Tinplate Market Size, Share, By Product Type (Electrolytic Tinplate, Hot-Dipped Tinplate, and Others), By Thickness (Single Reduced and Double Reduced), By Form (Coils, Sheets, and Cut-To-Size Pieces), By Application (Food Beverage Packaging, Aerosol Cans, General Line Cans, Industrial Applications, Automotive Applications, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4717

Published

May 4, 2026

Pages

314 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

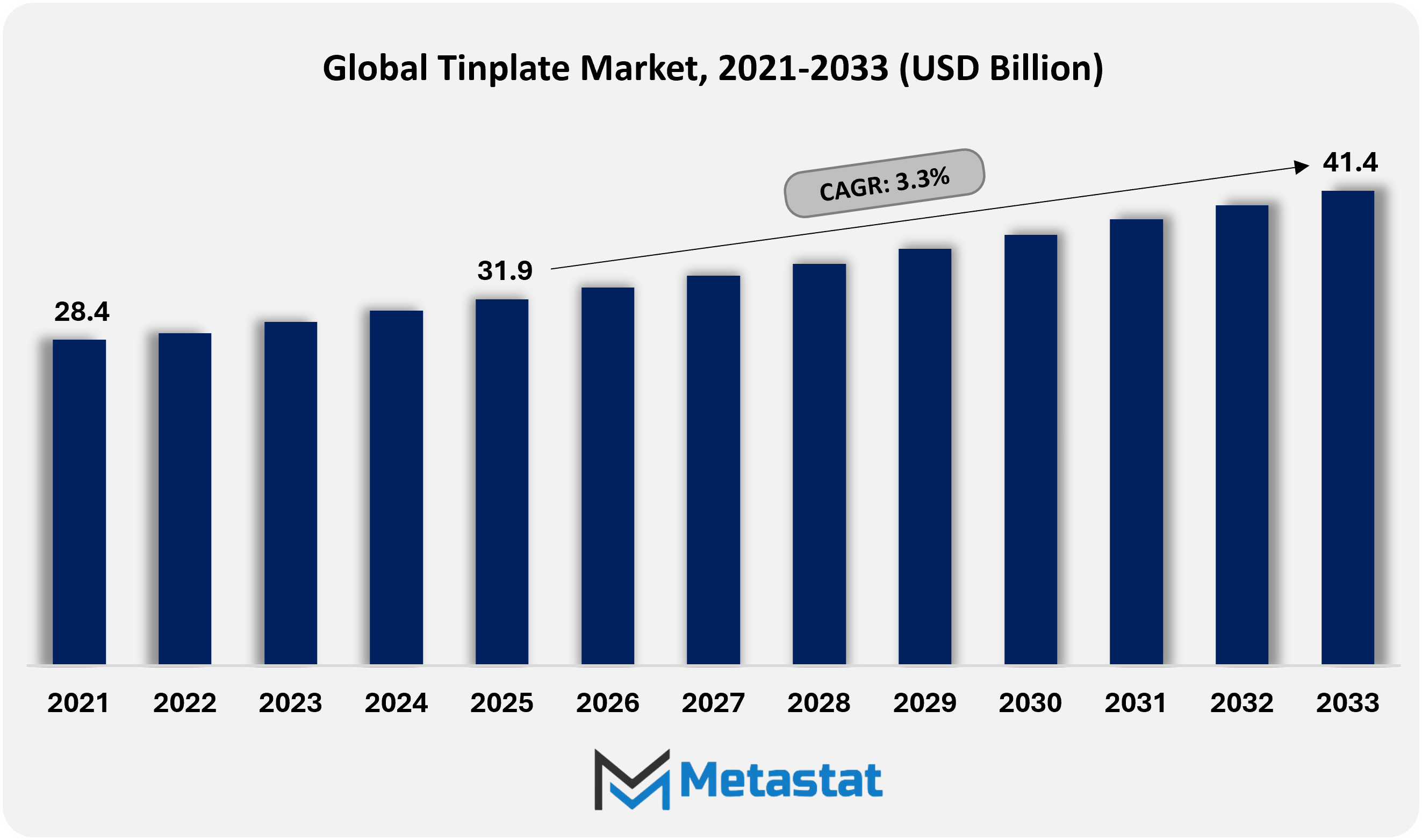

Global Tinplate market size is valued at USD 31.9 billion in 2025 and projected to grow at a CAGR of 3.3% during the forecast period, reaching USD 41.4 billion by 2033.

Global Tinplate Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

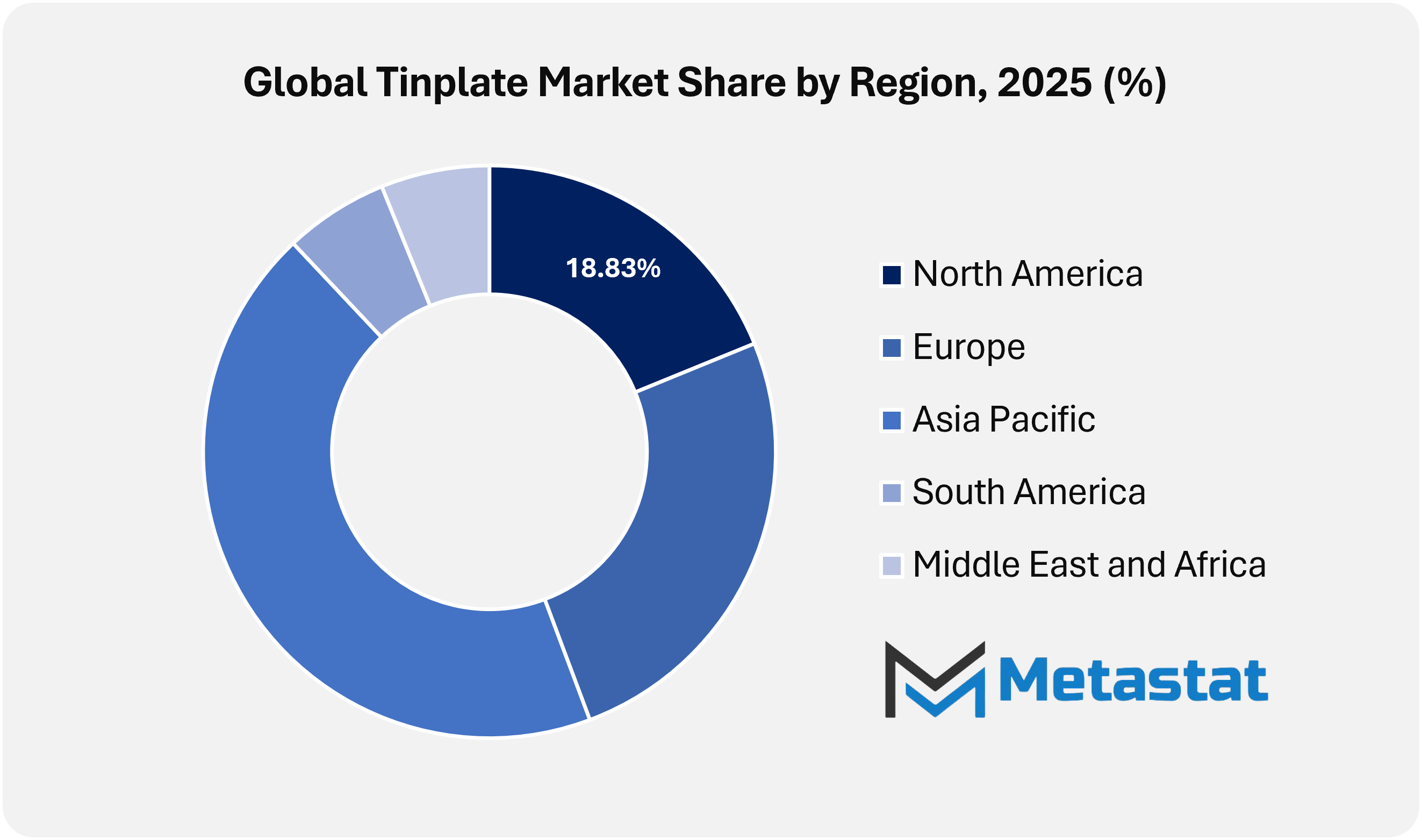

North America accounted for 18.8% of the global market in 2025, with the U.S. leading the regional market.

Electrolytic Tinplate segment accounts for a market share of 91.1% in 2025.

Key trends driving growth: Shift toward metal packaging for shelf-stable food & beverage and rising adoption of printed, decorated, and premium metal packs in consumer goods.

Opportunities include high-recycled-content tinplate and advanced surface treatments supporting sustainability-led packaging conversions.

Key insight: Rising demand from food packaging and sustainability focus reshape competitive dynamics in the Global Tinplate Market.

The global tinplate market within the metal packaging industry is evolving beyond conventional applications and is increasingly positioned at the intersection of material innovation, branding, and circular economy objectives. While beverage and food cans continue to hold a strong presence across retail shelves, future demand will be shaped by specialized packaging formats for pharmaceuticals, aerosols, and premium consumer goods that require extended shelf life and reliable product protection. Manufacturers will focus not only on production expansion but also on metallurgical refinement, advanced surface coatings, and digital traceability systems that improve product differentiation and operational efficiency.

Manufacturers are increasingly adopting advanced tempering techniques and ultra-thin gauge rolling to reduce material weight while maintaining structural integrity, enabling lower freight loads and reduced carbon emissions across logistics networks. At the same time, decorative lithography and smart labeling are transforming tin-coated steel into a value-added packaging medium capable of supporting QR-based authentication and anti-counterfeiting features. This trend is creating opportunities in luxury packaging, specialty chemicals, and niche export categories where durability must align with premium visual appeal.

Market Dynamics

Growth Drivers:

Shift toward metal packaging for shelf-stable food and beverage.

Global Tinplate market will gain strong momentum from expanding demand for shelf-stable food and beverage packaging. Urban lifestyles, longer supply chains, and rising preference for packaged food products are increasing reliance on durable metal containers. Superior barrier performance against light and oxygen strengthens product protection and extends storage life. Manufacturers continue to prefer tinplate cans for consistent quality retention, supporting wider distribution across domestic and export markets.

Rising adoption of printed, decorated, and premium metal packs in consumer goods

Global Tinplate market is benefiting from the growing use of printed and decorated metal packaging across personal care, confectionery, and specialty retail categories. Premium finishes, embossing, and advanced coating technologies improve brand visibility on crowded shelves. Manufacturers are investing in high-definition printing and surface design capabilities to strengthen consumer engagement. Enhanced packaging aesthetics are supporting value-added positioning, higher margins, and stronger product differentiation.

Restraints and Challenges:

Tin and steel input cost volatility affecting can-stock economics

Global Tinplate market faces pressure from fluctuations in tin and steel prices, which directly affect can-stock production costs and procurement planning. Price volatility can compress margins for converters and food processors operating under fixed supply contracts. Budget forecasting becomes increasingly difficult during unstable commodity cycles. Although long-term agreements and hedging strategies can reduce some risk, raw material price swings continue to challenge cost stability across the value chain.

Substitution pressure from aluminum, plastics, and flexible packaging in select use cases

Global Tinplate market faces substitution pressure from aluminum containers, rigid plastics, and flexible pouches across selected packaging applications. Lightweight alternatives remain attractive to cost-sensitive manufacturers seeking lower transportation costs. Flexible materials also appeal to brands focused on convenience-oriented packaging designs. This competitive material landscape is intensifying the need for tinplate manufacturers to strengthen performance differentiation and highlight recyclability advantages.

Opportunities:

High-recycled-content tinplate and advanced surface treatments supporting sustainability-led packaging conversions

Global Tinplate market is creating opportunity through the development of high-recycled-content grades and advanced surface treatments aligned with sustainability goals. Circular economy targets are encouraging brand owners to adopt recyclable steel packaging formats with lower carbon footprints. Improved corrosion resistance and food-contact coatings are enhancing durability and product safety. Sustainability mandates across packaging value chains will accelerate the shift from non-recyclable materials toward responsible tinplate solutions.

Market Segmentation Analysis

The Global Tinplate market is classified based on Product Type, Thickness, Form, and Application.

By Product Type, the market is further segmented into:

Electrolytic Tinplate

Electrolytic Tinplate segment is valued at USD 30.0 billion in 2026 and is projected to reach USD 38.5 billion by 2033, at a CAGR of 3.6% during the forecast period.

Electrolytic Tinplate will gain preference owing to its uniform coating control and improved surface finish. Advanced plating technologies enhance corrosion resistance and printability, supporting demand for premium packaging applications. Rising consumption of processed food and branded consumer goods is further strengthening production demand across both emerging and developed manufacturing hubs.

Hot-Dipped Tinplate

Hot-Dipped Tinplate segment is valued at USD 1.8 billion in 2026 and is projected to reach USD 1.7 billion by 2033, at a CAGR of 1.3% during the forecast period.

Hot-Dipped Tinplate retains relevance through its strong mechanical properties and reliable protective layering. Heavy-duty packaging and storage applications continue to support steady demand. Modern furnace systems and energy-efficient dipping processes are improving cost structures, enabling manufacturers to serve bulk industrial customers with consistent quality standards.

Others

Others segment is valued at USD 1.1 billion in 2026 and is projected to reach USD 1.2 billion by 2033, at a CAGR of 1.4% during the forecast period.

Other product variations are witnessing selective growth driven by niche industrial requirements. Customized coatings and alloy blends are addressing specialized application needs across specific end-use sectors. Ongoing research into alternative surface treatments is expanding technical possibilities and enabling differentiated offerings for industries requiring enhanced durability and longer shelf stability.

By Thickness, the market is divided into:

Single Reduced

Single Reduced segment is projected to reach USD 28.2 billion by 2033, at a CAGR of 2.6% during the forecast period.

Single Reduced material remains widely used across standard packaging formats. Its balanced strength and flexibility support efficient forming operations in high-volume manufacturing environments. Continuous improvements in rolling precision are enabling producers to optimize weight management while preserving structural integrity, supporting cost efficiency in consumer goods packaging.

Double Reduced

Double Reduced segment is projected to reach USD 13.2 billion by 2033, at a CAGR of 4.9% during the forecast period.

Double Reduced variants are expanding in lightweight packaging applications. Higher tensile strength combined with reduced thickness enables material savings and improved transportation efficiency. Growing sustainability targets across supply chains are encouraging adoption, while manufacturers continue investing in advanced rolling mills to meet evolving performance requirements.

By Form, the market is further divided into:

Coils

Coils segment is projected to reach USD 29.6 billion by 2033.

Coils dominate large-scale manufacturing owing to their seamless integration into automated production lines. Efficient bulk handling and reduced processing interruptions improve operational productivity across high-volume facilities. Smart inventory systems and predictive maintenance tools are further enhancing coil utilization rates in packaging and fabrication operations.

Sheets

Sheets segment is projected to reach USD 9.6 billion by 2033.

Sheets continue to serve medium-scale processors seeking manageable and flexible formats. Standardized dimensions simplify storage, handling, and customization across multiple production environments. Technological upgrades in cutting and leveling equipment are improving surface flatness and ensuring consistent output for decorative packaging and specialty box manufacturing.

Cut-To-Size Pieces

Cut-To-Size Pieces segment is projected to reach USD 2.2 billion by 2033.

Cut-To-Size Pieces are witnessing steady demand from small-scale and specialized manufacturers. Precision cutting technologies reduce material waste and improve turnaround times. Flexible order volumes support customized production requirements, encouraging suppliers to offer digitally managed fabrication services.

By Application, the Global Tinplate market is divided as:

Food Beverage Packaging

Food Beverage Packaging segment is projected to grow at a CAGR of 3.5% during the forecast period.

Food and Beverage Packaging is witnessing sustained expansion driven by rising packaged food and beverage consumption. Enhanced barrier properties help protect flavor, freshness, and nutritional value. Regulatory emphasis on safe storage solutions is encouraging innovation in coating formulations, strengthening long-term demand across domestic and export markets.

Aerosol Cans

Aerosol Cans segment is projected to grow at a CAGR of 3.8% during the forecast period.

Aerosol Cans are benefiting from growth in personal care, household, and healthcare products. Improved internal lacquering systems are increasing compatibility with pressurized contents and sensitive formulations. Automated shaping and sealing technologies are enhancing safety standards and supporting higher output across global filling operations.

General Line Cans

General Line Cans segment is projected to grow at a CAGR of 2.3% during the forecast period.

General Line Cans will continue to show stable growth driven by demand from paints, chemicals, and consumer goods. Strong sealing performance and stacking strength improve logistics efficiency and storage reliability. Ongoing modernization of can-making equipment is also enhancing design flexibility and branding potential.

Industrial and Automotive Applications

Industrial and Automotive Applications segment is projected to grow at a CAGR of 1.9% during the forecast period.

Industrial and Automotive applications are expanding through demand for durable containers and protective components. Resistance to environmental exposure supports long-term storage of lubricants and specialty fluids. Advanced coating development is improving performance under demanding mechanical and industrial conditions.

Others

Others segment is projected to grow at a CAGR of 4.1% during the forecast period.

Other applications are emerging through innovative use across construction materials, promotional packaging, and niche industrial formats. Product diversification strategies are encouraging the adoption of decorative finishes and specialty coatings. Collaboration between material scientists and manufacturers will open additional commercial opportunities over the forecast period.

By Region:

Based on geography, the Global Tinplate market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Tinplate Market is set to expand at a CAGR of 3.3% within the forecast period, reaching a market size (TAM) of USD 6.6 billion by the end of 2033.

North America supports the Tinplate market through strong demand from the food canning industry, supported by advanced packaging standards and high consumption of processed food products.

North America strengthens the Tinplate market through sustained investments in sustainable metal packaging and well-established recycling infrastructure across the U.S. and Canada.

Europe holds a significant position in the Tinplate market owing to its established food canning, beverage packaging, and aerosol manufacturing industries.

Asia Pacific presents significant opportunities in the Tinplate market owing to rapid urbanization and increasing demand for packaged food and beverage products across China and India.

Across the Middle East, Africa, and South America, the Tinplate market gains regular traction through expanding meals processing sectors, growing retail networks, and growing preference for long lasting steel packaging solutions.

Competitive Landscape and Strategic Insights

The global tinplate market plays a vital role in modern packaging and industrial supply chains. Tinplate, which is steel coated with a thin layer of tin, widely used in food cans, beverage containers, aerosol cans, and a range of industrial packaging applications. Its strength, corrosion resistance, and ability to preserve contents over extended periods make it a reliable material across end-use sectors. Demand will remain steady, supported by urbanization, rising packaged goods consumption, and the expansion of organized retail and processed food industries, particularly in developing economies.

Large steel manufacturers dominate the competitive landscape, with companies investing in advanced coating lines and quality control systems to meet strict food safety standards. ArcelorMittal S.A. and Nippon Steel Corporation maintain strong positions owing to their global production networks and deep expertise in flat steel products. Tata Steel Limited and JSW Steel Limited continue to expand their tinplate capacity to serve both domestic and export markets. At the same time, Asian manufacturers such as China Baowu Steel Group Corporation Limited and POSCO Group strengthen regional supply through cost-efficient production and extensive distribution networks.

Several specialized and regional players also contribute to market stability. TCC Steel and Toyo Kohan Co., Ltd. focus heavily on high-grade tinplate used in food and beverage packaging. European companies such as Thyssenkrupp AG and Ternium S.A. maintain a strong presence through technological upgrades and strategic supply agreements. In Southeast Asia, Perusahaan Sadur Timah Malaysia and Thai Tinplate Manufacturing Public Company Limited serve growing local demand, while companies such as NS-Siam United Steel Co., Ltd. strengthen cross-border supply collaboration.

Other key contributors including JFE Steel Corporation, KG Dongbu Steel Co., Ltd., Beijing Shougang Co., Ltd., Altos Hornos de Mexico, S.A.B. de C.V. (AHMSA), HBIS Group Serbia Iron & Steel LLC Belgrade, and Ohio Coatings Company add further depth to the global supply base. Emerging and trading-focused companies such as Sino East, Jingye Steel Group, Guangnan Holdings Limited, Hebei Yehui Metal Materials Co., Ltd., Asian Global Ltd., and Indo Global Steel help connect producers with end users across regions. With continuous advancements in coating technologies, stronger focus on recyclable packaging, and rising demand from food processing industries, the global tinplate market will remain competitive and growth-oriented over the coming years.

Forecast and Future Outlook

Market size is forecast to rise from USD 31.9 billion in 2025 to over USD 41.4 billion by 2033.

Strategic partnerships between steel mills and consumer goods manufacturers will redefine specification standards, leading to customized tin coatings engineered for improved corrosion resistance across diverse climatic conditions. Over the coming years, the industry will strengthen its role not only as a packaging material supplier but also as a materials innovation partner supporting sustainability targets and premium product positioning across multiple industrial verticals.

This research report categorizes the Tinplate market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Tinplate market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Tinplate market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 3.3% from 2026 to 2033

Revenue Unit

USD billion

Sales Volume Unit

Kilotons

Segmentation

By Product Type, Thickness, Form, Application, and Region

By Region

North America (By Product Type, Thickness, Form, Application, and Country)

United States

Canada

Mexico

Europe (By Product Type, Thickness, Form, Application, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Product Type, Thickness, Form, Application, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Product Type, Thickness, Form, Application, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Product Type, Thickness, Form, Application, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Emerging Segments and Regional Growth Potential

Key Strategic Recommendations

Competitive Benchmarking

End of Report Overview

Frequently Asked Questions

Find answers to common questions about this report

Top players operating in the Tinplate industry include ArcelorMittal S.A., TCC Steel, Tata Steel Limited, SMS Group, JSW Steel Limited, Promisteel Co., Ltd., and Thyssenkrupp AG.

Global Tinplate market is estimated to reach USD 41.4 billion by 2033.

Tin and steel input cost volatility affecting can-stock economics will hamper the market growth within the forecast period.

Asia Pacific region dominates the market.

The Electrolytic Tinplate is the leading type segment in the Global market.

Shift toward metal packaging for shelf-stable food and beverage and Rising adoption of printed, decorated, and premium metal packs in consumer goods are key driving factors, boosting the market.

The Metastat Insights analysis shows that the North America Tinplate market size is estimated to be USD 6.6 billion by 2033.

The Global Tinplate market is expected to grow at a CAGR of 3.3% over the forecast period (2026-2033).

The Metastat Insights study shows that the Global Tinplate market size was USD 31.9 billion in 2025.

Kraft Paper market size is valued at USD 19.3 billion in 2025 and projected to reach USD 29.9 billion by 2033, growing at a CAGR of 5.6% from 2026 to 2033.

Kraft Paper market, Kraft Paper Market Size, Kraft Paper Market Share, Kraft Paper Market Analysis, Kraft Paper Market Growth, Kraft Paper Market Trends, Kraft Paper Market Research Report, Kraft Paper Market Forecast, Kraft Paper, Kraft Paper Market Research, Kraft Paper Industry, Kraft Paper Industry Report, Kraft Paper Market Data, Kraft Paper Statistics, Kraft Paper Market Statistics, Kraft Paper Industry Trends, Kraft Paper Market Report, Kraft Paper Market Trends, Kraft Paper Market News, Kraft Paper Forecasts, Kraft Paper Market Intelligence Report, Kraft Paper market outlook, Kraft Paper market segmentation, Kraft Paper market drivers, Kraft Paper market restraints, Kraft Paper market opportunities, Kraft Paper market CAGR, Kraft Paper suppliers, Kraft Paper manufacturers, Kraft Paper market by region, North America Kraft Paper market, Asia Pacific Kraft Paper market, Europe Kraft Paper market, Kraft Paper market competitive landscape, Kraft Paper market key players, Unbleached Kraft Paper market, Semi-Bleached Kraft Paper market, Bleached Kraft Paper market, Virgin Natural Kraft Paper market, Recycled Kraft Paper market, Corrugated Boxes Kraft Paper market, Grocery and Shopping Bags Kraft Paper market, Multiwall Sacks Kraft Paper market, Carryout Bags Kraft Paper market, Food and Beverages Kraft Paper market, Electronics Kraft Paper market, Construction Kraft Paper market, Cosmetics and Personal Care Kraft Paper market, Textile Manufacturing Kraft Paper market.

Pallets market size is valued at USD 88.3 billion in 2025 and projected to reach USD 138.6 billion by 2033, growing at a CAGR of 5.8% from 2026 to 2033.

Europe Premium Molded Fiber Market Size, Share, Trends, 2033

Europe Premium Molded Fiber market size is valued at USD 448.0 million in 2025 and is projected to reach USD 901.0 million in 2033, at a CAGR of 9.2% from 2026 to 2033

Europe Premium Molded Fiber Market, Europe Premium Molded Fiber Market Size, Europe Premium Molded Fiber Market Share, Europe Premium Molded Fiber Market Analysis, Europe Premium Molded Fiber Market Growth, Europe Premium Molded Fiber Market Trends, Europe Premium Molded Fiber Market Research Report, Europe Premium Molded Fiber Market Forecast, Europe Premium Molded Fiber, Europe Premium Molded Fiber Market Research, Europe Premium Molded Fiber Industry, Europe Premium Molded Fiber Industry Report, Europe Premium Molded Fiber Market Data, Europe Premium Molded Fiber Statistics, Europe Premium Molded Fiber Market Statistics, Europe Premium Molded Fiber Industry Trends, Europe Premium Molded Fiber Market Report, Europe Premium Molded Fiber Market Trends, Europe Premium Molded Fiber Market News, Europe Premium Molded Fiber Forecasts, Europe Premium Molded Fiber Market Intelligence Report

North America Infant Formula Metal Packaging Market Size, Share, Trends, 2033

North America Infant Formula Metal Packaging market size is valued at USD 7,665.5 million in 2025 and is projected to reach USD 12,123.8 million in 2033, at a CAGR of 5.7% from 2026 to 2033

North America Infant Formula Metal Packaging Market, North America Infant Formula Metal Packaging Market Size, North America Infant Formula Metal Packaging Market Share, North America Infant Formula Metal Packaging Market Analysis, North America Infant Formula Metal Packaging Market Growth, North America Infant Formula Metal Packaging Market Trends, North America Infant Formula Metal Packaging Market Research Report, North America Infant Formula Metal Packaging Market Forecast, North America Infant Formula Metal Packaging, North America Infant Formula Metal Packaging Market Research, North America Infant Formula Metal Packaging Industry, North America Infant Formula Metal Packaging Industry Report, North America Infant Formula Metal Packaging Market Data, North America Infant Formula Metal Packaging Statistics, North America Infant Formula Metal Packaging Market Statistics, North America Infant Formula Metal Packaging Industry Trends, North America Infant Formula Metal Packaging Market Report, North America Infant Formula Metal Packaging Market Trends, North America Infant Formula Metal Packaging Market News, North America Infant Formula Metal Packaging Forecasts, North America Infant Formula Metal Packaging Market Intelligence Report