Fundus Cameras Market By Product (Mydriatic Fundus Cameras, Non-Mydriatic Fundus Cameras, Hybrid Fundus Cameras, ROP (Retinopathy of Prematurity), and Fundus Cameras), By Modality (Tabletop Fundus Cameras and Handheld Fundus Cameras), By Application (Diabetic Retinopathy Diagnosis, Glaucoma Diagnosis, Age-related Macular Degeneration Diagnosis, and Others) By End-User (Hospitals, Ophthalmology Clinics, Optometrist Offices, and Others), Industry Analysis, Size, Share, Growth, Trends, and Forecast, 2025-2032

Report ID

MSI-3470

Published

February 11, 2026

Pages

257 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

MARKET OVERVIEW

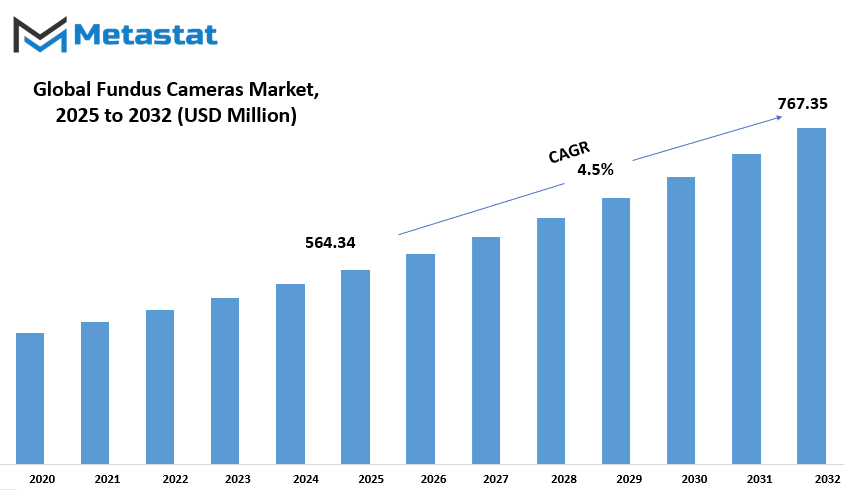

The Global Fundus Cameras market is estimated to reach $767.35 Million by 2032; growing at a CAGR of 4.5% from 2025 to 2032.

The Global Fundus Cameras market is very central to the ophthalmic community, which brings about advanced diagnostic techniques for eye care specialists worldwide. AI said it is one of the most important machines for taking high-resolution images of the retina for timely diagnosis and management of diabetic retinopathy, glaucoma, and age-related macular degeneration. The greater precision in ophthalmology as a criterion is attracting health organizations and technology developers, and research institutes looking to improve diagnostic accuracy and outcomes toward patient care.

One start promising area of improvement of the Global Fundus Cameras market lies in the advances in technology globally in the field of medical imaging. Artificial intelligence and machine learning algorithms are set to change the working of these devices in aiding the diagnosis of retinal diseases beyond recognition. The automatic image analysis that these devices offer will hasten the process for clinicians to detect abnormalities with increased accuracy and speed. Furthermore, it is apparent that the stronger urge for acceptance of telemedicine will assist in putting portable fundus cameras in the limelight for remote screening and consultation. Such a digital shift may dictate the end of the extended chasm existing between specialized eye care and the underprivileged areas with critical ophthalmic diagnostics.

Developmental upgrades in imaging sensors and optics will raise fundus photography to the next higher level. Non-mydriatic and ultra-widefield imaging technologies are bound to set standards of clarity and detail with minimum patient discomfort during clinical evaluations. Manufacturers will seek to improve workflow integration by expanding connectivity options between fundus cameras and electronic health records. These advancements will be instrumental in easing the management of patient data and facilitating broader ophthalmic examinations.

With the shifting atmosphere of health care towards patient-specific treatment strategies, fundus imaging could become a more significant player in prediction analytics. The analysis of retinal images for early signs of systemic diseases like cardiovascular conditions and neurological disorders could endow fundus cameras to become an indispensable tool beyond purely ophthalmic issues. Such convergence between ophthalmic imaging and widely embraced medical diagnostics could usher in a new way of handling preventive health care, which, in turn, may spur collaborative efforts between clinicians from different backgrounds.

Although the prospects appear bright, a number of determinants will shape the future of this market. The cost of purchasing and maintaining high-end fundus cameras remains a deterrent for smaller clinics and healthcare facilities in the developing regions. Thus, the manufacturers must contemplate less expensive means of production to make these devices more accessible.

GROWTH FACTORS

There is increasing demand for global fundus cameras market due to a rising incidence of disorders of the eye. Given the ever-ageing population, most cases of these eye disorders can now be detected using these devices as tools of proper diagnosis. Through the ability of machines to detect earlier retinal diseases, it may be diagnosed and allow earlier interventions for patients towards what can otherwise be a better outcome. Fundus cameras are high-resolution cameras used for imaging the retina and assisting in diagnosing various retinal diseases, including diabetic retinopathy, glaucoma, and age-related macular degeneration. Increased awareness of eye care and of the need for screening is furthering the growth of these markets.

They can, thus, detect them even before retinal diseases can be diagnosed, allowing the practitioner to intervene earlier for a better outcome for quite a number of the patients. Fundus cameras are high-resolution cameras that take pictures of the retina and help to diagnose the different retinal diseases, such as diabetic retinopathy, glaucoma, and age-related macular degeneration. Even increased awareness of eye health and advocating for routine screening have aided in adding fuels to the fire in market growth.

Moreover, the ongoing advancement in imaging technology has posteriorly contributed to the greater acceptance of a fundus camera in the clinical setup. Noninvasive diagnosis at high resolution and restoration allows imaging form-field of these cameras to detect the disease accurately. These are then also not forgotten while adding on features such as optical coherence tomography (OCT) and artificial intelligence-based image analysis. Thus, their utilities increase diagnostic precision and save valuable time spent on assessment in the near future, rendering eyecare more accessible and less time-consuming.

Though there are several advantages of these devices, some challenges may hinder growth for the industry. A primary factor in this respect is the affordability of fundus cameras. Most advanced imaging systems need heavy investments, which block the possibility of replication in resource-limited settings. Most of the smaller clinics and medical facilities cannot have these devices, which leads to restricted access to such an important diagnostic tool. Apart from that, skilled professionals are needed to handle these technologies and comprehend results derived from them. Proper training is required to achieve the right diagnosis, but there are not enough qualified personnel in many areas, which prevents healthcare providers from benefiting from these advanced imaging systems.

Nonetheless, it does provide a market opportunity integrating fundus cameras with telemedicine solutions. Remote diagnosis has increasingly become necessary, especially for patients that live in an area with more limited access to specialized eye care. While connecting these fundus cameras with telehealth platforms, ophthalmologist would be able to treat patients remotely through timely guidance and less burden on physical clinics. It would, therefore, result in a global expansion of eye care services, thereby reaching more people who tend to miss necessary screenings and treatment recommendations. As technology improves, the fundus cameras market is obviously rising with innovation and increased demand for more effective diagnostic solutions.

MARKET SEGMENTATION

By Product

Particularly, technical advancements in medical imaging in the area of ophthalmology would actually lead to the developing Global Fundus Cameras market. Fundus cameras are great in identifying severe eye diseases, which include diabetic retinopathy, glaucoma, and macular degeneration, from the clearest vision to total blindness. The conditions continue growing within populations globally; hence, the demand for such diagnostic tools increase. Fundus cameras provide a proper approach for healthcare professionals to capture the retina images, where planners and early detectors manage patients' treatment in reduced time. The market has undergone real improvement in imaging technology to making the devices easy and accessible for use.

The Global Fundus Cameras market product range consists of approximately $174.18 million in Mydriatic Fundus Cameras, Non-Mydriatic Fundus Cameras, Hybrid Fundus Cameras, and ROP (Retinopathy of Prematurity) Fundus Cameras. Each serves a unique purpose according to different clinical needs. Mydriatic Fundus Cameras need pupil dilation so that clearer images can be taken while Non-Mydriatic models take the advantage of taking pictures without dilation, thus making it a more comfortable procedure for the patient. Hybrid Fundus Cameras fuse both of these features together to be more versatile in a diagnostic situation. The ROP Fundus Cameras are meant particularly for monitoring premature infants who may develop retinal damage, so that they can be approached with timely intervention and improved outcomes of treatment.

AI-assisted analysis, high-resolution imaging, and portable devices for improved accessibility in remote areas have all been the result of technological advancements. Adoption of this technology is on the rise in hospitals, clinics, and research institutions as eyecare gets more focus. Governments and health organizations worldwide are taking the lead in planning initiatives for screening improvement hence promoting the market. Besides that, manufacturers are significantly pouring funds into R&D to discover economical yet efficient solutions.

Despite the developments, several challenges still exist; the costs of the advanced fundus cameras would limit the population of developing regions. Free training and expertise are required to use such a device, thus posing obstacles to a wider reach. The growth of interest in eye health and investment into the overall infrastructure for healthcare will improve the market situation in the future. The future of the Global Fundus Cameras market will be shaped by increasingly innovative technologies in imaging, ensuring better diagnostics accuracy and enabling earlier detection of diseases for patients all over the world.

By Modality

Global fundus cameras are essentially diagnostic equipment in the clinic for the ophthalmic field. It is used for advanced imaging techniques to identify and monitor eye diseases. Fundus cameras generally allow the capture of adequate images of the retina that can enable detection of conditions like diabetic retinopathy, glaucoma, and vision loss from macular degeneration. Being on the lookout for early detection of diseases and setting the patient right in terms of eye care has resulted in downhill pressure on demand for fundus cameras. With high-tech advancement, high-resolution imaging systems can enhance diagnostic accuracy and aim for better patient outcomes. The market, therefore, has two broad categories: tabletop fundus camera and handheld fundus camera.

Tabletop fundus cameras are widely used in hospitals, specialized eye clinics, and research institutions. These were chosen for thorough retinal examinations because of stable imaging with detail that assists in accurate diagnosis. AI integration and digital connectivity improve their capabilities, assist ophthalmologists with easy data storing, patient analysis, and data sharing. While tabletop models have advanced imaging features, generally they would be comparatively larger and permanently installed for dedicated space.

Handheld fundus cameras, on the other hand, provide more flexibility and convenience; hence, they are very effective during mobile clinics, telemedicine, and point-of-care diagnostics. They can be carried easily, thus allowing eye screening to be done in areas where there may not be easily viewed healthcare provisions. With these hand-held devices, medical practitioners can easily conduct quick yet efficient examinations without compromising quality in the images taken. Flipping the bulb is stealing in multi-specialty hospitals that focus on more and more expanded access to eye care.

This increased incidence of eye disorders, together with the increasing numbers of elderly people, created a huge need for effective diagnostic tools. Governments and healthcare organizations are now focusing on increased frequency and access to routine eye screenings, which in turn has reflected in more demand for fundus cameras. There have been continuous ongoing research and development efforts toward improving imaging technology that gains market growth.

Most advanced imaging systems would be costly for many healthcare institutions, but the trade-off is not that large as early diagnosis and improved patient care enjoyed by most patients would dwarf the initial investment. There will be fundus cameras with the new imaging technology innovations as more develop because they will be able to stay in the forefront of ophthalmology with respect to their application in early detection and effective management of retinal diseases.

By Application

In contemporary ophthalmology, Fundus cameras assume the immensely critical role of improving diagnosis and care of numerous eye conditions at an early stage. The cameras allow for photographic imaging of the retina in detail so that it could be diagnosed by a specialist to find diseases leading to blindness in case there is no treatment. As technology evolved, so has the need to have reliable and accurate diagnostic instruments in the eye care domain, which has been the reason for a burgeoning increase in this specific sector.

The other prominent factor propelling the market is the rising incidence of eye ailments like diabetic retinopathy, glaucoma, and age-related macular degeneration. It leads to blindness if not diagnosed early. In diabetic retinopathy, the blood vessels that supply the retina are damaged as a complication of diabetes. This condition requires high-resolution images obtained through fundus cameras for the physician to determine the extent of damage.

Glaucoma can also be diagnosed using fundus imaging, wherein damage is caused in the optic nerve because of increased intraocular pressure, making it possible for timely intervention. Age-related macular degeneration is one of the most common causes for vision loss due to detailed imaging away from just these spine major applications; it requires thorough imaging for diagnosis and monitoring and, of course, fundus cameras are also used to detect other retinal diseases.

By finding ways and means of adopting an advanced imaging technology, fundus cameras have also made improvement in the efficiency of the modality. Diagnostic precision improved as there was introduction of artificial intelligence and automated screening systems which facilitate faster and improved assessments. Digital fundus cameras are becoming a popular choice for healthcare providers due to better image quality as well as easy retrieval of patient records. The advantages are better disease detection as well as much-improved treatment planning. These increasingly popular portable and non-mydriatic fundus cameras have also made things even more comfortable, bringing eye examinations to the people in remote areas.

With the mounting trend of developing fundus cameras, barriers to market growth are also continuing to pose challenges. Advanced expensive imaging systems and limited accessibility across developing regions create an obstacle to market expansion. Nevertheless, the increasing research and initiatives from government to better eye care services will overcome these problems in the long term. Hence, the Global Fundus Cameras market will continue booming as the people's awareness increases on eye health and the cost of technology makes these devices more affordable. This ensures that as time goes by, eye care improves in every corner of the world.

By End-User

The rise in Global Fundus Cameras means that medical imaging is on the up and bettering diagnostic capabilities. Fundus cameras are the backbones of any ophthalmology department, for ultra-high-definition imaging of retina for premature diagnosis and monitoring of conditions such as diabetic retinopathy, glaucoma, and age-related macular degeneration. With the increase in eye diseases together with a steadily increasing geriatric population, the demand for fundus cameras has gotten even higher in other healthcare settings. Modern fundus cameras have now evolved as a result of technological advancements, and non-mydriatic imaging, high-resolution output, and AI-assisted analysis make these tools uncomplicated and easily accessible to the medical personnel.

For the purpose of end-users, the segmentation consists of hospitals, ophthalmology clinics, optometrist offices, and other healthcare facilities. The hospitals form a major share in the market since they have better infrastructure and advanced diagnostic equipment. These institutions serve a larger volume of patients who require specialized retinal imaging for complicated clinical cases. In comparison, ophthalmology clinics are dedicated mostly to treatments concerning the eye and extensively depend on fundus cameras for routine examinations and disease management.

Optometrist offices are now adopting fundus cameras with increasing alacrity, as optometrists employ more advanced imaging tools to render comprehensive eye care services. Various other healthcare practitioners, including academic research institutions and mobile eye care units, support the fundus camera market by using them for research studies and outreach programs that expand access to retinal imaging.

Technological advances have led to the development of handheld and smartphone-based fundus cameras to make retinal imaging available in remote and underprivileged areas. Such innovations are particularly helpful in telemedicine whereby specialists can diagnose and recommend treatment plans without the necessity of patients visiting a medical facility. The incorporation of artificial intelligence into fundus imaging further enhances the accuracy of the diagnoses, thus enabling rapid and precise identification of retinal pathology. High costs of operations and a highly skilled labor force required to operate these devices are some barriers to widespread acceptance. However, the market will rise as awareness improves and governments begin pumping funds into healthcare infrastructure. Fundus cameras are likely to be made even more efficient with ongoing research and development, enhancing their role further in modern ophthalmology.

Forecast Period

2025-2032

Market Size in 2025

$564.34 Million

Market Size by 2032

$767.35Million

Growth Rate from 2025 to 2032

4.5%

Base Year

2025

Regions Covered

North America, Europe, Asia-Pacific, South America, Middle East & Africa

REGIONAL ANALYSIS

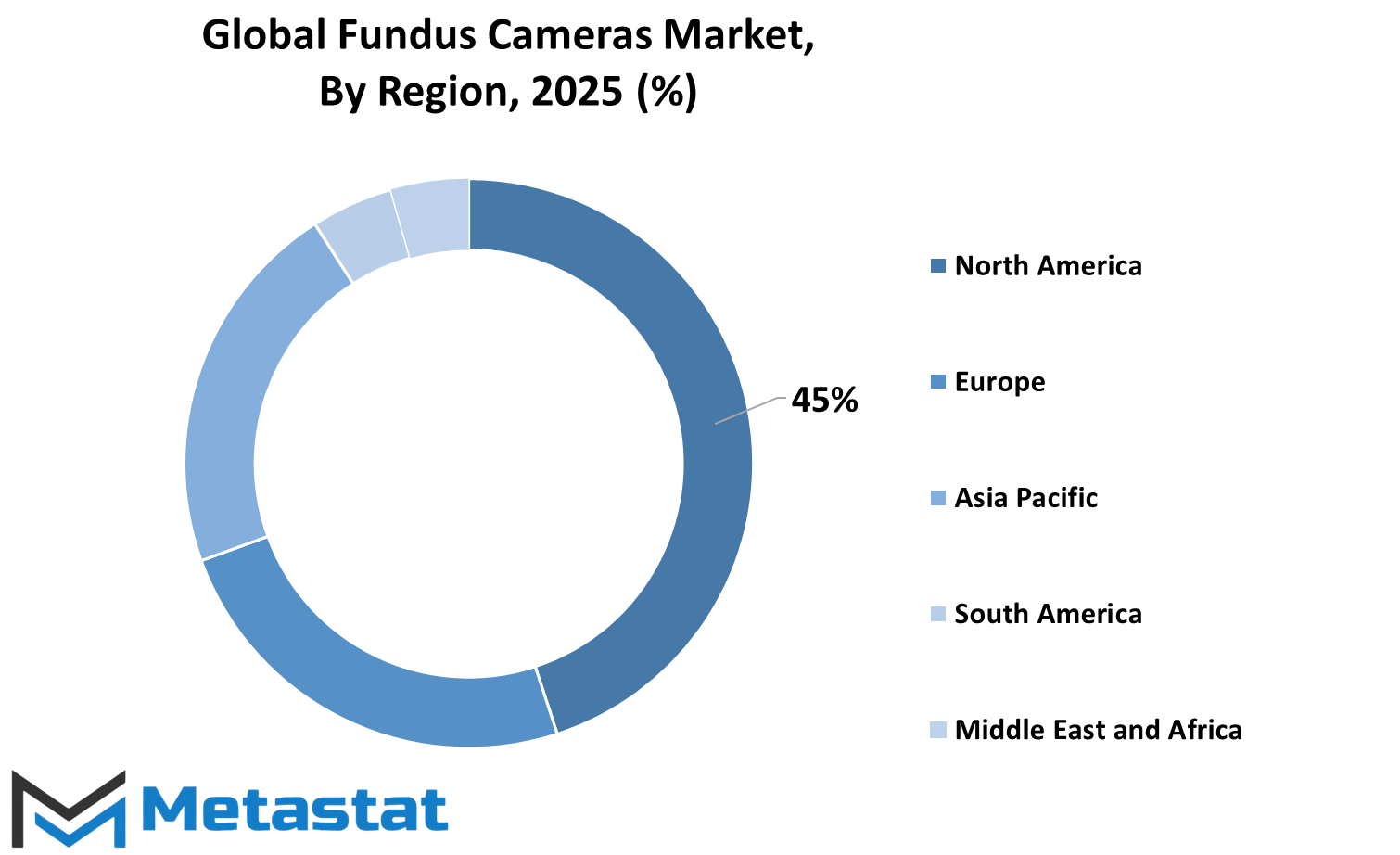

This global Fundus Cameras market has geographical segmentation which covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa. Within North America, there is segmentation for the three regions such as US, Canada, and Mexico. Major countries in Europe are the UK, Germany, France, and Italy, followed by all other countries under Rest of Europe. Major markets in Asia-Pacific are India, China, Japan, and South Korea. All other countries are classified under Rest of Asia-Pacific. South America has Brazil and Argentina and other countries listed as Rest of South America. The Middle East & Africa has a subdivision into GCC Countries, Egypt, and South Africa, with all others classified under Rest of the Middle East & Africa.

By segmentation of the market in these regions, it would have a more extensive and clearer grasp of the demand trends and growth opportunities available for different parts of the world. North America is likely to hold a considerable share because of its advanced network of healthcare delivery systems and early adoption of medical technology. Europe also has importance in the expansion of the market because it has an already developed medical sector.

The emerging demand in the Asia-Pacific region of rapid growth might be due to rising healthcare investments and increasing patients. Steady growth is seen in South America with Brazil and Argentina taking charge in the adoption of advanced medical imaging devices. Improvement in healthcare access and initiatives from the government in the region will increase demand for Fundus Cameras in the Middle East & Africa.

The conditions under which each of the regions will drive the market differ-from their economic conditions, healthcare policy, technological advancements, and the incidence of diseases related to the eye-influencing the demand for the market differently across the regions. The segmentation will thus also provide a strategic perspective to manufacturers and investors into knowing key markets and developing appropriate strategies.

COMPETITIVE PLAYERS

The Global Fundus Cameras Market is flourishing and this is largely as a result of the new advancements in medical imaging which are continually revolutionizing eye care. These very specialized apparatus serve as diagnostic tools and guides in monitoring various types of retinal disorders, such as diabetic retinopathy, macular degeneration, and glaucoma. Eye disorders are increasingly on the increase and the need for progressive diagnostic tools is increasingly becoming more urgent due to the growing aging population. Fundus cameras enable healthcare professionals to capture high quality images of retina which aids in the early detection and planning for treatments. This usage is beyond being specific to ophthalmology clinics alone but also-inclusive of healthcare facilities in general and telemedicine platforms, thus making eye care more widely available.

Technological advancements are the other factors that largely propelled the increasing use of fundus cameras. Imaging technologies have advanced from conventional modality using mydriatic cameras to non-mydriatic and ultra-wide-field images providing comfortable diagnostics for patient evaluation. Automation of disease detection has been realized in retinal imaging with the introduction of artificial intelligence to improve the efficiency of screening processes. These gave fundus cameras the potential of being increasingly useful for high coverage screening, even in remote and difficult-to-access contexts, where specialized care is lacking.

The leading companies worldwide in fundus cameras' innovations and their continuous production focus on significant improvements of these devices regarding their imaging capability and user-friendliness. Major institutions in the industry comprise Topcon Medical Systems Inc., Canon Inc., Carl Zeiss Meditec AG, NIDEK Co., Ltd., Kowa Company, Ltd., Optomed Plc, Optovue Incorporated, Epipole Ltd., Forus Health Pvt. Ltd., Volk Optical Inc., Revenio Group Corporation, and Shanghai New Eyes Medical Inc. These manufacturers focus on research and development to introduce advanced imaging solutions that enhance clinical efficiency. Their efforts have contributed to the widespread adoption of fundus cameras across hospitals, clinics, and research institutions.

Despite the high demand, various challenges such as high cost and the need for specialized knowledge have greatly marked their adoption in particular regions. The development of more affordable options in these devices continues to expand their footprints. Increased recognition by health care providers regarding benefits from early diagnosis through such devices will boost the use of fundus cameras in the future. With the ongoing technology improvements and increase awareness about eye health, the Global Fundus Cameras market is much likely to be at the forefront of the advancement of ophthalmic diagnostics and subsequently improvement of patient outcomes worldwide.

Former, on-going, and projected market analysis in terms of volume and value

Assessment of niche industry developments

Market share analysis

Key strategies of major players

Emerging segments and regional growth potential

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

Global Fundus Cameras market is valued at $ 564.34 million in 2025.

Global Fundus Cameras market is estimated to grow with a CAGR of 4.5% from 2025 to 2032.

Global Fundus Cameras market is estimated to reach $767.35 million by 2032.

Top players operating in the Fundus Cameras industry includes Topcon Medical Systems Inc., Canon Inc., Carl Zeiss Meditec AG, NIDEK Co., Ltd., Kowa Company, Ltd., and others.

Fluid Management Systems Market Size, Share, Trends, 2033

Fluid Management Systems market size is valued at USD 13.5 billion in 2025 and projected to reach USD 35.9 billion by 2033, growing at a CAGR of 13.0%.

Fluid Management Systems market, Fluid Management Systems Market Size, Fluid Management Systems Market Share, Fluid Management Systems Market Analysis, Fluid Management Systems Market Growth, Fluid Management Systems Market Trends, Fluid Management Systems Market Research Report, Fluid Management Systems Market Forecast, Fluid Management Systems, Fluid Management Systems Market Research, Fluid Management Systems Industry, Fluid Management Systems Industry Report, Fluid Management Systems Market Data, Fluid Management Systems Statistics, Fluid Management Systems Market Statistics, Fluid Management Systems Industry Trends, Fluid Management Systems Market Report, Fluid Management Systems Market Trends, Fluid Management Systems Market News, Fluid Management Systems Forecasts, Fluid Management Systems Market Intelligence Report, Fluid Management Systems market 2033, Fluid Management Systems market outlook, Fluid Management Systems market segmentation, Fluid Management Systems market drivers, Fluid Management Systems market restraints, Fluid Management Systems market opportunities, Fluid Management Systems market CAGR, Fluid Management Systems suppliers, Fluid Management Systems manufacturers, Fluid Management Systems market by region, North America Fluid Management Systems market, Asia Pacific Fluid Management Systems market, Europe Fluid Management Systems market, Fluid Management Systems market competitive landscape, Fluid Management Systems market key players, Fluid Management Systems Disposables and Consumables, Fluid Management Systems Arthroscopy market, Fluid Management Systems Urology and Nephrology market, Fluid Management Systems Hospitals market, Fluid Management Systems Dialysis Centers market.

Global Nanorobotics market size reached USD 8.3 billion in 2025 and is forecast to hit USD 15.5 billion by 2033 at a 8.2% CAGR. Segment and regional data.

Ga 68 DOTATOC market size is valued at USD 100.9 million in 2025 and projected to reach USD 235.9 million by 2033, growing at a CAGR of 11.2%.

Ga 68 DOTATOC market, Ga 68 DOTATOC Market Size, Ga 68 DOTATOC Market Share, Ga 68 DOTATOC Market Analysis, Ga 68 DOTATOC Market Growth, Ga 68 DOTATOC Market Trends, Ga 68 DOTATOC Market Research Report, Ga 68 DOTATOC Market Forecast, Ga 68 DOTATOC, Ga 68 DOTATOC Market Research, Ga 68 DOTATOC Industry, Ga 68 DOTATOC Industry Report, Ga 68 DOTATOC Market Data, Ga 68 DOTATOC Statistics, Ga 68 DOTATOC Market Statistics, Ga 68 DOTATOC Industry Trends, Ga 68 DOTATOC Market Report, Ga 68 DOTATOC Market Trends, Ga 68 DOTATOC Market News, Ga 68 DOTATOC Forecasts, Ga 68 DOTATOC Market Intelligence Report, Ga 68 DOTATOC Market Outlook, Ga 68 DOTATOC Market Segmentation, Ga 68 DOTATOC Market Drivers, Ga 68 DOTATOC Market Restraints, Ga 68 DOTATOC Market Opportunities, Ga 68 DOTATOC Market CAGR, Ga 68 DOTATOC Suppliers, Ga 68 DOTATOC Manufacturers, Ga 68 DOTATOC Market by Region, North America Ga 68 DOTATOC Market, Asia Pacific Ga 68 DOTATOC Market, Europe Ga 68 DOTATOC Market, Ga 68 DOTATOC Market Competitive Landscape, Ga 68 DOTATOC Market Key Players, Ga-68 DOTATOC Ready-to-Use Market, Ga-68 DOTATOC Radiolabeling Kits Market, Gastrointestinal Neuroendocrine Tumor Market, Pancreatic Neuroendocrine Tumor Market, Lung Neuroendocrine Tumor Market, Hospitals and Academic Medical Centers Market, Specialty Nuclear Medicine Centers Market, Diagnostic Imaging Centers Market, Radiopharmacies Market, Oncology Centers Market

Bone Graft Substitutes Market Size, Share, Trends, 2033

Bone Graft Substitutes market to hit $5,275.6M by 2033, growing from $1,004.1M in 2025 at a 6.0% CAGR. Explore top industry trends & insights.

Bone Graft Substitutes market, Bone Graft Substitutes Market Size, Bone Graft Substitutes Market Share, Bone Graft Substitutes Market Analysis, Bone Graft Substitutes Market Growth, Bone Graft Substitutes Market Trends, Bone Graft Substitutes Market Research Report, Bone Graft Substitutes Market Forecast, Bone Graft Substitutes, Bone Graft Substitutes Market Research, Bone Graft Substitutes Industry, Bone Graft Substitutes Industry Report, Bone Graft Substitutes Market Data, Bone Graft Substitutes Statistics, Bone Graft Substitutes Market Statistics, Bone Graft Substitutes Industry Trends, Bone Graft Substitutes Market Report, Bone Graft Substitutes Market Trends, Bone Graft Substitutes Market News, Bone Graft Substitutes Forecasts, Bone Graft Substitutes Market Intelligence Report, Bone Graft Substitutes Market 2033, Bone Graft Substitutes Market Outlook, Bone Graft Substitutes Market Segmentation, Bone Graft Substitutes Market Drivers, Bone Graft Substitutes Market Restraints, Bone Graft Substitutes Market Opportunities, Bone Graft Substitutes Market CAGR, Bone Graft Substitutes Suppliers, Bone Graft Substitutes Manufacturers, Bone Graft Substitutes Market by Region, North America Bone Graft Substitutes Market, Asia Pacific Bone Graft Substitutes Market, Europe Bone Graft Substitutes Market, Bone Graft Substitutes Market Competitive Landscape, Bone Graft Substitutes Market Key Players, Mineralized Bone Allografts Market, Demineralized Bone Matrix Market, Cellular Bone Matrices Market, Synthetic Bone Graft Substitutes Market, Bone Morphogenetic Protein-Based Grafts Market, Spinal Fusion Bone Graft Substitutes, Trauma and Long-Bone Repair Bone Graft Substitutes, Joint Reconstruction Bone Graft Substitutes, Dental Bone Grafting Market.