Rare Disease Genetic Testing Market Size, Share, By Disease Type (Neurological Disorders, Immunological Disorders, Cancer, Hematology Diseases, Cardiovascular Disorders (CVDs), Endocrine & Metabolism Diseases, Musculoskeletal Disorders, Dermatology Disease, and Others,), By Technology (Whole Exome Sequencing (WES), Whole Genome Sequencing (WGS), Array Technology, PCR-based Testing, Sanger Sequencing, FISH, and Karyotyping), By Specialty (Molecular Genetic Tests, Chromosomal Genetic Tests, and Biochemical Genetic Tests), By End User (Research Laboratories & CROs, Diagnostic Laboratories, and Hospitals & Clinics), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-2311

Published

February 3, 2026

Pages

304 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Definition

Rare disease genetic testing screens all genes known to cause human disease. About 6000 genes are reported to be clinically relevant. The genetic tests are focused on analysis of specific genes, depending on which possible genetic diagnoses are suspected.

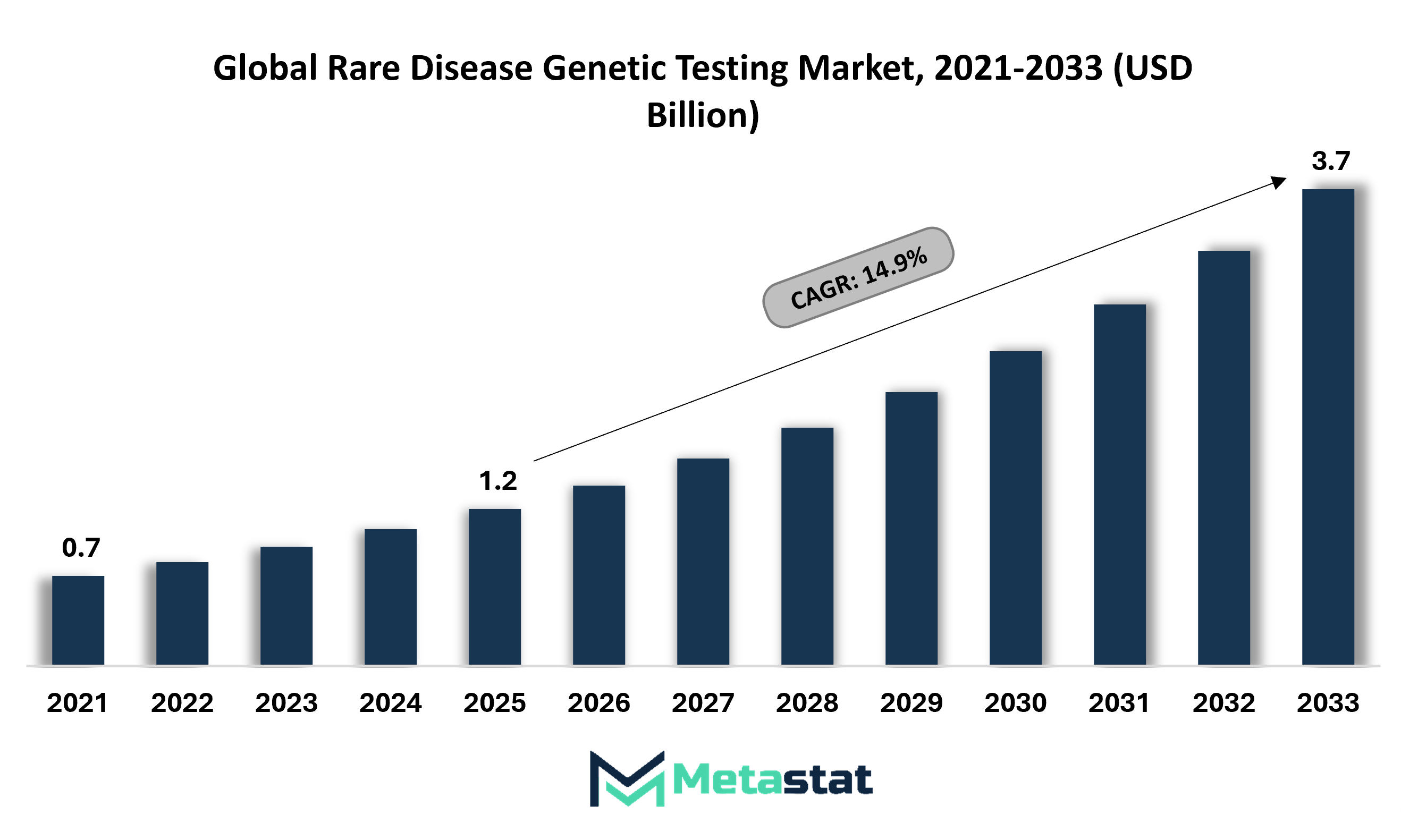

Global Rare Disease Genetic Testing market size is valued at USD 1.2 billion in 2025 and projected to grow at a CAGR of 14.9% during the forecast period, reaching USD 3.7 billion by 2033.

Market Dynamics

Rising incidence of rare diseases is boosting the market growth. For instance, according to the World Health Organization (WHO), over 400 million people are living with one or more of 6,000 identified rare diseases around the world.Rare diseases affect 3.5% to 5.9% of the worldwide population. According to the Genetic and Rare Diseases Information Center, 1 in 10 American, which is 30 million people suffer for some kind of rare disease. 50% of people affected by rare diseases are children. According to the European Commission, approximately 5,000-8,000 distinct rare diseases affect 6% to 8% of the EU population, which is between 27 and 36 million people. In 2019, 70 million people in India are affected by rare diseases. According to the Australians Department of Health, around 8% of Australians, which is 2 million people live with a rare disease. About 80% of rare diseases are genetic in Australia. Further, innovative technologies for rare disease genetic testing is a key driving factor of the market. However, lack of awareness pertaining to rare diseases might hamper the market growth. Moreover, government support for rare disease diagnosis would provide lucrative opportunities for the market in coming years.

Market Segmentation

The global rare disease genetic testing market is mainly classified based on technology, disease type, specialty, and end user. Technology is further segmented into Whole Exome Sequencing (WES), Whole Genome Sequencing (WGS), Array Technology, PCR-based Testing, Sanger Sequencing, FISH, and Karyotyping. By disease type the market is divided into Neurological Disorders, Immunological Disorders, Cancer, Hematology Diseases, Cardiovascular Disorders (CVDs), Endocrine & Metabolism Diseases, Musculoskeletal Disorders, Dermatology Disease, and Others. By specialty the market is further divided into Molecular Genetic Tests, Chromosomal Genetic Tests, and Biochemical Genetic Tests. By end user the global Rare Disease Genetic Testing market is divided as Research Laboratories & CROs, Diagnostic Laboratories, and Hospitals & Clinics.

Based in technology, Whole Exome Sequencing (WES) has shown significant growth in 2020, owing to the increasing studies for whole exome sequencing (WES), rising awareness for rare disease genetic testing, and commercialization of service for whole exome sequencing (WES). For instance, Natera, a leader in cell-free DNA testing, has commercialized a research-use-only (RUO) service for whole exome sequencing (WES) of circulating tumor DNA, using plasma samples from patients with cancer.The assay allows researchers to characterize resistance mutations, actionable mutations, neoantigens, and tumor evolution.

Regional Analysis

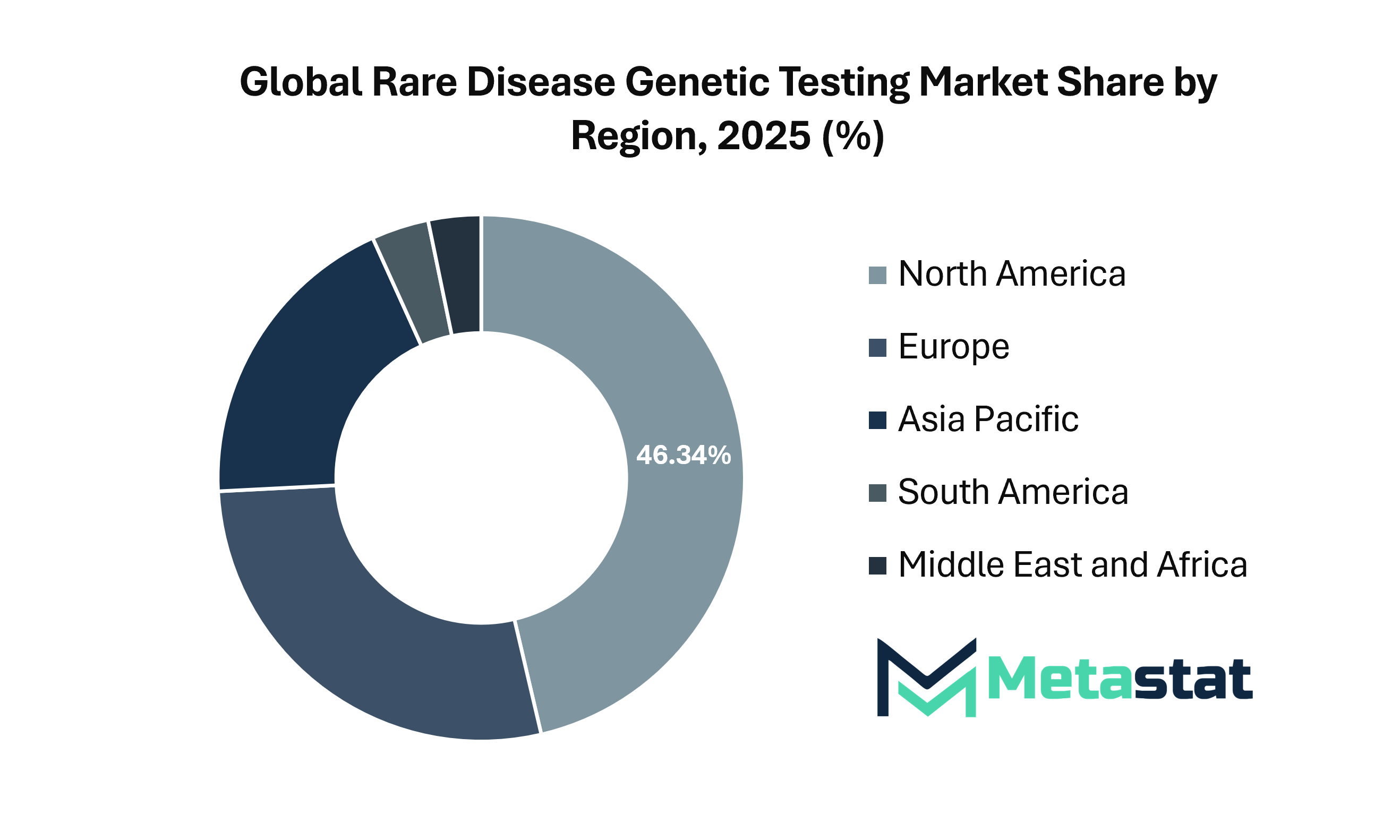

Based on geography, the global rare disease genetic testing market is divided into North America, Europe, Asia-Pacific, South America, and Middle East & Africa. North America is further divided in the U.S., Canada, and Mexico, whereas Europe consists of the UK, Germany, France, Italy, and Rest of Europe. Asia-Pacific is segmented into India, China, Japan, South Korea, and Rest of Asia-Pacific. The South America region includes Brazil, Argentina, and the Rest of South America, while the Middle East & Africa is categorized into GCC Countries, Egypt, South Africa, and Rest of Middle East & Africa.

North America was dominating the rare disease genetic testing market, due to the rising incidence of rare disorders, rising awareness regarding the rare disease genetic testing, commercialization of new testing technique for rare disease, and partnership between pharmaceutical companies and other health care institutes to introduce Rare Disease Institute (RDI). For instance, Prognos Health, an AI-driven platform company focused on predicting the trajectory of disease to drive informed decisions earlier in the patient journey, has introduced the Rare Disease Institute (RDI).The RDI is partnering with pharmaceutical companies, reference and genetic testing labs, health systems/academic centers, patient advocacy groups and innovative technology companies to improve testing and therapies for patients, educate patients and physicians on the latest in diagnostics, and empower the pharmaceutical industry with the development of new therapies to treat and cure rare disease.

Competitive landscape

Key players operating in the rare disease genetic testing industry include Quest Diagnostics Inc., Strand Life Sciences, Myriad Genetics, Centogene N.V., Perkin Elmer, 3billion Inc., Invitae Corporation, Baylor Genetics, Ambry Genetics, Macrogen Inc., Preventiongenetics, Opko Health Inc., Progenity Inc., and Fulgent Genetics Inc.

The strategic mergers & acquisitions between companies to expand their offerings and strengthen their presence in this market, increasing clinical studies on rare disease genetic testing technique, commercialization of rare disease genetic testing technique, and extending partnership between companies to continue the diagnose of rare genetic disorders patients are some of the strategies adopted by the major companies. For instance, on April 14, 2021, Centogene N.V., a commercial-stage company focused on rare diseases has extended its partnership with Takeda Pharmaceutical Company Limited to diagnose patients with rare genetic disorders. The partnership has extended until March 2022, under which CENTOGENE will continue to provide rare genetic testing to patients around the world.

India Human Dermal and Amniotic Tissue Market Size, Share, Trends, 2033

India Human Dermal and Amniotic Tissue market size is valued at USD 119.1 million in 2025 and is projected to reach USD 351.1 million in 2033, at a CAGR of 14.5% from 2026 to 2033

India Human Dermal and Amniotic Tissue Market, India Human Dermal and Amniotic Tissue Market Size, India Human Dermal and Amniotic Tissue Market Share, India Human Dermal and Amniotic Tissue Market Analysis, India Human Dermal and Amniotic Tissue Market Growth, India Human Dermal and Amniotic Tissue Market Trends, India Human Dermal and Amniotic Tissue Market Research Report, India Human Dermal and Amniotic Tissue Market Forecast, India Human Dermal and Amniotic Tissue, India Human Dermal and Amniotic Tissue Market Research, India Human Dermal and Amniotic Tissue Industry, India Human Dermal and Amniotic Tissue Industry Report, India Human Dermal and Amniotic Tissue Market Data, India Human Dermal and Amniotic Tissue Statistics, India Human Dermal and Amniotic Tissue Market Statistics, India Human Dermal and Amniotic Tissue Industry Trends, India Human Dermal and Amniotic Tissue Market Report, India Human Dermal and Amniotic Tissue Market Trends, India Human Dermal and Amniotic Tissue Market News, India Human Dermal and Amniotic Tissue Forecasts, India Human Dermal and Amniotic Tissue Market Intelligence Report

Undenatured Type II Collagen Market Size, Share, Trends, 2033

Global Undenatured Type II Collagen market size is valued at USD 1,449.4 million in 2025 and is projected to reach USD 2,397.3 million in 2033, at a CAGR of 6.5% from 2026 to 2033

Undenatured Type II Collagen Market, Undenatured Type II Collagen Market Size, Undenatured Type II Collagen Market Share, Undenatured Type II Collagen Market Analysis, Undenatured Type II Collagen Market Growth, Undenatured Type II Collagen Market Trends, Undenatured Type II Collagen Market Research Report, Undenatured Type II Collagen Market Forecast, Undenatured Type II Collagen, Undenatured Type II Collagen Market Research, Undenatured Type II Collagen Industry, Undenatured Type II Collagen Industry Report, Undenatured Type II Collagen Market Data, Undenatured Type II Collagen Statistics, Undenatured Type II Collagen Market Statistics, Undenatured Type II Collagen Industry Trends, Undenatured Type II Collagen Market Report, Undenatured Type II Collagen Market Trends, Undenatured Type II Collagen Market News, Undenatured Type II Collagen Forecasts, Undenatured Type II Collagen Market Intelligence Report

Pure EPA Active Pharmaceutical Ingredient (API) Market Size, Share, Trends, 2033

Global Pure EPA Active Pharmaceutical Ingredient (API) market size is valued at USD 358.9 million in 2025 and is projected to reach USD 820.8 million in 2033, at a CAGR of 10.9% from 2026 to 2033

Pure EPA Active Pharmaceutical Ingredient (API) Market, Pure EPA Active Pharmaceutical Ingredient (API) Market Size, Pure EPA Active Pharmaceutical Ingredient (API) Market Share, Pure EPA Active Pharmaceutical Ingredient (API) Market Analysis, Pure EPA Active Pharmaceutical Ingredient (API) Market Growth, Pure EPA Active Pharmaceutical Ingredient (API) Market Trends, Pure EPA Active Pharmaceutical Ingredient (API) Market Research Report, Pure EPA Active Pharmaceutical Ingredient (API) Market Forecast, Pure EPA Active Pharmaceutical Ingredient (API), Pure EPA Active Pharmaceutical Ingredient (API) Market Research, Pure EPA Active Pharmaceutical Ingredient (API) Industry, Pure EPA Active Pharmaceutical Ingredient (API) Industry Report, Pure EPA Active Pharmaceutical Ingredient (API) Market Data, Pure EPA Active Pharmaceutical Ingredient (API) Statistics, Pure EPA Active Pharmaceutical Ingredient (API) Market Statistics, Pure EPA Active Pharmaceutical Ingredient (API) Industry Trends, Pure EPA Active Pharmaceutical Ingredient (API) Market Report, Pure EPA Active Pharmaceutical Ingredient (API) Market Trends, Pure EPA Active Pharmaceutical Ingredient (API) Market News, Pure EPA Active Pharmaceutical Ingredient (API) Forecasts, Pure EPA Active Pharmaceutical Ingredient (API) Market Intelligence Report

Global Shaking Incubators market size is valued at USD 1,322.6 million in 2025 and is projected to reach USD 2,357.4 million in 2033, at a CAGR of 7.5% from 2026 to 2033