MARKET OVERVIEW

The Global Barrier Paper market is among those industries, which have already responded to more sustainable packaging options. Its capabilities to replace other non-biodegradable materials within the food and beverage, cosmetic, and pharmaceutical industries have also captured much interest. Because of its ability to offer multiple layers of protection for moisture, grease, air, and other elements, this type of paper creates an area in packaging innovation. The market continues to evolve as industries seek eco-friendly alternatives, adapting to emerging challenges and setting new standards for sustainability.

This market is expected to grow further in the coming years as technology advances, enhancing the performance of barrier papers. The idea of producing products with improved resistance to environmental stressors without losing out on their recyclable and biodegradable nature will be a concept defined by the future of packaging. Industries will look into collaboration with barrier paper manufacturers to produce custom solutions that cater to specific applications. This collaboration will open the doors to innovation as it creates an environment that fosters competitiveness.

Beyond the present scope of applications, the Global Barrier Paper market is expected to diversify into niche segments. For example, as e-commerce continues its upward trajectory, packaging requirements for fragile and sensitive products will demand barrier solutions that prioritize durability and environmental responsibility. Similarly, sectors like agriculture and construction may emerge as potential users of barrier paper, integrating it into processes that require moisture control and material protection.

The market will also be influenced by regulatory pressures. Governments around the world are adopting strong policies to combat plastic waste and persuade people to use more environmentally friendly alternatives. The manufacturers of barrier papers will have to contend with these regulations while remaining cost-effective and preserving product quality. The potential to comply with such regulatory requirements and be competitive will determine the failure or success of participants in the market.

The market will look towards scalability. Some companies will invest in infrastructure and supply chains to meet growing global demands. The process will go from raw material sourcing to implementing sustainability in a forestry concern. Sourcing and production processes will be such that there is visibility into the whole process- not only in terms of meeting environmental goals but through consumer trust as well. The increasing awareness among buyers about the environmental impact of their purchases is likely to be a factor influencing the strategies that businesses operating in the market may use.

The Global Barrier Paper market will also look into design and branding innovations. Packaging aesthetics, along with functionality, will be a major factor in grabbing consumer attention. Enhanced printing capabilities, along with the versatility of barrier papers, will offer brands an opportunity to differentiate themselves while adhering to sustainability principles.

As the market evolves, so will its impacts extend beyond just packaging. It will be associated with educational awareness and collaborative movements that will sensitize people towards the use of sustainable materials. This in turn will translate into a general cultural shift for environmental awareness. In a nutshell, the Global Barrier Paper market is at an inflection point, poised to lead the pack in defining best practices for the future, both ecologically friendly and innovative enough.

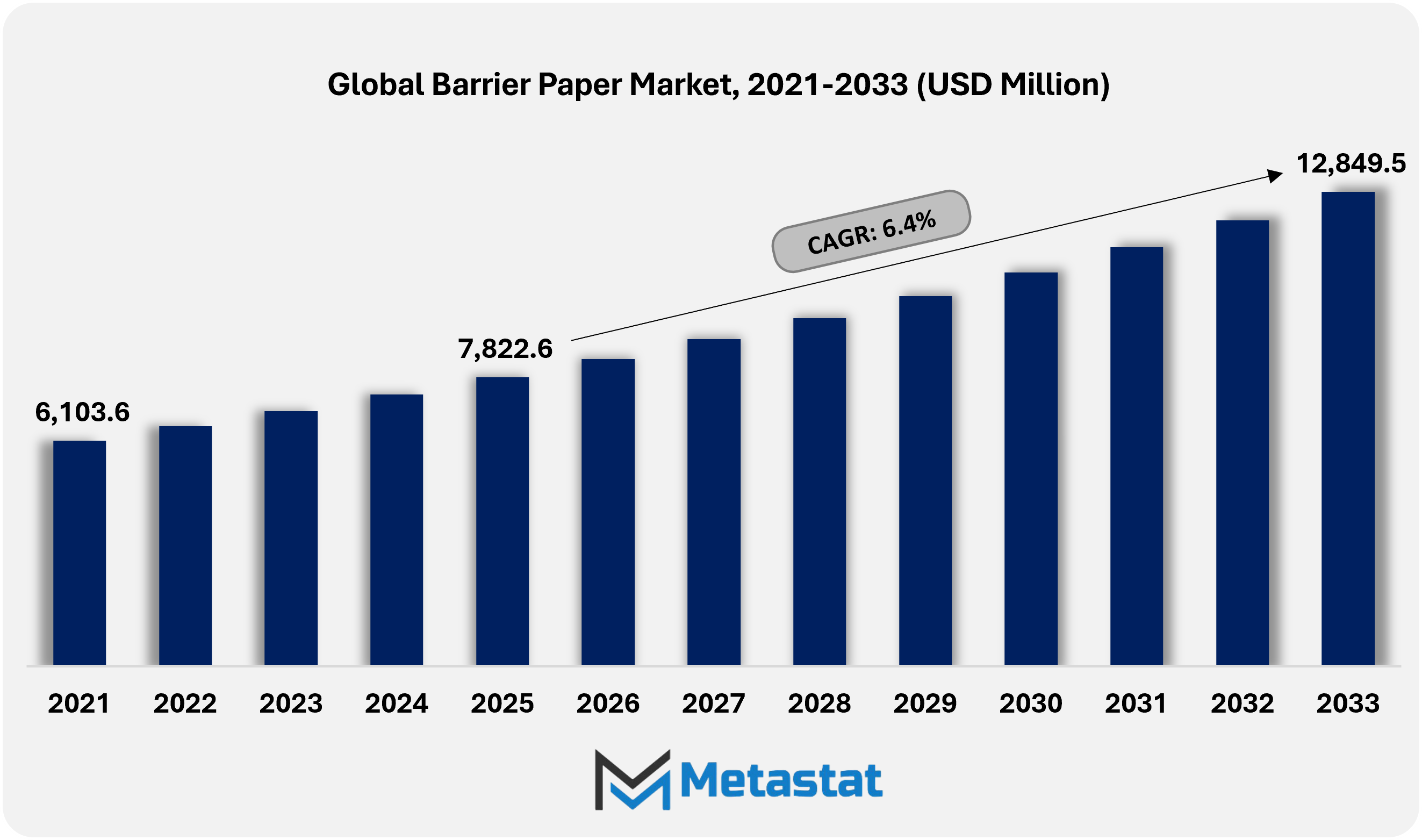

Barrier Paper market size was valued at USD 7822.6 million in 2025. The market is projected to grow from USD 8323.3 million in 2026 to USD 12849.5 million by 2033, exhibiting a CAGR of 6.4% during the forecast period.

GROWTH FACTORS

The global barrier paper market is rising at a strong pace, majorly due to the rising requirement for sustainable packaging solutions. Along with the increasing concerns toward the environment, consumers and industries are switching over to eco-friendly alternatives, creating high demand for barrier paper. The use of plastics by governments around the world is strictly regulated, promoting the adoption of barrier paper in diverse sectors. These trends depict a general effort on the reduction of environmental impact and promotion of a circular economy. However, promising as the growth prospect might be, the market has some challenges.

The high cost of production for barrier paper makes it less affordable and difficult to acquire widely. The reason behind this is that the production of barrier paper requires advanced processes and coating that raise costs. In addition, scarcity of raw materials adds to the problem, resulting in supply chain pressures and impacts market scalability. These present challenges require novel solutions to ensure that the market will be able to sustain its growth trajectory. However, on the positive side, the growth in coating technologies is a big opportunity for the barrier paper market.

There's an improvement coming in coatings as far as function is concerned- barrier paper-to make it significantly more effective towards moisture, greases, or oxygen resistance, and now more openness to new use areas across diversified industries, the food and beverages, pharmaceutical and cosmetics. Apart from that growth potential comes even from emerging Asian-Pacific markets, which further strengthen potential growth. The rapidly urbanizing and economically developing regions with awareness about sustainable practices are opening new markets for barrier paper products. Conclusively, the global market of barrier paper will witness a substantial growth because the emphasis on sustainability is increasing, as well as governments are taking stringent actions against the use of plastics. While the hurdles are still present in the form of high production costs and shortages of raw materials, technology is developing and new markets are being opened up with potential that bodes well.

Through further innovation and market development, barrier paper is destined to be used increasingly for packaging the world. This balance of challenges and opportunities underscores the need for collaboration among industry stakeholders toward overcoming challenges that face this market and fully capitalizing on its potential.

MARKET SEGMENTATION

By Coating Type

The growth rate of the Global Barrier Paper Market has remained pretty satisfactory, due to the rise in consumers' pursuit for eco-friendly and sustainable packaging products. Because of plastic usage reduction happening globally, barrier paper is becoming a more feasible option. Such type of paper is actually meant to offer protection against moisture and grease and other environmental influences, which makes it suitable for packaging purposes. It holds the property of maintaining product integrity while maintaining biodegradability-a feature for more environment-friendly products.

Two basic categories under the coating type classify barrier paper-coated and uncoated. Coated has a relatively more significant value than uncoated, worth around $5,424.28 million. In its variant, coatings are especially given to boost up its performance concerning water resistance and oil protection properties. That variant is generally for food packing purposes and some similar applications demanding substantial protection. On the other hand, uncoated barrier paper, valued at $1,936.03 million, relies on its natural fibers to provide moderate resistance. The product is preferred in applications where minimal processing and natural aesthetics are desired, though it doesn't provide the same level of protection as coated paper.

Consumer awareness regarding environmental issues has increased the demand for sustainable packaging materials. Many organizations have adopted the use of barrier paper due to campaigns to reduce carbon footprint and stricter regulations on single-use plastics. This market segment has a higher market value with its versatility, as different industries such as food, beverages, and personal care can be catered for. In contrast, the uncoated segment appeals to industries seeking cost-effective, eco-friendly options without compromising essential protective qualities.

It also finds growth supported by manufacturing process improvements that give producers the means to produce high-functioning, sustainable barrier papers. Innovation in coatings - which can be based on water, biodegradable, or another form of a solution - continues to enhance coated barrier paper. Conversely, uncoated continues to enjoy simplicity along with the support of being suitable for recyclables.

As businesses and consumers increasingly make choices that are more environmentally responsible, the barrier paper market is likely to continue its growth. It is playing a vital role in shaping the future of sustainable packaging by providing solutions that meet functional and ecological requirements. The coated and uncoated segments have their distinct advantages and cater to different needs across various industries, hence promising a good trajectory for this market.

By Printing Method

The Global Barrier Paper market has been gradually gaining importance as it is the key in sustainable packaging solutions. According to printing method, the market is segmented into Flexo, Offset, and Rotogravure, with their respective benefits that are specifically suitable for various needs. This classification represents the efforts of the industry to fulfill various demands without compromising on environmental-friendliness.

Flexo printing is a very versatile process used throughout the barrier paper market, it is known to be very effective and print to various substrates. It supports cost-effective production, therefore making it favorable for high volume applications. Being compatible with water-based inks is in perfect alignment with industry trends of a greener tomorrow. Flexo printing is really beneficial for packaging where packaging has to combine strength with printed quality.

Another area of this market is offset printing, where the prints appear sharp and clean. The advantage of offset printing is in cases where a particular application calls for detailed graphics and high-impact colors; hence, high-end packaging fits the bill for this technique. Although setting it up takes time and cost more, the high-quality print produced makes it all worth it. With precise results, the offset print makes it possible to meet the need of brand names that demand appeal in packaging.

The third printing method is rotogravure, which is famous for its speed of operation and high-quality reproduction of fine details. This printing method is also widely used for producing large volumes of barrier paper, such as wrapping foodstuffs or perishable goods. The quality of the prints can be maintained over a long run; therefore, it continues to be used in markets that need consistency and efficiency. It also boasts the ability to print intricate patterns and rich colors, making it a popular choice for special applications.

With sustainability at the forefront of consumer choice, the barrier paper market is also evolving, with more focus on print methods that enable eco-friendly solutions. Each printing method provides a unique service, meeting various needs for functionality and design. Flexo can be versatile and cost-effective; Offset can deliver sharp details; while Rotogravure is suited for mass volumes. These printing methods, in concert, serve diverse packaging needs as the industry pursues innovation with environmental responsibility.

The emphasis on barrier paper as a sustainable alternative underlines the need for production techniques to be aligned with changing consumer expectations. Refining these printing methods further, the market continues to expand its role in promoting environmentally conscious packaging solutions. This is a critical step toward reducing reliance on non-renewable resources while meeting practical and aesthetic requirements.

By Thickness

The Global Barrier Paper Market has expanded rapidly in the last few years due to increased demand for sustainable packaging solutions. It is used in various sectors like food and beverages, cosmetics, and pharmaceuticals, among others. It offers protection from external factors such as moisture, grease, and air. Paper was a non-plastic alternative to packaging materials, a direct response to the growing popular need and emphasis on controlling plastic waste levels and embracing earth-friendly practices around the world.

The market categorizes paper thickness, which helps determine the respective application and functioning of the respective paper. The most common applications for barrier paper of 0 to 50 µm thickness are for lightweight applications such as snack or small food items wrapping. This is because it has a thin structure that would be appropriate for products requiring the least amount of protection but keeping costs efficient. The 51 to 75 µm segment provides moderate protection and is often used for bakery products, frozen foods, and personal care items. Finally, the 75 to 100 µm range offers superior strength and is often selected for heavy-duty packaging applications, including protecting bulk food products or industrial materials.

Since customers are more mindful of their activities' implications for the environment, companies have shifted to adopting barrier paper to support sustainable goals. On the same trend, governments across the world continue to influence regulatory and institutional incentives to boost use of recyclable and biodegradable products. With these and related factors driving demand, the producers are developing novel products with additional protective capabilities in barrier paper yet remain recyclable.

In addition, the barrier paper market is growing with e-commerce. Due to online shopping, there has been a growth in demand for protective packaging materials. Barrier paper provides a strong protection for goods while being shipped and thus comes in handy in such situations. Also, advancement in coating technology helps in improving water and grease resistance in barrier papers, thus spreading the application into different sectors.

In conclusion, the Global Barrier Paper Market, segmented by thickness into 0 to 50 µm, 51 to 75 µm, and 75 to 100 µm, is growing rapidly due to its eco-friendly properties and versatility. As industries and consumers prioritize sustainability, barrier paper is poised to become an integral part of modern packaging solutions.

By End Use

The global Barrier Paper market is mainly segmented based on its end-use applications. These include Food & Beverages, Personal Care & Cosmetics Packaging, Pharmaceutical Packaging, and other sectors. This segmentation helps in understanding how barrier paper is used across various industries, thus proving its versatility and growing importance in sustainable packaging solutions.

In the Food & Beverages sector, barrier paper is used for maintaining freshness and protecting contents from external factors like moisture, grease, and oxygen. Its eco-friendly properties, as compared to traditional plastic packaging, have made it a preferred choice for companies that are looking forward to reducing their environmental footprint. Similarly, in the Personal Care & Cosmetics Packaging industry, the use of barrier paper is gaining traction. Its application to provide the layer of protection as well as branding through personalized designs is tailored to fit the aesthetic and functional necessities of this industry.

The Pharmaceutical Packaging industry is the other vital sector where barrier paper is doing great. It here offers an alternative, more dependable way to shield sensitive products from contamination while retaining their effectiveness when being shipped and stored. The requirements of security and sustainability, given by rising regulations and an emphasis on safety, make barrier paper answer those demands for safe and green packaging solutions. Some other uses of barrier paper include niche applications that are dependent on durability and sustainability.

This demand for barrier paper across these industries is driven by its functionality and sustainability. Businesses and consumers are becoming increasingly conscious of the environment, and this shift away from single-use plastics to biodegradable alternatives has accelerated. The versatility of barrier paper and ongoing advancements in its production technology have further expanded its applications.

With constant innovation and improvement in product lines, the global Barrier Paper market evolves to address varied needs and also promote ecological balance. The pattern reflects a balancing act between functionality and ecological considerations, and such a pattern is likely to determine the future of packaging. In Food & Beverages, Personal Care & Cosmetics Packaging, and Pharmaceutical Packaging, and many more fields, barrier paper is being set as the norm for sustainable, effective packaging. It also marks the path of reduced waste that aligns well with global sustainability goals.

|

Report Coverage

|

Details

|

|

Forecast Period

|

2025-2032

|

|

Market Size in 2025

|

USD 7,822.6 million

|

|

Market Size by 2033

|

USD 12,849.5 million

|

|

Growth Rate from 2026 to 2033

|

6.4%

|

|

Base Year

|

2022

|

|

Regions Covered

|

North America, Europe, Asia-Pacific Green, South America, Middle East & Africa

|

REGIONAL ANALYSIS

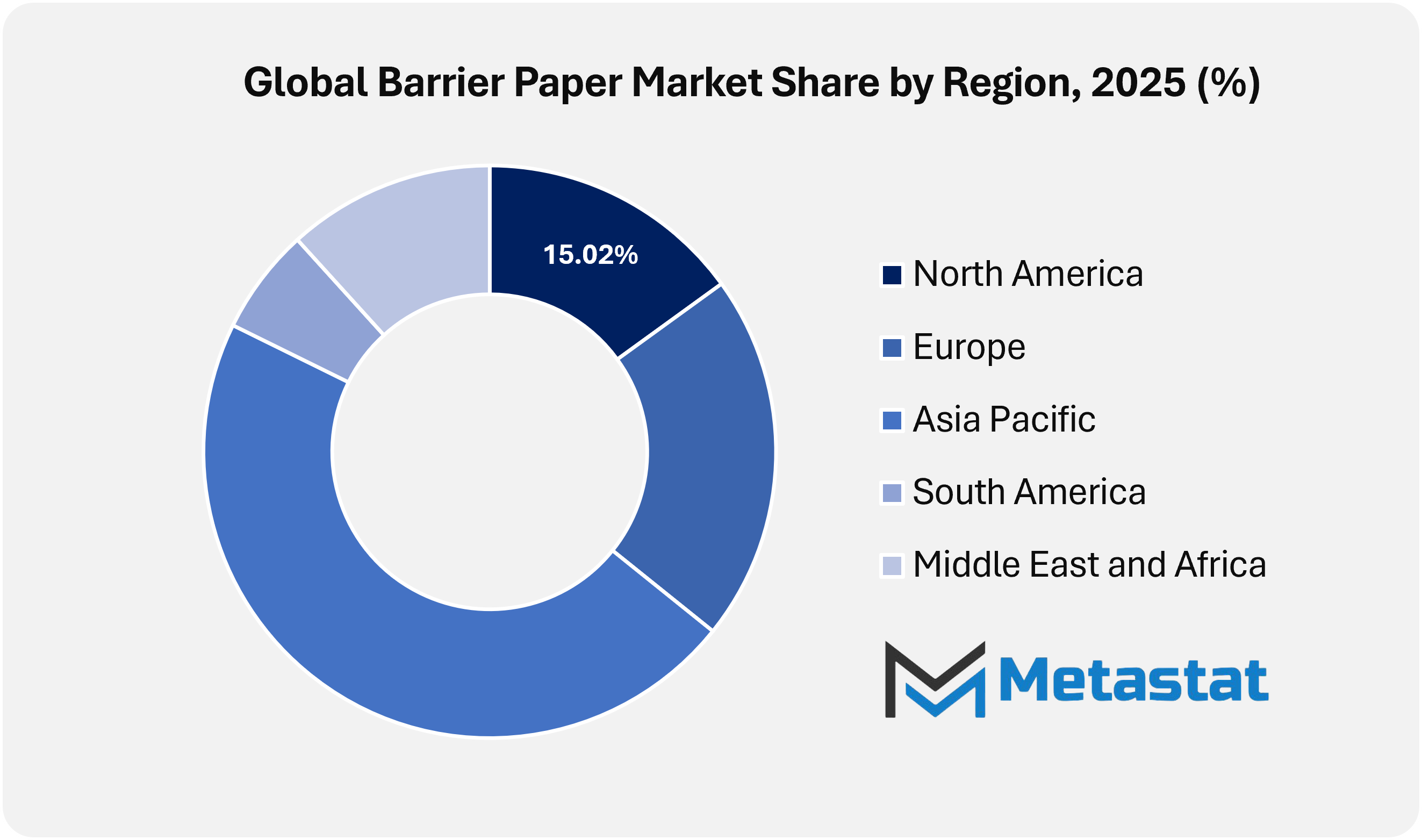

This market of Barrier Paper worldwide is a part of various sectors, which delivers sustainable and functional packaging solutions to cater to the rising demands for eco-friendly materials. This market is further divided into different key regions based on geographical regions, and North America is one of the prime regions that encompasses the U.S., Canada, and Mexico. This region has seen significant growth in packaging technologies and increased awareness of environmentally friendly alternatives, leading to the increased demand for barrier paper products.

The UK, Germany, France, and Italy continue to be core contributors to market growth in the European region, which is increasingly driven by green regulations and sensitivity towards sustainability while promoting the paper barrier across regions. The remainder of Europe provides a similar impulse, as people in this geography are also oriented towards reducing usage of plastics along with paper products.

Asia-Pacific is another significant region, which is further divided into India, China, Japan, South Korea, and the Rest of Asia-Pacific. The industrialization and urbanization in these countries, especially in China and India, have increased the consumption of packaged goods. This trend, along with growing environmental concerns, has driven the demand for barrier paper. Japan and South Korea, with their technological advancement, are also significant players in this market, contributing to innovations in the production of barrier paper.

South America, including Brazil and Argentina, is a rising market for barrier paper. In these countries, the increasing trend of sustainable packaging reflects an environmentally conscious attitude. The Rest of South America also shows potential for growth, fueled by growing consumer awareness and government initiatives to encourage green alternatives.

The Middle East & Africa region, with GCC Countries, Egypt, South Africa, and the Rest of the Middle East & Africa, represents an array of opportunities for the barrier paper market. While there is demand for economic development and infrastructure growth in the GCC countries and South Africa, other parts of the region are slowly embracing the use of eco-friendly packaging. This reflects the global move to switch to an eco-friendly solution for packaging.

In summary, the geographical segmentation of the global Barrier Paper market highlights the specific contributions and growth potential of each region. This market is poised to expand further as industries and consumers around the world continue to focus on sustainable and functional packaging solutions.

COMPETITIVE PLAYERS

The global market for barrier paper is growing well since it provides a more 'ecofriendly' alternative from traditional plastic packaging. Barrier papers protect goods, mostly foodstuff and personal and pharmaceutical products from moisture, greasy, or aerial attacks on its contents by packaging. Businesses with a 'go green' motive are in demand of more and more this eco-friendly variant for their commercial interests.

This market is influenced by several major players, bringing innovative products and the latest technologies to the fore. Among the company leaders are Mondi Group, Smurfit Kappa, Amcor, Pudumjee Paper Products, Mitsubishi Hitec Paper, Nippon Paper Industries, Stora Enso, Sappi Group, UPM Specialty Paper, Koehler Paper, Toppan, Cascades Inc., and Huhtamaki. These companies are continuously investing in research and development to improve the performance of barrier paper and meet the growing demand for sustainable packaging materials.

The shift towards environmentally friendly packaging solutions is driven by growing concerns over plastic pollution and stricter regulations imposed by governments worldwide. Consumers are also becoming more conscious of the environmental impact of their choices, which has further amplified the need for sustainable packaging alternatives. Barrier paper, with its biodegradable and recyclable properties, aligns with these evolving preferences, encouraging industries to adopt it for their packaging needs.

Apart from environmental purposes, barrier paper also provides flexibility concerning design and functionality, making it possible to support a wide variety of packaging. It can use it for food items like snack wrappers, bakery products, or pharmaceutical packaging, in which the material provides protection but does not tamper with the product's outlook. This is why companies combine sustainability with great product presentation with this material.

The competitive landscape of the barrier paper market is characterized by continuous technological advancements and a focus on customer needs. Companies are working to enhance barrier properties, including moisture and oil resistance, while ensuring that the paper remains recyclable. Manufacturers, suppliers, and end-users are also collaborating to drive innovation, ensuring that barrier paper remains a viable and effective alternative in the packaging sector.

With increasing demand for sustainable packaging, the global barrier paper market is likely to see tremendous growth with innovation and the commitment of key industry players in creating eco-friendly solutions.

Barrier Paper Market Key Segments:

By Coating Type

By Printing Method

By Thickness

- 0 to 50 µm

- 51 to 75 µm

- 75 to 100 µm

By End Use

- Food & Beverages

- Personal Care & Cosmetics Packaging

- Pharmaceutical Packaging

- Other

Key Global Barrier Paper Industry Players

- Mondi Group

- Smurfit Kappa

- Amcor

- Pudumjee Paper Products

- Mitsubishi Hitec Paper;

- Nippon Paper Industries

- Stora Enso

- Sappi Group

- UPM Specialty Paper

- Koehler Paper

- Toppan

- Cascades Inc.

- Huhtamaki

- Ahlstrom Oyj

- International Paper Company

- Georgia-Pacific LLC

- DS Smith Plc

- Domtar Corporation

- Holmen AB

- delfortgroup AG

- Felix Schoeller Group

- MM Group

- Nordic Paper Holding AB

- Appvion Inc

- ITC Limited

- APP Group

- Metsä Board Corporation

- Fedrigoni S.p.A.

- Twin Rivers Paper Company LLC

- Seaman Paper Company

- Billerud AB

- Lecta Group

- Pixelle Specialty Solutions LLC

- Oji Holdings Corporation

- Kotkamills Oy

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential

- Fiber-based barrier technologies landscape

- Replacement of plastic packaging landscape