MARKET OVERVIEW

The global district cooling market is a revolutionary sector of the infrastructure and energy industry, and its course for the future lies light-years ahead of traditional paradigms. With expanding urban areas and smart city efforts currently at the forefront, the implementation of district cooling systems will influence a future era of climate control with a "green" twist. These systems, which flow into chilled water for aircon in a web of insulated pipes, will become ubiquitous in business districts, business parks, and an increasing number of in excessive-density housing. This trend isn't always primarily based on quick-time period bursts of demand or seasonal cycles; it's far deeply connected to a larger shift in how cities will approach electricity performance and ecological duty.

In the next few years, the global district cooling market will quit to be a spot marketplace constrained to unique geographies or constructing sorts. It will advantage traction in areas historically depending on decentralized air con, as policymakers, developers, and strength providers recognize the long-time period payoffs of centralized cooling networks. In sub-tropical and tropical areas, specially Asia and elements of the Middle East, the market will see extended infrastructure investment because of developing population density and concrete migration. Yet this boom might not be delivered approximately totally by using climatic necessities however by way of a bigger strategic shift towards centralized structures that provide decrease emissions, extra efficiency, and a smaller footprint of operation.

As city infrastructure keeps upgrading, the aggregate of district cooling with virtual monitoring networks and smart grids becomes the same old. The advances will facilitate actual-time optimization of cooling demand and deliver, yielding value financial savings and extra reliability. More importantly, information-pushed planning will result in extra shrewd expansions and improvements, minimizing capital waste and strength inefficiencies. Thermal strength storage innovations can also be a key aspect, enabling those structures to seize cooling all through non-height hours and disburse it at some point of top demands, ensuing in greater levelled power intake across cities.

The position of personal corporations and public-private partnerships in the global district cooling market will also growth. With converting financing fashions and the growing recognition of lengthy-time period provider preparations, investment in district cooling infrastructure will not be a situation of municipal government. Developers will begin to see cooling flowers now not merely as utilities, however as strategic belongings that build belongings price, minimize lifecycle charges, and meet international sustainability standards. Carbon credit score incentives and green certification requirements may also spur adoption, driving older HVAC fashions to turn out to be out of date in the long run.

Glancing beyond the region, global collaboration and knowledge-sharing platforms will shape standards-setting, system design, and performance measurement. Global policy dialogues and forums will position district cooling at the center of climate resilience planning, allowing it to be integrated into environmental planning from the very beginning instead of it being an afterthought solution.

In the give up, the global district cooling market will no longer in reality reply to evolving urban necessities it will form them. Its destiny is to end up a constituent part of the current infrastructure, figuring out the manner towns may be capable of use their power, acquire sustainability objectives, and provide consolation inside the useful resource-scarce global.

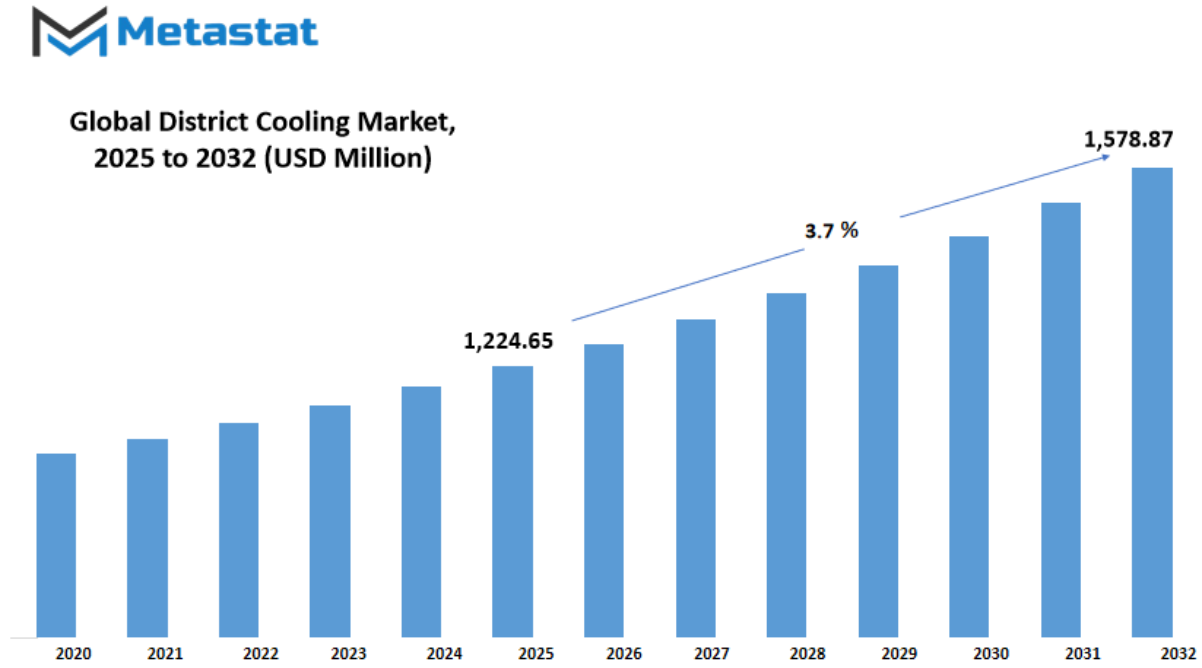

Global district cooling market is estimated to reach $1,578.87 Million by 2032; growing at a CAGR of 3.7% from 2025 to 2032.

GROWTH FACTORS

The global district cooling market is steadily emerging as an integral part of new-age urban development, fueled by an increasing demand for energy-efficient and sustainable cooling solutions. With conventional air conditioning units being major power and carbon emitters in most cities, there has been a move from both the public and private sectors towards wiser options. District cooling, that is renowned for delivering chilled water from a principal facility to diverse structures, affords a more efficient manner of addressing big-scale cooling wishes. With urban infrastructure increase and the need to lower carbon footprints, district cooling is turning into an answer of desire, especially for industrial centers and excessive-density areas.

Much of the global district cooling marketis moreover boosted with the aid of authorities incentives and help packages for promoting cleaner electricity assets. Governments in many countries are offering subsidies, tax comfort, and policy assistance to enhance the uptake of district cooling structures. These tasks now not simplest ease the value strain for developers but additionally decorate investor confidence in lengthy-term tendencies. Furthermore, developers have become more aware about green constructing codes, further driving the call for district cooling systems that store power and lower greenhouse gases.

Yet, even with the growing popularity, the global district cooling market is experiencing discernible problems. One of these challenges is high initial capital outlay in the development of infrastructure as well as the installation of the system. Relative to traditional cooling, district cooling systems demand intensive planning, capital, and coordination among stakeholders. This tends to slow down implementation, particularly in those markets with budget limitations or splintered planning. In addition, limited knowledge in most developing areas continues to retard the adoption pace. Without adequate education on long-term savings and environmental advantages, most cities do not get an opportunity to transition toward this new cooling technique.

Nevertheless, the future of the global district cooling market remains optimistic. The international move towards smart cities is generating a new wave of prospects. Urban developers are incorporating district cooling systems into the fundamental conception of smart city architecture, where optimization of energy is paramount. Such smart schemes are conceived to utilize centralized facilities that can be remotely monitored and optimized in real-time, and thus district cooling is a perfect fit. In addition, increasing interest in integrating renewable energy e.g., integrating solar thermal systems with district cooling networks is anticipated to increase efficiency and attract environmentally motivated policies.

As word gets out and technology advances, district cooling will become more available and affordable. The intersection of wise urban making plans and easy energy targets locations this market squarely at the course to sustained expansion. As tough as it could be, with non-stop improvements and favorable rules, district cooling turns into a cornerstone of the sector's transition to cleaner, extra sustainable cities.

MARKET SEGMENTATION

By Technology

The global district cooling market is slowly picking up pace as cities look for more intelligent, more environmentally friendly means of tackling their increasing energy demands. As urban growth and commercial infrastructure expand, there is a greater demand for cost-saving cooling systems with lower energy use and reduced environmental footprint. The district cooling presents a centralized solution through the distribution of cold water through a system of burial, untouched pipes in many buildings and thus reduces power consumption compared to the standalone air conditioning system. This system not only facilitates environmental purposes, but also provides long -term financial savings with governments, developers and companies, which makes it look attractive.

Technological progress provides a central role in the global district cooling market, leading to electric chiller. These systems, worth $725.11 million, find a wide scale of adoption because they are efficient, reliable, and compatible with city infrastructure. Electric chillers, in most cases, are accompanied by renewable energy sources, which enables cities to reduce carbon emissions. Coupled with them are absorption chillers, which are also starting to be felt, particularly where there is convenient waste heat or thermal energy available. It offers a solution for urban areas that seek to diversify inputs in terms of energy and still achieve cooling efficiency. Other technologies in this category are also offering flexibility and customization as per geographical climate factors and end-user requirements.

With the awareness of weather exchange and sustainable power use on the rise, district cooling is gaining popularity in regions with extreme climates and high cooling hundreds, such as the Middle East and positive areas of Asia. These regions are experiencing most important funding in urban improvement schemes, and district cooling systems are generally integrated into the making plans system itself. The government is aiding those efforts through policy interventions and infrastructure investments, urging the private zone to come on board to force more green urban utilities. Integration of smart technology and real-time tracking devices is also assisting agencies in higher load control, lowering wastage, and improving basic system overall performance.

Although it has advantages, the global district cooling market still has the issues of high upfront investment and long project durations. Installing a full district cooling system takes time, planning, and money, which might impede take-up in countries where immediate return is valued. Nevertheless, with increased recognition and proven long-term costs savings, these issues will likely ease out over time. Technological advancements, particularly in electric and absorption chiller efficiency, will also work to reduce costs and bring these systems to wider and more varied markets. District cooling will, over time, be a key component of how contemporary cities are going to manage energy efficiency and climate responsibility.

By End-user

District cooling is picking up pace as a wise and efficient way of controlling city temperatures. Rather than the usage of separate air con units in each building, district cooling elements chilled water from one valuable plant to several buildings the usage of an underground community of insulated pipes. Not simplest does this keep strength, but additionally carbon emissions and upkeep expenses are minimized. As cities growth their density and the demand for sustainable infrastructure grows, district cooling will more and more emerge as part of the urban landscape. The global market is reacting with consistent investment and developer, government, and utility provider interest.

The residential market is taking an increasingly prominent role in the district cooling market, particularly in areas with severe climates and high density. Across most of the rapidly growing cities, housing complexes are being constructed with district cooling links already established. This provides homeowners with affordable and reliable cooling and allows urban authorities to better manage energy burdens. The attraction comes in terms of the comfort of stable indoor temperatures and economic savings from centralized system efficiency. Developers also see value in encouraging green buildings that meet green building standards.

The business segment places of work, malls, accommodations, and entertainment hubs remains a strong driving force of call for. These buildings frequently require 24/7 temperature control, specifically in areas with hot weather most of the year. By switching to district cooling, industrial institutions can decrease energy payments and decrease pressure at the nearby strength grid. For companies looking to attain sustainability, district cooling presents a sensible way in the direction of reduced emissions without having to sacrifice comfort. Its continuous use in business areas shows destiny growth as extra corporations prioritize sustainable operations.

In business environments, the requirement for managed temperatures is regularly undertaking-important. From factories to statistics centers, industries depend on effective cooling to make sure productiveness and shield system. District cooling affords an alternative it really is now not simply dependable, but additionally scalable as facilities develop. It comprises long cycles of operation and may be custom designed to match precise necessities, which makes it a worthy choice for industrial customers in search of to decrease operational hazard and environmental footprint.

Overall, the global district cooling market is heading in the direction of mass adoption across numerous industries, with end-users becoming more aware of its benefits. With growing recognition of climate trade and strength performance, demand from residential, business, and commercial clients will similarly advantage energy. Urban developers and planners already consist of district cooling in new developments, indicating a future when commonplace cooling structures are the guideline and no longer the exception.

|

Forecast Period |

2025-2032 |

|

Market Size in 2025 |

$1,224.65 million |

|

Market Size by 2032 |

$1,578.87 Million |

|

Growth Rate from 2025 to 2032 |

3.7% |

|

Base Year |

2024 |

|

Regions Covered |

North America, Europe, Asia-Pacific Green, South America, Middle East & Africa |

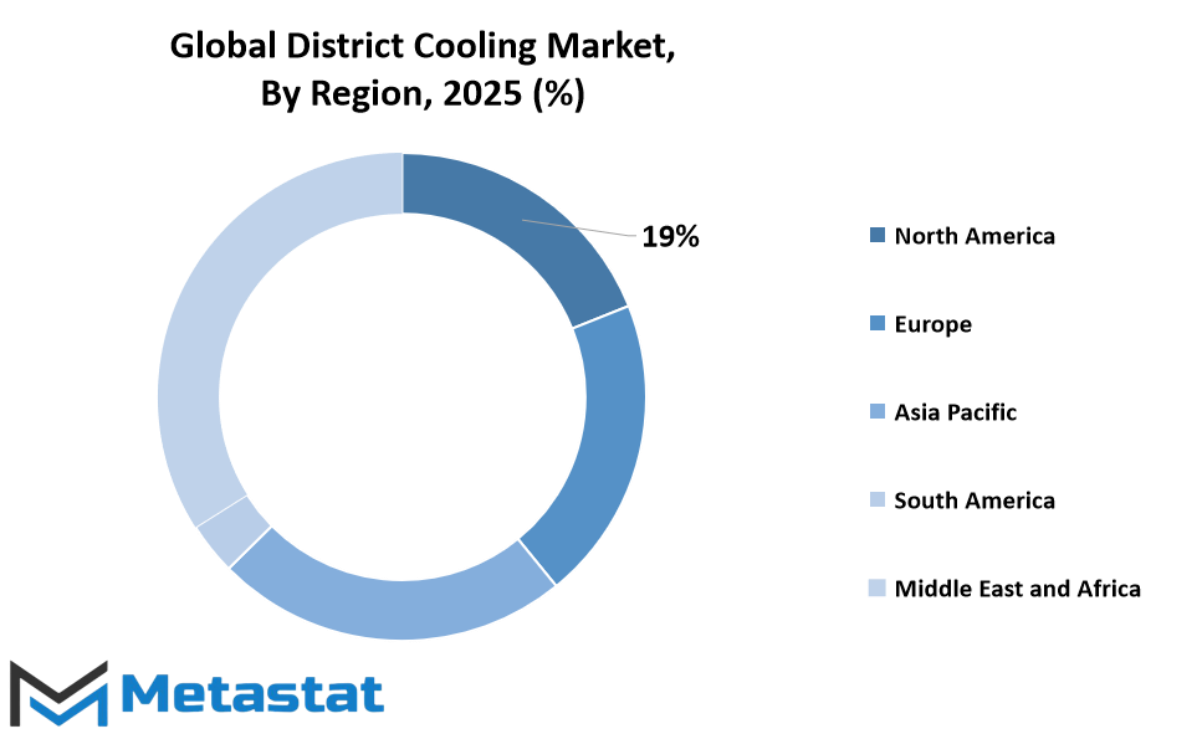

REGIONAL ANALYSIS

The global district cooling market is witnessing constant attention in all regions, inspired by using climatic necessities, power performance targets, and urbanization styles. On the basis of geography, the market is classified into five primary regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Every region has its personal set of opportunities and demanding situations, pushed by way of economic situations, environmental laws, and growing necessities for sustainable cooling solutions in excessive-density city areas. Nations are leaving behind conventional air-conditioning structures in favor of centralized networks, minimizing energy use and decreasing greenhouse gasoline emissions. District cooling, on this recognize, will remain an indispensable part of large techniques for attaining lengthy-term strength efficiency.

In North America, the United States, Canada, and Mexico are the predominant participants to the global district cooling market. Over the years, the U.S. Has been one of the early adopters of district cooling technologies, in particular in big towns and university campuses. With growing worries over strength costs and carbon footprints, utilities and personal sector players are making an investment in systems that provide constant performance whilst reducing operational fees. Canada is witnessing demand for district cooling for the same reasons, particularly in the dense urban areas of Toronto and Vancouver, where concentrated infrastructure is well-served by communal energy systems. Mexico, although relatively lagging behind, is seeking to apply such models to newer construction, especially in commercial areas.

Europe comes next with the UK, Germany, France, Italy, and the rest of the continent participating heavily. They tend to take the lead in energy transition and climate action discussions, which makes district cooling a logical expansion of current environmental policy. Germany and France, for example, have actively advocated infrastructure schemes which can be focused on performance and sustainability, and this is evident inside the growing quantity of district cooling networks. Italy, the UK, and others also are selling public-private partnerships to increase coverage, in particular in historical past architecture regions wherein traditional systems are tough to install with out considerable modifications. The necessity to reconcile with climate targets will keep to maintain district cooling an integral part of European town planning.

Asia-Pacific, such as India, China, Japan, South Korea, and nearby nations, is becoming one of the maximum promising areas for market development. Urbanization, international warming, and monetary increase are putting excellent pressure on modern-day cooling infrastructure. China and India, with their good sized populace and growing center elegance, are also key markets. Country-pushed efforts to reduce emissions and top energy demand management are starting up possibilities for district cooling answers. Japan and South Korea are already pioneers in integrating technology and will most probably leverage their revel in to improve cooling infrastructure in smart cities. Rest of Asia-Pacific will take this momentum, modulating according to local improvement and energy regulations.

In South America, Brazil and Argentina are slowly transitioning closer to implementing greater green cooling structures. While the transition is slow in comparison to other countries, it's far taking place, specifically in densely populated commercial districts and concrete redevelopment tasks. Financial constraints may be a difficulty, however accelerated consciousness of long-time period savings and power safety will propel demand.

COMPETITIVE PLAYERS

The global district cooling market will remain in the spotlight as cities seek smarter and more efficient means of meeting energy needs. As populace growth in towns will increase and climate styles become more extreme, there may be increased demand for cooling answers that consume less energy and are environmentally pleasant. District Cooling, a cooling gadget that circulates bloodless water from a important facility to numerous homes, is turning into an increasing number of popular amongst densely urbanized regions. This system reduces the call for for separate air conditioners, which are typically much less power green and greater steeply-priced in the end.

Middle Eastern countries, Southeast Asian nations, and some European countries have already implemented this system on a mass scale. The advantage is that it can decrease electricity usage, cut carbon emissions, and provide improved indoor comfort. Developers and governments are now starting to view it as a long-term solution that is favorable for the environment without making utility bills uncertain. In areas where the power grid is strained, District Cooling provides means through which the strain can be minimized by distributing the load more effectively. In addition, its centralized structure makes it simpler to monitor and maintain.

Several key players in the industry will participate in the global district cooling market with full force and lead the manner in which District Cooling systems are designed and implemented. Emirates Central Cooling Systems Corporation (Empower) and National Central Cooling Company PJSC (Tabreed) are among the companies leading the industry in high standards. Others consisting of Veolia Environnement S.A., ENGIE, Fortum, and Ramboll Group A/S are increasing their presence in one of a kind countries, leveraging their infrastructure and sustainable solution competencies. Technological help from Danfoss, Alfa Laval, and Cetetherm is also spearheading increased performance, even as businesses along with ADC Energy Systems and Stellar Energy are supplying custom designed systems for business and home packages. Keppel Corporation Limited, Shinryo Corporation, and Logstor additionally preserve to play full-size roles inside the physical and operational infrastructure of these systems.

District Cooling is no longer considered a luxury service for large commercial areas. It's gradually turning into a viable alternative for mixed-use developments and residential complexes. With governments nudging the use of cleaner energy and regulations on carbon emissions, the inducements for such systems will be more. Public-private collaborations, investment in infrastructure, and increasing consumer awareness will all contribute to the growth of this market.

With increasing temperatures and increased urbanization, the global district cooling market not only will survive but also prosper.As more cities make efforts to improve their cooling infrastructures, this approach provides a scalable and low-priced method of addressing electricity responsibly. With healthy enterprise leaders spearheading innovation and governments imparting the right incentives, the global district cooling market is probable to revel in constant increase in both rising and evolved economies.

District Cooling Market Key Segments:

By Technology

- Electric Chillers

- Absorption Chillers

- Others

By End-user

- Residential

- Industrial

- Commercial

Key Global District Cooling Industry Players

- Emirates Central Cooling Systems Corporation (Empower)

- National Central Cooling Company PJSC (Tabreed)

- Veolia Environnement S.A.

- ENGIE

- Fortum

- Ramboll Group A/S

- ADC Energy Systems

- Danfoss

- Emirates District Cooling LLC (Emicool)

- Alfa Laval

- Keppel Corporation Limited

- Shinryo Corporation

- Cetetherm

- Stellar Energy

- Logstor

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential

US: +1 3023308252

US: +1 3023308252