MARKET OVERVIEW

The Warm Edge Spacer Market, a dynamic and transformative industry, has experienced remarkable growth and innovation in recent years. This market is at the forefront of the construction and energy-efficient window industry, playing a pivotal role in enhancing the performance and sustainability of windows.

At its core, the Warm Edge Spacer Market is a specialized sector within the broader glazing industry. Warm edge spacers are vital components of insulating glass units (IGUs) and are primarily responsible for maintaining the structural integrity and insulating capabilities of these units. IGUs are a fundamental part of modern windows, providing a clear and insulating barrier between the interior and exterior of a building.

One of the most significant aspects driving the Warm Edge Spacer Market's growth is its contribution to improving energy efficiency in buildings. As societies worldwide become more energy-conscious, the demand for energy-efficient products has surged. Warm edge spacers are instrumental in minimizing heat loss through windows, thus reducing heating and cooling costs. This aligns perfectly with the global trend toward sustainability and energy conservation.

Moreover, advancements in materials and manufacturing techniques have led to the development of warm edge spacers that outperform traditional aluminum spacers. Warm edge spacers are available in various materials such as stainless steel, thermoplastic, and hybrid designs. These materials offer superior thermal performance and durability, addressing the need for better insulation and condensation resistance.

The adoption of warm edge spacers is not limited to residential applications. The commercial and industrial sectors have also recognized their benefits. For instance, large-scale projects, including office complexes and institutional buildings, are increasingly incorporating these advanced spacers to meet energy efficiency regulations and improve the overall comfort of their spaces.

In addition to their thermal performance, warm edge spacers contribute to the longevity of IGUs. They reduce the risk of condensation within the unit, thus preventing mold growth and damage to the window frame and surrounding structures. This results in lower maintenance costs and prolonged lifespans for the windows, making them an attractive option for homeowners, builders, and property managers.

The Warm Edge Spacer Market's significance extends beyond the hardware itself. It has stimulated research and development in related fields, including the improvement of sealants and desiccants within IGUs, as well as innovative methods for installation and glazing techniques. This continuous evolution in technology is testament to the market's dynamism.

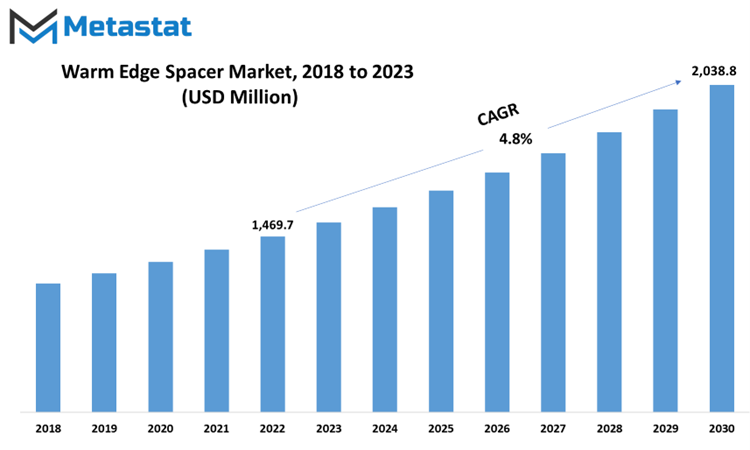

Global Warm Edge Spacer market is estimated to reach $ 2,038.8 Million by 2030; growing at a CAGR of 4.8% from 2023 to 2030.

GROWTH FACTORS

The increasing adoption of triple glazed windows, both in residential and non-residential buildings, has significantly contributed to this growing demand. These windows are designed to enhance sound and thermal insulation, and they achieve this by incorporating an extra glass pane, which limits heat transfer and ultimately results in improved heat insulation. Warm edge spacers play a crucial role in this context as they effectively separate the glass panes, creating better insulation, particularly in triple glazed windows. Their robust and efficient design further adds to the overall energy efficiency of buildings.

One notable aspect of these warm edge spacers is their low conductance edge design, which significantly boosts their adoption in triple glazed windows. Furthermore, they are also highly effective in reducing condensation, which makes them even more appealing to the market. Another driving force behind the demand for warm edge spacers is the growing consumer interest in reducing glare and UV rays entering indoor spaces. This has led to an increased interest in triple glazed windows, which, in turn, drives the adoption of warm edge spacers due to their crucial role in the construction of such windows.

On a broader scale, the rising focus on energy efficiency in commercial buildings is another market driver. This includes attention to creating more energy-efficient structures, reducing carbon emissions, and optimizing energy consumption. Warm edge spacers, when integrated with double or triple glazed windows, contribute to this by reducing heat conduction, which enhances thermal efficiency and decreases the risk of condensation. These innovations result in reduced reliance on air conditioning and heating, which not only leads to lower energy bills but also significantly reduces carbon emissions. This aspect attracts the attention of both public and private entities who are increasingly conscious of environmental concerns. Moreover, the use of warm edge spacers also helps in reducing the risk of mold or bacteria growth, contributing to the creation of a more hygienic environment in commercial spaces.

However, despite these driving factors, there are certain restraints to consider in the market. One such factor is the volatility of raw material prices and shipping costs, which may hinder the overall growth of the market. Fluctuations in the prices of materials like plastic polymers and metal alloys, along with their limited availability, can have a direct impact on production. In addition to this, there are additional tariffs and taxes imposed on the transportation of these raw materials, which further increase costs and, subsequently, make warm edge spacers more expensive. This can be a deterrent for potential buyers, particularly those with budget constraints. The high cost of warm edge spacers, combined with the added expenses for double or triple glazed windows and low-emissivity coatings, can collectively act as a barrier to their widespread adoption.

However, the market is not without its opportunities. The government's emphasis on green construction initiatives in infrastructure projects provides new avenues for warm edge spacer manufacturers. In line with this, the growing emphasis on energy-efficient buildings and lower carbon footprints creates opportunities for warm edge spacer installations worldwide. Furthermore, stricter regulations on emission levels and carbon footprints in developed countries are driving the demand for warm edge spacers and related materials. Federal initiatives aimed at achieving net-zero emissions in commercial buildings are leading to a surge in warm edge spacer sales, as buildings seek technologies to comply with energy efficiency guidelines. Additionally, the integration of warm edge spacers in windows offers untapped markets for manufacturers, providing energy cost savings and improved energy efficiency, which are becoming increasingly attractive in today's environmentally conscious world.

MARKET SEGMENTATION

By Type

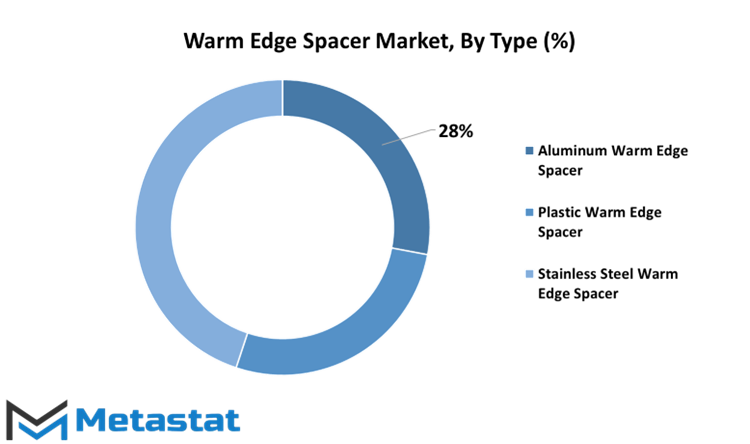

The global Warm Edge Spacer market exhibits diversity in its segments. Specifically, it can be categorized into different types based on the materials used in the spacer. These materials include aluminum, plastic, and stainless steel, each having unique characteristics and applications. In 2020, the Aluminum Warm Edge Spacer segment recorded a value of 165.3 million US dollars. Aluminum, known for its lightweight and corrosion-resistant properties, is a popular choice for warm edge spacers. It effectively reduces heat transfer and condensation, making it a preferred option for improving the energy efficiency of windows.

The Plastic Warm Edge Spacer segment, on the other hand, achieved a value of 145.9 million US dollars in 2020. Plastic warm edge spacers are valued for their cost-effectiveness and durability. They are often used in double glazing units to enhance insulation. Plastic spacers offer an economical solution without compromising on performance.

In the same year, the Stainless-Steel Warm Edge Spacer segment reached a valuation of 272.1 million US dollars. Stainless steel, recognized for its strength and resistance to corrosion, is an ideal choice for demanding applications. It provides exceptional durability and structural support to windows, making it a valuable material for warm edge spacers.

These segment values highlight the significance of material choice in the warm edge spacer market. Each material type caters to distinct needs and preferences, offering solutions that align with varying cost considerations, performance requirements, and durability expectations in the construction industry.

By Application

The global Warm Edge Spacer market exhibits notable diversity when considering its applications. By application, the market is effectively divided into two key segments: Residential and Commercial. Each of these segments boasts its own set of characteristics and growth prospects.

In the residential domain, the Warm Edge Spacer market is poised for a steady expansion. Projections indicate a Compound Annual Growth Rate (CAGR) of 4.8% during the period spanning from 2021 to 2027. This growth trajectory signifies a consistent rise in demand within residential contexts. The usage of Warm Edge Spacers in residential applications primarily revolves around enhancing energy efficiency. Homeowners and builders are increasingly recognizing the importance of energy conservation, seeking solutions that facilitate better insulation and reduced heat loss.

On the other hand, the commercial segment of the Warm Edge Spacer market is not far behind in terms of growth potential. Forecasts predict a CAGR of 4.7% during the same period from 2021 to 2027. Commercial spaces, which encompass a wide range of settings from office buildings to retail establishments, are also embracing the benefits of Warm Edge Spacers. The commercial sector's adoption of these spacers is fueled by a dual objective of energy efficiency and cost savings. Efficient insulation leads to reduced energy consumption, contributing to both environmental sustainability and economic feasibility.

The segmentation of the global Warm Edge Spacer market into residential and commercial applications indicates a promising future for both. The residential sector focuses on enhancing energy efficiency and sustainability in individual homes, while the commercial sector seeks similar benefits, but within the complex and multifaceted world of commercial real estate. Regardless of the setting, the common goal is clear: to reduce energy consumption, lower greenhouse gas emissions, and promote sustainable building practices. The modestly divergent growth rates in these segments signify the unique factors at play but collectively underscore the global shift towards more responsible and energy-efficient construction practices.

REGIONAL ANALYSIS

Market drivers are pivotal forces that steer the global Warm Edge Spacer market, and these forces exhibit distinctive impacts across different geographical regions. The market's geographical distribution encompasses North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, each experiencing unique influences. North America, including the U.S., Canada, and Mexico, possesses a substantial market share. This dominance is fueled by a strong emphasis on energy efficiency and sustainable construction practices. The region's commitment to reducing heat loss through windows bolsters the demand for warm edge spacers. Whereas, Europe has the UK, Germany, France, Italy, and other nations, showcases a thriving market driven by stringent energy performance regulations. European countries are committed to reducing greenhouse gas emissions, promoting the adoption of energy-efficient building materials like warm edge spacers.

COMPETITIVE PLAYERS

The Warm Edge Spacer industry encompasses several key players, and two prominent companies in this sector are Cardinal Glass Industries and GED Integrated Solutions. Cardinal Glass Industries, a management-owned S-Corporation, stands at the forefront of residential glass development for windows and doors. Established in 1962, it is headquartered in Minnesota, United States. This company distinguishes itself through the design and fabrication of cutting-edge residential glass products, making it a leading force in the industry.

On the other hand, GED Integrated Solutions is a comprehensive provider of various services within the industry. Their offerings span across glass and screen fabrication, software processes, decorative vinyl, cleaning services, and solutions for glass handling, assembling, and sorting. GED Integrated Solutions not only manufactures these products but also markets and provides services for them, primarily within the United States.

These two companies, Cardinal Glass Industries and GED Integrated Solutions, represent significant contributors to the advancement of technologies and services in the Warm Edge Spacer industry. Their dedication to innovation and excellence propels the industry forward, meeting the evolving needs of residential glass products for windows and doors.

Warm Edge Spacer Market Key Segments:

By Type

- Aluminum Warm Edge Spacer

- Plastic Warm Edge Spacer

- Stainless Steel Warm Edge Spacer

By Application

- Residential

- Commercial

Key Global Warm Edge Spacer Industry Players

- ALU-PRO S.r.l.

- Cardinal Glass Industries

- GED Integrated Solutions

- Glasslam

- HELIMA GmbH

- Hygrade Components

- KÖMMERLING

- Quanex Building Products Corporation

- Saint Best Group Ltd.

- Swisspacer AG

- Technoform

- Thermoseal Group

- Viracon, Inc.

- All Metal

- Nippon Sheet Glass

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential

US: +1 3023308252

US: +1 3023308252