Foodservice Market Size, Share, By Foodservice Type (Cafes, Bars, Cloud Kitchens, Full-Service Restaurants, QSR, and Others), By Outlet (Chained Outlets and Independent Outlets), By Service Type (Dine-in, Takeaway, and Delivery), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4545

Published

February 10, 2026

Pages

310 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Leader

Report Details

Comprehensive Market Analysis And Insights

Market Overview

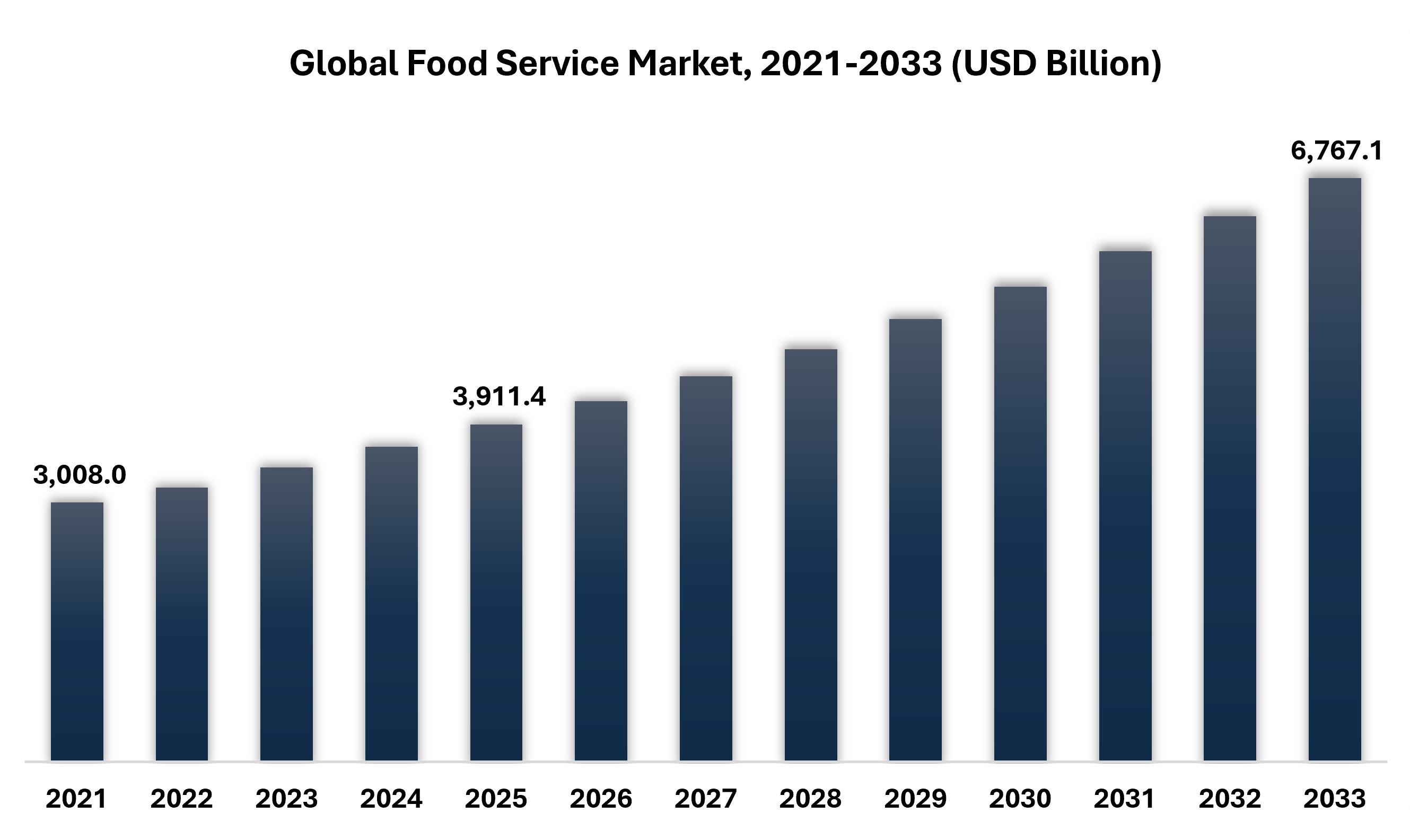

The global Food Service market size is valued at USD 3,911.4 billion in 2025.and is projected to grow from USD 4,185 billion in 2026 to USD 6,767.11 billion by 2033, exhibiting a CAGR of 7.1%

Global Food Service Market Comprehensive Data-Driven Market Analysis & Strategic Outlook

Global foodservice market was valued at USD 3,911.4 billion in 2025 and is projected to reach USD 6,767.11 billion by 2033, reflecting a CAGR of 7.1% over the forecast period.

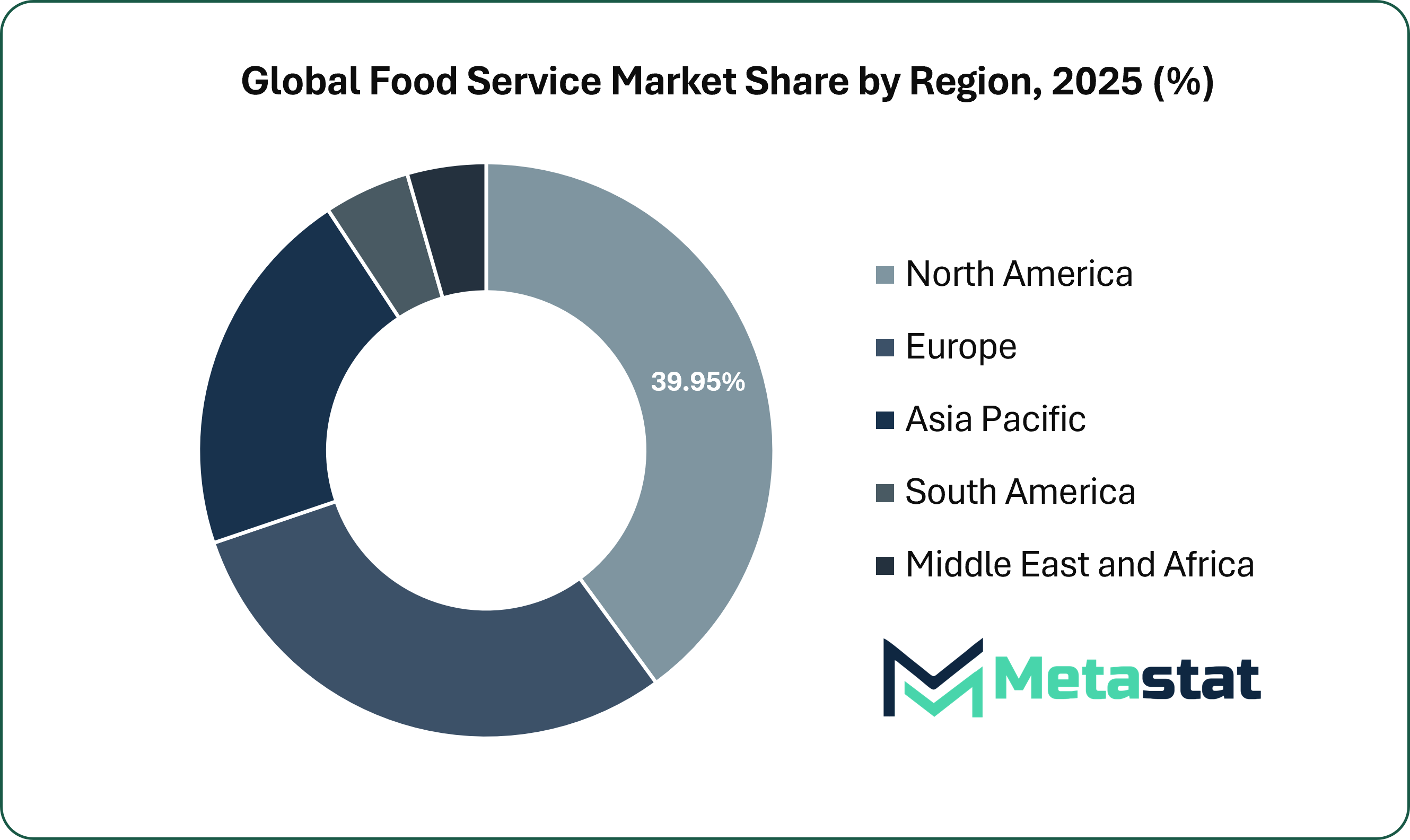

North America holds 39.95% of the food service market in 2025, with the US leading the market share in 2026.

Cafes and Bars accounted for a market share of 15.8% in 2025, owing to menu innovation and concept diversification through new product and format experimentation.

Key trends driving growth include increasing demand for convenience and off-premises dining options, and consumer preference for experience-driven and premium dining.

Opportunities include the growth of operational efficiency technology and personalized marketing.

Key insight: Shifting towards tech-driven personalized menus and loyalty programs can significantly enhance customer lifetime value.

Market Dynamics

Increasing Demand for Convenience and Off-premises Dining Options

Increased preference for convenience and out-of-home occasions is reshaping operating models, with higher reliance on delivery, takeout, and drive-thru formats accelerating investments in digital ordering, kitchen throughput, and packaging performance.

Consumer Preference for Experience-driven and Premium Dining

Increased preference for experience-led dining is supporting premium formats, with high-touch venues commanding higher checks owing to differentiated culinary narratives, artisanal positioning, and immersive ambience.

Restraints & Challenges:

Persistent Labor Shortages Compounded by Wage Inflation

Chronic workforce shortages and wage inflation represent material operational constraints, limiting capacity and pressuring margins through higher labor costs, reduced operating hours, and trade-offs between service standards and price positioning.

Volatile Food Input Costs and Supply Chain Disruption

Volatile food costs and supply disruptions increase margin volatility and execution risk, with logistics delays and incremental procurement costs disrupting menu planning, pricing discipline, and product availability.

Opportunities:

Growth of Operational Efficiency Technology with Personalized Marketing

Operational efficiency technology and personalized marketing represent a dual opportunity, enabling workflow automation to mitigate labor constraints and supporting data-led targeting to strengthen loyalty and marketing return on investment.

Market Segmentation Analysis

The global foodservice market is classified by foodservice type, outlet, and service type.

By Foodservice Type, the market is further segmented into:

Cafés and Bars

Cafés and bars represent a blended format aligned with premium beverages and convenience, integrating daytime café occasions with evening bar traffic to improve margin mix via specialty drinks, curated snacks, and differentiated atmosphere. Cafés and Bars segment is valued at USD 661.3 billion in 2026 and is projected to reach USD 1054.3 billion by 2033, at a CAGR of 6.9% during the forecast period.

Cloud Kitchens

Cloud kitchens are digital-first production hubs aligned with off-premises consumption, enabling delivery-only brands to scale without dining rooms or prime real estate costs, while supporting multi-brand, multi-cuisine throughput from a centralized footprint. Cloud Kitchens segment is valued at USD 596 billion in 2026 and is projected to reach USD 1038.7 billion by 2033, at a CAGR of 8.3% during the forecast period.

Full-Service Restaurants

Full-service restaurants compete on experience and perceived value, using table service, atmosphere, and menu craftsmanship to justify premium checks and capture destination dining occasions. Full-Service Restaurants segment is valued at USD 1050 billion in 2026 and is projected to reach USD 1669.4 billion by 2033, at a CAGR of 6.8% during the forecast period.

Quick-Service Restaurants

Quick-service restaurants maximize throughput in cost-sensitive environments, balancing speed and convenience with value positioning through simplified menus, counter service, drive-thru operations, and digital ordering. Quick-Service Restaurants segment is valued at USD 1642.8 billion in 2026 and is projected to reach USD 2654 billion by 2033, at a CAGR of 7.1% during the forecast period.

Others

Food trucks, pop-ups, and convenience-store foodservice act as agile formats with alternative access points, leveraging lower entry costs and flexible location strategies to test new concepts and capture impulse-led occasions.

By Outlet, the market is divided into:

Chained Outlets

Chained outlets represent a scale-driven operating model, enabling cost advantages, consistent brand execution across geographies, faster rollout of new items and formats through standardized systems, and procurement leverage. Chained Outlets segment is projected to reach USD 6076.1 billion by 2033, at a CAGR of 7.2% during the forecast period.

Independent Outlets

Independent outlets compete through differentiation and local relevance, using concept diversity, community ties, and chef-led innovation to deliver distinctive menus and faster adoption of emerging food trends.

By Service Type, the market is further divided into:

Dine-in

Dine-in represents the premium, experience-led service model where ambience, hospitality, and table service increase dwell time and average check size while strengthening direct loyalty through higher-touch interactions.

Takeaway

Takeaway supports convenience and throughput, serving customers seeking off-premises meal solutions via optimized packaging and streamlined handoff processes that improve peak-hour flow across outlet types.

Delivery

Delivery has evolved into a large, technology-led growth channel supported by third-party platforms, extending restaurant reach while reshaping unit economics through commissions, packaging requirements, service-time expectations, and digital visibility.

By Region:

Based on geography, the global Food Service market is divided into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

North America foodservice market is projected to expand at a CAGR of 7.1% during 2026-2033, reaching a market size (TAM) of USD 2,692.6 billion by 2033.

The biggest driver of the foodservice market in North America is sustained consumer preference for digital convenience, accelerating structural shifts in ordering, fulfillment, and loyalty execution.

APAC presents high-potential growth opportunities supported by technology-led scaling, hyper-local menu localization, and flexible expansion models aligned with diverse consumer preferences. It involves using data analytics and digital platforms to customize menus to local taste profiles and consumption occasions across key APAC markets.

APAC has a massive potential in the food service market, by improving the dining experience and taking advantage of increasing disposable income and by giving people something new, something that stakes out more territory than mere survival.

Middle East & Africa and South America reflect an uneven foodservice landscape shaped by fragmented supply chains, price-sensitive consumers, and gradual formalization of foodservice infrastructure.

Competitive Landscape & Strategic Insights

Global foodservice comprises multiple strategic groups that compete across scale, price positioning, experience, and digital execution. Global QSR franchise leaders such as McDonald's, Yum! Brands, Restaurant Brands International, and Domino's hold scale advantages rooted in asset-light, predominantly franchised models that accelerate international expansion. RBI operates a franchise-dominant model, with approximately 95% of system-wide restaurants franchised, and has guided toward at least 40,000 restaurants by 2028, supported by digital ordering, marketing investment, and unit expansion across its brand portfolio.

A second competitive group includes fast-casual and specialty leaders such as Starbucks, Chipotle, Chick-fil-A, and Panera Bread, competing through brand experience, perceived quality, and operational excellence within focused categories. Their approach revolves around driving premium pricing with high consumer loyalty, powered by digital loyalty and menu innovation augmented by LTOs. Full-service and casual dining operators such as Darden Restaurants and Bloomin' Brands compete on experience-led dining occasions, strengthening off-premises execution alongside dine-in differentiation. Their brand DNA is table service and social, which is being developed to enable strong off-premise and delivery participation due to changing consumer behaviours. The competitive landscape is not made any more approachable by the International & Regional Powerhouses such as Jollibee Foods Corporation out of the Philippines and China’s Luckin Coffee and Haidilao, which benefit from strong cultural relevancy in high-growth Asia Pacific as they go on acquisition binges to accumulate multi-brand portfolios into new categories.

Future Outlook

Market size is forecast to rise from USD 3,911.4 billion in 2025 to over USD 6,767.11 billion by 2033.

The global foodservice market is projected to expand over the long term, while near-term economic headwinds and shifting consumer priorities are creating execution pressure across formats. One headwind is less of a price gap as inflation from QSRs has made casual dining look like a better value, pressuring QSRs to be more aggressive with menu innovation and LTOs. Key competitive trends in the space include accelerated implementation of artificial intelligence in operations and personalization, the adoption of delivery-only models such as ghost kitchens, and a consumer-led demand for sustainability, experiential dining and global fusion food. M&A activity is likely to rebound in 2026, supported by easing capital costs and expansion priorities toward higher-growth territories such as Southeast Asia.

This research report categorizes the Food Service market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Food Service market. Recent market developments and competitive strategies such as expansion, new format and menu launches, partnerships, and mergers and acquisitions have been included to illustrate the competitive landscape.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Food Service market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 7.1% from 2026 to 2033

Revenue Unit

USD billion

Segmentation

By Foodservice Type, Outlet, Service Type, and Region

By Foodservice Type

Cafés and Bars

Cloud Kitchens

Full-Service Restaurants

Quick-Service Restaurants

Others

By Outlet

Chained Outlets

Independent Outlets

By Service Type

Dine-in

Takeaway

Delivery

By Region

North America (By Foodservice Type, Outlet, Service Type, and Country)

United States

Canada

Mexico

Europe (By Foodservice Type, Outlet, Service Type, and Country)

Germany

France

UK

Italy

Spain

Russia

Asia Pacific (By Foodservice Type, Outlet, Service Type, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Foodservice Type, Outlet, Service Type, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Foodservice Type, Outlet, Service Type, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Prepositions of Leading Market Players

Kazakhstan Frozen Potato Products market size is valued at USD 26.4 million in 2025 and is projected to reach USD 53.0 million in 2033, at a CAGR of 9.0% from 2026 to 2033.

Switzerland Poke Food market size is valued at USD 29.2 million in 2025 and is projected to reach USD 44.5 million in 2033, at a CAGR of 5.5% from 2026 to 2033.

Netherlands Food and Beverages QA, QC, and Compliance Software Solutions Market Size, Share, Trends, 2033

Netherlands F&B QA, QC, and Compliance Software Solutions market size is valued at USD 272.5 million in 2025 and is projected to reach USD 421.3 million in 2033, at a CAGR of 5.6% from 2026 to 2033.

Netherlands F&B QA, QC, and Compliance Software Solutions Market, Netherlands F&B QA, QC, and Compliance Software Solutions Market Size, Netherlands F&B QA, QC, and Compliance Software Solutions Market Share, Netherlands F&B QA, QC, and Compliance Software Solutions Market Analysis, Netherlands F&B QA, QC, and Compliance Software Solutions Market Growth, Netherlands F&B QA, QC, and Compliance Software Solutions Market Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market Research Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Forecast, Netherlands F&B QA, QC, and Compliance Software Solutions, Netherlands F&B QA, QC, and Compliance Software Solutions Market Research, Netherlands F&B QA, QC, and Compliance Software Solutions Industry, Netherlands F&B QA, QC, and Compliance Software Solutions Industry Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Data, Netherlands F&B QA, QC, and Compliance Software Solutions Statistics, Netherlands F&B QA, QC, and Compliance Software Solutions Market Statistics, Netherlands F&B QA, QC, and Compliance Software Solutions Industry Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market Report, Netherlands F&B QA, QC, and Compliance Software Solutions Market Trends, Netherlands F&B QA, QC, and Compliance Software Solutions Market News, Netherlands F&B QA, QC, and Compliance Software Solutions Forecasts, Netherlands F&B QA, QC, and Compliance Software Solutions Market Intelligence Report

Global Antibiotic-Free Pork market size is valued at USD 25,430.6 million in 2025 and is projected to reach USD 42,528 million in 2033, at a CAGR of 6.6% from 2026 to 2033