MARKET OVERVIEW

The Denmark and Sweden life science instrumentation market will evolve into a unique scenario defined by scientific accuracy and territorial technology advances. As a field based on biomedical research, clinical diagnostics, and analytical innovation, it will not only benefit the healthcare but also stretch its influence over various scientific disciplines. Both in Denmark and Sweden, where public spending on research will continue to hold firm, the instrumentation future will go beyond traditional frameworks. It will tilt towards integrating with artificial intelligence, microfluidics, and real-time data analytics to drive a transition from standalone systems to more intelligent, networked platforms.

The Denmark and Sweden life science instrumentation market will reshape the way research institutions, pharmaceutical firms, and diagnostic labs function. Advanced instrumentation that is designed to comply with local regulations will increasingly be optimized for reproducibility and minimization of experimental error, as part of a general focus on sustainability and responsible science. As concern for the environment continues to increase, manufacturers will be forced to rethink the design of instruments with fewer waste products and better energy efficiency. This change will not be sudden, but its orientation will be clear-cut tools will be lighter, intelligent, and more versatile for multi-purpose laboratories.

Denmark and Sweden are most likely to see a rise in academic-industry partnerships so that universities can become more involved in developing and certifying new equipment. Novel technologies, by means of these partnerships, will be tried not just in controlled settings but also under actual situations, leading to more pragmatic applications. The distinction between research and commercial application will fade, as life science tools start to impact not only laboratories but also personalized health monitoring and agricultural testing. Such broader applications will require new data privacy frameworks, tool standardization, and transboundary regulatory convergence.

As the years progress, the Denmark and Sweden life science instrumentation market will no longer concentrate on isolated performance measures such as speed or sensitivity. In its place, it will value integrative thinking how a single instrument contributes to an integrated workflow or aids a research hypothesis. As the requirements for multi-omics research and regenerative medicine change, so will instrumentation expectations. The instruments of tomorrow will not merely produce results but offer interpretive guidance, adapting to researchers with intuitive software interfaces and automatic maintenance schedules.

Global manufacturers will continue to be present, but local companies will take center stage by providing customization to match local lab conditions and user preferences. Specialized startups based in Denmark and Sweden will develop hybrid tools that will fulfill dual or even triple purposes. This trend will redefine innovation not radical reinvention, but incremental refinement that enhances usability and compatibility across multiple research environments.

So the Denmark and Sweden life science instrumentation market will extend well beyond its historical limits. It will design a future in which investigation is not simply performed but maximized, not simply dissected but comprehended, and not simply quantified but realized with precision and authority. This process will be a silent but stern revolution in the manner in which science engages with the instruments created to probe it.

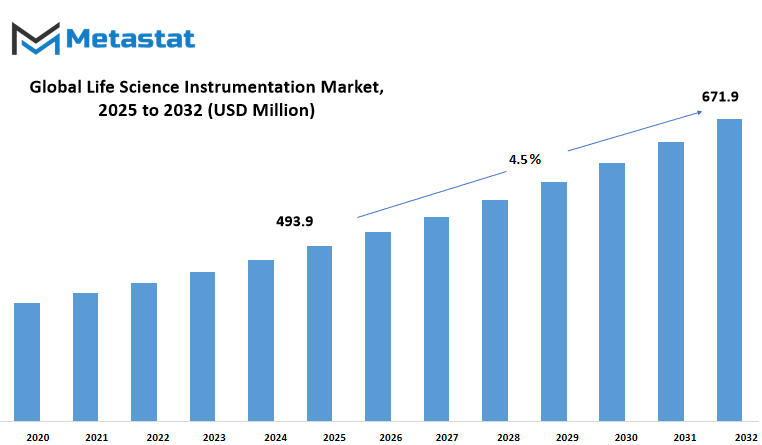

Denmark and Sweden life science instrumentation market is estimated to reach $671.9 Million by 2032; growing at a CAGR of 4.5% from 2025 to 2032.

GROWTH FACTORS

The Denmark and Sweden life science instrumentation market is evolving into an important driver of biomedical advances in Northern Europe. As healthcare demands shift and scientific interest becomes more concentrated, these nations are experiencing important innovation in the way laboratories and research centers function. One of the prime causes of this drive is the growing government support. As extra cash is injected into biomedical studies, there's more call for for pretty sophisticated gadgets able to deal with complicated checking out and offer short, accurate results. Scientists are actually higher positioned to pursue clinical questions that formerly regarded out of reach, and this trend is propelling the instrumentation market's common growth.

Another giant aspect is growing old. Both Denmark and Sweden have witnessed a steady increase inside the wide variety of older residents, which routinely puts extra call for for diagnosis solutions and medical research. Older citizens generally tend to need greater medical care, and to help facilitate on-time and correct treatment, hospitals and laboratories require reliable, updated gadget. This has resulted in increased deployment of analytical equipment in the research and diagnostic environments, opening up new growth opportunities throughout the market.

Nevertheless, problems exist. One significant problem is expensive high-technology equipment. While large hospitals and research facilities can afford to implement new systems, many smaller laboratories are unable to afford these types of devices. This disparity hinders broad application and accelerates progress, particularly in rural or lower-funded regions. Apart from financial barriers, businesses also encounter regulatory lag times. Cautious approval processes can delay product introductions and restrict how rapidly new tools find their way to the market. Such regulations, while critical for guaranteeing safety and efficacy, tend to complicate innovation progressing at top speed.

But opportunities persist. Probably the most encouraging avenue is personalized medicine. This emerging area calls for extremely particular information, and it's creating a premium on equipment that can provide nuanced, bespoke information. As this technique maintains to benefit popularity amongst healthcare companies, demand for accurate and bendy device have to increase. In addition, latest tendencies in molecular diagnostics are growing new opportunities. They allow the detection of illnesses at an in advance and more particular degree, finally increasing the cost of next-era system.

In this fast-moving world, the Denmark and Sweden life science instrumentation market, as described by Metastat Insight, is a mirror to the increasing ambitions and real-world difficulties of contemporary healthcare. With some obstacles still in place, the way is yet evident technology, policy, and patient need are converging to transform the future of regional biomedical research.

MARKET SEGMENTATION

By Region

The Denmark and Sweden life science instrumentation market remains a bright future as technological advancement and healthcare needs drive the frontier of innovation. Both nations here are setting themselves apart in building up the scientific and medical infrastructure. Denmark, worth $186.4 million, is notable for its organized approach to healthcare and research spending, while Sweden demonstrates consistent growth through public-private partnerships in medical technology.

The Denmark and Sweden life science instrumentation market here is defined by a common interest in life science applications that increase diagnostics, drug discovery, and patient monitoring. Throughout labs, research institutions, and pharmaceutical firms, there's an increasing requirement for accurate, efficient, and trustworthy instrumentation. These instruments are a key component of daily business enabling everything from standard testing to intricate molecular investigations. As more sophisticated diseases come under the spotlight and individualized treatments take center stage, the demand for more intelligent equipment will only escalate.

Both nations have government support and university-driven innovation, providing a solid base for new product creation. Startups and long-term players alike are also trying to simplify tools and automate them, evidence of an evolution toward streamlined workflows. Environmental and regulation standards are also driving what products thrive, an added layer of quality control and innovation pressure.

Despite problems inclusive of the rate of system and strict regulatory techniques, the continued rise in studies expenditure and biotech investment maintains the momentum intact. Digitalization is likewise a main contributor cloud-based technologies, information-sharing software program, and AI-aided systems are step by step becoming the norm, inducing greater productiveness and smarter decision-making throughout labs and scientific settings.

The Denmark and Sweden life science instrumentation market will stay on a trajectory of endured evolution, with long-time period outcomes throughout industries from healthcare to environmental testing. This consistent but directed motion will hold the area as a considerable force in shaping the global future of lifestyles sciences. The destiny will display us how properly they've performed of their enterprise.

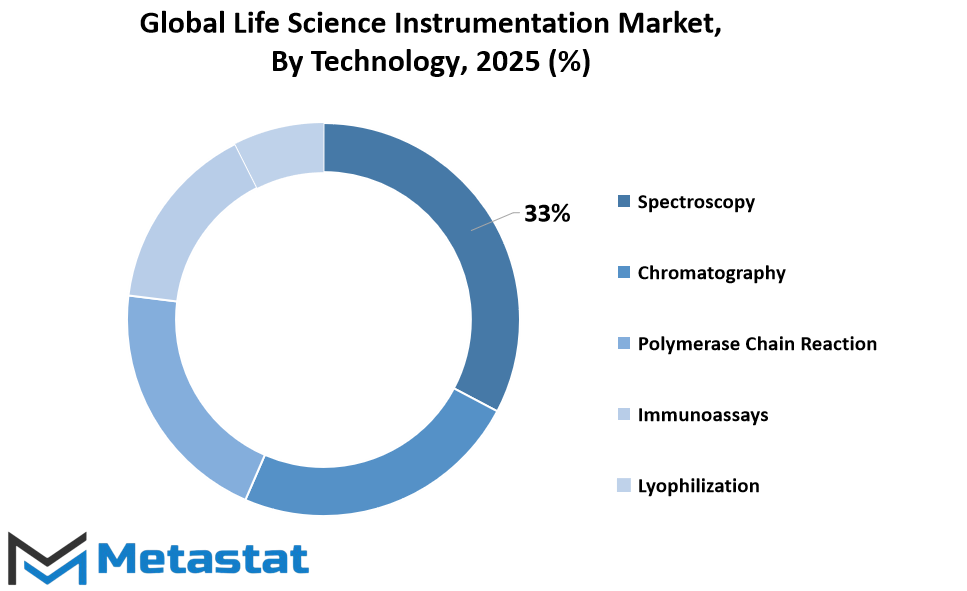

By Technology

The Denmark and Sweden life science instrumentation market is experiencing significant adjustments described by innovation and accelerated call for within the fitness and research industries. With high emphasis on accuracy and precision, this marketplace continues to play a important function in fostering scientific and scientific improvements inside the vicinity. What differentiates this marketplace is its increasing reliance on era which can supply outcomes in much less time and with expanded reality. As public and private sectors hold to make investments extra in healthcare and biotech research, the need for properly-satisfactory contraptions maintains to increase.

On the basis of technology, the market is segmented into Spectroscopy, Chromatography, Polymerase Chain Reaction, Immunoassays, Lyophilization, Liquid Handling Systems, Clinical Chemistry Analyzers, Microscopy, Flow Cytometry, and others. Each of these technology has a unique benefit to provide laboratories and studies establishments. For instance, Chromatography and Spectroscopy are used drastically for separating and figuring out complicated mixtures of compounds, while PCR and Immunoassays are at the middle of diagnostics in addition to genetic studies. Equipment including Clinical Chemistry Analyzers and Liquid Handling Systems aid in routine trying out, ensuring that paintings inside the laboratory is extra effective. On the alternative hand, Microscopy and Flow Cytometry facilitate the examine of particles and cells with excessive element, critical in instructional and scientific investigations.

In Sweden and Denmark, the dominance of pharmaceutical companies, research establishments, and healthcare infrastructure keeps to offer impetus for increase. Government rules that desire the improvement of life technological know-how innovation also aid local demand in those international locations, that have made manufacturers. Though the above-mentioned technologies will continue to be at the forefront, the Denmark and Sweden life science instrumentation market can expect greater automation and digital adoption in future years to streamline workflows and minimize errors.

The Denmark and Sweden life science instrumentation market from Metastat Insight provides an in-depth view of how these instruments are redefining the future of diagnostics and research. Strong regional backing, growing use in clinical labs, and ongoing improvements in intelligent instruments drive the market to continue gaining traction in the broader European market.

By Application

The Denmark and Sweden life science instrumentation market - By Application the market is further segmented into Research Applications, Clinical & Diagnostics Applications, Other Applications. These segments address the functional application of instruments that continue to influence how scientific advancement is made in both countries. Research applications will probably experience steady demand, particularly as institutions private and public seek to improve their knowledge of biological systems. Universities, biotechnology companies, and pharmaceutical companies are investing in accuracy and speed-improving tools in laboratory settings, which in turn underlies wider innovation.

Diagnostics and clinical packages will stay vital seeing that each Denmark and Sweden have a sturdy cognizance on public fitness. With getting older populations and a excessive priority on detecting sickness at an early degree, the want for classy diagnostic technologies should growth. These gadgets no longer simplest find usage in hospitals but also in devoted trying out and tracking labs, allowing medical doctors to make more timely and correct decisions. This utility section allows extra personalized treatment, something both international locations have increasingly more moved toward of their healthcare guidelines.

Other makes use of, at the same time as less particular, are although large. They encompass a large kind of industry-related applications, ranging from environmental checking out to agricultural studies. These markets won't be as distinguished as medical or educational research, yet they contribute to the general cost of the instrumentation marketplace through filling local needs that promote sustainability and safety.

Combined, these segments indicate the ways in which the Denmark and Sweden life science instrumentation market is formed by functional demand in industries that depend on precision and reliability. The expansion of each use will be based on national objectives, international trends in medicine and research, and the rate at which new technologies are embraced as a part of daily routines.

By End-User

The Denmark and Sweden life science instrumentation market shows how clinical equipment continue to form studies and healthcare effects across various sectors. When searching at this marketplace by way of give up-consumer, it turns into clear how diverse its attain is spanning from academic environments to pharmaceutical production, diagnostic services, and different specialized regions. Each of these segments plays a selected function in using call for high-precision units that support obligations ranging from disorder detection to drug development.

Research institutes stand as one of the primary users of existence technological know-how instruments. These facilities depend on detailed evaluation and constant accuracy to explore biological questions and test scientific hypotheses. The gear they use must guide the entirety from primary lab experiments to superior genetic studies. As technology becomes greater refined, researchers in Denmark and Sweden will maintain integrating more recent systems into their workflows, aiming for greater green and reproducible results.

Pharmaceutical and biotechnology businesses are some other predominant phase. These groups are under constant strain to innovate, whether with the aid of growing new remedies or enhancing current ones. Precision, consistency, and reliability are non-negotiable on this space, and the want for dependable existence technology instrumentation will continue to be a key factor of their potential to fulfill regulatory standards and supply results. The Danish and Swedish biotech sectors, both active in international collaborations, will preserve to put money into higher gear that accelerate discovery without sacrificing pleasant.

Diagnostic laboratories also use a large variety of units in daily operations. These labs are critical for identifying illnesses fast and as it should be. Their call for is shaped not best via the rise of chronic conditions but also via the want for quicker turnaround instances and extra complete trying out abilties. Whether processing blood samples or reading molecular information, those labs rely upon technology that could keep up with growing healthcare expectations.

The very last class others consists of a combination of smaller establishments, non-public labs, and public fitness companies. While now not as huge in marketplace share, these users make contributions to typical demand by filling area of interest wishes, frequently in personalized medicinal drug, agricultural trying out, or meals protection research. Their attention can be greater specialized, but their reliance on lifestyles science instrumentation remains strong.

Overall, the Denmark and Sweden life science instrumentation market by means of give up-user displays a structure that balances innovation, application, and precision. From research desks to medical labs, the usage of superior tools will hold shaping the way science affects lives, with each region contributing in its very own vital manner.

|

Forecast Period |

2025-2032 |

|

Market Size in 2025 |

$493.9 million |

|

Market Size by 2032 |

$671.9 Million |

|

Growth Rate from 2025 to 2032 |

4.5% |

|

Base Year |

2024 |

|

Regions Covered |

North America, Europe, Asia-Pacific, South America, Middle East & Africa |

REGIONAL ANALYSIS

The Denmark and Sweden life science instrumentation market, as offered by Metastat Insight, exists as a part of a wider global context defined by regional trends and innovations. Based as it is in Northern Europe, comprehending this market in its entirety means going beyond boundaries to observe how various geographical areas shape and add to the general movement of life science instrumentation.

Internationally, this industry is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Each of them presents specific strengths and weaknesses for the sector. North America, for instance, is further subdivided into the U.S., Canada, and Mexico. This region, especially the United States, is characterized by aggressive investment in healthcare research and technology, creating a stable platform for life science tools innovation and product development. Canada and Mexico also exhibit increasing interest in biotechnology and diagnostics, which is responsible for consistent growth.

In Europe, the life science instrumentation market comprises the UK, Germany, France, Italy, and the Rest of Europe. Germany and the UK have been leaders in research and lab technologies. This is followed by France and Italy with growing focus on drug developments and academic study. The combined pressure of these countries, combined with continuous cooperation and policies to foster innovation, provides a favorable platform for scientific instruments throughout the continent.

Asia-Pacific is another significant sector, comprising India, China, Japan, South Korea, and the Rest of Asia-Pacific. Having significant populations and growing healthcare systems, China and India are fast becoming crucial contributors. Japan and South Korea, with their areas of focus on precision and technology advancement, contribute more value to the industry. Their concentration on automation and medical diagnostic testing is particularly crucial in advancing the frontiers of lab efficiency and precision.

In South America, Brazil and Argentina are notable, together with the Rest of South America. Historically, less prominent in this area, they are now spending more on current laboratory equipment and covering biotechnology-based industries. This incremental development is assisting in enhancing the availability of life science instrumentation within the region.

Finally, the Middle East & Africa region consists of GCC Countries, Egypt, South Africa, and Rest of the Middle East & Africa. These regions are now starting to demonstrate more interest in scientific research and medical infrastructure. The availability of academic centers and the introduction of healthcare reforms have begun to unveil prospects for firms that provide high-quality instrumentation tools.

Together, Denmark and Sweden represent a focused and strategic part of the European life science instrumentation market, but their engagement with trends throughout these regions is important in shaping future directions. How innovation is exchanged, and how demand differs from region to region, will continue to dictate how companies are positioned and address increasing scientific and clinical demands.

COMPETITIVE PLAYERS

The Denmark and Sweden life science instrumentation market, by Metastat Insight, provides a clear image of the manner in which scientific technology and tools continue to influence healthcare, research, and diagnosis in the Nordic region. Both nations have a solid science and innovation base, supported by academic success, public health initiatives, and government support. All these result in the region being a hub for innovation in life science instrumentation, particularly in diagnostics, molecular biology, and clinical use.

Businesses are adapting to meet the increasing need for precise and efficient testing tools in research and clinical environments. Hospitals and labs require apparatus that provides quick, trustworthy results while ensuring high levels of safety. That is where devices like spectrometers, chromatographs, and PCR machines become important. They are not mere data-collecting tools anymore they are at the heart of disease research and treatment. The heightened sense of awareness for early diagnosis and individualized medicine is also driving the demand for more advanced instrumentation.

At the forefront are firms such as Agilent Technologies, Inc., Becton, Dickinson and Company (BD), Thermo Fisher Scientific Inc., Bruker Corporation, Danaher Corporation, Eppendorf AG, GE Healthcare, Hitachi, Ltd., Horiba, Ltd., Merck KGaA, and Oxford Instruments plc. These are not only suppliers but also innovation partners to numerous institutions in Denmark and Sweden. What they do underpins routine diagnostics through to pioneering achievements in genomics and cell biology.

Sustainability is another factor that is determining choices in this arena. Institutions are now paying more attention to energy consumption, waste, and lifecycle cost while investing in laboratory equipment. To meet this challenge, manufacturers are launching systems with reduced energy usage, more intelligent calibration, and extended life in operation. This not only saves the environment but also assists labs in saving money in the long term.

As digital transformation reaches all areas of science and medicine, the merging of software with hardware is gaining significance. Equipment is now being called upon to seamlessly integrate with lab management software and cloud storage, allowing data to be readily accessed and shared. This is altering the way labs function on a daily basis, enabling professionals to spend more time analyzing and less time recording by hand.

In Denmark and Sweden life science instrumentation market is influenced by a very special blend of high-quality research culture, need for healthcare efficiency, and common vision for innovation. As technologies get better and applications increase, the market will continue to evolve in response to new scientific and medical requirements.

Denmark and Sweden Life Science Instrumentation Market Key Segments:

By Region

- Denmark

- Sweden

By Technology

- Spectroscopy

- Chromatography

- Polymerase Chain Reaction

- Immunoassays

- Lyophilization

- Liquid Handling Systems

- Clinical Chemistry Analyzers

- Microscopy

- Flow Cytometry

- Other

By Application

- Research Applications

- Clinical & Diagnostics Applications

- Other Applications

By End-User

- Research Institutes

- Pharmaceutical & Biotechnology Companies

- Diagnostic Laboratories

- Others

Key Denmark and Sweden Life Science Instrumentation Industry Players

- Agilent Technologies, Inc.

- Becton, Dickinson and Company (BD)

- Thermo Fisher Scientific Inc.

- Bruker Corporation

- Danaher Corporation

- Eppendorf AG

- GE Healthcare

- Hitachi, Ltd.

- Horiba, Ltd.

- Merck KGaA

- Oxford Instruments plc

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential

US: +1 3023308252

US: +1 3023308252