Global Electronic Data Capture Market - Comprehensive Data-Driven Market Analysis & Strategic Outlook

The global electronic data capture market and its related industry have been existing for quite a while before the digital trial introduced as a standard practice. The history of this industry can be traced back to the late 1980s when the first pharmaceutical firms changed to computerized case report forms instead of the handwritten ones that led to the analysis delays and errors. The very first trials with computer entry were tedious and limited in scope but already pointed out the beginning of a trend that would, in time, revolutionize clinical research and medical data management. By the late 1990s, regulatory agencies such as the U.S. Food and Drug Administration had already digitized and modernized their record-keeping expectations, thereby influencing the trial sponsors and contract research organizations to test the effectiveness of structured digital systems. Presently, we are only seeing the early development of the commercially available platforms which will in the future support and represent the increasingly sophisticated cloud computing-based data management.

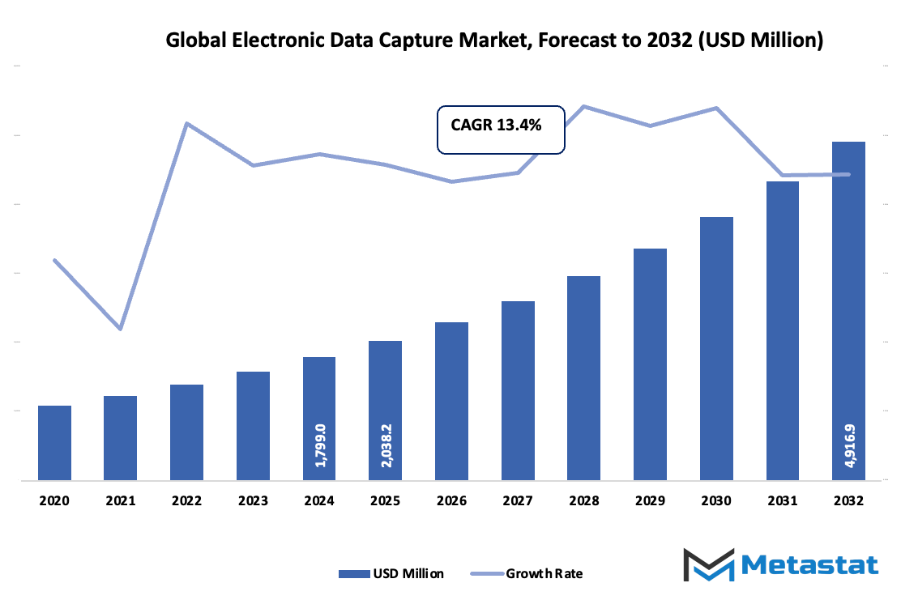

- The global electronic data capture market is estimated to reach approximately USD 2038.2 million by 2025, showing a CAGR of around 13.4% through to 2032 and possibly exceeding USD 4916.9 million.

- On-Premises will be nearly 15.4% of the total market and will be one of the primary factors for the maturation of the field and expansion of its application through detailed research.

- The requirement for automation in clinical trials is the leading factor attracting firms to the market, and the use of EDC systems at hospitals and health centers is also on the rise.

- Partnerships with AI and machine learning will be among the new technologies that will significantly contribute to the growth trajectory of the global electronic data capture market.

- Integration opportunities with AI and machine learning are among the emerging technologies that will be the main driving Force behind the trends.

- Market insight: Massive increase in value is expected in the market over the coming ten years highlighting the strong growth potential.

The defining moment for the industry coincided with the enhancement of internet connectivity. Clinical trial platforms for the web were introduced in the early 2000s, which made it possible for the investigators to enter data directly from the respective research locations, which, as per the National Institutes of Health official reports, shortened the verification phase by up to 40 percent. The shift further supported conducting clinical trials on a worldwide scale and enabled research facilities located far apart to share similar datasets in few minutes. The upcoming decade would witness the data protection law changes for example, the European Union's upgrades to the patients' privacy law affecting the way data was kept, encrypted, and moved around. The technology vendors reacted to this by incorporating more robust authentication and logging features, thus making sure that the electronic records were in line with the evolving laws of the various regulatory authorities.

One of the major reasons behind the decentralized trial concept has been the development of mobile-friendly patient tools that can gather information from outside of the traditional clinical settings. Besides, the technology need for adaptable data interfaces got additional validation from the Centers for Disease Control and Prevention, which indicated that remote patient monitoring programs had increased by more than 25 percent during health emergencies. At the same time, research facilities have put considerable resources into implementing automated validation features that will shorten the time for manual review and increase the reliability of the records kept for a long time. The industry will at its own pace move to platforms that are capable of handling larger and diverse datasets as health reporting through devices becomes more common, thus paving the way for the next generation.

Market Segments

The global electronic data capture market is mainly classified based on Delivery Mode, Development Phase, End-User.

By Delivery Mode is further segmented into:

- On-Premises: In the global electronic data capture market, on-premises delivery mode will support secure handling of study records within internal systems. This approach will give direct control over storage, updates, and access rules. Many organizations will select this mode when strict data rules, limited internet access, or specific internal processes shape daily study operations.

- Web & Cloud-Based: Web and cloud-based delivery mode will allow flexible access to study information through online platforms. This option will reduce hardware demands and will help organizations adjust capacity during intense research periods. Easy updates, shared access, and remote monitoring will support smoother coordination across teams handling clinical activities.

By Development Phase the market is divided into:

- Phase I: Phase I development stage will focus on early safety checks that require clear tracking tools for participant responses. Electronic systems in this stage will support structured inputs that reduce errors and speed up early review. Quick access to collected information will help teams decide the next steps with confidence during initial testing.

- Phase II: Phase II stage will involve deeper testing to understand how a treatment performs. Data systems will organize growing volumes of observations and help maintain steady communication among research groups. Accurate records will guide decisions on dose levels, participant management, and study adjustments needed before moving to larger testing.

- Phase III: Phase III stage will demand strong data support because large participant groups will generate extensive information. Electronic tools will streamline tracking, reduce paperwork delays, and help teams compare patterns across multiple sites. Reliable collection methods will be important for meeting strict review standards before approval steps proceed.

- Phase IV: Phase IV stage will continue after product approval and will monitor performance in real-world settings. Systems will help track long-term outcomes, side-effect patterns, and responses across wider groups. Consistent recording will allow organizations to refine safety actions and maintain trust through ongoing observation after public release.

By End-User the market is further divided into:

- Hospitals/Healthcare Providers: Hospitals and healthcare providers will use electronic systems to manage study entries, improve accuracy, and reduce time spent on manual tasks. Direct real-time access will support clinical staff in updating treatment responses and monitoring progress. This will help create smoother coordination between study needs and regular care duties.

- CROs: Contract research organizations will rely on reliable digital tools to coordinate studies for multiple clients. Centralized systems will help manage timelines, documentation, and site communication. This will allow efficient handling of varied study sizes and support consistent tracking standards across all locations involved in outsourced clinical work.

- Pharmaceutical and Biotechnology Firms: These firms will use digital data tools to manage research stages, maintain accurate results, and speed up decision cycles. Streamlined entries will improve review processes and help teams adjust methods based on incoming information. Organized systems will support faster progress toward regulatory steps and product development goals.

- Medical Device Firms: Medical device firms will apply digital tools to track testing outcomes, performance measures, and user feedback across clinical studies. Clear data structures will help teams detect issues early and adjust prototypes when required. This will create steady support for evaluation steps tied to safety, function, and user experience standards.

- Others: Other organizations involved in research will use electronic data tools to improve organization, reporting, and review activities. These systems will support smoother communication and reduce delays caused by manual handling. Flexible setups will help varied teams manage their tasks without complications tied to changing study conditions or workflow needs.

|

Forecast Period

|

2025-2032

|

|

Market Size in 2025

|

$2038.2 Million

|

|

Market Size by 2032

|

$4916.9 Million

|

|

Growth Rate from 2025 to 2032

|

13.4%

|

|

Base Year

|

2024

|

|

Regions Covered

|

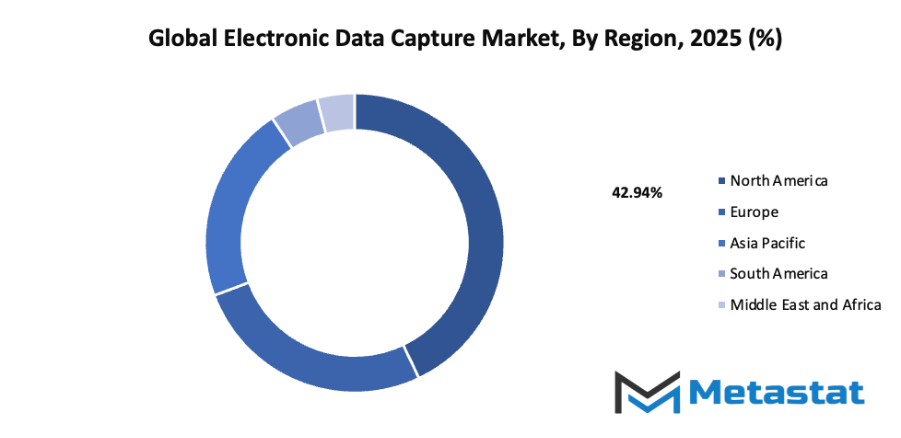

North America, Europe, Asia-Pacific, South America, Middle East & Africa

|

By Region:

- Based on geography, the global electronic data capture market is divided into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

- North America is further divided into the U.S., Canada, and Mexico, whereas Europe consists of the UK, Germany, France, Italy, and the Rest of Europe.

- Asia-Pacific is segmented into India, China, Japan, South Korea, and the Rest of Asia-Pacific.

- The South America region includes Brazil, Argentina, and the Rest of South America, while the Middle East & Africa is categorized into GCC Countries, Egypt, South Africa, and the Rest of the Middle East & Africa.

Growth Drivers

- Increasing demand for automation in clinical trials: Growing automation needs continue to guide expansion of the global electronic data capture market as clinical research teams pursue faster data handling, reduced manual errors, and smoother study workflows. Rising pressure for timely trial outcomes encourages wider platform adoption across major research centers and contract organizations.

- Growing adoption of EDC systems in the healthcare sector: Rising acceptance of digital data tools across hospitals, clinics, and research units supports stronger platform use for study oversight, form design, and reliable data collection. Broader workflow standardization encourages structured data capture that supports quality review, faster reporting, and consistent study output across diverse medical environments.

Challenges and Opportunities

- High implementation costs: Significant investment requirements for software licensing, system configuration, staff training, and long-term maintenance create barriers for smaller research groups and emerging healthcare facilities. Limited budgets restrict broader system deployment, causing slower modernization and delayed adoption of structured digital platforms across several regions with constrained funding resources.

- Data privacy and security concerns: Increasing regulatory expectations demand stronger safeguards for sensitive clinical information, encouraging rigorous validation, controlled access, encryption tools, and monitored data flows. Weak protection measures risk unauthorized exposure, operational delays, and reduced stakeholder confidence, leading to cautious platform deployment within organizations handling significant volumes of confidential study information.

Opportunities

Integration with emerging technologies such as AI and machine learning: New analytical capabilities support responsive data checks, smarter study design, and faster pattern recognition that can strengthen trial oversight. Automated insights encourage flexible platform use, enhanced data quality, and timely decision support across varied clinical programs seeking structured digital assessment.

Competitive Landscape & Strategic Insights

The industry presents a landscape shaped by long-standing global companies working alongside ambitious regional groups. Each organization brings a different history, level of experience, and set of tools, creating steady movement toward better data handling and stronger support for research activities. Growth in digital research methods continues to push every participant toward higher accuracy, smoother workflows, and dependable systems that support complex studies without unnecessary delays or confusion.

A wide range of established names guides much of the direction taken within the global electronic data capture market. Key organizations such as Calyx, Medidata Solutions, Inc., Oracle, Veeva Systems, Fountayn, Acceliant, MedNet, Advarra, Medrio, Inc., Greenlight Guru Clinical, Clinion, ICON plc, OpenClinica LLC, Castor, ClinCapture, Inc., Merative Clinical Development, Vanderbilt (REDCap), and Dacima Survey (EvidentIQ Group) stand at the center of current progress. Each group offers platforms designed to strengthen research quality, reduce errors, and support dependable study management from early planning stages to final reporting. Constant updates, growing integration features, and strong customer support encourage wider adoption, especially as more studies move toward digital formats.

Competition among international leaders and rising regional firms encourages steady improvement, leading to systems that support clearer data entry, quick access to information, and consistent protection of sensitive material. Better design also helps research teams work without unnecessary challenges, allowing faster turnaround on important tasks. Frequent collaboration between technology groups and research organizations encourages thoughtful development, ensuring that new tools support real-world needs rather than creating additional steps or confusion.

Market size is forecast to rise from USD 2038.2 million in 2025 to over USD 4916.9 million by 2032. Electronic Data Capture will maintain dominance but face growing competition from emerging formats.

With many influential companies working toward similar goals, the market continues to benefit from strong innovation, dependable service, and a growing focus on accuracy. Careful attention to user experience, data safety, and study efficiency pushes every organization toward higher standards, supporting a future built on trust, clarity, and steady progress.

Report Coverage

This research report categorizes the global electronic data capture market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the global electronic data capture market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the global electronic data capture market.

Electronic Data Capture Market Key Segments:

By Delivery Mode

- On-Premises

- Web & Cloud-Based

By Development Phase

- Phase I

- Phase II

- Phase III

- Phase IV

By End-User

- Hospitals/Healthcare Providers

- CROs

- Pharmaceutical and Biotechnology Firms

- Medical Device Firms

- Others

Key Global Electronic Data Capture Industry Players

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential