MARKET OVERVIEW

The Global Electronic Warfare market will soon see new heights as new innovation and technologies take over how modern defense strategies are shaped. The major threats are the usual like costs or integration issues; yet, AI, cyber warfare technologies, and autonomous defense systems adoption increases innovation even further.

There is much technological evolution attached to the global electronic warfare market that will be aligned strategically for defense initiatives to mold capabilities into present-day militaries. Countries will continue to invest heavily in electronic warfare (EW) systems in defense and offensive strategies as geopolitical issues continue to sway global policy on security. Within this defense market, electronic warfare is a critical part of warfare, including cyber operations, intelligence collection, and advanced threat detection mechanisms. With adversaries always refining and countering their electronic attack strategies, the demand for superior EW capacities will be continuous.

These comprise technologies that keep signals-disrupting, jamming, decoying, or incapacitating enemy communications, intelligence, and radar systems. This has considerably changed the courses of battle fought by most countries making defense countermeasures indispensable. The Global Electronic Warfare market will significantly contribute toward improved situational awareness, electronic support measures, and cyber resilience. Future developments may integrate artificial intelligence, machine learning, and autonomous systems for action programming to enable high adaptability in these solutions for electronic warfare. The use of AI will make decisions faster and lessen the extent of human involvement in threat response.

However, the future would also see the growing usage of space-based electronic warfare as countries increasingly consider satellite communication and navigation security. These assets will be vital in conducting military operations with great potential for disruption through adversarial EW attacks. Innovative space-based electronic countermeasures will be deployed to safeguard such assets from possible attack in order to ensure continuous conduct of intelligence, surveillance, and reconnaissance operations. Furthermore, battlefield space manoeuvrability is likely to enhance more space combat capabilities within the Global Electronic Warfare market, thus making it even much more critical within the defense industry.

Cyber and electronic warfare will likely increasingly merge with each other, increasingly blurring delineating the boundary between conflict with conventional military means and a digitally engaged military conflict. The operations of cyber-electronic warfare will include precise targeting of vital enemy infrastructure while protecting the home network from advanced cyber threats. More operational flexibility is afforded by making software-defined radio (SDR) and cognitive electronic warfare integration so that forces can rapidly reconfigure their electronic attack and defense systems as threats materialize.

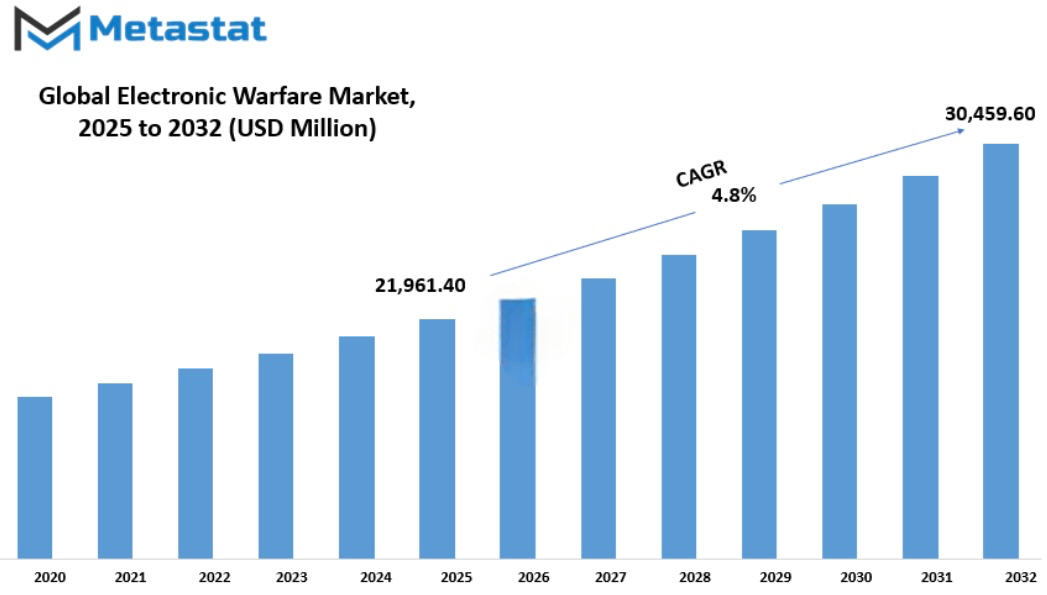

Global Electronic Warfare market is estimated to reach $30,459.60 Million by 2032; growing at a CAGR of 4.8% from 2025 to 2032.

GROWTH FACTORS

The Global Electronic Warfare market is assuming great importance on account of progressing changes in modern conflict and innovations in defense strategies. Electronic warfare is quickly becoming a necessary aspect of ensuring the national defense of every country as it focuses much on fortifying military capabilities. Geopolitical tensions in countries investing heavily in defense modernization have driven the market. Governments of numerous states have increased substantially in their budgets regarding the augmentation of electronic warfare systems. Cost cuts were applied, and the performance standards became aberrant very quickly as unprecedented changes occurred in the defense landscape. The operational area of the dishant work will also be widened with the addition of artificial intelligence and cyber warfare technologies, which will improve electronic warfare operations by quick decision-making, automated threat detection, and better situation awareness.

The market is increasingly becoming important because of growing challenges regarding modern warfare and advanced defense strategies. However, the challenges are challenging the market for wide adoption. The most significant barrier is the high cost attached to developing and procuring electronic warfare systems. Countries such as emerging economies are particularly finding it hard to invest in these technologies due to financial constraints. Advanced as well as requiring a hefty investment in research, development, and deployment, these systems often make it tough for some countries to align their capabilities with those of leading defense players. Further complicating the matter is the fact that many electronic warfare systems are quite new and cannot be easily integrated into existing defense systems. Such infrastructures contain reliant legacy systems, which were not planned to cater to modern electronic warfare solutions. This causes quite a lot of problems in compatibilities, leads to deployment delays, and costs extra for modifications and upgrades.

There are, however, areas that may present huge opportunities for expansion and innovation within the market. This is one of those trends speeding up the market, the increasing demand for electronic warfare solutions on unmanned systems and autonomous defense platforms. Since some of the military operational burdens are transferred to the electric warfare technologies being imperative for effectiveness and security, their automation is not enough. Much-needed solutions to that include real-time detection, jamming, and countering of threats, ideally when unmanned systems can also be made resilient against cyber and electronic attacks. Moreover, extending electronic warfare capabilities into both space and cyber domains indicates expansive development possibilities as well. As military strategies are being adapted by countries, they are now looking to secure their assets in space and cyberspace, leading to elevated investments in electronic warfare technologies adapted for those domains.

The Global Electronic Warfare market will soon see new heights as new innovation and technologies take over how modern defense strategies are shaped. The major threats are the usual like costs or integration issues; yet, AI, cyber warfare technologies, and autonomous defense systems adoption increases innovation even further.

MARKET SEGMENTATION

The Global Electronic Warfare market integrates advanced technologies to enhance military capabilities in various domains, thereby influencing the modern defense strategies. The complexity of global security threats around the world has prompted most nations towards making serious strides in developing electronic warfare systems for the strengthening of their defense mechanisms. These systems provide critical support for surveillance, communication interception, and countermeasure operations so that military forces can operate in environments that are being contested. With mounting geopolitical tensions and the need for increased battlefield awareness, the market is expanding rapidly.

Electronic warfare includes technical interference, jamming, and operation control with respect to enemy communications, radar signals, and all other electronic systems. The amplitude of demand for such technologies has seen an upswing because of modern warfare's focus on information superiority. Global military operations are now employing advanced electronic warfare solutions to protect their communication networks while neutralizing any possible adversary threats. AI and machine learning integration in these systems will further streamline the effectiveness of these systems in decision-making and real-time threat detection. The considerable budget allocation for research and development by governments and defense agencies will encourage more innovation and the rollout of next-generation warfare capabilities.

The platform segment of the Global Electronic Warfare market is classified into Airborne, Ground, Naval, and Space systems, each serving a different purpose. Airborne electronic warfare is the major segment valued at $9,106.52 million, whereas there is a considerable emphasis on the use of aircraft in reconnaissance, electronic attack, and signal jamming operations. Ground systems are vital for tactical operations in the areas of secure communications and countermeasures against adversarial electronic threats. Naval electronic warfare capabilities are focused on protection against radar detection and missile threats to warships, while space-based assets further establish intelligence gathering and strategic communications.

Some of the instances are the expectation of electronic warfare solutions to counter cyber threats and electronic warfare attacks, increasing reliance on digital and cyber technologies, and working alongside technology enterprises to develop highly sophisticated electronic warfare solutions adaptable to the evolution of threats. The emergence of autonomous systems and unmanned platforms has directed its fair share in the market dynamics, with more traction gained on electronic warfare solutions that maximize operational ability.

The challenges facing the market, such as high development costs and complicated integration of electronic warfare capabilities with existing defense systems, will still remain. However, continuing advancements in technology and defense spending increases from major economies suggest and confirm that the sector is set to continue expanding.

By Product

The Global Electronic Warfare market is on an advancing horizon as countries build on their defense capabilities. Electronic warfare is a central theme in contemporary military tactics that give forces the ability to disrupt their enemies' communications, detect threats, and protect their own systems from hostile interference. Warfare has introduced a massive disparity in technological sophistication; hence electronic systems are paramount to national security. In the face of increasing cyber threats, electronic warfare has diversified into a much broader spectrum of operations such as jamming of enemy signals, intercepting communications, and deploying countermeasures to eliminate possible threats. With major defense agencies across the globe setting aside huge budgetary allocations for capability enhancement, there has been intensified demand for advanced electronic warfare solutions.

Based on the type, equipment and operational support are the two segments of the market. The equipment segment includes radar jammers, countermeasures, communication interceptors, and electronic support measures, which assist in surveillance and threat assessment. Operation Support: Is more related to the application of electronic warfare technologies in the strategy domain, including training, mission planning, system integration, and technical assistance for the effective coordination of electronic warfare components. The two are vital for contemporary defense strategy to further improve situational awareness and timely response capability during high-risk situations.

There are various drivers driving the growth of this market. Increased tension in international relations among various countries causes several fightings, and therefore defense expenditure is set to rise, with the governments investing in new technologies in electronic warfare systems. Apart from that, rapid advancements in artificial intelligence and machine learning have contributed this new dimension of creating highly efficient and precise, and adaptive electronic warfare systems. Further developments in unmanned aerial vehicles and satellite networks for warfare have also set a very high demand for viable electronic defense mechanisms.

The industry has also some issues ahead in its evolution. High cost with regard to research and development, and challenges for the integration of new systems into the contemporary military infrastructure, are the significant challenges.The other challenge is continual cyber threat to electronic warfare systems, which calls for incessant innovation to stay ahead through counter attacking any possible threats. Governments and defense organizations must collaborate closely with technology providers to provide safe and efficient solutions that can withstand evolving challenges.

By Technology

Global Electronic Warfare is at the forefront of developing advanced solutions that march with the future of defense technology. The improvement of defense forces, for any nation, makes electronic warfare an indispensable portion of defense strategy. The need for advanced protection, surveillance, and countermeasure systems to help armed forces detect, disrupt, and neutralize will drive this market. Advances in technology continue to spark the need for extremely sophisticated electronic warfare systems, thus triggering ample investment in research and development activities in many countries.

Electronic warfare covers a wide range of technologies, which enhance military operations. The market is further classified according to technology into segments, such as antennas, anti-jam electronic protection systems, directed energy weapons, IR missile warning systems, and other protection systems. These technologies will play important roles in the solutions intended for data security and communications; jamming enemy radars and sensors; as well as intelligence gathering in near real-time by military forces.

Communication channels would operate through antennas, being the basic enabling components for communicating. Anti-jam electronic protection systems are used to minimize interference and assure mission accomplishment for forces. Directed energy weapons essentially allow targeting with high precision, thus, disarming the enemy threat with the least collateral damage. IR missile warning systems improve situational awareness by identifying incoming missile threats and taking appropriate actions, thus, enhancing its defense mechanisms.

Consequently, the increased dependency and reliance on electronic warfare electronic solutions shall potently drive the investment stakes in the global electronic warfare market. To cut edge the collaboration between the governmental and defense establishments and private organizations is being undertaken in research to churn out newer technologies capable of ensuring a far-reaching strategic advantage in conflict scenarios. Development studies would also include re-evaluating the fundamental efficiencies of each electronic warfare system while ensuring that new threats would be considered. Inclusion of artificial intelligence and machine learning also plays a vital role in efficiency enhancement of threat detection and response system. It is expected that these additions will further fortify defense systems.

Even if there are advantages, much has been put on hold in the present-day electronic warfare market by costs of heavy investments, very complex regulatory requirements for the market, and continuing vigil to stay ahead of ever-changing threats. However, with the ever-advancing technology, these challenges are being solved either by innovation or strategic collaborations. Heightened levels of geopolitical tension and demands for better defense mechanisms are all factors likely to witness subsequent growth in the market. Thanks to further advancements and the constant introduction of new technologies, electronic warfare is asserted to future advance global defense strategies.

By System Type

Such developments in the Global Electronic Warfare market are quite dynamic with nations and defense agencies gearing towards capacity building for modern wars. Indeed, Electronic warfare is the strategic use of the electromagnetism for threat detection disruption and protection against those threats. Coordination and operation of military missions will have increasing technological requirements, and thus, demand for advanced electronic warfare systems for operational superiority on the battlefield will increase. The market is structured into three categories according to system type: Electronic Support Measures (ESM), Electronic Attack (EA), and Electronic Protection (EP)-each one of them crucial in defense strategies.

ESM provides intelligence through the detection, identification, and analysis of enemy communications, radar, and other electronic signals as input to military operations. These Systems give up to-the-minute situational awareness of military forces in relation to real-time threat data and provide the ability to intercept and decode information useful for planning and decision-making. Therefore, such systems enable a military force to understand enemy moves and capabilities and thereby maintain a tactical advantage.

Electronic Attack (EA) disrupts, degrades, or neutralizes enemy communication systems and radar systems. Jamming, deception, and other countermeasures toward defeating hostile electronic capabilities are included in this segment. EA has changed the definition of modern warfare because it interferes greatly with enemies denying the ability to conduct coordinated attacks as well as maintain surveillance of their targets. The rapid advancement of cyber war and electronic jamming technology has delivered the effectiveness of EA systems into a much higher level for military application.

Electronic Protection (EP) makes it possible for a friendly electronic system to be immune to a hostile interference. Increasing dangers of electronic attacks brought its significant importance in producing solid defensive mechanisms typically for military hardware protection from jamming, cyber threats, and other episodes. A summary of EP technologies is increasing integrity of signals, securing and improving encryption techniques, as well as establishing counter-countermeasures for operational efficiency. As with electronic threats, developing even stronger protective systems would have to continue as a priority for all defense forces worldwide.

These substantial investments in research and development go a long way into improving such systems. Of course, within the Global Electronic Warfare market, all this holds true. The various forms of conflict that have emerged, plus the rapid advances in technology, have compelled countries to intensify the incorporation of artificial intelligence adopting machine learning and cybersecurity levels in their electronic warfare capabilities. Further integration of electronic systems emphasizes roles played by ESM, EA, and EP in national defense strategies and the advantage scored by reliance on them.

|

Forecast Period

|

2025-2032

|

|

Market Size in 2025

|

$21,961.40 million

|

|

Market Size by 2032

|

$30,459.60 Million

|

|

Growth Rate from 2025 to 2032

|

4.8%

|

|

Base Year

|

2025

|

|

Regions Covered

|

North America, Europe, Asia-Pacific, South America, Middle East & Africa

|

REGIONAL ANALYSIS

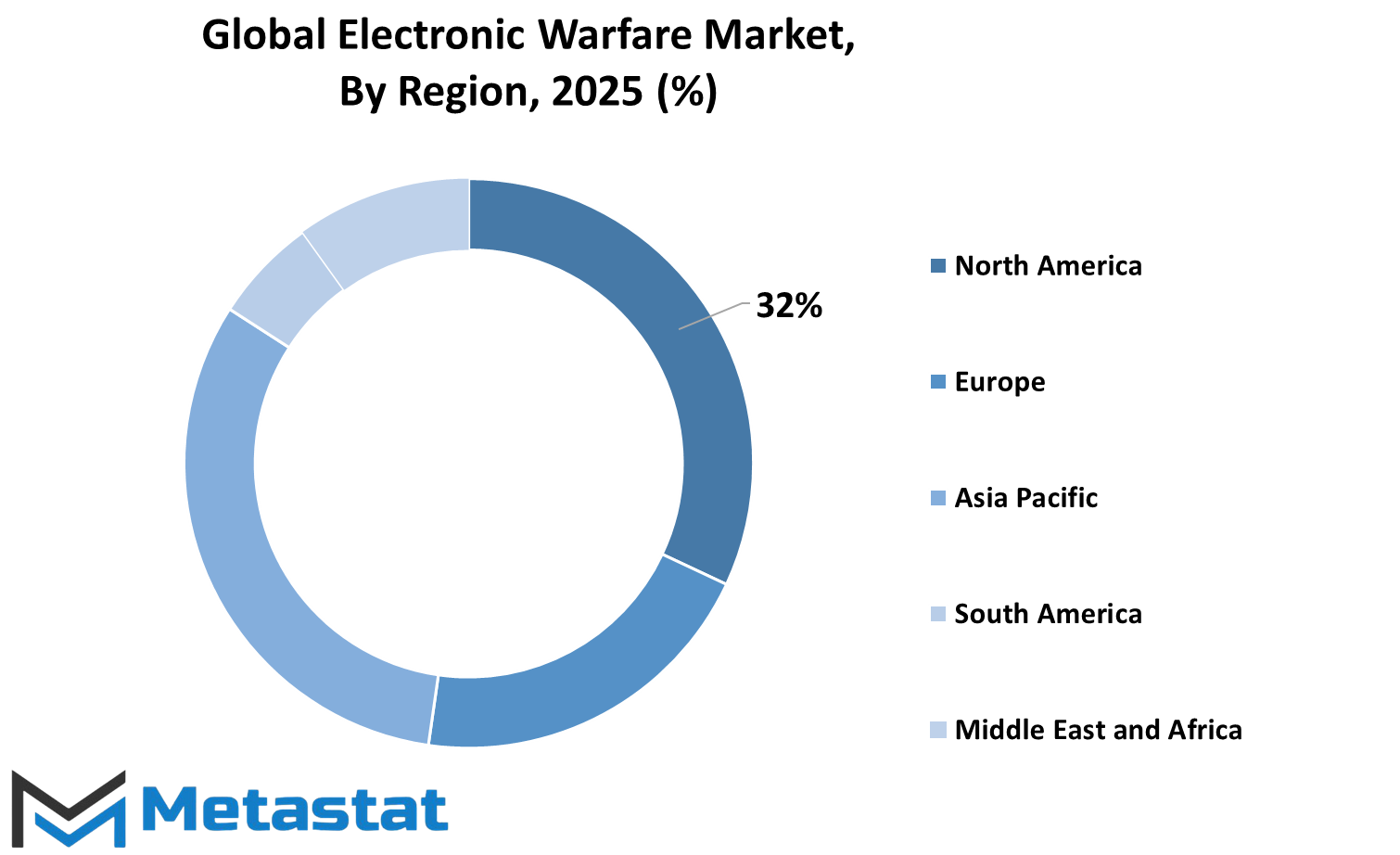

Several geographical planets affect the Global Electronic Warfare market. The market has segments: North America, Europe, Asia Pacific, South America, and the Middle East-Africa as to influencing them reason in different ways to the overall growth of this global industry. North America, which comprises the United States, Canada, and Mexico, but strong defense investments, modernization increases demand for electronic warfare systems in the region through strong technological advancements.

Some countries in Europe affecting the market include United Kingdom, Germany, France, and Italy. They have been emphasizing advanced electronic warfare technologies in their defense strategies with respect to national security enhancement. The rest of Europe also has an active place in the market activities via extensive cooperation and defense projects aimed at augmenting the capacities. Such is the case for the Asia-Pacific region, which has India, China, Japan, and South Korea; developments in the place continue with an upsurge in defense budgets and rising geopolitical tensions. Strong modernizations programs in the militaries of these nations thrive on the demand for high-end and sophisticated electronic warfare systems, ensuring a strong requisition and demand for advanced solutions.

South America, primarily Brazil and Argentina and some others, remains at a pace showing gradual growth in market presence. While far less investment is seen in the region compared to North America or Europe, there are clear signs of modernization efforts in military operations and improvements in defense systems. Part of the growing Middle East & Africa area focuses on EW technologies. Therein are GCC countries, Egypt, and South Africa. An increase in security concerns and conflicts in the region heightens the demand for advanced defense solutions, thus ensuring continuous growth for the market.

Each of these regions takes a particular shape of the Global Electronic Warfare market. Differences in defense strategies, technological advancements, and needs for security are often the characteristics that determine the rate at which electronic warfare systems are adopted. As countries continue to emphasize defense modernization, this market will record continuous advancements that will be much more strengthened by newer developments in global security.

COMPETITIVE PLAYERS

The Global Electronic Warfare market is shaping the future strategies of defense with which nations pursue their interests in terms of security in face of emerging threats with an emphasis on developing military capabilities. Electronic Warfare, short for EW, refers to the actions of using electromagnetic spectrum technologies to detect, disrupt, or protect against hostile actions in EWs. The need for EW systems has increased tremendously due to rising geopolitical tensions, rapid advances in the technology of electronics, and the reasons behind these credits. Today, nations are designing advanced solutions to upgrade their security infrastructures against any threats and sustain an overwhelming superiority in warfare scenarios.

Modern EW systems are expected to provide better situational awareness by allowing the forces to discover potential threats in real time. Significant threats to networks of communications, signal interference, and cyber threats have made such systems indispensable. Digital warfare is ever increasing in multiple dimensions, which is no longer sufficient to warrant military forces sticking only with conventional means of defense. Marked states have made their defense strategies dependent on intercepting and neutralizing hostile signals before creating any damage.

such continuous research and development has become an engine to innovation and adoption of next-generation technologies. This market is huge because it has been dominated by defense majors and defense technology firms that develop high-performance systems, which are usually perfectly suited for today's needs in modern combat. BAE Systems, Raytheon Technologies, Northrop Grumman, and Lockheed Martin play vital roles in promoting the EW capabilities across the globe. These organizations devote themselves to state-of-the-art solutions, which cover the application points on land, air, sea, and space. The Europeans and Israelis with their defense manufacturers, Thales Group; Leonardo S.p.A.; Saab AB; and Elbit Systems also take part in the worldwide growth of these technologies. Companies as such these will keep bubbling with more innovations as defense budgets grow along with better requirements for intelligence and surveillance.

There is also a trend in EW for moving deeper into law enforcement, homeland security, and critical infrastructure protection. To counter electronic threats is not only relevant in traditional warfare, but it sets the stage for fluids in defenses against cyber-attacks and electronic espionage. Anticipating the new-method attack used by adversaries, defense agencies are seeking to strengthen their electronic capabilities. This will lead to advances in EW capability through increased cooperation between defense companies and their respective governments toward speeding up the development and deployment of such advanced technologies.

Electronic Warfare Market Key Segments:

- Airborne

- Ground

- Naval

- Space

By Product

- Equipment

- Operational Support

By Technology

- Antennas

- Anti-Jam Electronic Protection System

- Directed Energy Weapon

- IR Missile Warning System

- Protection System

- Directed Energy Weapon

- Others

By System Type

- Electronic Support Measures (ESM)

- Electronic Attack (EA)

- Electronic Protection (EP)

Key Global Electronic Warfare Industry Players

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential