MARKET OVERVIEW

The North America Gluten-Free Flour market within the food industry, showcasing a remarkable shift in consumer preferences and dietary choices. This sector, integral to the broader food market, has witnessed a transformative journey, reflecting the changing needs and health-conscious mindset of the population.

In recent years, the North America Gluten-Free Flour market has emerged as a vital player in the food industry, responding to the escalating demand for gluten-free alternatives. This surge is deeply rooted in the growing awareness of gluten-related health issues and an increasing number of individuals adopting gluten-free diets due to gluten sensitivity or celiac disease.

The industry has experienced a paradigm shift in product offerings, with a diverse range of gluten-free flours becoming more accessible and appealing to consumers. Traditional staples like wheat flour are being replaced by innovative alternatives such as almond flour, coconut flour, and chickpea flour, providing not only gluten-free options but also catering to a broader spectrum of dietary preferences.

One of the driving forces behind the evolution of the North America Gluten-Free Flour market is the rise of health-conscious consumerism. As individuals become more informed about the impact of dietary choices on well-being, there is a discernible trend towards embracing gluten-free lifestyles. This shift is not merely a passing fad but rather a fundamental change in how people perceive and prioritize their nutritional intake.

Industry has responded to this demand by fostering innovation in product development. Manufacturers are continually exploring new formulations and combinations to enhance the nutritional profile, taste, and texture of gluten-free flours. This commitment to innovation is reshaping the market, ensuring that gluten-free options are not just seen as substitutes but as viable and delectable choices.

Beyond consumer preferences, the North America Gluten-Free Flour market has also been influenced by the broader socio-economic landscape. The increasing prevalence of gluten-related health issues has prompted regulatory bodies to scrutinize food labeling and ingredient transparency. This has resulted in a more stringent regulatory environment, ensuring that products labeled as gluten-free genuinely meet the required standards.

Furthermore, the market dynamics are also shaped by the collaborative efforts of various stakeholders, including food manufacturers, health professionals, and consumer advocacy groups. The shared goal of promoting gluten-free alternatives has led to increased awareness campaigns, educational initiatives, and the establishment of support networks for individuals navigating gluten-free lifestyles.

The North America Gluten-Free Flour market stands at the forefront of a dietary revolution, driven by health-conscious consumerism and an increased understanding of gluten-related health issues. This industry’s vibrant landscape reflects a commitment to providing diverse, innovative, and quality gluten-free options, ensuring that individuals can make informed choices that align with their health and lifestyle preferences.

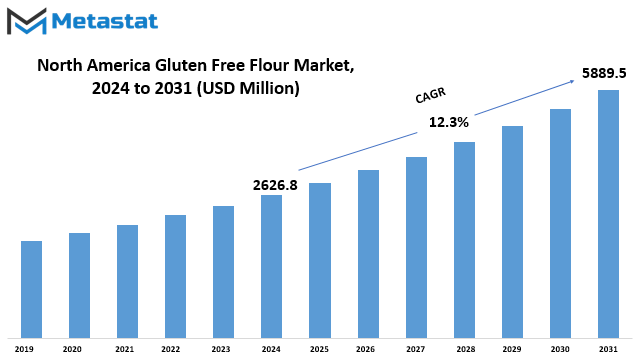

North America Gluten Free Flour market is estimated to reach $5889.5 Million by 2031; growing at a CAGR of 12.3% from 2024 to 2031.

GROWTH FACTORS

In recent times, the North American Gluten-Free Flour market has experienced notable shifts, influenced by various factors shaping consumer preferences and industry dynamics. This essay will delve into the key drivers, restraints, and opportunities that characterize this market.

One significant driver propelling the growth of the North American Gluten-Free Flour market is the increasing awareness of health among consumers. As individuals become more conscious of their well-being, there is a growing inclination towards dietary choices that align with healthier lifestyles. This shift in consumer behavior has created a demand for gluten-free alternatives, driving the expansion of the market.

Another driving force behind the market's momentum is dietary diversification. Consumers are exploring and adopting diverse diets, including gluten-free options, for reasons ranging from personal health goals to addressing specific dietary restrictions. This trend has led to an expanded market share for gluten-free flour, as it caters to the needs of those seeking alternative dietary choices.

However, the market is not without its challenges. One notable restraint is the higher cost associated with gluten-free flour compared to traditional counterparts. The increased production expenses and specialized processing contribute to a higher price point, limiting its accessibility to a broader consumer base.

Additionally, taste and texture challenges pose a restraint to the widespread adoption of gluten-free flour. Some consumers find it challenging to reconcile the distinctive taste and texture of gluten-free products with their accustomed preferences, leading to hesitancy in embracing these alternatives.

Amidst these challenges, there lies a significant opportunity within the food service and hospitality sector. The increasing demand for gluten-free options in restaurants, cafes, and other food establishments creates a potential avenue for market growth. Businesses in the foodservice industry can tap into this opportunity by incorporating gluten-free flour into their offerings, catering to the evolving preferences of their clientele.

The North American Gluten-Free Flour market reflects the evolving landscape of consumer choices and industry trends. The drivers of health awareness and dietary diversification push the market forward, while challenges related to cost and taste hinder its widespread acceptance. Nevertheless, the opportunity within the foodservice and hospitality sector provides a promising outlook for the continued expansion of the gluten-free flour market in North America.

MARKET SEGMENTATION

By Type of Flour

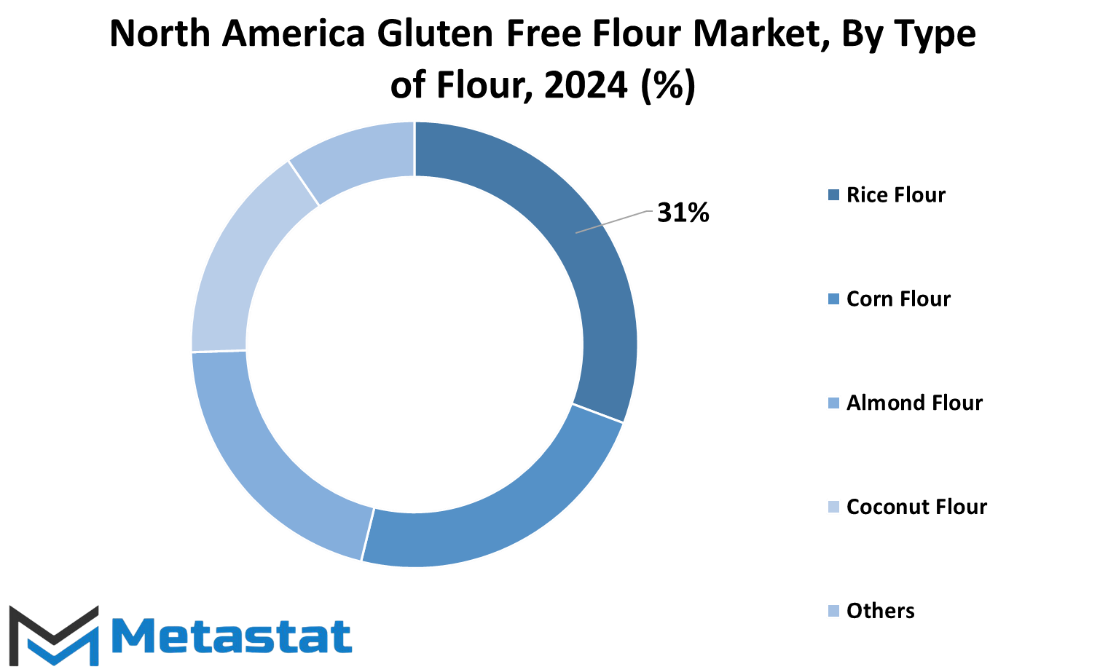

In the North American Gluten-Free Flour market, the classification based on the type of flour is more detailed, encompassing Rice Flour, Corn Flour, Almond Flour, Coconut Flour, and others. This market analysis dissects the diverse types of gluten-free flour available, offering insights into the specific varieties that consumers can choose from.

The North American market for gluten-free flour is intricately divided by the type of flour it comprises. Rice Flour, known for its versatility, stands as one of the options for those seeking gluten-free alternatives. Corn Flour, with its distinct texture and flavor, represents another viable choice. Almond Flour, appreciated for its nutty taste, provides yet another avenue for those adhering to a gluten-free diet. Coconut Flour, derived from coconuts, adds to the array of options available.

The segmentation doesn't end here; it also includes other types of gluten-free flours, expanding the horizon for consumers who may have specific preferences or dietary requirements. This detailed breakdown enables a comprehensive understanding of the North American Gluten-Free Flour market, allowing consumers and industry players alike to navigate the choices available with greater clarity.

The North American Gluten-Free Flour market, categorized by the type of flour, exhibits a dynamic landscape. In 2022, the Rice Flour segment commanded a noteworthy value of 650.6 USD Million. Simultaneously, the Corn Flour segment contributed significantly with a value of 497.3 USD Million. Almond Flour, gaining prominence, held a valuation of 439.1 USD Million. The Coconut Flour segment carved its place, securing a value of 339.3 USD Million. Additionally, the Others segment made a substantial impact, registering a value of 208.4 USD Million in the same year.

This segmentation sheds light on the diverse preferences within the gluten-free flour market, where each flour type establishes its unique position based on consumer demand and market trends. The Rice Flour segment, leading in value, signifies its popularity or perhaps its versatile applications in various culinary endeavors. Meanwhile, the Corn Flour segment, closely trailing, reflects its widespread use and consumer acceptance.

Almond Flour's impressive valuation indicates a growing interest in alternative flours, possibly due to perceived health benefits or culinary innovations. Coconut Flour, with its distinct flavor and nutritional attributes, has found a considerable market share. The Others segment, while not specified, underscores the existence of various flour types catering to specific consumer needs and preferences.

The North American Gluten-Free Flour market, dissected by flour types, exemplifies a vibrant industry with each segment contributing uniquely to its overall dynamics. Consumer choices, culinary trends, and nutritional considerations collectively shape the trajectory of this market, making it a fascinating sector to observe and analyze.

By Source

In the North American gluten-free flour market, various sources contribute to its diversity. These sources are categorized into Grains, Nuts, Seeds, and Others. Each segment holds a distinct value, reflecting the market dynamics in 2022.

The Grains segment, accounting for a substantial portion, was valued at 1147.9 USD Million. This signifies the significance of grain-based gluten-free flour products in the market. On the other hand, the Nuts segment, with a value of 778.4 USD Million, highlights the popularity and economic contribution of nut-derived gluten-free flour.

Seeds, another integral source in this market, attained a value of 72.9 USD Million in 2022. This showcases the consistent demand and market presence of seed-based gluten-free flours. Furthermore, the Others segment, with a value of 135.4 USD Million, encompasses additional sources, contributing to the overall market diversity.

The North American gluten-free flour market thrives on the varied sources, each segment playing a crucial role in shaping the market landscape. The market's dynamism is evident through the distinct values attributed to Grains, Nuts, Seeds, and Others, reflecting the evolving preferences and economic dimensions within the gluten-free flour industry.

By Distribution Channel

In the North American gluten-free flour market, the distribution channels play a pivotal role in reaching consumers. These channels are categorized into Supermarkets and Hypermarkets, Specialty Stores, Online Retail, and Others.

Supermarkets and Hypermarkets form a significant part of this market’s distribution network. These large retail spaces provide a wide array of products, making them accessible to a broad customer base. Customers often find gluten-free flour alongside conventional flours, enhancing convenience.

Specialty Stores, another segment in the distribution network, cater specifically to niche markets. These stores focus on offering a curated selection of gluten-free products, attracting consumers seeking specialized dietary options. This targeted approach enhances the shopping experience for individuals with specific dietary needs.

The Online Retail sector has witnessed a notable surge in recent times. With the convenience of online shopping, consumers can easily access gluten-free flour from the comfort of their homes. This distribution channel has expanded the market’s reach, particularly appealing to those looking for a hassle-free shopping experience.

The category labeled as Others encompasses various outlets that may include local grocery stores or smaller retailers. These outlets, though not falling into the categories, still contribute to the overall distribution of gluten-free flour in the market.

The North American gluten-free flour market is intricately connected to diverse distribution channels. Supermarkets and Hypermarkets offer broad accessibility, Specialty Stores cater to niche preferences, Online Retail provides convenience, and the Others category captures additional outlets contributing to the availability of gluten-free flour for consumers with varying dietary requirements.

By Application

The North America Gluten Free Flour market is segmented based on its applications, categorizing it into Bakery Products, Snacks and Convenience Foods, Ready to Eat Food Products, Pasta and Noodles, and Others. This segmentation offers a comprehensive understanding of how gluten-free flour is utilized across various food categories in the region.

Bakery Products represent a significant sector where gluten-free flour finds its application. The demand for gluten-free alternatives in baking has risen, catering to consumers with dietary restrictions or those seeking healthier alternatives.

Snacks and Convenience Foods, gluten-free flour plays a pivotal role. As consumer preferences shift towards healthier snacking options, the market for gluten-free snacks has seen growth. The versatile nature of gluten-free flour allows for the creation of a diverse range of snack products to meet this demand.

Ready to Eat Food Products also embrace the use of gluten-free flour. The convenience and quick preparation of these foods align with the contemporary lifestyle, and the inclusion of gluten-free options caters to a broader consumer base.

Pasta and Noodles, another significant segment, witnesses the incorporation of gluten-free flour to meet the dietary needs of individuals with gluten sensitivity. This adaptation reflects the industry's responsiveness to the diverse dietary requirements of consumers.

The category labeled as Others encapsulates various applications where gluten-free flour finds use. This flexible category allows for the inclusion of emerging trends and novel applications, showcasing the dynamic nature of the market.

The North America Gluten Free Flour market, through its diversified applications in Bakery Products, Snacks and Convenience Foods, Ready to Eat Food Products, Pasta and Noodles, and Others, reflects the evolving landscape of consumer preferences and dietary choices. This segmentation sheds light on the widespread adoption of gluten-free alternatives in the region's food industry, catering to a diverse range of consumer needs.

REGIONAL ANALYSIS

The North American gluten-free flour market can be segmented into the United States, Canada, and Mexico. Each country plays a distinct role in shaping the regional gluten-free flour landscape. The market's dynamics in the United States differ from those in Canada and Mexico, reflecting unique consumer preferences and economic influences.

In the U.S., the gluten-free flour market showcases a robust growth pattern, driven by an increasing awareness of gluten-related issues and a growing health-conscious population. Consumers here are inclined towards gluten-free alternatives, influencing the market trends and product innovations. This has led to a diverse range of gluten-free flours available, catering to various dietary needs and preferences.

Canada, on the other hand, exhibits a slightly different scenario. While the awareness of gluten-free options is on the rise, the market growth is characterized by a balanced blend of health-conscious choices and traditional preferences. The gluten-free flour market in Canada is evolving steadily, with consumers seeking a harmonious integration of gluten-free products into their culinary routines.

In Mexico, the gluten-free flour market is gaining traction as dietary awareness expands. The Mexican consumer landscape is witnessing a shift towards healthier choices, and gluten-free alternatives are becoming increasingly popular. However, the market in Mexico is still in its developmental phase compared to the more mature markets in the U.S. and Canada.

Despite these variations, the overarching theme across North America is the increasing acceptance and incorporation of gluten-free flour into daily diets. The market's diversity reflects the nuanced culinary and dietary landscapes of each country, providing a rich tapestry of options for consumers seeking gluten-free alternatives. As the awareness of gluten-related concerns continues to grow, the North American gluten-free flour market is poised for further evolution, adapting to the unique demands of consumers in the U.S., Canada, and Mexico alike.

COMPETITIVE PLAYERS

In the realm of the North America Gluten Free Flour market, several key players are actively participating in shaping the industry. These competitive entities are pivotal in influencing the market dynamics and meeting the demands of consumers seeking gluten-free alternatives.

Among the prominent competitors in the Gluten Free Flour industry are General Mills, Inc (commonly known for Pillsbury products), Ardent Mills (operating under the name Firebird Artisan Mills), Hometown Food Company (recognized for Arrowhead Mills), Bob’s Red Mill Natural Foods, Better Batter Gluten Free Flour, The Kroger Co., Nature's Eats Inc., King Arthur Baking Company, Petley Grain LLC, and Blue Diamond Growers.

These companies play a crucial role in catering to the growing demand for gluten-free products, contributing to the diverse choices available to consumers. The market is significantly impacted by the offerings and strategies of these key players, reflecting the competitive landscape of the Gluten Free Flour industry in North America.

North America Gluten Free Flour Market Key Segments:

By Type of Flour

- Rice Flour

- Corn Flour

- Almond Flour

- Coconut Flour

- Others

By Source

- Grains

- Nuts

- Seeds

- Others

By Distribution Channel

- Supermarkets and Hypermarkets

- Specialty Stores

- Online Retail

- Others

By Application

- Bakery Products

- Snacks and Convenience Foods

- Ready to Eat Food Products

- Pasta and Noodles

- Others

Key North America Gluten Free Flour Industry Players

- General Mills, Inc (Pillsbury)

- Ardent Mills (Firebird Artisan Mills)

- Hometown Food Company (Arrowhead Mills)

- Bob’s Red Mill Natural Foods

- Better Batter Gluten Free Flour

- The Kroger Co.

- Nature's Eats Inc.

- King Arthur Baking Company

- Petley Grain LLC

- Blue Diamond Growers

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential

US: +1 3023308252

US: +1 3023308252