Global Carbon Management System Market - Comprehensive Data-Driven Market Analysis & Strategic Outlook

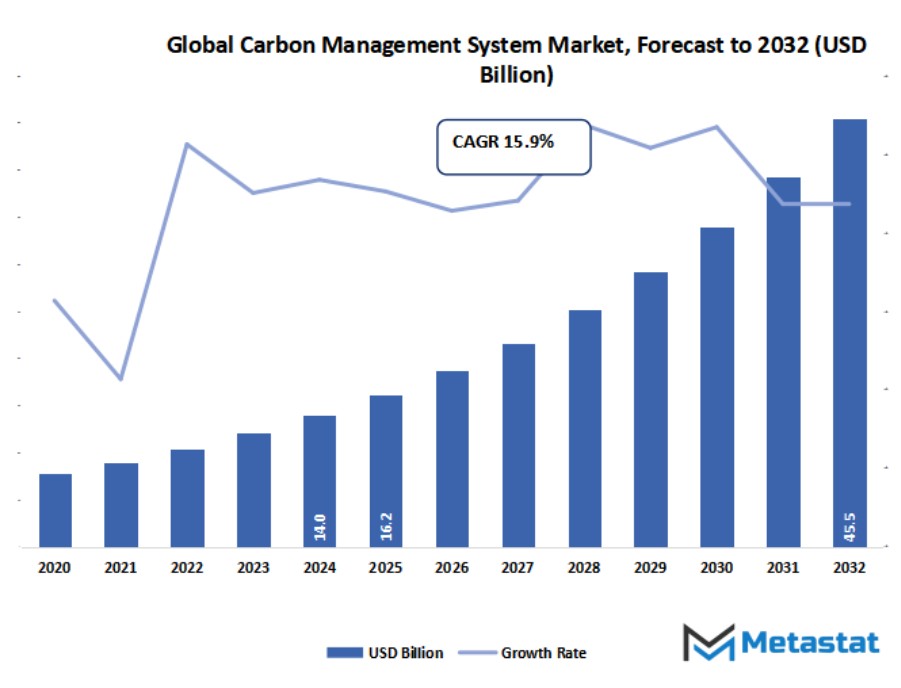

- Global carbon management system market valued at approximately USD 16.2 Billion in 2025, growing at a CAGR of around 15.9% through 2032, with potential to exceed USD 45.5 Billion.

- Software account for a market share of 74.2% in 2024, driving innovation and expanding applications through intense research.

- Key trends driving growth: Rising global emphasis on sustainability and net-zero targets, Stringent government regulations on carbon emissions reporting

- Opportunities include Integration of AI and IoT in emission tracking creates new opportunities

- Key insight: The market is set to grow exponentially in value over the next decade, highlighting significant growth opportunities.

Market Background & Overview

The global carbon management system market and its sector will keep pushing ahead of conventional fences, evolving into a sector where technology, responsibility, and innovation will crossroads in a manner that redefines the way businesses are conducted. It will no longer be limited to reporting within organizations or regulatory requirements but will stretch to wider landscapes where openness and stakeholder trust will be a part of it. The sector will extend to regions that link with corporate plans, long-term investments, and product and service design that is constructed based on sustainability at its heart.

Since new criteria and standards will be established globally, the global carbon management system market will not just deal with compliance but will become a decision-making guide for industries. It will drive supply chain action, investment decisions, and consumer attitude, transcending far beyond a technical application to be a basis for how companies will represent value. Digital platforms, sophisticated data systems, and networked solutions will enable companies to measure and present progress, broadening the scope from a limited operational function to a central element of corporate branding.

Market Segmentation Analysis

The global carbon management system market is mainly classified based on Offering, Deployment Mode, Application, End-User.

By Offering is further segmented into:

- Software - Software offerings in the global carbon management system market will be more sophisticated, providing predictive analysis and real-time tracking of carbon traces. Upcoming technologies will emphasize combining artificial intelligence and automation to scrutinize environmental data in order to assist industries in mitigating emissions more efficiently and making choices that are aligned with sustainability goals.

- Services - Services within the global carbon management system market will become increasingly important as companies require guidance for compliance and strategic planning. Advisory, training, and integration of systems will be the backbone of service provision. Demand in the future will be biased toward end-to-end solutions that facilitate seamless uptake and quantifiable outcomes in industries across the globe.

By Deployment Mode the market is divided into:

- Cloud-Based - Cloud deployment in the global carbon management system market will grow based on its flexibility and accessibility. The future will be driven by companies focusing on cost-effectiveness, remote access, and real-time collaboration. Cloud platforms will also enable companies to consolidate global data, allowing them to respond to carbon reduction requirements more quickly.

- On-Premises - On-premises installation in the global carbon management system market will remain appealing to industries that need higher levels of control on data. This method will be appreciated by industries handling sensitive operations. Future application will be on hybrid models that combine the security of on-site systems with cloud capabilities' flexibility.

By Application the market is further divided into:

- Energy - Energy use within the global carbon management system market will meet the increasing need for cleaner energy supply. Future systems will monitor carbon intensity through the energy supply chain and maximize the integration of renewable energy. These technologies will inform policy-making and encourage investment in carbon-reducing technologies.

- Greenhouse Gas Management - Greenhouse gas administration will continue to be at the heart of the market. Sophisticated systems will monitor emissions throughout various production and transportation phases. The future will focus on truthful reporting, transparency, and accountability, which will hold companies accountable for meeting international climate objectives and helping firms become carbon neutral.

- Air Quality Management - Air management will expand in the market as urbanization poses pollution issues. Future systems will monitor pollutants at a micro level and provide predictive models to avoid risks. Governments and companies will adopt these systems to create healthier environments and form data-based sustainability plans.

- Sustainability - Sustainability usage in the market will help organizations develop long-term plans that harmonize growth with environmental stewardship. Future systems will combine sustainability metrics and financial objectives so that carbon reductions are not viewed as a cost but as an innovation and efficiency driver.

- Others - Other uses within the global carbon management system market will be research, education, and policy enforcement. Future innovations will reach into carbon trading and offset validation. These uses will promote greater awareness and inspire cooperative efforts in reaching carbon targets in many sectors and communities.

By End-User the global carbon management system market is divided as:

- Oil and Gas - The oil and gas industry will remain a prominent adopter of the global carbon management system market. Upcoming systems will monitor emissions in extraction, refining, and distribution, encouraging more environmentally friendly practices. Digital technologies will lead the industry in aligning demand with agreements to lower carbon production.

- Manufacturing - Manufacturing will continue to be a key end-user in the market. Future solutions will track emissions at all stages of production, from the source of raw materials to finished product. Adoption will move towards more sustainable manufacturing paradigms that reduce environmental footprint without sacrificing efficiency and competitiveness in global markets.

- Healthcare - Healthcare solutions in the market will target hospital, laboratory, and pharma production emissions. Upcoming systems will monitor waste management and energy consumption, enabling green hospital projects. Healthcare services will be aligned with overall sustainability goals without interfering with core operations.

- IT and Telecom - The IT and telecom industry will drive the market by virtual innovation and infrastructure. Next-era structures will maximize energy performance in statistics facilities and networks and minimize emissions, permitting worldwide connectivity. There might be a focus on growing environmentally pleasant digital ecosystems that enable sustainable improvement.

- Power and Utilities - Utilities and energy will stay a leading segment within the market. Future systems will assist screen carbon depth in electricity era and shipping. As renewable resources see increasing adoption, these answers will help successfully combine sun, wind, and different smooth strength into the present-day grids.

- Transportation and Logistics - Logistics and transportation will spur adoption within the market because it will become vital to song emissions. New systems will monitor automobile emissions, lessen gas consumption, and promote adoption of electrical automobiles. This technology will revolutionize global deliver chains by way of placing a stability between performance and environmental stewardship.

- Construction and Infrastructure - Construction and infrastructure will embody technology of the market to limit emissions in production tasks. Next-generation systems will monitor material sourcing, energy consumption, and construction waste. Such tools will propel companies toward sustainable urban growth while responding to increased global demand for infrastructure.

- Others - Other sectors to embrace solutions from the global carbon management system market include agriculture, education, and government. Future application will reach policy enforcement, sustainability education, and rural development. Such applications will motivate communities and institutions to make proactive contributions towards reducing carbon over the long term.

|

Forecast Period |

2025-2032 |

|

Market Size in 2025 |

$16.2 Billion |

|

Market Size by 2032 |

$45.5 Billion |

|

Growth Rate from 2025 to 2032 |

15.9% |

|

Base Year |

2024 |

|

Regions Covered |

North America, Europe, Asia-Pacific, South America, Middle East & Africa |

By Region:

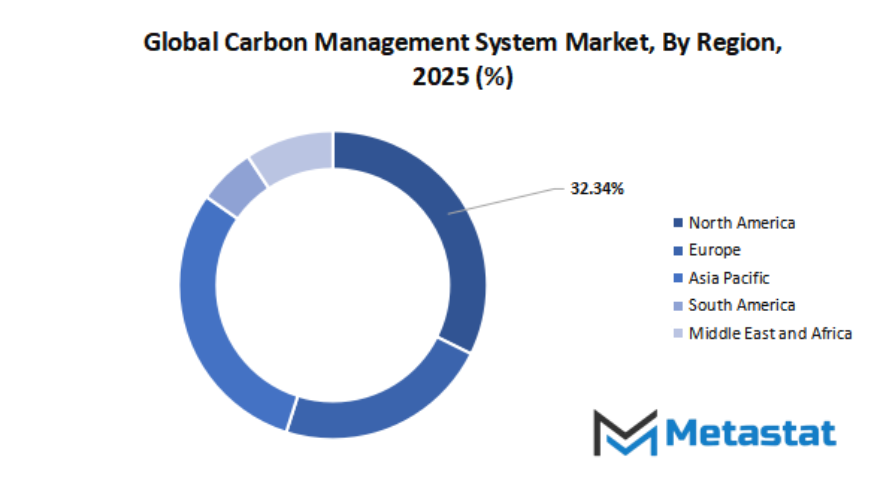

- Based on geography, the global carbon management system market is divided into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

- North America is further divided into the U.S., Canada, and Mexico, whereas Europe consists of the UK, Germany, France, Italy, and the Rest of Europe.

- Asia-Pacific is segmented into India, China, Japan, South Korea, and the Rest of Asia-Pacific.

- The South America region includes Brazil, Argentina, and the Rest of South America, while the Middle East & Africa is categorized into GCC Countries, Egypt, South Africa, and the Rest of the Middle East & Africa.

Market Dynamics

Growth Drivers:

- Rising global emphasis on sustainability and net-zero targets - The global carbon management system market will preserve growing as agencies globally align with sustainability targets and net-0 aims. Companies will put into effect sophisticated structures to track emissions, limit carbon footprints, and meet climate commitments. This transition will assure long-time period market boom and mass adoption.

- Stringent government regulations on carbon emissions reporting - The global carbon management system market will expand as governments impose tighter policies that demand effective carbon reporting. Firms will continue to implement organized solutions in order to evade fines and prove accountability. Regulatory systems over time will become tighter, so good carbon management systems will be key to remaining compliant and making operational performance transparent.

Restraints & Challenges:

- High implementation and maintenance costs limit adoption - The global carbon management system market will be challenged by high installation and maintenance costs. Small- and medium-sized firms can expect to find adoption challenging, which would decelerate the rate of penetration. Affordability will, in the future, be a determining factor, calling for scalable technologies that optimize efficiency with cost-effectiveness.

- Lack of standardization in carbon measurement frameworks - The market will face challenges due to a lack of globally accepted carbon measurement systems. Varying data collection and reporting mechanisms will lead to uncertainty for organizations. This challenge will persist until such systems become globally adopted, impairing cross-border collaboration and leading to complexities in tracking emissions accurately.

Opportunities:

- Integration of AI and IoT in emission tracking creates new opportunities - The global carbon management system market will gain loads through incorporating AI and IoT technology into emissions tracking. Predictive analytics and automated sensors will improve facts accuracy and choice making. Next-technology systems will development in the direction of real-time tracking, growing smarter, greater efficient solutions for companies trying to gain sustainability desires.

Competitive Landscape & Strategic Insights

The global carbon management system market is molding itself into the most significant domain for government and industries as the need for emissions reductions and climate objectives increases. Organizations are being scrutinized more than ever to monitor, manage, and reduce their carbon footprint, something that has fostered robust demand for sophisticated solutions capable of processing the management of data collection, monitoring, reporting, and compliance. The market is not exclusive to a single group of providers since it unites established global corporations and new regional entrants who are coming in with new platforms and fresh ideas. The blend of established know-how and emerging innovation makes the industry very dynamic and competitive.

Eminent technology leaders are taking center stage in this market by providing end-to-end systems that merge efficiency with scalability. Businesses such as IBM Corporation, SAP SE, Microsoft Corporation, and Salesforce.com Inc. have played a key role in developing systems that enable organizations to incorporate carbon tracking into their normal workflow. They provide credibility and wide coverage since they can deal with multinational clients that have complicated reporting obligations. Meanwhile, Schneider Electric SE and ENGIE Impact are adding value by merging their expertise in energy systems with digital platforms that assist businesses in shifting to sustainable practices. They point out how big business is repositioning itself as indispensable partners to carbon-cutting strategies.

In addition to the industry titans, there is a rapidly expanding category of specialist providers who are devoting themselves entirely to managing carbon. Companies like Persefoni AI, Watershed Technology Inc., Greenstone+ Ltd, and Sphera Solutions are increasingly recognized for their specialized software that ensures accurate carbon accounting and scenario analysis. Such platforms tend to be popular among businesses looking for exact measurement and forecasting abilities, which allows them to take greater control of their sustainability goals. Newer names such as Terrascope Pte Ltd, Emitwise, Greenly, Sweep SAS, and Carbmee GmbH indicate how regional innovation is starting to affect international practices. They ensure agility, personalization, and digital-first solutions that frequently disrupt conventional methods.

Competitor diversity in this market implies that purchasers have more choices than ever before. Firms can opt for general software ecosystems from the world leaders or more focused platforms from upstart players, based on their resources and requirements. This diversity is likely to keep fueling innovation, as both sides urge the other to enhance features, streamline processes, and enhance compliance capabilities. In the next couple of years, the global carbon management system market will grow further with the help of global climate pacts, regulation compressing, and companies pledging for sustainability. With prominent companies such as Johnson Matthey Plc and LG Chem Ltd in other sectors already illustrating how transitions go green reshape markets, the sector of carbon management will also take the same route of strong growth, being driven by technology and policy.

Forecast & Future Outlook

- Short-Term (1–2 Years): Recovery from COVID-19 disruptions with renewed testing demand as healthcare providers emphasize metabolic risk monitoring.

- Mid-Term (3–5 Years): Greater automation and multiplex assay adoption improve throughput and cost efficiency, increasing clinical adoption.

- Long-Term (6–10 Years): Potential integration into routine metabolic screening programs globally, supported by replacement of conventional tests with advanced biomarker panels.

Market size is forecast to rise from USD 16.2 Billion in 2025 to over USD 45.5 Billion by 2032. Carbon Management System will maintain dominance but face growing competition from emerging formats.

The limits of this market will also stretch into collaboration, as businesses will increasingly see that carbon management will not be a competitive edge, but a responsibility shared. Collaborations will emerge between borders, with businesses aligning their systems to work toward mutual objectives that will define future economies. Aside from short-term objectives, the global carbon management system market will also contribute to creating reputations, gaining investor trust, and determining how societies will measure success in the next few decades. It will be more than a tool for monitoring but a forum through which companies will shape their future purpose and direction.

Report Coverage

This research report categorizes the global carbon management system market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the global carbon management system market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the global carbon management system market.

Carbon Management System Market Key Segments:

By Offering

- Software

- Services

By Deployment Mode

- Cloud-Based

- On-Premise

By Application

- Energy

- Greenhouse Gas Management

- Air Quality Management

- Sustainability

- Others

By End-User

- Oil and Gas

- Manufacturing

- Healthcare

- IT and Telecom

- Power and Utilities

- Transportation and Logistics

- Construction and Infrastructure

- Others

Key Global Carbon Management System Industry Players

- SAP SE

- ENGIE Impact

- Simble Solutions Ltd

- GreenStep Solutions Inc

- Microsoft Corporation

- Schneider Electric SE

- Salesforcecom Inc

- Greenstone + Ltd

- Sphera Solutions

- Enablon SA (Wolters Kluwer)

- IsoMetrix

- Persefoni AI

- Watershed Technology Inc

- Plan A

- Net

- Sinai Technologies Inc

- Workiva Inc

- Brightly Software

- Terrascope Pte Ltd

- Carbmee GmbH

- Diligent Corporation

- Emitwise

- Sweep SAS

- Greenly

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential

US: +1 3023308252

US: +1 3023308252