchanging interest rate from the starting to the finishing of the loan. It is, therefore, a simple statement that says a borrower will be paying the same interest rate starting from the initial period and then to the latter period, ensuring stability and predictability. It is very popular among homeowners as it has to be done at a fixed schedule of repayment.

These loans prove particularly attractive when interest rates are low, and borrowers, in return for such a reasonable rate structure can lock into a favorable duration, and in an environment where interest rates are anticipated to rise, fixed-rate loans offer protection-ensuring borrowers that their monthly payments are immune from market fluctuations.

Variable-rate loans have their interest rates changeable over time, due often to fluctuations related to an underlying benchmark, such as the prime rate or LIBOR. The interest rates under this type of loan are usually low at initiation, as compared to fixed-rate loans. This makes variable-rate loans rather attractive in the short run, but borrowers experience a change in their monthly payments as they fluctuate.

This therefore means that even if the initial payments are lower, the cost of the loan may rise due to a rise in the interest rates. This makes variable rate loans higher risk; however, they can be advantageous in a market where interest rates are expected to decrease or stabilize for a longer term.

This is mainly a decision based on financial goals, risk tolerance, and expectations of the borrower about the future movements in interest rates. Those interested in predictability and stability in payments would go for fixed-rate loans, whereas those who are comfortable with fluctuating payments may go for variable-rate loans for initial savings. The decision mainly affects not just the monthly but also the actual long-term borrowing cost. A proper understanding between these two varieties of home equity loans is pretty important while shopping in the marketplace for home equity lending.

By Loan Duration

The Global Home Equity Lending market is a core part of the financial sector and allows homeowners to borrow against equity in their houses. Several drivers are associated with this market, including the necessity for available credit and increasing demand for flexible credit options. Home equity lending enables a borrower to tap the value he or she has generated in the property, which then can be applied for different objectives, such as home improvements, debt consolidation, or other personal financial needs.

This market has been segmented into two categories on the basis of loan duration. These are short-term loans and long-term loans. Short-term loans have a short period of usually several years. Long-term loans are usually for many decades. Depending on the need of the borrower, different loans offer varied benefits. The advantages of each loan type differ with the requirement of the individual taking the loan. Short-term loans are very convenient for individuals who require quick cash and expect to repay the loan within a short period of time. These are less expensive compared to long-term loans and, thus, are of great interest to those who repay the loan over a short time.

Long-term loans pay slowly as the client repays at a convenient time. Borrowers can repay this loan over time, which will be useful in cases where someone needs more cash or if someone prefers low monthly payments. Even though interest rates may be higher for a long-term loan, many individuals consider the ability to manage their monthly payments as well worth the additional cost.

In the home equity lending market, dividing short-term and long-term loans will ensure there is a borrowing option for almost every type of homeowner, whether financially well-situated or with other requirements and preferences when it comes to repaying the loan. For immediate needs and fast repayment ability, one may be interested in short-term loans. Long-term loans are meant for people with a more flexible approach or willing to take their time and commitment for repayment.

The Global Home Equity Lending market, thus segmented clearly between short-term and long-term loans, is a very important part of the financial services industry. It serves the wide variety of customers and thus provides flexible solutions according to the duration of the loan, that why it is commonly used by many homeowners.

By End Users

The global home equity lending market is one of the more vibrant industries within the world's finance sectors. It is an area where people borrow money based on the equity of a home, where home-owning individuals or companies use the value of the property to get a loan. The market splits into the two categories depending on the nature of end-users: residential property owners and commercial property owners. Each group typifies a certain type of borrowers with different home equity lending requirements and needs.

The majority comprises residential property owners. These house owners usually secure home equity loans or lines of credit to provide for a lot of financial obligations, including some home improvements, debt consolidation, or emergency money. Homeowners find this type of loan quite attractive because they can borrow a significant amount at relatively lower interest rates compared to other forms of borrowing.

With equity directly available from their homes, homeowners have an easier means for managing finance and achieving personal objectives. This market element is characterized by the desire to have cash available for flexibility in their finances and also to enhance their homes' value or even eliminate some urgent financial liabilities.

The other category of the home equity lending market is commercial property owners. They are the business investors or owners who have these commercial properties to take loans to get more for expansion, or just to take more properties and improve them. Commercial property owners usually apply different financial policies than the residential property owners, and the loans that they take tend to be on a larger scale and longer durations. Given that the investment in these types of assets has different natures, coupled with the risks entailed with commercial real estate investments, such terms and conditions may be so far apart from what is received for residential property owners.

Residential and commercial property owners, each with their differing needs, are the drivers of growth and diversification in the world home equity lending market. As the economic conditions and property values continue to change, the demand for home equity loans will continue to shift, and each group will look for the most favorable terms to support their financial goals. Whether it is for personal or business expansion, the global home equity lending market caters to a wide variety of borrowers with different financial objectives.

Forecast Period

2025-2032

Market Size in 2025

$31,865.08 Million

Market Size by 2032

$41,634.30 Million

Growth Rate from 2024 to 2031

3.9%

Base Year

2024

Regions Covered

North America, Europe, Asia-Pacific, South America, Middle East & Africa

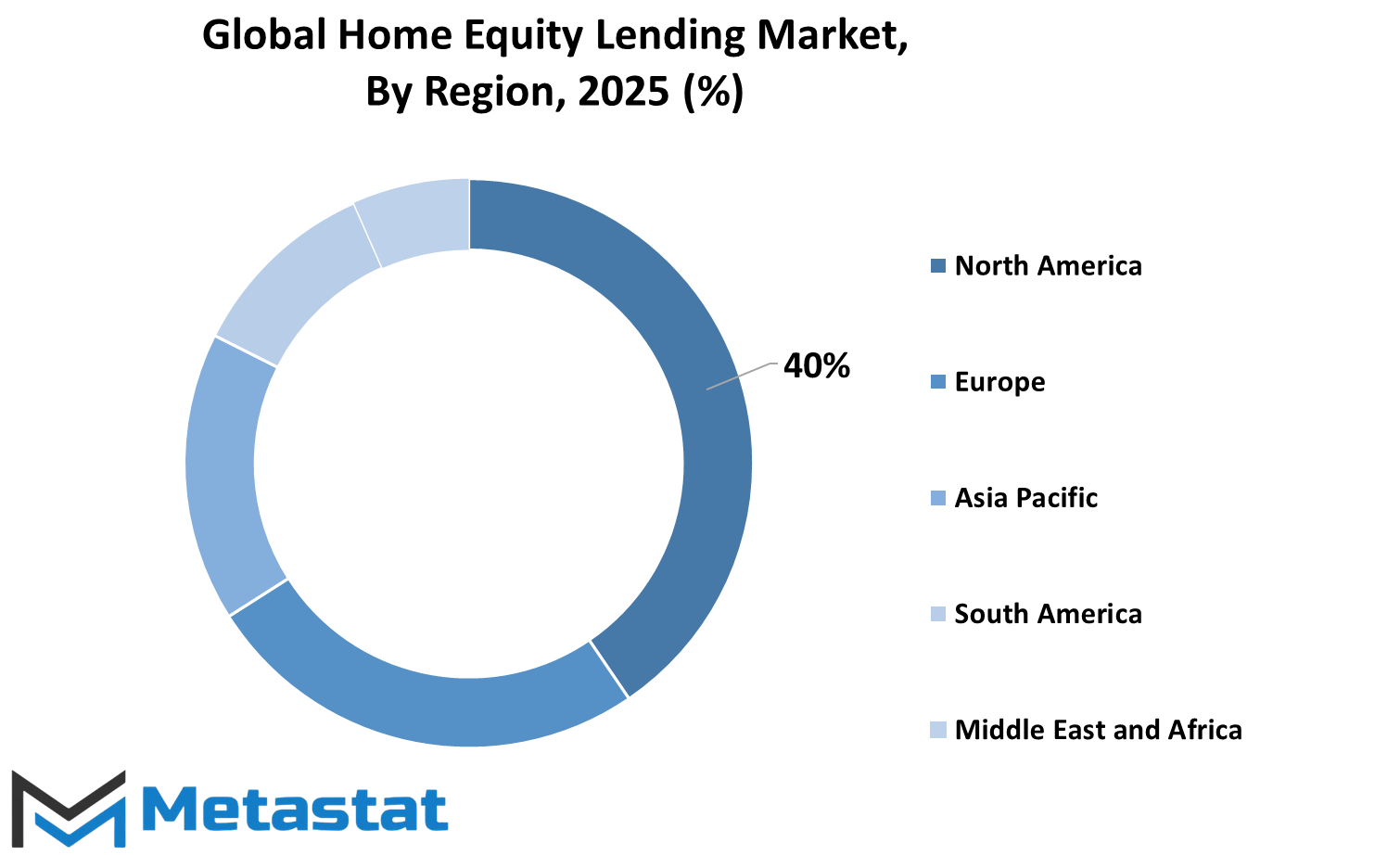

REGIONAL ANALYSIS

The global Home Equity Lending market is divided into several geographic regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Each of these regions is further broken down into specific countries and areas that play a key role in the market’s dynamics.

In North America, the market is divided into the U.S., Canada, and Mexico. The U.S. is the largest player in the market, driven by a robust financial sector and high homeownership rates. Canada follows with its stable economy and growing demand for home equity products, while Mexico, though smaller, has seen increased interest in these types of loans as its economy grows.

The other region is Europe, with the UK, Germany, France, and Italy as the major markets. The UK is standout with a mature real estate market, while Germany and France contribute significantly since they have strong economies and housing sectors. Italy is smaller but has steady demand for home equity loans; the rest of Europe also contributes to the growth of the market.

Asia-Pacific, which includes key countries like India, China, Japan, and South Korea, is an emerging region for Home Equity Lending. China’s rapidly growing real estate market, along with India’s expanding middle class, contributes to increasing demand for these financial products. Japan and South Korea are also seeing growth, with more people turning to home equity loans as part of their financial strategies. Other countries in the region, grouped as the Rest of Asia-Pacific, also show promise, as their economies develop and housing markets expand.

South America is another growing market, with Brazil and Argentina leading the way. Both countries have seen improvements in their financial sectors, making home equity lending more accessible to homeowners. Other countries in South America, collectively referred to as the Rest of South America, are also gradually participating in this market, contributing to its growth in the region.

Finally, the Middle East & Africa is divided into the GCC countries, Egypt, South Africa, and the rest of the region. The GCC countries, with their oil wealth and increasing urbanization, have a high demand for home equity loans. Egypt, with its growing population and economic challenges, sees a more moderate demand but remains important in the market. South Africa is the largest market in sub-Saharan Africa, and other countries in the region also play a role as financial markets evolve.

In conclusion, the Home Equity Lending market across these regions is diverse, with each area contributing to the overall growth in different ways based on their unique economic and housing conditions. The market will continue to expand as homeownership rates rise, economies grow, and more people seek financial solutions.

COMPETITIVE PLAYERS

Several strong players drive the global home equity lending market forward. Some of the key players in this area include well-established financial institutions, such as Wells Fargo, Bank of America, JPMorgan Chase & Co., Citigroup Inc., and U.S. Bank. Such institutions have an extensive presence in the lending sector, providing consumers with home equity loans and lines of credit throughout different regions.

Wells Fargo has been recognized for its diversified financial services and is one of the major players in the home equity lending market. As one of the oldest institutions, it has established a reputation over time for offering competitive products suited to the needs of homeowners. Bank of America is another giant institution offering flexible home equity solutions to help customers achieve their financial objectives - for enhancing their homes or even debt consolidation.

JPMorgan Chase & Co. and Citigroup Inc. also play crucial roles in this market, leveraging their extensive customer base and technological advancements to provide easy access to home equity products. These companies focus on delivering high-quality services to both existing and new customers, ensuring they maintain a strong market position. U.S. Bank, a leading national bank, contributes to the market with its tailored home equity solutions that help borrowers access funds for various purposes.

Other important players in the industry include The PNC Financial Services Group, Inc., Truist Financial Corporation, and TD Bank. These institutions are expanding their services and making home equity lending more accessible to a wider range of customers. Their innovative approaches, combined with customer-centric services, make them key contenders in the market.

Rocket Mortgage, LLC, a company that has been specializing in a digital approach towards lending, is totally transforming the way consumers can access home equity products. Application processes are simplified. The diversity and competitiveness of home equity lending sector would be furthered by other contributors such as Citizens Financial Group, Inc. and Flagstar Bank, N.A. as other sources of loans or lines of credit.

Regions Bank and Fifth Third Bank complete the list of major participants in this market. Their focus on customer-friendly services and efforts to provide differentiated lending solutions are what keep them firmly entrenched in the competitive space of home equity lending. As a whole, these institutions determine the global landscape of home equity lending, allowing consumers to explore the value embedded in their homes.

Operational Technology (OT) and Industrial Cybersecurity Mar

Operational Technology (OT) and Industrial Cybersecurity market size is valued at USD 25.8 billion in 2025 and projected to reach USD 82.7 billion by 2033.

Operational Technology (OT) and Industrial Cybersecurity market, Operational Technology (OT) and Industrial Cybersecurity Market Size, Operational Technology (OT) and Industrial Cybersecurity Market Share, Operational Technology (OT) and Industrial Cybersecurity Market Analysis, Operational Technology (OT) and Industrial Cybersecurity Market Growth, Operational Technology (OT) and Industrial Cybersecurity Market Trends, Operational Technology (OT) and Industrial Cybersecurity Market Research Report, Operational Technology (OT) and Industrial Cybersecurity Market Forecast, Operational Technology (OT) and Industrial Cybersecurity, Operational Technology (OT) and Industrial Cybersecurity Market Research, Operational Technology (OT) and Industrial Cybersecurity Industry, Operational Technology (OT) and Industrial Cybersecurity Industry Report, Operational Technology (OT) and Industrial Cybersecurity Market Data, Operational Technology (OT) and Industrial Cybersecurity Statistics, Operational Technology (OT) and Industrial Cybersecurity Market Statistics, Operational Technology (OT) and Industrial Cybersecurity Industry Trends, Operational Technology (OT) and Industrial Cybersecurity Market Report, Operational Technology (OT) and Industrial Cybersecurity Market Trends, Operational Technology (OT) and Industrial Cybersecurity Market News, Operational Technology (OT) and Industrial Cybersecurity Forecasts, Operational Technology (OT) and Industrial Cybersecurity Market Intelligence Report, Operational Technology (OT) and Industrial Cybersecurity market 2033, Operational Technology (OT) and Industrial Cybersecurity market outlook, Operational Technology (OT) and Industrial Cybersecurity market segmentation, Operational Technology (OT) and Industrial Cybersecurity market drivers, Operational Technology (OT) and Industrial Cybersecurity market restraints, Operational Technology (OT) and Industrial Cybersecurity market opportunities, Operational Technology (OT) and Industrial Cybersecurity market CAGR, Operational Technology (OT) and Industrial Cybersecurity suppliers, Operational Technology (OT) and Industrial Cybersecurity manufacturers, Operational Technology (OT) and Industrial Cybersecurity market by region, North America Operational Technology (OT) and Industrial Cybersecurity market, Asia Pacific Operational Technology (OT) and Industrial Cybersecurity market, Europe Operational Technology (OT) and Industrial Cybersecurity market, Operational Technology (OT) and Industrial Cybersecurity market competitive landscape, Operational Technology (OT) and Industrial Cybersecurity market key players, OT Security Platforms and Software market, Network Security Appliances and Industrial Gateways market, Professional and Advisory Services in OT Cybersecurity, Managed OT Security Services market, Asset Discovery, Inventory and Exposure Assessment market, Network Monitoring, Threat Detection and Incident Response market, Vulnerability, Risk and Compliance Management market, Supervisory Control and Data Acquisition Systems market, Distributed Control Systems market, Programmable Logic Controllers and Safety Systems market, Industrial IoT and Edge Devices market, Manufacturing OT and Industrial Cybersecurity market, Energy and Utilities OT and Industrial Cybersecurity market.

New Zealand Optical Encryption Market Size, Share, Trends, 2033

New Zealand Optical Encryption market size is valued at USD 34.5 million in 2025 and is projected to reach USD 76.9 million in 2033, at a CAGR of 10.3% from 2026 to 2033.

New Zealand Optical Encryption Market, New Zealand Optical Encryption Market Size, New Zealand Optical Encryption Market Share, New Zealand Optical Encryption Market Analysis, New Zealand Optical Encryption Market Growth, New Zealand Optical Encryption Market Trends, New Zealand Optical Encryption Market Research Report, New Zealand Optical Encryption Market Forecast, New Zealand Optical Encryption, New Zealand Optical Encryption Market Research, New Zealand Optical Encryption Industry, New Zealand Optical Encryption Industry Report, New Zealand Optical Encryption Market Data, New Zealand Optical Encryption Statistics, New Zealand Optical Encryption Market Statistics, New Zealand Optical Encryption Industry Trends, New Zealand Optical Encryption Market Report, New Zealand Optical Encryption Market Trends, New Zealand Optical Encryption Market News, New Zealand Optical Encryption Forecasts, New Zealand Optical Encryption Market Intelligence Report

Retail Project Management Software market size is valued at USD 1,505.5 million in 2025 and is projected to reach USD 3,524.9 million in 2033, at a CAGR of 11.2% from 2026 to 2033.

Generative AI in Analytics Market Size, Share, Trends, 2033

Generative AI in Analytics market size is valued at USD 1.6 billion in 2025 and is projected to reach USD 10.9 billion in 2033, at a CAGR of 26.8% from 2026 to 2033.

Generative AI in Analytics Market, Generative AI in Analytics Market Size, Generative AI in Analytics Market Share, Generative AI in Analytics Market Analysis, Generative AI in Analytics Market Growth, Generative AI in Analytics Market Trends, Generative AI in Analytics Market Research Report, Generative AI in Analytics Market Forecast, Generative AI in Analytics, Generative AI in Analytics Market Research, Generative AI in Analytics Industry, Generative AI in Analytics Industry Report, Generative AI in Analytics Market Data, Generative AI in Analytics Statistics, Generative AI in Analytics Market Statistics, Generative AI in Analytics Industry Trends, Generative AI in Analytics Market Report, Generative AI in Analytics Market Trends, Generative AI in Analytics Market News, Generative AI in Analytics Forecasts, Generative AI in Analytics Market Intelligence Report