MARKET OVERVIEW

The global DBC ceramic substrate market, which is placed in the advanced materials and electronic packaging sector, will be a niche market devoted to substrates produced using the direct bonding of copper on ceramic materials. The technique, referred to as Direct Bonded Copper (DBC) technology, will play significant roles in high-performance electronic packages that require superior thermal conductivity, mechanical strength, and stable electrical insulation. The market will be heavily interlinked with applications where power electronics are subject to harsh thermal and electrical stresses, i.e., electric vehicles, industrial drives, renewable energy systems, rail transport, and aerospace. In the global DBC ceramic substrate market, the key materials utilized will be alumina (Al₂O₃), aluminum nitride (AlN), and silicon nitride (Si₃N₄).

Each of these ceramics will provide unique combinations of thermal characteristics, mechanical ruggedness, and cost-effectiveness for manufacturers to customize their products according to application-specific demands. Copper layers plated onto these ceramics will offer electrical paths while also enabling heat dissipation from high-power devices. This dual purpose will become the key value of DBC substrates across various markets. The extent of the global DBC ceramic substrate market will spread to encompass not only material science but also the production technologies and quality control procedures that guarantee product performance and reliability. Production of DBC substrates will entail tight control over thermal expansion coefficients, adhesion strength, and surface flatness.

These parameters will have a direct bearing on the reliability and longevity of the end power modules where the substrates are mounted. Market participants will invest in optimizing lamination methods and surface treatments to satisfy the technical requirements imposed by system integrators and component manufacturers. This market will also involve a differentiated and intricate supply structure. Suppliers will vary from vertically integrated firms that can manufacture both base ceramics as well as metallized substrates, to highly specialized firms that handle only the bonding processes. End-user needs in markets with well-established electronics manufacturing hubs, notably East Asia, North America, and selected areas of Europe, will influence supply chain dynamics.

Regional regulations of material safety, recycling, and energy consumption during manufacturing will also influence how manufacturers develop products and manage operations. Demand distribution in the global DBC ceramic substrate market will directly track high-power electronics usage trends. As companies look for components that can withstand higher temperatures and switching frequencies without degrading, the demand for high-strength packaging materials will increase. This market will indirectly serve those needs by making innovation in material choice and bonding top priority. The future architecture of this market will be impacted by performance metrics alone, however, and also by industry-specific reliability testing and certification standards. As power electronic systems become more sophisticated, Global DBC Ceramic Substrate market will modify their capability to accommodate increasingly smaller, efficient, and thermally robust devices. The market will serve as a technical foundation for electronic design and integration, facilitating innovation across industries requiring persistent performance under harsh operating conditions.

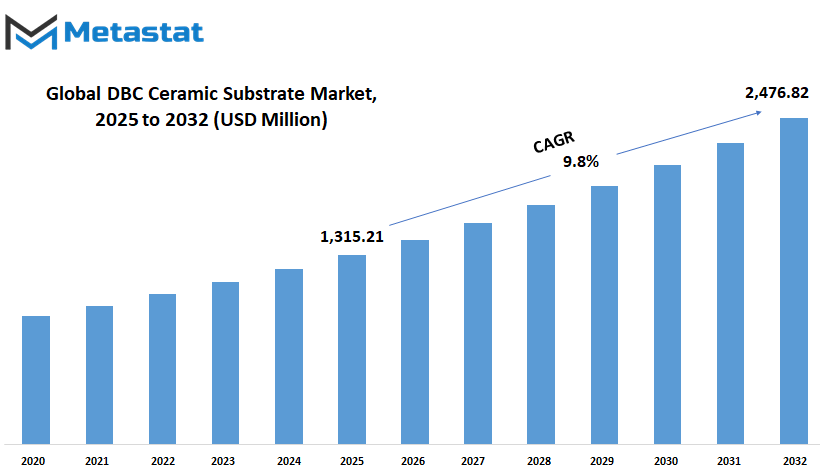

Global DBC ceramic substrate market is estimated to reach $2,476.82 Million by 2032; growing at a CAGR of 9.8% from 2025 to 2032.

GROWTH FACTORS

The global DBC ceramic substrate market is anticipated to witness significant changes in the years to come due to increased interest in electric vehicles and technological developments in industries. With increasing nations giving importance to cutting down emissions and sustainability, electric vehicle demand will continue to grow. These vehicles depend greatly on power modules that need to perform well under great stress, and DBC ceramic substrates have been found to be a reliable material in abetting these requirements. Their properties in heat management make them particularly appropriate for high-voltage applications, which are increasingly popular in both the auto and industrial markets. In high-performance applications where heat management is essential, conventional printed circuit board materials tend to lag behind.

DBC ceramic substrates provide a distinct benefit of even heat distribution, minimizing the possibility of overheating and enhancing the life of electronic components. This benefit is essential in contemporary technologies requiring long-term dependability and efficiency, particularly in applications where failure is not acceptable. As such, engineers and manufacturers are now turning towards these substrates as a reliable option in developing next-generation systems. In spite of these advantages, there are certain reasons that can hold up the broader adoption of these materials. One of the primary concerns is production cost.

Compared to more traditional materials, DBC ceramic substrates are still considerably higher to manufacture. This financial disparity makes it tough for smaller producers to implement them without suffering budget constraints. Another issue is the low compatibility across a broad range of materials. This makes it more challenging for designers to develop highly customized solutions, which is usually necessary in sophisticated applications that require more flexibility. Despite these limitations, there are encouraging indications suggesting development. The increasing trend towards renewable power sources like solar and wind necessitates efficient energy conversion and management systems. These tend to produce high levels of heat and operate at high voltages, posing a perfect complement to the use of DBC ceramic substrates.

In the same vein, the transition towards electric mobility for not just personal cars but also public transport and heavy machinery further contributes to the need for robust, heat-efficient materials. In the future, these changes offer a chance for business entities in the global DBC ceramic substrate market to invest and diversify into more effective means of production. With increasing demand for cleaner energy and more intelligent forms of transportation, the market will have new regions of application to tap into, making its future more promising by the day.

MARKET SEGMENTATION

By Type

One of the most common is the AlN DBC Ceramic Substrate. It has superior thermal conductivity and strength. When devices continue to shrink and become more powerful, the demand for materials that can dissipate heat well without deterioration will become greater. AlN substrates are capable of fulfilling these requirements and will be used more in systems that produce lots of heat or need to perform stably for long times. Another important type is the Al2O3 DBC Ceramic Substrate. While less conductive than AlN, it is still well liked for being lower cost and maintaining steady performance in standard operating conditions. In most devices where extreme temperatures are not an ongoing problem, Al2O3 offers a good balance of performance at a lower price. Manufacturers will still apply Al2O3 to most standard applications, and this will drive steady growth across various sectors. The global DBC ceramic substrate market will be influenced by developing innovations in manufacturing and material science as well. With investment in research by companies, we can expect newer iterations of these substrates that last longer under stress or provide improved durability with reduced cost. This type of innovation will determine how businesses select AlN or Al2O3 options on the basis of demand.

In the not-too-distant future, market decisions will be based on a mix of price, performance, and availability. Markets will not only consider what is best technically, but also what is sensible in supply terms and for use over time.

Therefore, AlN and Al2O3 forms will each have their own niche, for different applications depending on the project. The global DBC ceramic substrate market future will be determined by the extent to which these materials embrace evolving demands and technologies.

By Material Type

The global DBC ceramic substrate market is expected to experience sustained growth as technology continues to shape the way industries are run. Power electronics, where these substrates are employed, are increasingly gaining significance with the development of electric vehicles, renewable energy equipment, and industrial automation. With suppliers seeking greater performance and reliability, ceramic substrates that provide high thermal conductivity and mechanical strength will become increasingly popular. This consistent demand will drive industries to seek out new applications and enhance the quality of materials utilized. When examining the market on a material basis, a number of possibilities have significant influence.

Alumina is arguably one of the most popular materials because it is cheap and has good performance. It can be used in most applications that do not require incredibly high performance, so it is a reliable option for everyday electronics. Yet, as increasingly more businesses require stronger and more efficient components, Aluminum Nitride is gaining popularity. It has superior heat resistance and greater thermal conductivity, making it a promising candidate for future electronics. These capabilities will be useful in high-stress or hot systems such as electric vehicle batteries or wind power converters. Silicon Carbide is yet another substance that holds promise for the future. Although it can be more difficult to work with, its ability to handle high voltages and temperatures makes it a good match for demanding applications.

As industries look for ways to make systems more compact and energy-efficient, this material may become more common. While these types are already in use, others are being tested to meet growing needs. Developers continually look for possibilities that exhibit heat resistance, mechanical strength, and affordability. The global DBC ceramic substrate market will be guided by the demand for more efficient and intelligent power systems in the future. With increased clean energy and smart infrastructure, manufacturers will need substrates that are more reliable and durable. Those businesses within this sector will tend to spend more money on research to enhance the attributes of each material type.

They will also focus efforts on reducing the cost of production. Along the way, sectors like automotive, energy, and industrial automation will enjoy more durable and efficient devices. This trend towards better technology will only continue to drive the industry forward, making these substrates an integral component of electronics tomorrow.

By Thickness

The global DBC ceramic substrate market is likely to have a major contribution to the future of semiconducting industries that are dependent on sophisticated electronics. As technology keeps increasing its relevance in semiconducting industries and other sectors, the demand for materials that provide longevity, thermal resistance, and optimal performance is on the rise. DBC ceramic substrates have the capability to withstand high power and heat and are thus needed in a wide range of applications today. Electric vehicles to renewable energy systems, the material is increasingly being seen and needed for future development. One of the significant features of this market is the way the substrates are classified according to thickness.

These are categorized into three broad groups: thin, medium, and thick. Thin substrates that go up to a certain height are usually utilized in those compact systems where space-saving is essential. They are particularly common in portable electronics and miniature control units where performance is still required to be robust despite the confined space. With increasing devices that are being miniaturized and made more powerful, thin DBC ceramic substrates are also expected to become more popular. Meanwhile, medium thickness substrates are the middle ground solution. They are neither too strong nor too thick, so they become a versatile choice for most system types.

They are usually found in applications where size and strength coexist. As industries keep on demanding efficiency while balancing cost and performance, this in-between option might soon be more commonly used. It works well for both consumer products and industrial equipment, providing a solid base for electronics components. Dense DBC ceramic substrate are utilized primarily when there is a demand for a good mechanical support and excellent heat management. These are utilized in high-stress applications, including power converters or heavy-duty inverters. As emphasis continues to shift toward designing energy-efficient systems, this thicker type will become increasingly significant. It enables improved temperature control, resulting in longer lifespan and more dependable operation. Ahead, the global DBC ceramic substrate market future will rest in its ability to keep up with emerging challenges and increasing demands. Production innovations and improved combinations of materials are likely to make these substrates cheaper and even more efficient. With the development of new technologies, ranging from smart grids to electric transport, the contribution of DBC ceramic substrates will expand further, powering a future founded on reliability and efficiency in energy usage.

By Application

The global DBC ceramic substrate market will keep expanding as industries increasingly use high-technology materials for improved performance and strength. As technology advances, demand for substrates with the ability to withstand heat, support heavy electrical currents, and be reliable in harsh conditions will grow. DBC ceramic substrate are particularly renowned for carrying heavy currents while maintaining their thermal stability. This makes them a strong choice across different fields that require both strength and efficiency. In power electronics, they are already a go-to choice since they provide improved thermal performance compared to conventional materials. Components in this industry will need to shrink, be more efficient, and deliver more power. To make this possible, companies will keep selecting materials that maintain integrity at high temperatures. DBC ceramic substrates are already part of this process and will only grow more important in the future.

Within the automobile electronics market, the move towards electric and intelligent systems is increasing the demand for solid and compact electronic components. DBC ceramic substrates are particularly suitable to be utilized for applications in inverters, converters, and battery management systems. With the increasing electronification and atomization of cars, the demand for high-temperature and high-performance materials will increase. This will automatically direct more focus and investment to this sector.

Home appliances are also becoming intelligent and interconnected, usually featuring systems that require steady performance and heat control. DBC ceramic substrates enable product manufacturers to create products that are powerful and long-lasting. Washing machines, refrigerators, and air conditioners require control units that can withstand frequent use, and these substrates provide a means of creating them more efficiently.

CPV and aerospace applications require materials that will not be stressed out. Be it a solar system or a system deployed in an aircraft, the component's quality and reliability count a lot. DBC ceramic substrates are finding their application in these sectors since they provide predictable performance even in harsh conditions.

Other industries will soon begin experiencing the advantages of these materials as technologies continue to advance. From industrial equipment to new communication devices, DBC ceramic substrates will have increasing applications where performance and thermal resistance are vital. As more attention is directed toward efficiency and sustainability, this industry will keep pace, driven by innovation and expanding industrial requirements.

|

Report Coverage |

Details |

|

Forecast Period |

2025-2032 |

|

Market Size in 2025 |

$1,315.21 million |

|

Market Size by 2032 |

$2,476.82 Million |

|

Growth Rate from 2025 to 2032 |

9.8% |

|

Base Year |

2024 |

|

Regions Covered |

North America, Europe, Asia-Pacific Green, South America, Middle East & Africa |

REGIONAL ANALYSIS

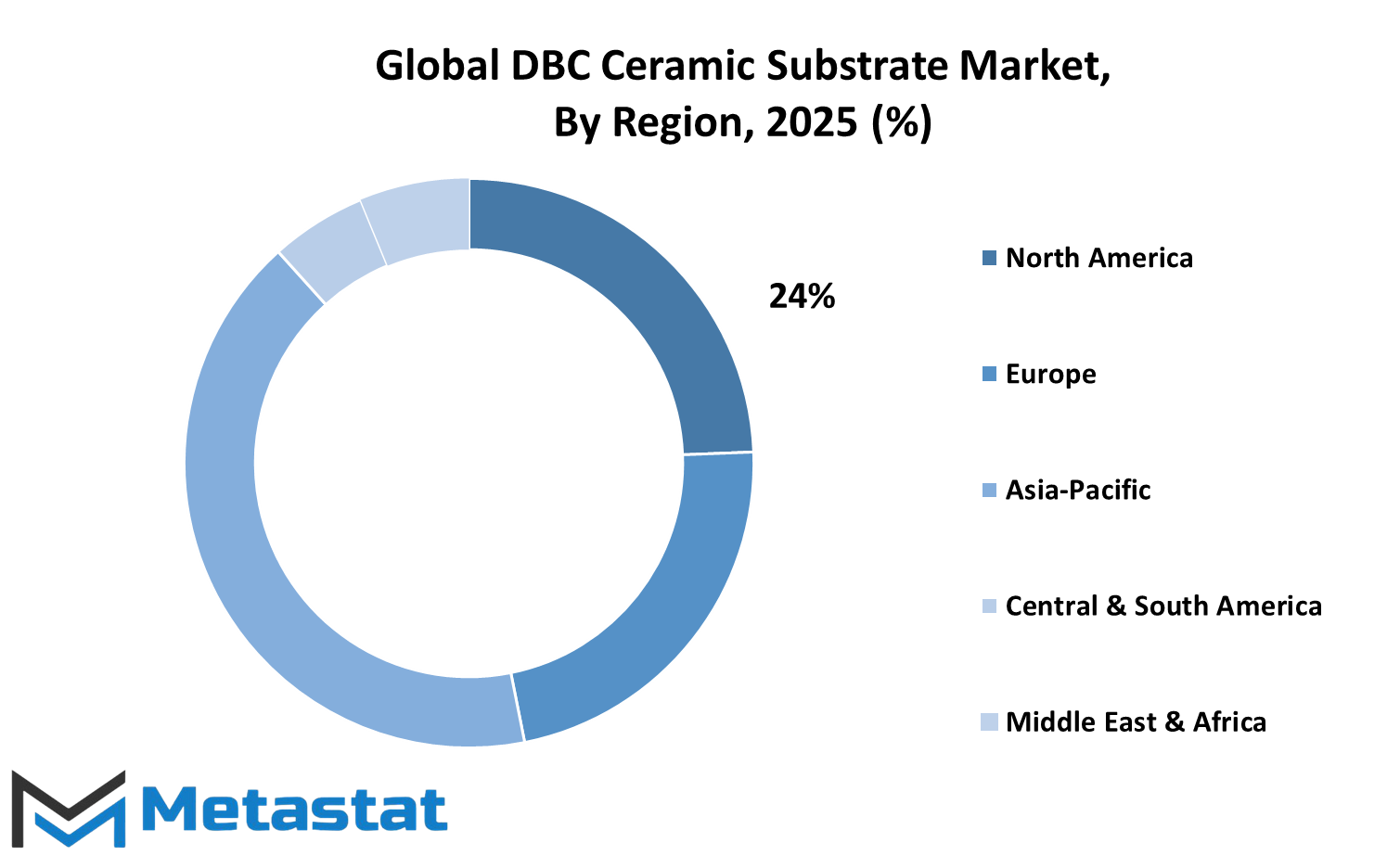

The global DBC ceramic substrate market will also experience transformations in the coming years, driven by increasing demand in industries and ongoing technological advancements. DBC ceramic substrates are renowned for their superior thermal conductivity as well as reliability and are thus applied in power electronics, automotive devices, and industrial machines. The higher the number of devices relying on effective heat management and longevity, the more crucial this market is likely to become. Ahead, applications such as electric vehicles and renewable energy systems will be more reliant on these materials. This transition is not just about addressing performance requirements but also enabling longer-lasting, more efficient solutions that can withstand greater power and temperatures. Geography heavily influences the trajectory of this market.

North America, encompassing the U.S., Canada, and Mexico, will continue to prioritize research and development, particularly in electric transportation and intelligent manufacturing. The U.S. will continue to be at the forefront of innovation, while Canada and Mexico facilitate this growth through both manufacturing and supply chain assistance. Europe, including the UK, Germany, France, Italy, and Rest of Europe, will tend towards cleaner technologies and energy efficiency. Germany will continue to be a dominant force in electric vehicle manufacture and industrial automation, which remain principal drivers of demand for ceramic substrates. Asia-Pacific, which includes India, China, Japan, South Korea, and Rest of Asia-Pacific, will become the most dynamic part of this market. China and Japan are already ahead in the production of semiconductors and will continue to invest in this sector.

India and South Korea too will increase, with an accelerating drive towards domestic production and innovation. This region's fast industrial growth and rising emphasis on electronics make it a hub of market activity. South America, comprising Brazil, Argentina, and the Rest of South America, will catch up gradually with the development of infrastructure and technology. In the meanwhile, the Middle East & Africa, the GCC Countries, Egypt, South Africa, and the Rest of the region will start to find the advantages of such materials, particularly in applications related to energy and transportation. As business moves toward intelligent systems and green technologies, the global DBC ceramic substrate market will be at the forefront of this change, enabling devices and systems that require strength and efficiency.

COMPETITIVE PLAYERS

The global DBC ceramic substrate market is gradually governing the electronic materials future by its distinguishing performance and reliability. With technology advancing day by day and rising demand for efficient and compact electronics, the position of DBC ceramic substrates becomes increasingly important. The materials are applied in power modules, automotive devices, and other high-frequency systems, possessing fine thermal conductivity as well as electrical insulation. With industries moving to more efficient and sustainable designs, this market is anticipated to remain relevant and experience substantial growth. In the future, the global DBC ceramic substrate market can be expected to gain from increasing demand in electric vehicles and renewable energy systems.

As governments and producers demand cleaner sources of energy and electric vehicles, power electronic materials must be robust, long-lasting, and able to dissipate heat without loss of performance. It is here that DBC ceramic substrates come into their own. They contribute to enhanced performance with safety and lifespan. Their application is not just for solar systems or cars; they are also crucial in industrial automation and other high-power devices where heat management is paramount. As regards who is at the forefront of innovation in this area, a number of firms are notable in terms of their research, production volumes, and ongoing investment. Competitive players like NGK Electronics Devices, Inc. and Ferrotec Corporation are characterized by persistent innovation and solid partnerships.

Zibo Linzi Yinhe High-tech Development Co., Ltd. and Maruwa Co., Ltd. are also recognized for their commitment to quality and cost-effectiveness. KCC Corporation and Tong Hsing Electronic Industries, Ltd. have retained solid positions by providing dependable solutions in diverse industries. Other significant contributors are Remtec, Inc. and Rogers Corporation, both of which have long-term industry experience and a firm commitment to innovation. Businesses such as Heraeus Electronics and Stellar Industries Corp continue to drive development with new materials and manufacturing methods. More recent names like Fujian Huaqing Electronic Material Technology Co., Ltd., Xiamen Innovacera Advanced Materials Co., Ltd, and Fuboon Technical Ceramics indicate good growth and their inclusion indicates growing competition and broader geographical reach.

These companies are not just fulfilling present demand but are also gearing up for the future. The global DBC ceramic substrate market will probably continue to expand as these businesses continue to evolve, develop improved solutions, and react to new requirements. As more electronic systems need improved heat management and reliability, this market is poised to be an essential aspect of upcoming technology innovation.

DBC Ceramic Substrate Market Key Segments:

By Type

- AlN DBC Ceramic Substrate

- Al2O3 DBC Ceramic Substrate

By Material Type

- Alumina

- Aluminum Nitride

- Silicon Carbide

- Others

By Thickness

- Thin (up to 0.5 mm)

- Medium (0.5 mm to 1 mm)

- Thick (above 1 mm)

By Application

- Power Electronics

- Automotive Electronics

- Home Appliances and CPV

- Aerospace

- Others

Key Global DBC Ceramic Substrate Industry Players

- NGK Electronics Devices, Inc.

- Zibo Linzi Yinhe High-tech Development Co., Ltd.

- KCC Corporation

- Tong Hsing Electronic Industires, Ltd.

- Maruwa Co., Ltd.

- Remtec, Inc.

- Ferrotec Corporation

- Rogers Corporation

- Heraeus Electronics

- Stellar Industries Corp

- Fujian Huaqing Electronic Material Technology Co.,Ltd

- Xiamen Innovacera Advanced Materials Co., Ltd

- Fuboon Technical Ceramics

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential

US: +1 3023308252

US: +1 3023308252