Care Management Solutions Market By Delivery Mode (On-premise and Cloud-based), By Component (Software and Services), By Application (Disease Management, Case Management, Utilization Management, and Other Applications), By End User (Healthcare Providers, Healthcare Payers, and Others), Industry Analysis, Size, Share, Growth, Trends, and Forecast, 2033

Report ID

MSI-4310

Published

October 23, 2025

Pages

255 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Global Care Management Solutions Market- Comprehensive Data-Driven Market Analysis & Strategic Outlook

The global care management solutions market started as a reaction to an increasing sophistication of healthcare systems that could not maintain cost, efficiency, and patient outcomes in balance. The industry was initially stimulated by a simple demand to manage patient information, eliminate redundancy in medical records, and assist care givers in communicating more efficiently. Initial software models were primitive, typically designed for in-house hospital usage, concentrating primarily on monitoring chronic diseases and organizing coordination among general practitioners and specialists. As the healthcare systems globally began adopting digital change, the market transformed into an organized segment of health IT, connecting payers, providers, and patients by integrated digital platforms.

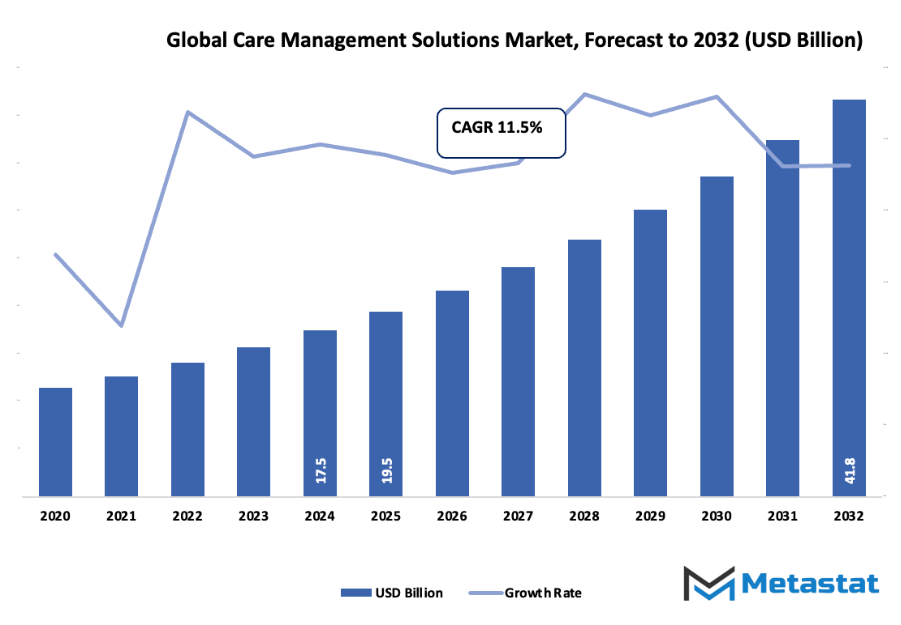

Global care management solutions market worth about USD 19.5 billion in 2025, expanding at a CAGR of about 11.5% during 2032, with the potential to extend beyond USD 41.8 billion.

On-premise contribute close to 47.3% market share, pushing innovation and broadening applications with rigorous research.

Aging Population Demands and Value-Based Care Models are the top trends driving growth.

Opportunities present: Telehealth Integration

Key insight: The market is set to grow exponentially in value over the next decade, highlighting significant growth opportunities.

A defining moment arrived when healthcare providers realized that electronic health records alone were not enough to manage the full continuum of care.

This recognition pushed developers to create systems capable of predictive analytics, patient engagement, and remote monitoring. The advent of cloud computing during the 2010s was another milestone moment that made care management platforms more scalable and secure. Governments across different regions started promoting interoperability standards, which instigated cooperation among insurers, hospitals, and technology vendors. This incremental alignment formed a more unified digital ecosystem that went beyond hospital walls. Over the last few years, consumer behaviour has begun to shift the direction of the worldwide Care Management Solutions market. Patients will increasingly demand personalized care plans, accelerated communication with providers, and openness in treatment choices. Consequently, organizations will concentrate on creating products that close the gap between hospital-based clinical care and home-based monitoring for health. Artificial intelligence will increasingly play a part in anticipating patient threats and providing guidance on intervention in advance of worsening conditions. Regulatory systems will also change, focusing on data privacy and fair access to technologies of care.

The market's future will hinge on partnership among governments, private health facilities, and digital innovators to develop a smooth exchange of information that enables improved outcomes. From its humble start as data management software to a worldwide network of smart health solutions, the market will be a testament to how technology can transform the care experience from beginning to end.

Market Segments

The global care management solutions market is mainly classified based on Delivery Mode, Component, Application, End User.

By Delivery Mode is further segmented into:

On-premise: The market under the on-premise delivery mode enables organizations to store and maintain data in internal servers. This solution offers enhanced security and control over sensitive patient data. It is used by large healthcare facilities that process substantial amounts of confidential data and provide direct control and low reliance on external networks.

Cloud-based: The cloud-based portion of the global care management solutions market is all about flexibility, scalability, and ease of access. It allows healthcare facilities to share information from any location, lowering the cost of infrastructure and making it easier to share information among professionals. This system allows for real-time collaboration and updates, enhancing overall operating efficiency across health systems.

By Component the market is divided into:

Software: The software component of the global care management solutions market is intended to automate clinical and administrative functions. It facilitates patient information management, scheduling, and reporting in addition to improving data accuracy. These electronic tools enable enhanced decision-making and enhanced workflow efficiency within healthcare organizations, producing better patient outcomes.

Services: The services segment of the global care management solutions market is aimed at support, consulting, and system integration. These services are designed to make healthcare institutions effectively implement and utilize care management software. Training, maintenance, and technical support are central characteristics that enable organizations to attain seamless operation and full utilization of digital care management platforms.

By Application the market is further divided into:

Disease Management: The global care management solutions market of disease management seeks to offer organized programs that assist in the monitoring and treatment of chronic diseases. It assists healthcare providers in monitoring the progress of patients, providing timely interventions, and enhancing adherence to treatment. This helps in minimizing readmission to hospitals and enhancing the quality of care for patients.

Case Management: The case management division of the global care management solutions market helps healthcare professionals coordinate the care of patients across services. It aims at enhancing communication among caregivers, optimizing the use of available resources, and ensuring continuity of care. This results in increased patient satisfaction and improved healthcare resource use.

Utilization Management: The utilization management segment of the worldwide Care Management Solutions market provides assurance that there is proper use of healthcare resources as well as their efficient use. It facilitates review of medical necessity, refining treatment plans, and cost control without adversely affecting the quality of patient care. This creates openness and accountability among healthcare systems.

Other Applications: Some other uses in the Care Management Solutions market globally are wellness programs, psychological support, and management of preventive care. These uses are focused on improving patient overall well-being and promoting proactive management of health. They help lower long-term healthcare expenses and enhance the efficiency of healthcare provision.

By End User the global care management solutions market is divided as:

Healthcare Providers:The healthcare providers segment of the global care management solutions market includes hospitals, clinics, and care centers. These organizations use care management tools to coordinate treatment plans, manage patient data, and ensure continuity of care. Such solutions support improved patient engagement, streamlined workflows, and data-driven decision-making in healthcare delivery.

Healthcare Payers:The healthcare payers segment of the global care management solutions market consists of insurance companies and government agencies. These entities use Care Management Solutions to monitor healthcare expenses, evaluate treatment efficiency, and manage claims. The tools assist in improving cost transparency, minimizing fraudulent claims, and enhancing service quality for members.

Others:The others segment within the global care management solutions market includes research organizations, employers, and community health programs. These groups use care management tools to analyze health trends, promote wellness initiatives, and support policy development. Their involvement helps in building a more efficient and patient-centered healthcare environment.

Forecast Period

2025-2032

Market Size in 2025

$19.5Billion

Market Size by 2032

$41.8Billion

Growth Rate from 2025 to 2032

11.5%

Base Year

2025

Regions Covered

North America, Europe, Asia-Pacific, South America, Middle East & Africa

By Region:

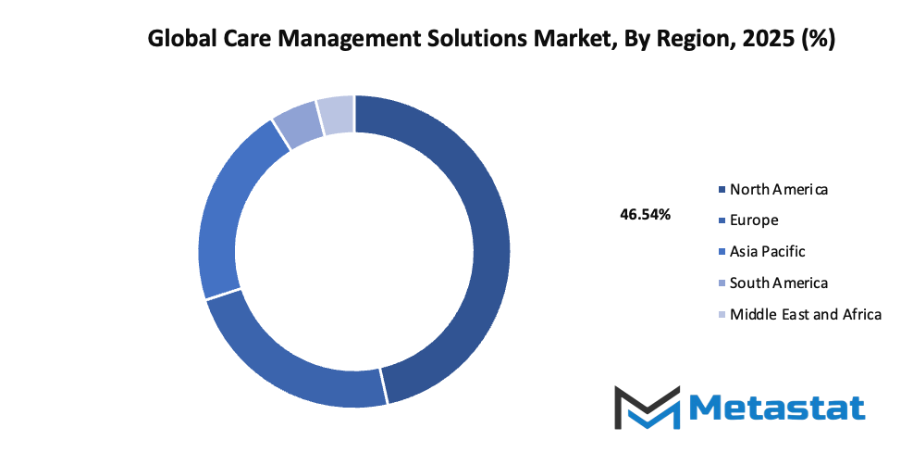

Based on geography, the global care management solutions market is divided into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

North America is further divided into the U.S., Canada, and Mexico, whereas Europe consists of the UK, Germany, France, Italy, and the Rest of Europe.

Asia-Pacific is segmented into India, China, Japan, South Korea, and the Rest of Asia-Pacific.

The South America region includes Brazil, Argentina, and the Rest of South America, while the Middle East & Africa is categorized into GCC Countries, Egypt, South Africa, and the Rest of the Middle East & Africa.

Growth Drivers

Aging Population Demands:The growing number of elderly individuals is creating a higher need for efficient care coordination. The global care management solutions market is addressing age-related conditions such as chronic illnesses and mobility challenges. These solutions help healthcare systems offer personalized support, continuous monitoring, and preventive care for elderly patients, reducing hospital readmissions.

Focus on Value-Based Care Models:Healthcare systems are shifting toward value-based care to improve quality while reducing costs. The global care management solutions market is supporting this change by enabling data-driven insights, improving patient engagement, and helping providers track performance outcomes. This model rewards quality treatment, encouraging long-term wellness and efficient care delivery.

Challenges and Opportunities

Data Security Concerns:As digital platforms handle sensitive patient data, the global care management solutions market must prioritize strong cybersecurity measures. Breaches can lead to loss of trust and legal complications. Advanced encryption, multi-level authentication, and regular audits are essential to protect medical records and ensure safe digital interactions across care networks.

Regulatory Compliance Challenges:Different regions enforce various healthcare regulations, creating complexity for solution providers. The global care management solutions market must follow strict standards related to data protection, patient rights, and medical accuracy. Compliance requires regular updates, staff training, and continuous monitoring to ensure all digital systems meet legal and ethical requirements.

Opportunities

Telehealth Integration:Telehealth advancements are creating major opportunities for the global care management solutions market. Integration with virtual care platforms allows real-time consultations, remote monitoring, and faster follow-ups. This digital connection improves patient convenience, reduces hospital visits, and helps healthcare providers maintain consistent contact with patients for ongoing treatment and preventive care.

Competitive Landscape & Strategic Insights

The global care management solutions market is entering a phase of rapid transformation, where innovation and competition are reshaping how healthcare organizations operate and deliver value. The industry is a mix of both international industry leaders and emerging regional competitors. Important competitors include EXL Service Holdings, Inc., Epic Systems Corporation, Allscripts Healthcare Solutions, Inc., Cognizant Technology Solutions, Hinduja Global Solutions Limited, Optum, Inc., Medecision, Inc., I2I Systems Inc., Koninklijke Philips N.V., IBM Corporation, Inovalon, HealthEC, LLC, Health Catalyst, ZeOmega, and Lightbeam Health Solutions. These companies are driving significant progress in data analytics, patient engagement, and care coordination, all of which are central to improving healthcare outcomes and reducing costs.

The increasing demand for digital health systems is leading to a future where healthcare management will be more interconnected and data-driven. The use of artificial intelligence, predictive analytics, and cloud technology is expected to expand, allowing for better identification of patient needs and timely intervention. This will help healthcare providers move from reactive care toward a more preventive and personalized model. As patient data becomes more accessible and securely managed, the ability to predict health risks before they escalate will improve, leading to better patient experiences and lower hospital readmission rates.

Market competition is expected to intensify as both established corporations and smaller firms continue to develop new platforms that simplify complex workflows. Large companies such as IBM Corporation and Koninklijke Philips N.V. are likely to focus on scaling global digital health ecosystems, integrating advanced analytics with clinical decision-making tools. Meanwhile, emerging players may focus on flexible and specialized software that targets specific healthcare challenges in developing markets. This balance between large-scale integration and targeted innovation will define the industry’s future growth pattern.

Regulatory support for digital transformation in healthcare will also play a major role in shaping the next generation of Care Management Solutions. Governments across different regions are increasingly prioritizing patient data interoperability, cybersecurity, and telehealth infrastructure. This will open opportunities for technology providers to design systems that align with global health standards and provide seamless care coordination across multiple platforms. The focus will shift from merely collecting data to actively using it to improve health outcomes and support clinical decisions in real time.

The growing emphasis on patient-centered care will push organizations to develop solutions that are not only technologically advanced but also user-friendly and accessible. Mobile health applications and remote monitoring systems will continue to grow in importance, enabling continuous communication between patients and healthcare teams. This will create a healthcare environment that is more responsive, efficient, and adaptable to different patient populations.

Market size is forecast to rise from USD 19.5 billion in 2025 to over USD 41.8 billion by 2032. Care Management Solutions will maintain dominance but face growing competition from emerging formats.

Looking ahead, the Care Management Solutions market will continue to evolve as digital innovation, collaboration, and strategic partnerships shape the future of healthcare delivery. The leading and emerging companies in this field will play a vital role in building systems that connect data, providers, and patients in meaningful ways. With ongoing technological progress and a growing global focus on quality care, the industry is positioned for sustained growth and long-term improvement in health management efficiency.

Report Coverage

This research report categorizes the global care management solutions market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the global care management solutions market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the global care management solutions market.

Care Management Solutions Market Key Segments:

By Delivery Mode

On-premises

Cloud-based

By Component

Software

Services

By Application

Disease Management

Case Management

Utilization Management

Other Applications

By End User

Healthcare Providers

Healthcare Payers

Others

Key Global Care Management Solutions Industry Players

Former, on-going, and projected market analysis in terms of volume and value

Assessment of niche industry developments

Market share analysis

Key strategies of major players

Emerging segments and regional growth potential

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

Global Care Management Solutions market is valued at $19.5 billion in 2025.

Global Care Management Solutions market is estimated to grow with a CAGR of 11.5% from 2025 to 2032.

Global Care Management Solutions market is estimated to reach $41.8 billion by 2032.

Top players operating in the Care Management Solutions industry includes EXL Service Holdings, Inc., Epic Systems Corporation, Allscripts Healthcare Solutions, Inc., and Others.

US Healthcare Payment Solutions Market Size, Share, Trends, 2033

US Healthcare Payment Solutions market size is valued at USD 34.2 million in 2025 and is projected to reach USD 56.9 million in 2033, at a CAGR of 6.6% from 2026 to 2033

US Healthcare Payment Solutions Market, US Healthcare Payment Solutions Market Size, US Healthcare Payment Solutions Market Share, US Healthcare Payment Solutions Market Analysis, US Healthcare Payment Solutions Market Growth, US Healthcare Payment Solutions Market Trends, US Healthcare Payment Solutions Market Research Report, US Healthcare Payment Solutions Market Forecast, US Healthcare Payment Solutions, US Healthcare Payment Solutions Market Research, US Healthcare Payment Solutions Industry, US Healthcare Payment Solutions Industry Report, US Healthcare Payment Solutions Market Data, US Healthcare Payment Solutions Statistics, US Healthcare Payment Solutions Market Statistics, US Healthcare Payment Solutions Industry Trends, US Healthcare Payment Solutions Market Report, US Healthcare Payment Solutions Market Trends, US Healthcare Payment Solutions Market News, US Healthcare Payment Solutions Forecasts, US Healthcare Payment Solutions Market Intelligence Report

Electronic Medical Records market Size, Share, Trends, 2033

Global Electronic Medical Records market size is valued at USD 20.1 billion in 2025 and is projected to reach USD 32.5 billion in 2033, at a CAGR of 6.2% from 2026 to 2033

Electronic Medical Records Market, Electronic Medical Records Market Size, Electronic Medical Records Market Share, Electronic Medical Records Market Analysis, Electronic Medical Records Market Growth, Electronic Medical Records Market Trends, Electronic Medical Records Market Research Report, Electronic Medical Records Market Forecast, Electronic Medical Records, Electronic Medical Records Market Research, Electronic Medical Records Industry, Electronic Medical Records Market Data, Electronic Medical Records Statistics, Electronic Medical Records Market Statistics, Electronic Medical Records Industry Trends

AI Diagnostics in Ophthalmology Market Size, Share, Trends, 2033

Global AI Diagnostics in Ophthalmology market is valued at USD 286.8 million in 2025 and is projected to reach USD 3,496.1 million by 2033, at a CAGR of 36.7% from 2026 to 2033

AI Diagnostics in Ophthalmology Market, AI Diagnostics in Ophthalmology Market Size, AI Diagnostics in Ophthalmology Market Share, AI Diagnostics in Ophthalmology Market Analysis, AI Diagnostics in Ophthalmology Market Growth, AI Diagnostics in Ophthalmology Market Trends, AI Diagnostics in Ophthalmology Market Research Report, AI Diagnostics in Ophthalmology Market Forecast, AI Diagnostics in Ophthalmology, AI Diagnostics in Ophthalmology Market Research, AI Diagnostics in Ophthalmology Market Industry

US Newborn Screening Technologies Market Size Report, 2032

US Newborn Screening Technologies market is estimated to reach $407.3 million in 2025 with a CAGR of 7.7% from 2025 to 2032

US Newborn Screening Technologies Market, US Newborn Screening Technologies Market Size, US Newborn Screening Technologies Market Share, US Newborn Screening Technologies Market Analysis, US Newborn Screening Technologies Market Growth, US Newborn Screening Technologies Market Trends, US Newborn Screening Technologies Market Research Report, US Newborn Screening Technologies Market Forecast, US Newborn Screening Technologies, US Newborn Screening Technologies Market Research, US Newborn Screening Technologies Market Industry