Nutricosmetics Market Size, Share, By Product Type (Skin Care, Hair Care, Nail Care, and Others), By Ingredient Type (Collagen and Peptides, Vitamins and Minerals, Omega-3 and EFAs, Probiotics and Postbiotics, Botanical Extracts, and Others), By Form (Tablets and Capsules, Powders and Liquids, Gummies and Soft-Chews, and Others), By Distribution Channel (Supermarkets & Hypermarkets, Health & Beauty Stores, Online Retail & D2C, and Others), Industry Analysis, Growth, Trends, and Forecasts, 2026-2033

Report ID

MSI-4530

Published

February 17, 2026

Pages

257 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Market Overview

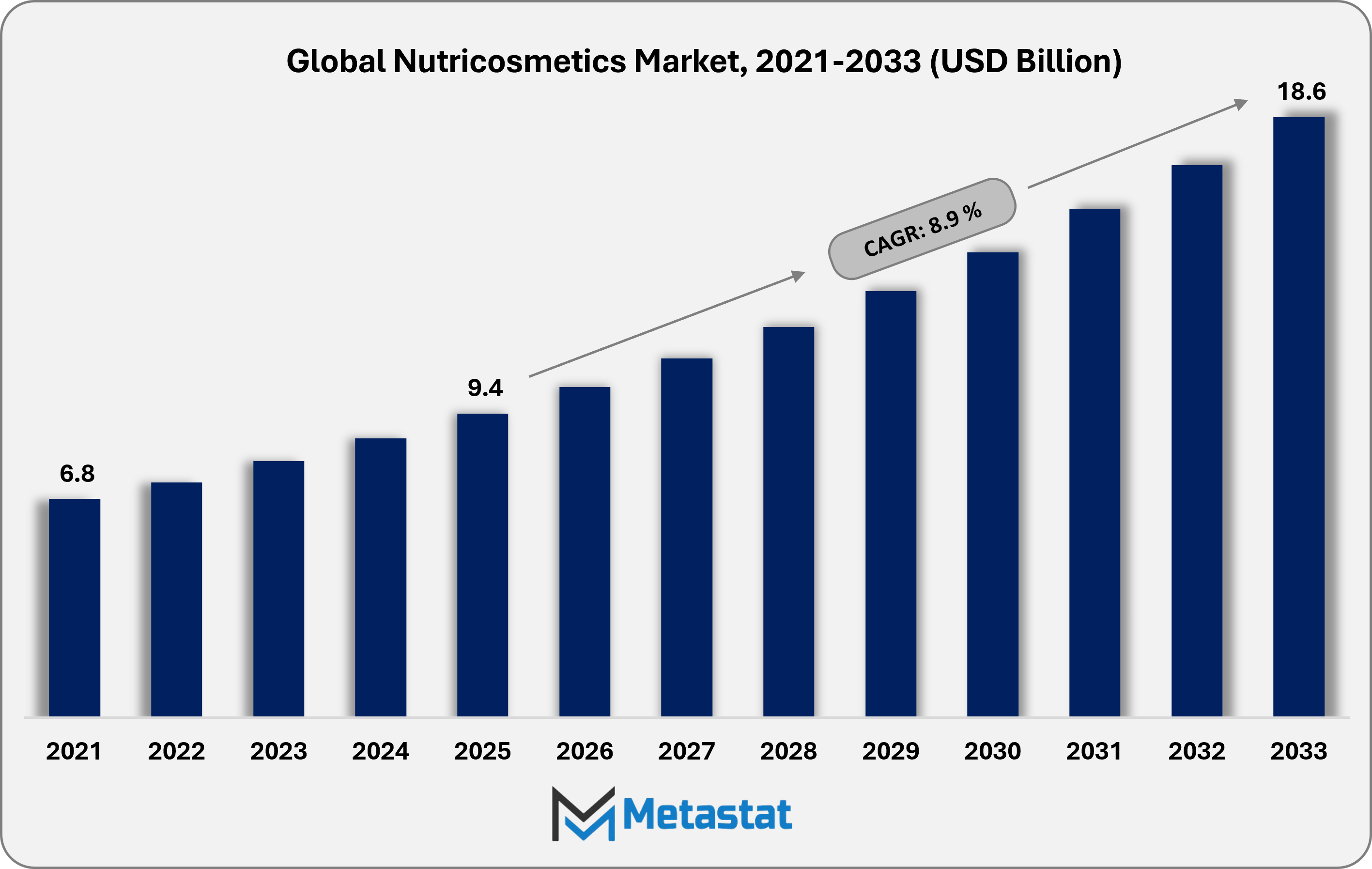

The global nutricosmetics market size was valued at USD 9.41 billion in 2025. The market is projected to grow from USD 10.2 billion in 2026 to USD 18.6 billion by 2033, exhibiting a CAGR of 8.9% during the forecast period.

Global Nutricosmetics Market Comprehensive Data-Driven Market Analysis & Strategic Outlook

The global nutricosmetics market was valued at USD 9.4 billion in 2025, growing at a CAGR of around 8.9% through 2033, with potential to exceed USD 18.6 billion.

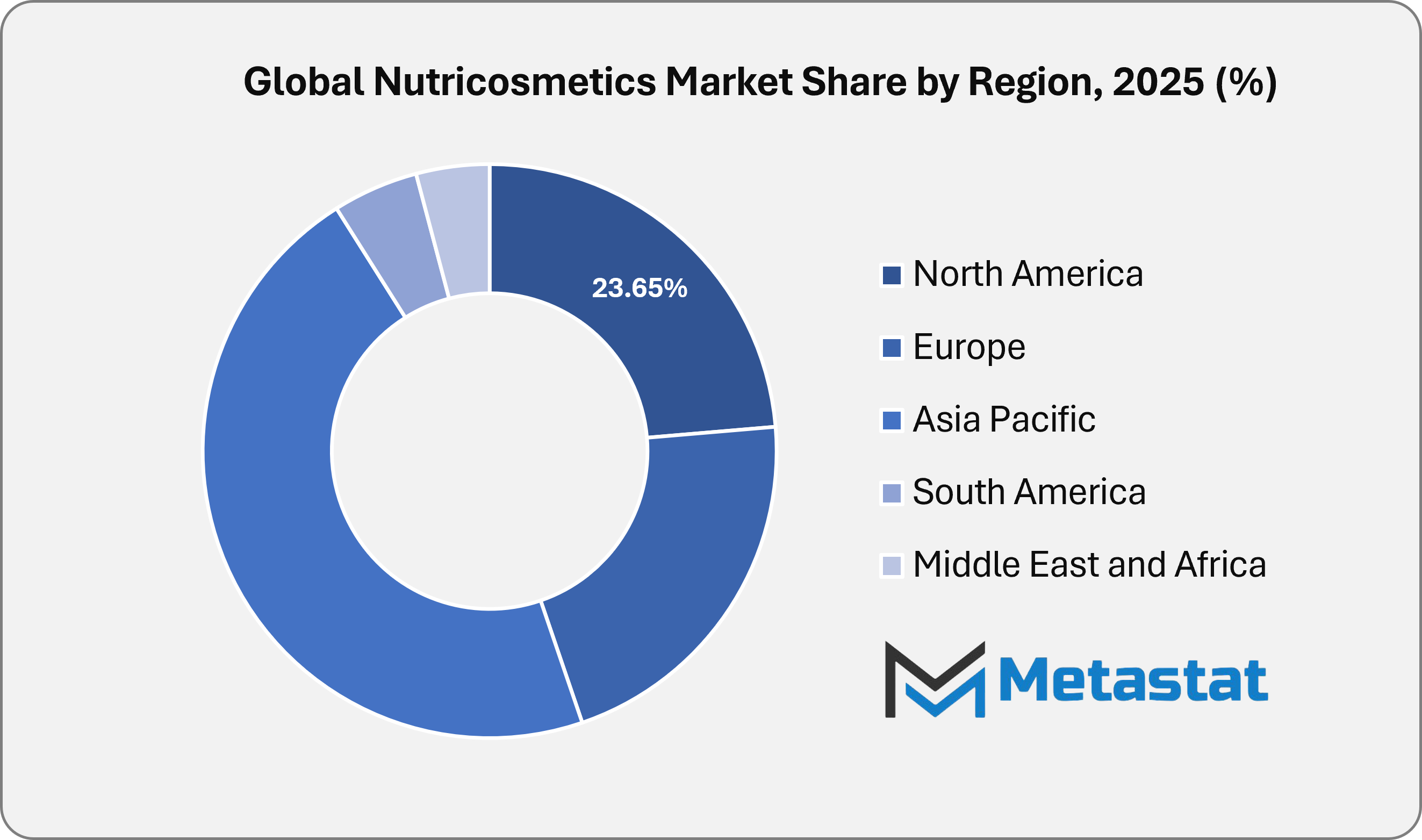

North America accounted for 23.7% of the nutricosmetics market in 2025, with the US leading the market share in 2026.

The Skin Care segment accounts for 57.6% of the nutricosmetics market share in 2025, driving innovation and expanding applications through clinically aligned multi-ingredient stacks combining collagen peptides, vitamin C, ceramides, hyaluronic acid, zinc, and antioxidant actives to support hydration, firmness, and barrier performance.

Rising consumer preference for beauty-from-within products supporting holistic wellness and growing awareness of anti-aging and skin rejuvenation benefits through nutritional supplements are key driving trends of nutricosmetics market.

Increasing innovation in personalized, plant-based, and collagen-enriched nutricosmetic formulations is an opportunity for the nutricosmetics market.

Key insight: Clinical-grade positioning and measurable beauty outcomes are expected to propel premiumization in nutricosmetics, with brands that pair evidence-backed actives, clean-label sourcing, and personalized formats likely to secure increased repeat purchases and stronger pricing power over the next decade.

The nutricosmetics market is shifting from occasional supplement consumption to integrated beauty routines, with consumers seeking outcomes for skin radiance, hydration, elasticity, hair density, and nail strength that fit preventive wellness priorities. The demand of nutricosmetics is being propelled by collagen peptides, hyaluronic acid, ceramides, biotin, carotenoids, and microbiome-oriented concepts delivered through gummies, powders, liquids, and functional beverages that emphasize taste, convenience, and measurable results. The direction is reinforced by the macro wellness backdrop, with the global wellness institute reporting that the wellness economy reached about USD 6,800 billion in 2024, growing by 7.9% from the previous year, highlighting the sustained consumer willingness to spend on integrated health and beauty routines.

The growth of the nutricosmetic market is expected to remain strong across the forecast period, with the brands set to increase clinical substantiation, strengthen third-party testing, and refine claim language around skin barrier support, anti-ageing, and hair-fall reduction. Subscription models and dermatologist-nutritionist collaborations are likely to increase repeat purchases, driven by rising preferences for personalized stacks and transparent ingredient sourcing. Large consumer goods players are validating the category's strategic relevance. For instance, Unilever's Beauty & Wellbeing business reported at Euro 13.2 billion in 2024 and delivering 6.5% underlying sales growth, supported by strong performance from its wellbeing brands, signalling increased competitive intensity and innovation pipelines in ingestible beauty.

Market Dynamics

Growth Drivers:

Rising Consumer Preference for Beauty-from-within Products Supporting Holistic Wellness

Consumers are connecting skin, hair, and nailcare outcomes with nutrition, sleep, stress balance, and gut health. Daily ingestible routines are gaining traction alongside topical regimens in urban and fitness-led groups. Gummies, powders, and ready-to-mix formats are improving adherence and lifestyle fit. The change of daily routine is expected to propel a sustained demand for science-led, preventive nutricosmetics.

Growing Awareness of Anti-Aging and Skin Rejuvenation Benefits through Nutritional Supplements

Increased exposure to clinical content is strengthening trust in collagen, antioxidants, ceramides, and hydrating blends. Users are seeking gradual, visible improvements in elasticity, hydration, and tone with consistent intake. Brands are expanding evidence-backed claims and dosage transparency to support credibility. The dynamic is likely to propel premium offerings and increased purchases of nutricosmetic products across all the age groups.

Restraints & Challenges:

High Product Cost and Limited Clinical Validation Affecting Consumer Trust

The premium pricing for collagen, ceramides, and specialty blends is narrowing nutricosmetics market adoption. The price-value audit is increasing in online channels where comparisons are immediate and frequent. Limited large-scale human trials in some claims are creating hesitation among new buyers. The combination is likely to slow brand switching and temper volume expansion in price-sensitive consumers.

Regulatory Inconsistencies across Regions Slowing Product Approvals

The legal health claims, ingredients and different labeling rules are complicating global launches in the nutricosmetics market. The major brands often need region-specific formulations and packaging, owing to an increase in deployment delays. Compliance costs are rising owing to increased inspection of efficacy and safety statements by authorities. The environment is expected to delay cross-border scale-up and constrain uniform portfolio strategies in the nutricosmetics market.

Opportunities:

Increasing Innovation in Personalized, Plant-Based, and Collagen-Enriched Nutricosmetic Formulations

The personalized collection of nutricosmetics aligned to age, lifestyle, and skin concerns are improving efficacy and loyalty. Plant-based actives and clean-label positioning are attracting vegan and sustainability-focused buyers to the nutricosmetic market. Next-generation collagen formats and synergistic blends are supporting improved bioavailability narratives. These opportunities are expected to propel growth and increased brand differentiation, owing to stronger alignment with individualized beauty goals.

Market Segmentation Analysis

The global Nutricosmetics market is mainly classified based on Product Type, Ingredient Type, Form, and Distribution Channel.

By Product Type, the market is further segmented into:

Skin Care

Skin care remains the primary source within the nutricosmetics market. Collagen peptides, hyaluronic acid, ceramides, antioxidants, and probiotic-led blends are supporting demand for hydration, elasticity, and barrier reinforcement. Cross-category adoption from dermatology, wellness, and preventive health is increasing purchase frequency. The clinically framed claims and routine-friendly formats will propel the growth in the nutricosmetics market.

Hair Care

Hairfall control, density support, and scalp health are strengthening consumer pull across all genders. Biotin, zinc, amino acids, marine and plant proteins, and adaptogen-based formulas are getting attention in the nutricosmetics market. The influencer-led routines and digital education are increasing trial and adoption.

Nail Care

Nail strength, brittleness reduction, and faster growth benefits are shaping nail care into a focused, performance-led subcategory. Formulations featuring biotin, collagen, silica, and trace minerals are supporting demand for targeted, outcome-driven approaches. Bundled hair-skin-nail offerings are increasing visibility while strengthening value insight.

Others

The others category includes emerging areas owing to oral beauty, body firming, pigmentation support, and microbiome-linked beauty concepts. Major brands are exploring botanicals, carotenoids, and functional beverage formats to widen consumer entry points. Innovation in clean-label, sugar-managed gummies and ready-to-drink options is increasing addressable demand in the nutricosmetics market. The others segment is expected to propel corner mainstream transitions, owing to accelerated product experimentation.

By Ingredient Type, the market is divided into:

Collagen and Peptides

Collagen and peptides support consumable beauty positioning owing to skin firmness, elasticity, and hydration. Marine and bovine sources, along with targeted peptide blends, are increasingly combined with vitamin C and hyaluronic acid to boost bioavailability and efficacy narratives in the nutricosmetics market. Consumers are adopting powders, sticks, and gummies, propelled by premium branding and improved taste profiles.

Vitamins and Minerals

Vitamins and minerals are expected to maintain broad demand across skin brightness, hair strength, and nail resilience propositions. Biotin, zinc, selenium, and vitamins A, C, D, and E dominate multi-benefit formulas in mainstream and premium ranges in the nutricosmetics market. Purchase frequency is increasing in daily wellness routines, owing to familiar ingredients and accessible pricing of nutricosmetic products.

Omega-3 and EFAs

Omega-3 and EFA offerings, which target skin barrier function, dryness management, and inflammation modulation, support the nutricosmetic market. Clean-label fish, algal, and plant-derived oils are strengthening trust among health-led consumers. Cross-category overlap with heart and cognitive wellness is expanding addressable demand and supporting increased repeat purchases in the nutricosmetic market.

Probiotics and Postbiotics

Probiotics and postbiotics are shaping gut-skin axis positioning centered on acne support, sensitivity reduction, and overall clarity. Shelf-stable strains, synbiotic combinations, and multi-format delivery systems are making swiftly innovation in the nutricosmetic market. Consumer familiarity is rising rapidly, propelled by broader digestive health adoption and clearer clinical communication.

Botanical Extracts

Botanical extracts diversify formulations across antioxidant protection, brightening, and stress-linked beauty claims. Astaxanthin, green tea, grape seed, turmeric, and adaptogens are gaining interest within clean-label portfolios. Demand for botanical extracts is increasing among younger groups, owing to plant-forward preferences and premium storytelling in the nutricosmetics market.

Others

The others category includes ceramides, hyaluronic acid, coenzymes, and emerging bioactives that extend beyond standard skin-hair-nail stacks. Brands are building synergistic combinations to differentiate in crowded assortments and strengthen evidence-led claims. Functional beverages and advanced gummy systems are widening entry points and supporting increased trial in the nutricosmetics market.

By Form, the market is further divided into:

Tablets and Capsules

Tablets and capsules remain a mature, trust-led format within nutricosmetics market, valued for dose precision and clean, clinical positioning. Brand portfolios continue to expand with multi-ingredient skin-hair-nail stacks that fit daily routines. The demand for tablets and capsules has led to the development of pharmacy-led credibility and cost-efficient pack sizes, which support consistent replenishment in the nutricosmetics market.

Powders and Liquids

Powders and liquids are strengthening their role in a premium and performance-focused approach centered on collagen, peptides, and hydration blends. Fast-mix convenience and flavour-led innovation are supporting increased adherence in fitness-aligned consumers. Adoption of these powder and liquid products is rising in online and specialty channels, owing to stronger perceived potency and flexible dosage options.

Gummies and Soft-Chews

Gummies and soft chews are driving accessibility with sensory appeal and simplified daily intake. This product format is particularly effective in first-time user conversion and younger demographics seeking enjoyable wellness habits. Brand innovation in low-sugar, clean-label, and functional combinations is helping propel repeat purchases and premium extensions.

Others

The others segment includes emerging delivery formats such as functional shots, ready-to-drink beauty beverages, and dissolvable strips. These formats are gaining attention in convenience-led and on-the-go consumption occasions. The interest in nutricosmetics products is increasing with brand differentiation strategies and lifestyle positioning that reinforces beauty-from-within routines.

By Distribution Channel, the global Nutricosmetics market is divided as:

Supermarkets & Hypermarkets

Supermarkets and hypermarkets provide high-visibility access for mass and mid-tier nutricosmetics, supporting impulse-led trial and bundled wellness purchases. Brand-led shelf education, sampling, and value packs are reinforcing routine adoption in mainstream consumer cohorts. Share stability is supported by price competitiveness and broad reach, owing to strong footfall and cross-category merchandising.

Health & Beauty Stores

Health and beauty stores strengthen premium positioning through expert-assisted selling and curated consumable beauty assortments. Dermatology-aligned recommendations and category specialists improve consumer confidence in collagen, probiotic, and antioxidant-based procedures. Health and beauty stores are rising with targeted launches and exclusive SKUs that propel repeat purchases and brand loyalty.

Online Retail & D2C

Online retail and D2C channels are accelerating category expansion through education-led discovery, subscriptions, and personalized regimen builders in the nutricosmetics market. Influencer-driven content, reviews, and clinical storytelling are increasing conversion and reducing trial barriers. Data-led product optimization and faster innovation cycles reinforce momentum, owing to direct consumer feedback loops.

Others

The others category includes pharmacies and specialty nutrition outlets, which support credibility-led purchases and targeted solutions aligned to specific beauty concerns. The contribution from other channels is strengthening owing to Omni channel strategies and premium sampling programs that enhance awareness and encourage routine adherence.

By Region:

Based on geography, the global Nutricosmetics market is divided into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

North America Nutricosmetics Market is set to expand at a CAGR of 8.9% within the forecast period, reaching a market size (TAM) of USD 4.4 billion by the end of 2033.

Holistic wellness culture and high supplement penetration are accelerating ingestible beauty adoption across North America. Consumers of nutricosmetic products link gut health, inflammation management, and healthy aging with visible skin and hair outcomes, supporting daily use of collagen, ceramides, and microbiome-oriented stacks.

Plant-forward actives, fermentation-led concepts, and functional beverage formats match everyday consumption habits and increase trial rates. Localized flavour profiles and culturally familiar botanicals support faster acceptance and premium storytelling, owing to their strong resonance with heritage wellness cues in the Asia-Pacific region.

Urban consumers in the Middle East, Africa, and leading Latin American economies are showing increased interest in preventive wellness routines that extend into ingestible beauty. Price sensitivity, import reliance, and cross-country regulatory variation elevate the importance of tiered portfolios, pharmacy-led credibility, and clear, locally compliant claims.

Competitive Landscape & Strategic Insights

Competitive intensity in nutricosmetics reflects a mix of global nutrition leaders, beauty multinationals, and high-credibility wellness platforms shaping category standards and consumer expectations. Amway Corporation and Herbalife Nutrition Ltd continue to leverage relationship-led selling and regimen-based education, while Nestle Health Science and Unilever bring scale, clinical framing, and adjacent wellbeing portfolios that support cross-category penetration. Shiseido Company Ltd, Suntory Holdings Ltd, Kirin Cosmetics Co., Ltd., FANCL Corporation, DHC Corporation, Orihiro Co., Ltd., and LG Household & Health Care Co., Ltd. strengthen Asia-led innovation in beauty-from-within through strong alignment to functional formats and premium brand equity. GNC Holdings LLC and Vitabiotics Ltd add broad retail visibility and science-positioned portfolios that boost mainstream trust, alongside Viviscal Limited and BioCell Technology LLC that retain specialist credibility within hair health and collagen-centric propositions.

Ingredient provenance, format innovation, and clinical storytelling increasingly define strategic differentiation, elevating brand trust and supporting premium pricing. Australia-origin players such as Blackmores Ltd, Swisse Wellness Pty Ltd, The Beauty Chef Pty Ltd, Vida Glow, and Advanced Nutrition Programme are pushing premium collagen, gut-skin axis, and clean-label narratives, supported by strong export momentum and lifestyle-led brand building. US and global digital-native brands including HUM Nutrition Inc, Olly Public Benefit Corp, Moon Juice, The Nue Co., and LYMA Life are accelerating personalization, subscription models, and influencer-healthcare crossover education to increase repeat purchases. Kora Organics and Wow Skin Science reinforce clean beauty adjacency and India-led accessibility, while GELITA AG represents a critical upstream enabler of high-purity collagen and peptide innovation that helps brand partners improve efficacy claims and sensory performance. Portfolio strategy across these players is moving toward modular skin-hair-nail stacks and microbiome-aligned offerings, propelled by increased consumer focus on measurable outcomes and preventive beauty routines.

Forecast & Statistical Outlook

Market size is forecast to rise from USD 9.4 billion in 2025 to over USD 18.6 billion by 2033.

Nutricosmetics is likely to maintain strong momentum over the forecast period as beauty-from-within routines become a mainstream extension of daily wellness. Premiumization will rise as clinically validated collagen, ceramides, probiotics, and multi-active stacks gain larger market shares in the nutricosmetics sector. In both mature and emerging markets, personalization, subscriptions, and condition-specific procedures will propel retention and lifetime value. Innovation in plant-based actives, low-sugar gummies, functional beverages, and advanced delivery systems will reinforce trial and repeat purchases. Regulatory tightening around claims and quality standards led to elevate entry barriers while improving consumer confidence in validated brands. Competitive strategies will increasingly prioritize evidence, ingredient traceability, and omnichannel education, owing to rising expectations for measurable outcomes.

LG Household & Health Care Co., Ltd. (LG H&H Co., Ltd.)

The Beauty Chef Pty Ltd

Vida Glow

Advanced Nutrition Programme

Moon Juice

The Nue Co.

LYMA Life

Synbiotic SE

GELITA AG

Report Coverage

This research report categorizes the nutricosmetics market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the nutricosmetics market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the nutricosmetics market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 8.9% from 2026 to 2033

Revenue Unit

USD billion

Sales Volume Unit

Kilotons

Segmentation

By Product Type, Ingredient Type, Form, Distribution Channel, and Region

By Product Type

Skin Care

Hair Care

Nail Care

Others

By Ingredient Type

Collagen and Peptides

Vitamins and Minerals

Omega-3 and EFAs

Probiotics and Postbiotics

Botanical Extracts

Others

By Form

Tablets and Capsules

Powders and Liquids

Gummies and Soft-Chews

Others

By Distribution Channel

Supermarkets & Hypermarkets

Health & Beauty Stores

Online Retail & D2C

Others

By Region

North America (By Product Type, Ingredient Type, Form, Distribution Channel, and Country)

United States

Canada

Mexico

Europe (By Product Type, Ingredient Type, Form, Distribution Channel, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of the Europe

Asia Pacific (By Product Type, Ingredient Type, Form, Distribution Channel, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Product Type, Ingredient Type, Form, Distribution Channel, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Product Type, Ingredient Type, Form, Distribution Channel, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Nutricosmetics Industry Statistics

Nutricosmetic Products Landscape

Nutricosmetic Company Analysis

Insights on skin minimalism and digital influence in the industry

Insight on nutricosmetics for menopause skin health

Key market analysis for microbiome-friendly beauty supplements

Emerging trends on skin-boosting beverages / beauty drinks

Snippet on 3D printed personalized supplements

Full in-depth analysis of the parent Industry

Important changes in market and its dynamics

Segmentation details of the market

Former, on-going, and projected market analysis in terms of volume and value

Kazakhstan Frozen Potato Products market size is valued at USD 26.4 million in 2025 and is projected to reach USD 53.0 million in 2033, at a CAGR of 9.0% from 2026 to 2033.

Switzerland Poke Food market size is valued at USD 29.2 million in 2025 and is projected to reach USD 44.5 million in 2033, at a CAGR of 5.5% from 2026 to 2033.

Netherlands Food and Beverages QA, QC, and Compliance Software Solutions Market Size, Share, Trends, 2033

Netherlands F&B QA, QC, and Compliance Software Solutions market size is valued at USD 272.5 million in 2025 and is projected to reach USD 421.3 million in 2033, at a CAGR of 5.6% from 2026 to 2033.

Netherlands F&B QA, QC, and Compliance Software Solutions Market, Netherlands F&B QA, QC, and Compliance Software Solutions Market Size, Netherlands F&B QA, QC, and Compliance Software Solutions Market Share, Netherlands F&B QA, QC, and Compliance Software Solutions Market Analysis, Netherlands F&B QA, QC, and Compliance Software Solutions Market Growth, Netherlands F&B QA, QC, and Compliance Software Solutions Market Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market Research Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Forecast, Netherlands F&B QA, QC, and Compliance Software Solutions, Netherlands F&B QA, QC, and Compliance Software Solutions Market Research, Netherlands F&B QA, QC, and Compliance Software Solutions Industry, Netherlands F&B QA, QC, and Compliance Software Solutions Industry Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Data, Netherlands F&B QA, QC, and Compliance Software Solutions Statistics, Netherlands F&B QA, QC, and Compliance Software Solutions Market Statistics, Netherlands F&B QA, QC, and Compliance Software Solutions Industry Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market News, Netherlands F&B QA, QC, and Compliance Software Solutions Forecasts, Netherlands F&B QA, QC, and Compliance Software Solutions Market Intelligence Report

Global Antibiotic-Free Pork market size is valued at USD 25,430.6 million in 2025 and is projected to reach USD 42,528 million in 2033, at a CAGR of 6.6% from 2026 to 2033