Defense Radar Market Size, Share, By Platform (Land-based Radars, Naval Radars, and Others), By Product Type (Surveillance, Early Airborne Warning Radar, Fire Control Radar, Multi-Function Radar, and Others), By Component (Antenna, Transmitter, Receiver, Duplexer, and Others), By Application (Air, Missile Defense, Intelligence, Surveillance and Reconnaissance, Navigation, Weapon Guidance, Space Situation Awareness, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4705

Published

April 30, 2026

Pages

313 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

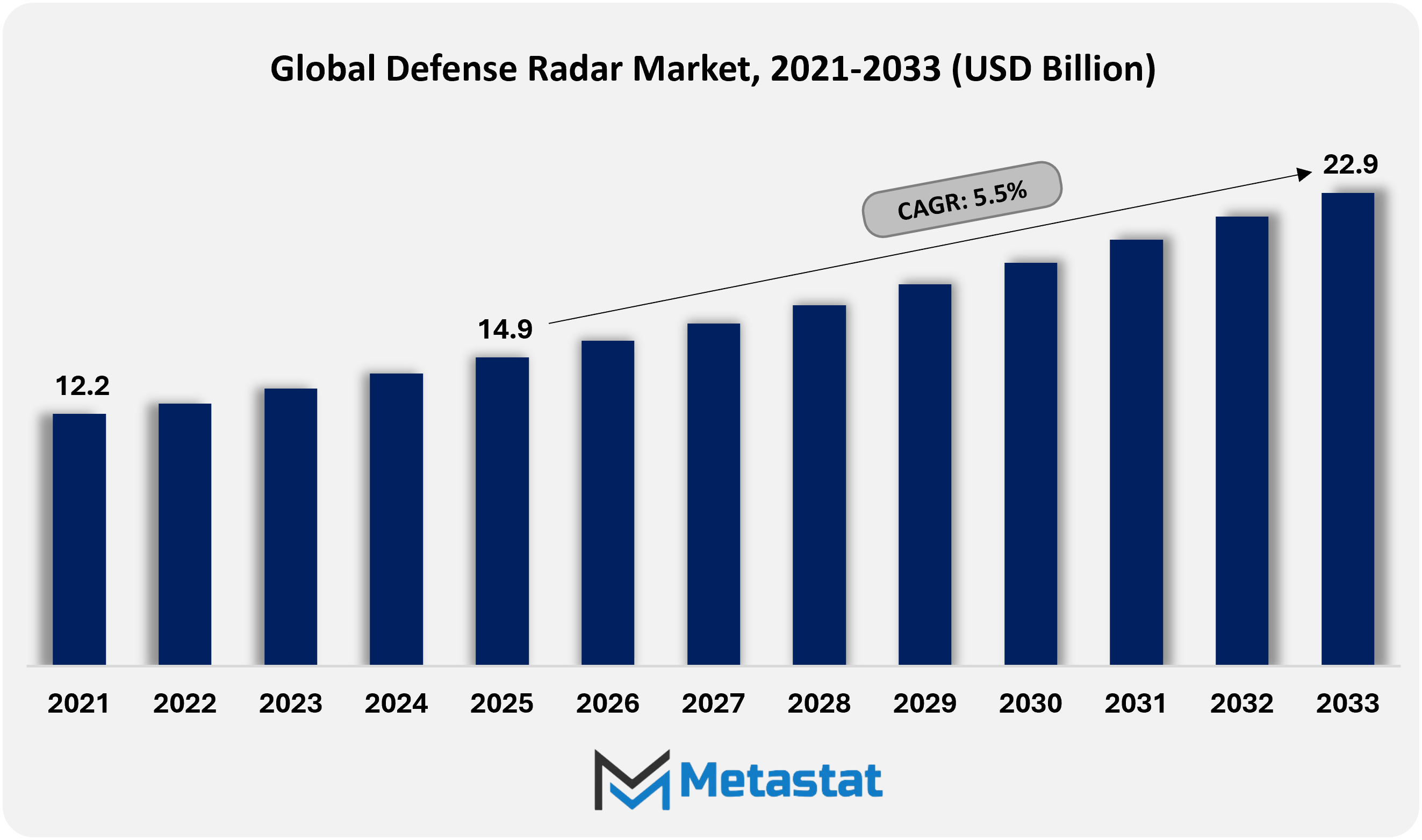

Global Defense Radar market size is valued at USD 14.9 billion in 2025 and projected to grow at a CAGR of 5.5% during the forecast period, reaching USD 22.9 billion by 2033.

Global Defense Radar Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

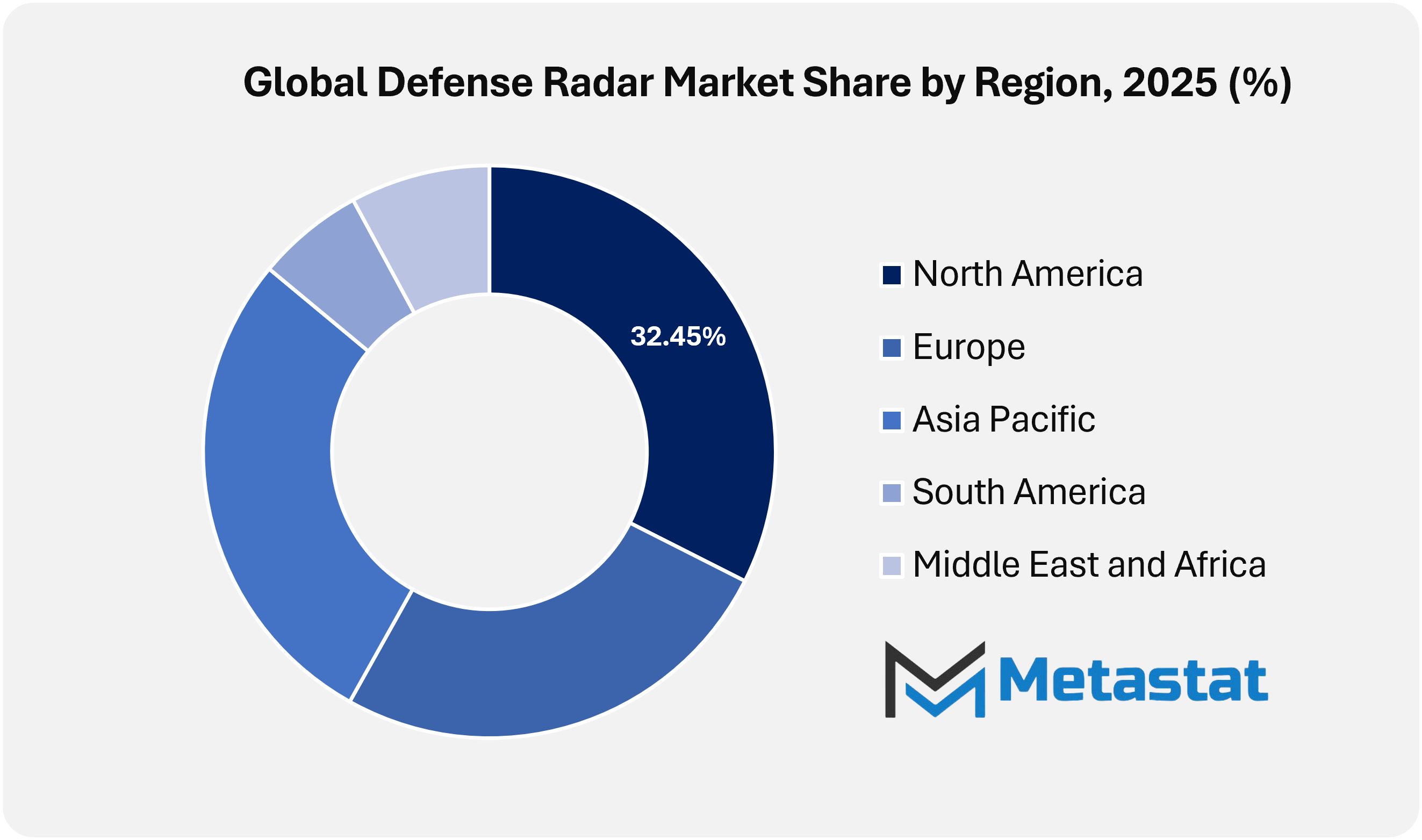

North America accounted for 32.5% of the global market in 2025, with the U.S. leading regional market revenue.

Land-based Radars segment accounted for a market share of 45.9% in 2025.

Key trends driving growth: Air and missile defense modernization programs across land, sea, and air forces along with Shift toward multi-function AESA architectures and software-defined radar upgrades.

Opportunities include counter-uncrewed aerial systems and low-altitude surveillance demand across critical infrastructure and forward bases.

Key insight: Rising geopolitical tensions and rapid modernization of military surveillance systems are accelerating demand in the Global Defense Radar market.

The Global Defense Radar market within the aerospace and defense industry is expanding beyond conventional battlefield surveillance and early warning functions. Over the forecast period, radar systems will play a central role in integrated digital warfare ecosystems, operating as intelligent nodes within distributed command architectures. Rather than serving only as standalone detection platforms, advanced radar systems will transmit encrypted real-time data into joint operational networks, supporting predictive threat assessment and coordinated response across air, sea, land, space, and cyber domains.

Future deployments will increasingly support space situational awareness, tracking not only ballistic trajectories but also orbital congestion and hostile satellite activity. Defense organizations will rely on next-generation radar arrays to monitor debris fields and protect strategic assets in low Earth orbit. Naval forces are also likely to adopt compact, energy-efficient radar systems capable of persistent maritime domain awareness, strengthening the security of undersea infrastructure and critical trade routes.

Market Dynamics

Growth Drivers:

Air and missile defense modernization programs across land, sea, and air forces.

Global Defense Radar market growth is being driven by sustained investment in air and missile defense modernization programs across ground-based batteries, naval combat systems, and airborne early warning fleets. Governments are prioritizing layered detection networks capable of tracking ballistic, cruise, and hypersonic threats. Procurement strategies are increasingly focused on long-range surveillance radars, integrated command networks, and rapid deployment systems that support joint-force interoperability.

Shift toward multi-function AESA architectures and software-defined radar upgrades

Global Defense Radar market expansion is further supported by the shift toward multi-function active electronically scanned array architectures and software-defined radar upgrades. Defense organizations are increasingly adopting systems that combine surveillance, fire control, and electronic protection capabilities within a single platform. Software-centric enhancements enable waveform agility, remote upgrades, improved target discrimination, and greater lifecycle flexibility without requiring full hardware replacement.

Restraints and Challenges:

High lifecycle costs tied to sustainment, calibration, and mission software updates

Global Defense Radar market growth faces constraints from high lifecycle costs associated with sustainment, precision calibration, and recurring mission software updates. Advanced radar installations require specialized maintenance infrastructure, trained personnel, and periodic component replacement. Budget pressures across defense ministries are increasing scrutiny over total cost of ownership, which will affect procurement timelines and long-term upgrade commitments.

Export controls, security clearances, and classified integration constraints across supply chains

Global Defense Radar market development is also challenged by export control regimes, strict security clearances, and classified integration requirements across global supply chains. Cross-border collaboration requires compliance with national security laws, technology transfer regulations, and secure communication standards. Delays in regulatory approvals can influence contract execution timelines and limit coordination across multinational defense programs.

Opportunities:

Counter-uncrewed aerial systems and low-altitude surveillance demand across critical infrastructure and forward bases

A major opportunity in the Global Defense Radar market lies in rising demand for counter-uncrewed aerial system detection and persistent low-altitude surveillance across critical infrastructure and forward operating bases. Radar solutions designed to detect small, slow, and low-signature targets are gaining strategic importance. Integration with command analytics, electronic countermeasures, and rapid response systems will strengthen adoption across defense and homeland security applications.

Market Segmentation Analysis

The Global Defense Radar market is classified based on Platform, Product Type, Component, and Application.

By Platform, the market is further segmented into:

Land-based Radars

Land-based Radars segment is valued at USD 7.2 billion in 2026 and is projected to reach USD 10.3 billion by 2033, at a CAGR of 5.1% during the forecast period.

Land-based Radars within the Global Defense Radar market are gaining strategic importance through border security modernization programs and integrated air defense networks. Advanced phased-array architectures, extended detection ranges, and AI-enabled tracking systems are strengthening national surveillance capabilities. Rising geopolitical tensions will accelerate procurement across both developed and emerging defense economies.

Naval Radars

Naval Radars segment is valued at USD 5.3 billion in 2026 and is projected to reach USD 7.4 billion by 2033, at a CAGR of 5.1% during the forecast period.

Naval Radars within the Global Defense Radar market are expanding through fleet modernization programs and the growing emphasis on blue-water naval capabilities. Future warship programs will require compact, high-resolution radar systems with improved maritime target discrimination. Increased focus on littoral combat readiness and anti-submarine warfare is also supporting adoption of advanced radar suites.

Others

Others segment is valued at USD 3.3 billion in 2026 and is projected to reach USD 5.2 billion by 2033, at a CAGR of 7% during the forecast period.

Other platforms in the Global Defense Radar market, including airborne and space-based systems, are witnessing rising investment driven by network-centric warfare strategies. Integration with unmanned systems and satellite-linked communication frameworks is improving operational flexibility. Defense organizations are prioritizing mobility, scalability, and rapid deployment capabilities across these radar platforms.

By Product Type, the market is divided into:

Surveillance and Early Airborne Warning Radar

Surveillance and Early Airborne Warning Radar segment is projected to reach USD 8.4 billion by 2033, at a CAGR of 4.9% during the forecast period.

Surveillance and Eearly Airborne Warning Radar remains a critical segment in the Global Defense Radar market, supporting real-time threat detection and long-range tracking capabilities. Next-generation systems are being developed with data fusion, electronic counter-countermeasure capability, and enhanced signal clarity. Demand is increasing with the growing need for cross-border monitoring and airborne threat management.

Fire Control Radar

Fire Control Radar segment is projected to reach USD 5.2 billion by 2033, at a CAGR of 5% during the forecast period.

Fire Control Radar in the Global Defense Radar market is growing with rising demand for precision targeting and missile interception applications. Enhanced tracking accuracy and faster response cycles are improving combat readiness. Military modernization programs continue to prioritize high-frequency radar systems capable of supporting advanced weapon platforms.

Multi-Function Radar

Multi-Function Radar segment is projected to reach USD 7.3 billion by 2033, at a CAGR of 7.2% during the forecast period.

Multi-Function Radar is attracting strong investment in the Global Defense Radar market owing to increasing demand for integrated surveillance and tracking solutions. The ability to combine command, control, and targeting functions within a single architecture reduces operational complexity. Advanced software-defined radar technologies are further improving adaptability across diverse combat environments.

Others

Others segment is projected to reach USD 2 billion by 2033, at a CAGR of 3.7% during the forecast period.

Other radar types in the Global Defense Radar market are expanding through specialized mission requirements such as weather monitoring and terrain mapping. Customizable radar modules are supporting niche defense applications where operational flexibility is critical. Continued research investment is also encouraging innovation in compact and energy-efficient radar technologies.

By Component, the market is further divided into:

Antenna

Antenna segment is projected to reach USD 5 billion by 2033.

Antenna systems within the Global Defense Radar market are advancing through active electronically scanned array developments. Improved beam steering, reduced signal interference, and higher detection precision are strengthening radar performance. Defense contractors are also investing in lightweight and durable antenna materials to improve long-term operational reliability.

Transmitter

Transmitter segment is projected to reach USD 3.7 billion by 2033.

Transmitter units within the Global Defense Radar market are evolving with improved power efficiency and stronger frequency generation capabilities. The adoption of gallium nitride technology is increasing transmission performance while reducing energy consumption. Modern combat environments are creating demand for transmitters that can operate reliably under extreme conditions.

Receiver

Receiver segment is projected to reach USD 3.7 billion by 2033.

Receiver components within the Global Defense Radar market are improving signal sensitivity and filtering accuracy. Enhanced noise reduction systems are enabling clearer target identification in dense electromagnetic environments. Defense research programs are also focusing on digital receiver architectures to improve overall situational awareness.

Duplexer

Duplexer segment is projected to reach USD 1.3 billion by 2033.

Duplexer technology within the Global Defense Radar market is strengthening system protection by efficiently managing signal transmission and reception cycles. Future radar designs will incorporate compact duplexer units to reduce overall size and weight. High power tolerance will remain important for supporting uninterrupted radar performance during extended missions.

Others

Others segment is projected to reach USD 9.3 billion by 2033.

Other components within the Global Defense Radar market, including processors and power systems, are receiving steady investment through broader defense digital transformation initiatives. Advanced computing modules are enabling faster data interpretation and automated threat classification. Modular component design is also improving maintenance efficiency and overall lifecycle performance.

By Application, the Global Defense Radar market is divided as:

Air and Missile Defense

Air and Missile Defense segment is projected to grow at a CAGR of 5.7% during the forecast period.

Air and Missile Defense remains a major application area in the Global Defense Radar market, driven by rising ballistic missile threats and the development of hypersonic weapons. Layered defense architectures depend on high-speed detection and interception capability. National security strategies are therefore prioritizing radar upgrades to strengthen aerial defense coverage.

Intelligence, Surveillance and Reconnaissance

Intelligence, Surveillance and Reconnaissance segment is projected to grow at a CAGR of 5.6% during the forecast period.

Intelligence, Surveillance, and Reconnaissance applications in the Global Defense Radar market are benefiting from continuous monitoring requirements and data-centric military strategies. Persistent surveillance capability is supporting border management, battlefield observation, and counterterrorism operations. Integration with autonomous systems is further improving real-time intelligence generation.

Navigation and Weapon Guidance

Navigation and Weapon Guidance segment is projected to grow at a CAGR of 4.5% during the forecast period.

Navigation and Weapon Guidance applications in the Global Defense Radar market are strengthening with the need for accurate trajectory tracking and targeting precision. Modern combat systems increasingly rely on radar-guided platforms to improve strike effectiveness. Advanced calibration and signal processing technologies are essential for mission-critical accuracy.

Space Situation Awareness

Space Situation Awareness segment is projected to grow at a CAGR of 6.9% during the forecast period.

Space Situation Awareness is emerging as an important application in the Global Defense Radar market with the growth of satellite deployments and increasing orbital congestion. Ground-based radar arrays are being used to monitor debris movement and potential collision threats. Strategic defense planning is increasingly incorporating radar-based space surveillance systems to support secure satellite operations.

Others

Others segment is projected to grow at a CAGR of 5% during the forecast period.

Other applications within the Global Defense Radar market are progressing through emerging defense requirements such as disaster response coordination and critical infrastructure monitoring. Flexible radar solutions are also supporting dual-use security functions across selected operational environments. Long-term defense investment will sustain innovation in adaptive and resilient radar ecosystems.

By Region:

Based on geography, the Global Defense Radar market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Defense Radar Market is set to expand at a CAGR of 5.5% within the forecast period, reaching a market size (TAM) of USD 7.1 billion by the end of 2033.

In North America, rising defense budgets and sustained investment in advanced surveillance programs are supporting strong demand in the Defense Radar market.

In North America, increasing focus on border security and missile defense modernization is accelerating procurement of next-generation radar systems in the Defense Radar market.

In Europe, rising defense modernization programs, NATO-led preparedness initiatives, and increasing investment in integrated air and missile defense systems are supporting steady growth in the Defense Radar market.

In Asia Pacific, expanding naval capabilities and air defense upgrades are opening new opportunities for radar deployment across land, sea, and airborne platforms in the Defense Radar market.

In Asia Pacific, increasing naval capabilities and air protection enhancements open new avenues for radar deployment across land, sea, and airborne structures in the Global Defense Radar market.

Across the Middle East, Africa, and South America, rising safety worries, protection diversification efforts, and gradual infrastructure upgrades support constant expansion of the Global Defense Radar market.

Competitive Landscape and Strategic Insights

The global defense radar market plays a critical role in modern defense systems by supporting surveillance, threat detection, missile guidance, and airspace control. Radar technology remains essential to national defense strategies as countries strengthen border security, air defense networks, and maritime monitoring capabilities. Rising geopolitical tensions and increased investment in advanced naval and air defense systems are encouraging governments to modernize radar infrastructure. From ground-based surveillance to airborne early warning systems and naval radars, demand is increasing across multiple defense segments. Countries are not only upgrading existing systems but also investing in next-generation radar solutions that offer higher accuracy, longer detection range, and improved resistance to electronic interference.

Major companies continue to shape competition and innovation within the defense radar market. Leading players such as RTX Corporation, Northrop Grumman, and Lockheed Martin are investing heavily in research and development to strengthen radar performance and integration capabilities. European defense leaders including BAE Systems, Thales, Leonardo S.p.A., Saab AB, HENSOLDT AG, and Rheinmetall AG are also expanding their portfolios with advanced sensor systems and digital processing solutions. These companies are focused on multifunction radar platforms capable of detecting, tracking, and classifying multiple targets simultaneously, which improves overall battlefield awareness.

In North America and allied markets, companies such as L3Harris Technologies, Inc., Israel Aerospace Industries, Leonardo DRS, and ASELSAN A.Ş. are expanding their presence through contracts across land, naval, and airborne radar programs. Specialized radar providers including Terma A/S, CEA Technologies, Reutech Radar Systems, and Weibel Scientific A/S are also gaining visibility for high-performance technologies tailored to specific defense requirements. In Asia, manufacturers such as Hanwha Systems, Bharat Electronics Limited, Mitsubishi Electric Corporation, Toshiba Corporation, and Meteksan Defence continue to support domestic defense programs while also strengthening export-oriented radar capabilities.

Other important participants include Elbit Systems, ERA a.s., PIT-RADWAR S.A., INVAP, Echodyne Corp., Infinity Radar, Fortem Technologies, and Raddef. These companies specialize in compact radar systems, counter-drone detection, and software-driven upgrades that improve deployment flexibility and response speed. The market is moving toward active electronically scanned array systems and digital radar architectures that enable faster data processing and improved target discrimination. With defense budgets remaining stable in many countries, partnerships between governments and private companies will support steady market expansion and reinforce the role of radar systems in national security strategies.

Forecast and Future Outlook

Market size is forecast to rise from USD 14.9 billion in 2025 to over USD 22.9 billion by 2033.

Artificial intelligence integration will transform radar signal processing, enabling systems to identify stealth signatures within complex electromagnetic environments. Advances in quantum sensing research can also influence long-range detection accuracy over time, pushing radar performance beyond conventional limitations. Export partnerships and joint defense initiatives will support cross-border standardization, contributing to a more interconnected radar ecosystem aligned with allied defense frameworks. Through these developments, the Global Defense Radar market will evolve into a foundational technology layer supporting strategic deterrence, space security management, and digitally coordinated defense operations.

This research report categorizes the Defense Radar market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Defense Radar market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Defense Radar market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 5.5% from 2026 to 2033

Revenue Unit

USD billion

Sales Volume Unit

Units

Segmentation

By Platform, Product Type, Component, Application, and Region

By Region

North America (By Platform, Product Type, Component, Application, and Country)

United States

Canada

Mexico

Europe (By Platform, Product Type, Component, Application, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Platform, Product Type, Component, Application, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Platform, Product Type, Component, Application, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Platform, Product Type, Component, Application, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Emerging Segments and Regional Growth Potential

Key Strategic Recommendations

Competitive Benchmarking

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

Top players operating in the Defense Radar industry include RTX Corporation, Northrop Grumman, Lockheed Martin, BAE Systems, Thales, Leonardo S.p.A., Saab AB, Hensoldt AG, Rheinmetall AG, and L3Harris Technologies, Inc.

North America region dominates the market.

The Metastat Insights analysis shows that the North America Defense Radar market size is estimated to be USD 7.1 billion by 2033.

High lifecycle costs tied to sustainment, calibration, and mission software updates will hamper the market growth within the forecast period.

The Surveillance and Early Airborne Warning Radar is the leading type segment in the Global market.

Global Defense Radar market is estimated to reach USD 22.9 billion by 2033.

The Global Defense Radar market will grow at a CAGR of 5.5% over the forecast period (2026-2033).

The Metastat Insights study shows that the Global Defense Radar market size was USD 14.9 billion in 2025.

Air and missile defense modernization programs across land, sea, and air forces and Shift toward multi-function AESA architectures and software-defined radar upgrades are key driving factors, boosting the market.

Global Robotic Combat Vehicle (RCV) market size is valued at USD 761.5 million in 2025 and is projected to reach USD 1,297.8 million in 2033, at a CAGR of 6.9% from 2026 to 2033

Global Autonomous Drone Market size was USD 22.7 billion in 2025 and is projected to reach USD 92.8 billion in 2033, at a CAGR of 19.3% from 2026 to 2033.

US Aerospace Material Testing Service Market Size, Share by 2030

US Aerospace Material Testing Service Market valued at $126.8 million in 2023 and projected to reach $201.0 million by 2030

US Aerospace Material Testing Service Market, US Aerospace Material Testing Service Market Size, US Aerospace Material Testing Service Market Share, US Aerospace Material Testing Service Market Analysis, US Aerospace Material Testing Service Market Growth, US Aerospace Material Testing Service Market Trends, US Aerospace Material Testing Service Market Research Report, US Aerospace Material Testing Service Market Forecast, US Aerospace Material Testing Service, US Aerospace Material Testing Service Market Research, US Aerospace Material Testing Service Industry, US Aerospace Material Testing Service Market Segmentation, US Aerospace Material Testing Service Market Companies, United States Aerospace Material Testing Service Market