Heat Transfer Equipment Market By Type (Shell, Tube, Plate, Air Cooled, and Other), By Application (Petrochemical, Electric Power, Metallurgy, Shipbuilding Industry, Mechanical Industry, Central Heating, Food Industry, and Others), Industry Analysis, Size, Share, Growth, Trends, and Forecast, 2033

Report ID

MSI-4277

Published

October 14, 2025

Pages

255 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Global Heat Transfer Equipment Market- Comprehensive Data-Driven Market Analysis & Strategic Outlook

The global heat transfer equipment market will experience an interesting ride from simple mechanical equipment to advanced systems with the ability to control complex thermal operations. Its origin will start at the beginning of the industrial age when crude heat exchangers were first introduced in steam power stations and chemical plants to achieve peak efficiency. By the mid-20th century, technological development in metallurgy and fluid mechanics will allow the producer to work with new materials and configurations and design smaller and more efficient units. In the 1970s, a breakthrough will occur when the green movement will cause industries to cut down wastage of energy, resulting in heat recovery systems being installed on a large scale.

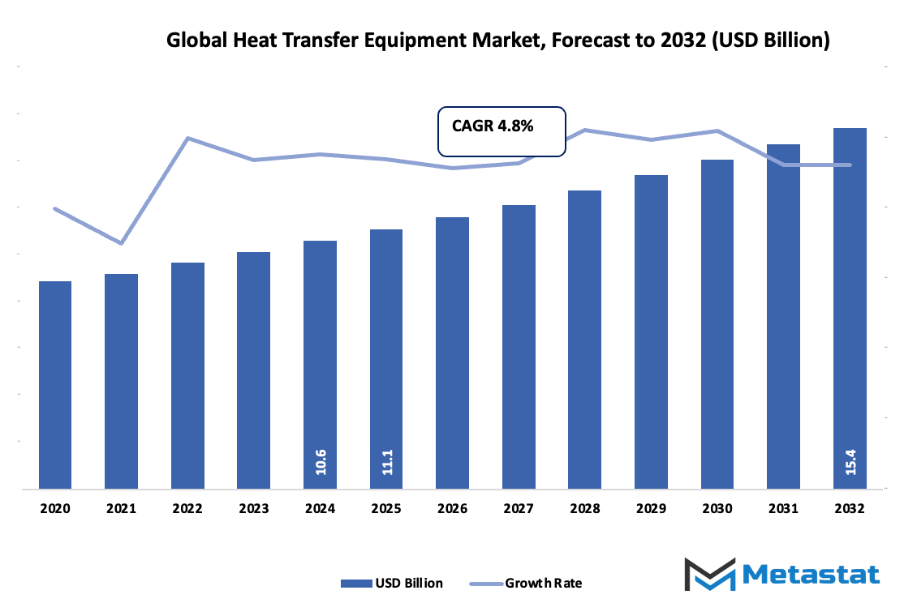

Global heat transfer equipment market value of approximately USD 11.1 Billion in the year 2025, growing at approximately 4.8% through 2032, with the scope for even greater growth above USD 15.4 Billion.

Shell & Tube has approximately 42.6% market share, with the lead in innovation and greater use through thorough research.

Drivers of growth: Greater manufacturing sector growth and industrialization, Greater energy-efficient heating and cooling system demand

Opportunities are: Adoption of new-generation materials and technology for improved thermal efficiency and green energy applications

Major takeaway: The market will grow exponentially in value over the next decade, offering tremendous opportunities for expansion.

With time, the company will evolve to suit new consumer and industrial needs. Simplicity and reliability will be the only features in early designs. As processing conditions are made more sophisticated and energy gets expensive, the need will shift to equipment that can resist higher temperature, pressure, and corrosive fluid exposure. This evolution will bring innovation in tube-and-shell, plate heat exchanger, and air-cooled design.

Technological innovation will be at the forefront of the future way of the global heat transfer equipment market. Computerized monitoring systems, condition monitoring and new materials will continually reshape Heat Transfer Equipment design, operation and maintenance. Companies will invest in research to maximize thermal performance and minimize environmental impact, anticipating increasingly stringent global regulation of emissions and energy use.

Concurrently, local industrialization trends will dictate adoption patterns because newly emerging markets demand flexible and cheap solutions. Regulatory pressures will increasingly aim at energy efficiency, safety standards, and environmental operations that will compel manufacturers to continually alter their processes. In addition, petrochemicals, power generation industries, and food processing industries will continue demanding hybrid technologies and modular technologies to meet shifting production needs.

By linking its historical roots to ongoing technological and regulatory evolution, the global heat transfer equipment market will be poised to become an integral force behind industrial modernization. Its evolution will demonstrate how a critical industry component can continue to evolve to meet advanced operating requirements, demonstrating the inexorable interdependence of innovation, efficiency, and regulation.

Market Segments

The global heat transfer equipment market is mainly classified based on Type, Application.

By Type is further segmented into:

Shell & Tube: The category will include equipment where heat transfer is achieved between liquids divided by a solid barrier, typically a cylindrical shell with tubes. Shell & tube heat exchangers are highly popular across various industries due to their high efficacy, periodicity, and high pressure and temperature resistance and hence are a key part of the worldwide Heat Transfer Equipment industry.

Plate: Plate heat exchangers will be made up of a number of thin, flat plates placed on top of each other to promote heat transfer between fluids. Because of their compact size, high efficiency, and ease of maintenance, they are suitable for a wide range of applications. Exchangers are gaining popularity in the global heat transfer equipment market for employment in products requiring immediate heat transfer and least installation space.

Air Cooled: Air cooled heat exchangers make use of surrounding air to cool or condense fluids. Air cooled systems do not use water and are environmentally friendly. Air cooled equipment will remain to face demand in regions of scarce water resources, facilitating development and growth of the global heat transfer equipment market.

Other: This segment will include proprietary Heat Transfer Equipment that cannot be placed under general description, such as spiral or scraped surface exchangers. The systems are specifically designed for specific industrial needs and contribute additional to the product portfolio in the global Heat Transfer Equipment industry by offering bespoke solutions for severe heat transfer applications.

By Application the market is divided into:

Petrochemical: Widespread use of Heat Transfer Equipment will be witnessed in the petrochemical industry for thermal regulation of chemical reactions, refining, and fluid processing. Effective heat transfer guarantees process stability, energy conservation, and safety, and thus this industry emerges as a leading contributor to the global heat transfer equipment market.

Electric Power & Metallurgy: Electric power generation and metallurgy are key applications wherein heat exchangers must be employed in order to cool as well as control temperature. Efficiency and life are the basis of equipment performance. Growing energy requirement and industrial processes stimulate steady adoption of the systems in the market.

Shipbuilding Industry: Shipbuilding industry will use Heat Transfer Equipment to cool engines, for HVAC, and other applications on board. Efficient systems improve ships' efficiency and safety. As world trade and naval construction continue to grow, shipbuilding industry is a major sector of application for the world Heat Transfer Equipment industry.

Mechanical Industry: Mechanical industries use heat exchangers to maintain the equipment at temperature and enhance production efficiency. Machinery cooling, lubrication systems, and industrial process support are uses that are witnessed here. Demand from this market will keep on fueling the growth of the market.

Central Heating: Central heating systems in residential and commercial settings use Heat Transfer Equipment to transfer heat. Efficient design and energy conservation are the primary motivators. Urbanization and infrastructure lead to greater consumption in the worldwide market for Heat Transfer Equipment.

Food Industry: Heat Transfer Equipment has applications in food processing for controlling heat in cooking, pasteurization, and refrigeration. Product safety and quality are extremely important, prompting continuous adoption and growth in the market.

Others: Other industrial applications apart from the above-mentioned industries, i.e., chemical processing, pharmaceuticals, and textiles. Equipment that changes and is specialized continues to expand the scope and applicability of the global heat transfer equipment market to various industries.

Forecast Period

2025-2032

Market Size in 2025

$11.1Billion

Market Size by 2032

$15.4Billion

Growth Rate from 2025 to 2032

4.8%

Base Year

2025

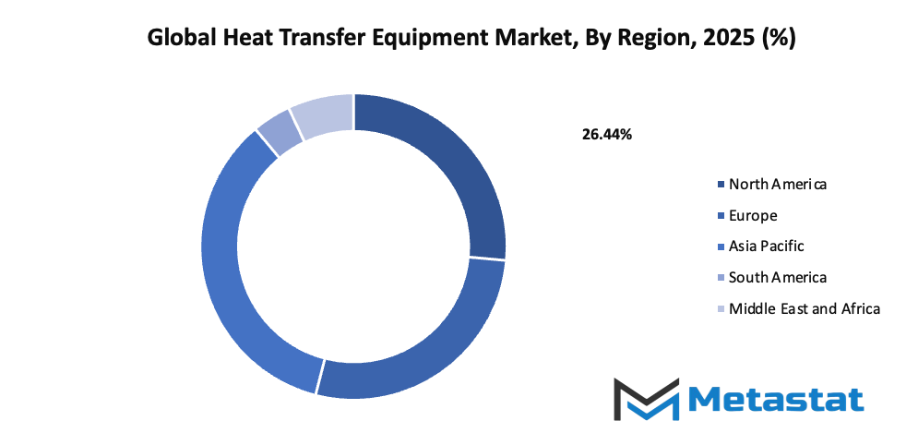

Regions Covered

North America, Europe, Asia-Pacific, South America, Middle East & Africa

By Region:

Based on geography, the global heat transfer equipment market is divided into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

North America is further divided into the U.S., Canada, and Mexico, whereas Europe consists of the UK, Germany, France, Italy, and the Rest of Europe.

Asia-Pacific is segmented into India, China, Japan, South Korea, and the Rest of Asia-Pacific.

The South America region includes Brazil, Argentina, and the Rest of South America, while the Middle East & Africa is categorized into GCC Countries, Egypt, South Africa, and the Rest of the Middle East & Africa.

Growth Drivers

Increasing industrialization and expansion of manufacturing sectors:The global heat transfer equipment market is witnessing growth due to the steady rise in industrial activities and the continuous expansion of manufacturing facilities across various regions. The growing need for effective thermal management systems in industries such as chemical, oil and gas, food processing, and power generation is creating consistent demand. As more production plants are established to meet global consumption needs, efficient heat transfer systems are becoming essential for optimizing operations, improving productivity, and ensuring process safety. This expansion directly supports the market’s development and encourages the adoption of innovative heat exchange technologies.

Rising demand for energy-efficient heating and cooling solutions:The global heat transfer equipment market is also being driven by the rising need for energy-efficient heating and cooling systems that help reduce energy consumption and operational costs. With growing environmental concerns and stricter emission standards, industries are focusing on solutions that minimize energy loss and carbon output. Advanced heat exchangers and cooling systems play a key role in achieving these goals, offering better thermal performance while supporting sustainable practices. The shift toward energy-efficient operations has led to increased investments in modernized equipment, further contributing to steady market growth.

Challenges and Opportunities

High initial investment and installation costs:One of the main challenges in the global heat transfer equipment market is the high upfront cost associated with the purchase, design, and installation of these systems. Many small and medium-sized enterprises find it difficult to allocate significant capital for such equipment, limiting adoption in certain regions. The complexity of installation and the need for specialized infrastructure can further increase total costs. Although the long-term energy savings are considerable, the initial expense often acts as a barrier for businesses with tight budgets, slowing down overall market penetration.

Maintenance challenges and risk of fouling or corrosion:The global heat transfer equipment market also faces issues related to maintenance and the potential for fouling or corrosion in equipment surfaces. Regular cleaning and inspection are essential to maintain optimal heat exchange efficiency, but this process can be costly and time-consuming. Accumulation of deposits and exposure to corrosive materials can reduce system lifespan and lead to performance deterioration. Addressing these maintenance challenges requires the use of protective coatings, efficient cleaning methods, and the implementation of monitoring systems to ensure consistent operation and lower the risk of unexpected breakdowns.

Opportunities

Adoption of advanced materials and technologies for enhanced thermal efficiency and sustainable energy applications: The global heat transfer equipment market has significant opportunities through the use of advanced materials and modern technologies designed to improve thermal performance and sustainability. The development of corrosion-resistant alloys, composite materials, and compact heat exchanger designs is helping industries achieve better heat transfer rates and reduce maintenance needs. Innovations such as nanotechnology-based coatings and smart monitoring systems allow for real-time performance analysis and improved energy management. These advancements not only increase operational efficiency but also support global efforts toward cleaner and more sustainable energy solutions, strengthening market potential for future growth.

Competitive Landscape & Strategic Insights

The global heat transfer equipment market is currently shaped by a combination of well-established international leaders and a growing number of regional players who are challenging traditional market positions. Companies such as Alfa Laval, Kelvion (GEA), SPX Corporation, IHI, SPX-Flow, DOOSAN, API, KNM, Funke, Xylem, Thermowave, Hisaka, Sondex A/S, SWEP, LARSEN & TOUBRO, Accessen, THT, Hitachi Zosen, LANPEC, Siping ViEX, Ormandy, and Lanzhou LS represent the most significant participants in the market, offering a wide range of technologies and services that cater to diverse industrial needs. These players have built their strengths through technological innovation, established distribution networks, and deep industry experience, which allow them to maintain strong positions in key regional and international markets.

Emerging competitors from regional markets are contributing to a more dynamic and competitive environment. These companies are leveraging cost-efficient manufacturing, local expertise, and tailored solutions to gain market share, particularly in areas where demand for energy-efficient and high-performance heat transfer solutions is increasing. The competitive landscape is expected to become more challenging as technological advancements continue to accelerate, creating opportunities for players who can innovate quickly and respond to shifting market requirements.

From a strategic perspective, companies are likely to focus on expanding their global footprints through partnerships, mergers, and acquisitions to strengthen capabilities and reach. Investments in research and development will play a pivotal role in creating products that are more energy-efficient, environmentally friendly, and adaptable to various industrial applications. Data-driven insights and predictive analytics will increasingly guide decision-making, allowing companies to optimize operations, anticipate market trends, and identify growth opportunities.

Looking ahead, companies that effectively combine technological innovation with strategic market positioning will be better prepared to navigate the evolving competitive environment. The future will favor players who can provide flexible solutions, maintain cost efficiency, and respond to industry demands quickly. Strategic collaborations and investment in digital technologies are likely to become critical differentiators, enabling companies to stay ahead in a market where competition is intensifying and global demand for advanced Heat Transfer Equipment continues to grow.

Market size is forecast to rise from USD 11.1 Billion in 2025 to over USD 15.4 Billion by 2032. Heat Transfer Equipment will maintain dominance but face growing competition from emerging formats.

The industry’s trajectory indicates that a clear focus on innovation, efficiency, and strategic expansion will define the success of key participants, shaping the global heat transfer equipment market over the next decade. Companies that align technological progress with market strategy will be positioned to capture emerging opportunities and sustain long-term growth in a landscape that is increasingly competitive and globally interconnected.

Report Coverage

This research report categorizes the global heat transfer equipment market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the global heat transfer equipment market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the global heat transfer equipment market.

Heat Transfer Equipment Market Key Segments:

By Type

Shell & Tube

Plate

Air Cooled

Other

By Application

Petrochemical

Electric Power & Metallurgy

Shipbuilding Industry

Mechanical Industry

Central Heating

Food Industry

Others

Key Global Heat Transfer Equipment Industry Players

Bangladesh Flavours and Fragrances Market Size, Share, Trends, 2033

Bangladesh Flavours and Fragrances market size is valued at USD 793.9 million in 2025 and is projected to reach USD 1,447.9 million in 2033, at a CAGR of 7.8% from 2026 to 2033

Bangladesh Flavours and Fragrances Market, Bangladesh Flavours and Fragrances Market Size, Bangladesh Flavours and Fragrances Market Share, Bangladesh Flavours and Fragrances Market Analysis, Bangladesh Flavours and Fragrances Market Growth, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market Research Report, Bangladesh Flavours and Fragrances Market Forecast, Bangladesh Flavours and Fragrances, Bangladesh Flavours and Fragrances Market Research, Bangladesh Flavours and Fragrances Industry, Bangladesh Flavours and Fragrances Industry Report, Bangladesh Flavours and Fragrances Market Data, Bangladesh Flavours and Fragrances Statistics, Bangladesh Flavours and Fragrances Market Statistics, Bangladesh Flavours and Fragrances Industry Trends, Bangladesh Flavours and Fragrances Market Report, Bangladesh Flavours and Fragrances Market Trends, Bangladesh Flavours and Fragrances Market News, Bangladesh Flavours and Fragrances Forecasts, Bangladesh Flavours and Fragrances Market Intelligence Report

Biocatalysis and Enzyme Biocatalysts Market Size, Share, Trends, 2033

Biocatalysis and Enzyme Biocatalysts market size is valued at USD 737.8 million in 2025 and is projected to reach USD 1,221.0 million in 2033, at a CAGR of 6.5% from 2026 to 2033.

Biocatalysis and Enzyme Biocatalysts Market, Biocatalysis and Enzyme Biocatalysts Market Size, Biocatalysis and Enzyme Biocatalysts Market Share, Biocatalysis and Enzyme Biocatalysts Market Analysis, Biocatalysis and Enzyme Biocatalysts Market Growth, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market Research Report, Biocatalysis and Enzyme Biocatalysts Market Forecast, Biocatalysis and Enzyme Biocatalysts, Biocatalysis and Enzyme Biocatalysts Market Research, Biocatalysis and Enzyme Biocatalysts Industry, Biocatalysis and Enzyme Biocatalysts Industry Report, Biocatalysis and Enzyme Biocatalysts Market Data, Biocatalysis and Enzyme Biocatalysts Statistics, Biocatalysis and Enzyme Biocatalysts Market Statistics, Biocatalysis and Enzyme Biocatalysts Industry Trends, Biocatalysis and Enzyme Biocatalysts Market Report, Biocatalysis and Enzyme Biocatalysts Market Trends, Biocatalysis and Enzyme Biocatalysts Market News, Biocatalysis and Enzyme Biocatalysts Forecasts, Biocatalysis and Enzyme Biocatalysts Market Intelligence Report

Malaysia Tyre Pyrolysis Products Market Size, Share, Trends, 2033

Malaysia Tyre Pyrolysis Products market size is valued at USD 205.9 million in 2025 and is projected to reach USD 421.8 million in 2033, at a CAGR of 9.3% from 2026 to 2033.

Malaysia Tyre Pyrolysis Products Market, Malaysia Tyre Pyrolysis Products Market Size, Malaysia Tyre Pyrolysis Products Market Share, Malaysia Tyre Pyrolysis Products Market Analysis, Malaysia Tyre Pyrolysis Products Market Growth, Malaysia Tyre Pyrolysis Products Market Trends, Malaysia Tyre Pyrolysis Products Market Research Report, Malaysia Tyre Pyrolysis Products Market Forecast, Malaysia Tyre Pyrolysis Products, Malaysia Tyre Pyrolysis Products Market Research, Malaysia Tyre Pyrolysis Products Industry, Malaysia Tyre Pyrolysis Products Industry Report, Malaysia Tyre Pyrolysis Products Market Data, Malaysia Tyre Pyrolysis Products Statistics, Malaysia Tyre Pyrolysis Products Market Statistics, Malaysia Tyre Pyrolysis Products Industry Trends, Malaysia Tyre Pyrolysis Products Market Report, Malaysia Tyre Pyrolysis Products Market Trends, Malaysia Tyre Pyrolysis Products Market News, Malaysia Tyre Pyrolysis Products Forecasts, Malaysia Tyre Pyrolysis Products Market Intelligence Report

Near Infrared (NIR) Analyzer Market Size, Share, Trends, 2033

Near Infrared (NIR) Analyzer market size is valued at USD 855.3 million in 2025 and is projected to reach USD 1,813.6 million in 2033, at a CAGR of 9.9% from 2026 to 2033.

Near Infrared (NIR) Analyzer Market, Near Infrared (NIR) Analyzer Market Size, Near Infrared (NIR) Analyzer Market Share, Near Infrared (NIR) Analyzer Market Analysis, Near Infrared (NIR) Analyzer Market Growth, Near Infrared (NIR) Analyzer Market Trends, Near Infrared (NIR) Analyzer Market Research Report, Near Infrared (NIR) Analyzer Market Forecast, Near Infrared (NIR) Analyzer, Near Infrared (NIR) Analyzer Market Research, Near Infrared (NIR) Analyzer Industry, Near Infrared (NIR) Analyzer Industry Report, Near Infrared (NIR) Analyzer Market Data, Near Infrared (NIR) Analyzer Statistics, Near Infrared (NIR) Analyzer Market Statistics, Near Infrared (NIR) Analyzer Industry Trends, Near Infrared (NIR) Analyzer Market Report, Near Infrared (NIR) Analyzer Market Trends, Near Infrared (NIR) Analyzer Market News, Near Infrared (NIR) Analyzer Forecasts, Near Infrared (NIR) Analyzer Market Intelligence Report