MARKET OVERVIEW

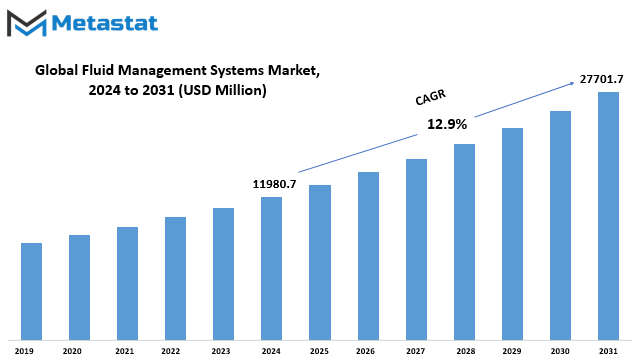

The Global Fluid Management Systems market is estimated to reach $27701.7 Million by 2031; growing at a CAGR of 12.9% from 2024 to 2031.

The Global Fluid Management Systems market plays a significant role in the healthcare industry, addressing critical needs for efficient fluid handling and monitoring within medical settings. This market revolves around cutting-edge technologies and solutions designed to optimize fluid-related processes in healthcare, catering to diverse medical applications.

In the medical infrastructure, the Fluid Management Systems market stands as a pivotal contributor, offering advanced solutions that transcend conventional methods. This industry is dedicated to enhancing the precision and reliability of fluid handling across various medical procedures, ensuring optimal patient care and safety.

Medical facilities worldwide heavily rely on Fluid Management Systems to maintain fluid balance during surgeries, diagnostic procedures, and therapeutic interventions. The integration of innovative technologies within these systems underscores their importance in ensuring seamless operations within the healthcare domain. These systems provide healthcare professionals with precise control over fluid administration, facilitating accurate monitoring and adjustment according to individual patient needs.

The Fluid Management Systems market is not confined to a singular facet; rather, it spans a spectrum of applications. From operating rooms to critical care units, these systems find utility in diverse medical settings, demonstrating their adaptability and indispensable role in modern healthcare. The industry constantly evolves to meet the dynamic demands of the healthcare landscape, incorporating advancements in technology to stay at the forefront of medical innovation.

In healthcare ecosystem, the Fluid Management Systems market addresses the intricacies of fluid dynamics, emphasizing the importance of accurate and real-time fluid monitoring. This goes beyond a mere technological adaptation; it represents a commitment to enhancing patient outcomes and streamlining medical processes. The industry’s focus on precision and reliability aligns with the healthcare sector’s overarching goal of delivering quality patient care.

Fluid Management Systems ensure the effective delivery of fluids and contribute to minimizing risks associated with fluid imbalances during medical procedures. As healthcare continues to advance, the demand for sophisticated Fluid Management Systems is set to rise, driven by the imperative to enhance patient safety and optimize medical practices.

The Global Fluid Management Systems market stands as a vital component within the healthcare industry, providing indispensable solutions for fluid handling and monitoring. Its impact extends across various medical applications, underscoring its adaptability and relevance in diverse healthcare settings. As technology continues to advance, the Fluid Management Systems market remains at the forefront of innovation, committed to meeting the evolving needs of modern healthcare and contributing to improved patient outcomes.

GROWTH FACTORS

In the global Fluid Management Systems market, various factors play a pivotal role in shaping its dynamics. Examining the drivers propelling this market forward, one finds a notable surge in surgical procedures, contributing significantly to its growth. The increasing demand for such procedures has become a driving force, underscoring the market's upward trajectory.

Moreover, technological advancements represent another key driver. The continuous evolution of technology in fluid management systems has enhanced their efficiency and their applicability. This technological progress is fostering innovation and opening new avenues within the market.

However, not without challenges, the market grapples with certain restraints that pose hurdles to its seamless progress. Chief among these obstacles is the high cost associated with advanced fluid management systems. The financial implications of investing in such cutting-edge technology can deter potential stakeholders, creating a barrier to widespread adoption.

Additionally, the risks of cross-contamination present another noteworthy restraint. As advancements bring more sophisticated systems into play, the potential for cross-contamination becomes a concern. This risk can compromise the integrity of procedures, urging a cautious approach in adopting these technologies.

Amidst these challenges, opportunities emerge that can reshape the market landscape. A notable opportunity lies in the shift towards minimally invasive surgeries. This trend not only addresses the concerns of high costs and contamination risks but also aligns with the growing preference for less invasive medical interventions. The market can capitalize on this shift by adapting and innovating its offerings to cater to the rising demand for minimally invasive solutions.

The global Fluid Management Systems market stands at the intersection of drivers, restraints, and opportunities. The increasing prevalence of surgical procedures and ongoing technological advancements drive its growth, while challenges such as high costs and contamination risks pose impediments. However, the promising opportunity presented by the shift towards minimally invasive surgeries offers a potential avenue for market players to navigate and thrive in this ever-changing landscape.

MARKET SEGMENTATION

By Product

In the global Fluid Management Systems market, the categorization based on products unveils a nuanced breakdown. The primary subdivisions include Fluid Management Systems themselves, along with Disposables and Consumables. This classification serves to offer a more detailed understanding of the diverse components contributing to the market's dynamics.

The delineation of the market into Fluid Management Systems signifies a focal point within the broader spectrum. These systems play a pivotal role in facilitating the management of fluids, and their significance becomes pronounced when dissected from the larger market context.

Moving beyond the core systems, the market further encompasses Disposables and Consumables. This segmentation acknowledges the supplementary elements that contribute to the overall functionality of Fluid Management Systems. Disposables, as the name suggests, represent items intended for one-time use, while Consumables cover materials integral to the ongoing operational aspects of the systems.

This layered categorization not only enhances clarity but also aids stakeholders in comprehending the distinct components shaping the global Fluid Management Systems market. It provides a framework for a more granular analysis, allowing for a comprehensive evaluation of the market's diverse facets.

As we navigate through the intricacies of the Fluid Management Systems market, this segmentation sheds light on the specific products that collectively constitute its dynamic landscape. From the core systems driving functionality to the supplementary disposables and consumables, each segment contributes uniquely to the overall tapestry of the market, creating a comprehensive framework for stakeholders to navigate and understand its intricacies.

By Application

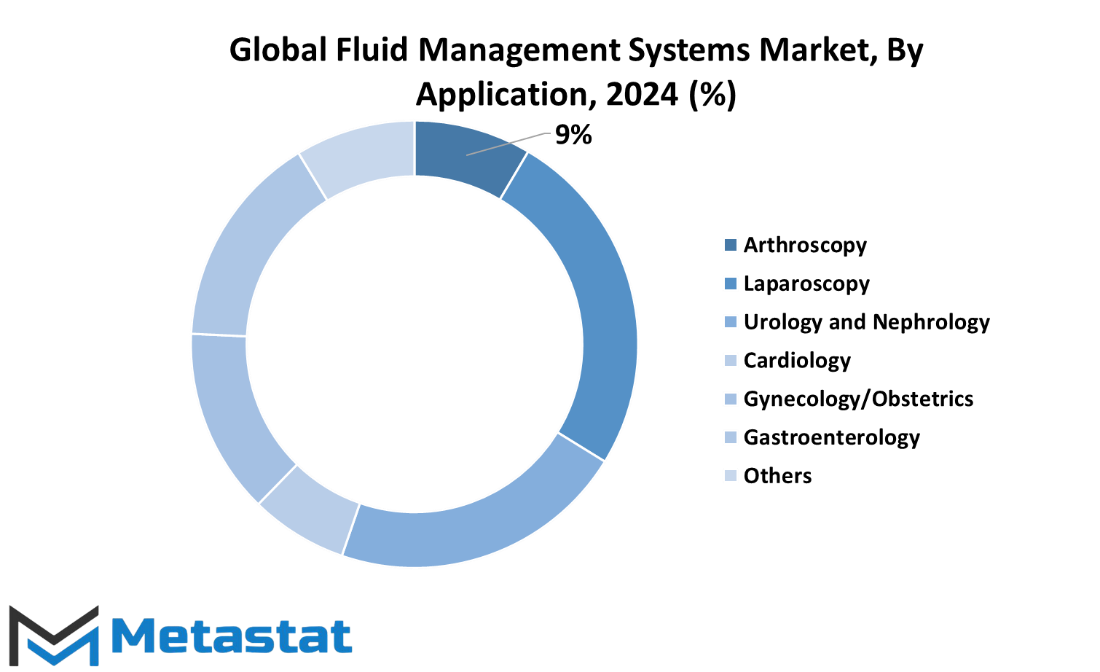

In today’s interconnected world, the global Fluid Management Systems market plays a pivotal role in various medical applications. The market is segmented by application into Arthroscopy, Laparoscopy, Urology and Nephrology, Cardiology, Gynecology/Obstetrics, Gastroenterology, and Others.

Arthroscopy, a technique involving minimally invasive joint surgeries, relies on fluid management systems to enhance visualization and facilitate surgical procedures. Laparoscopy, a method for examining the abdominal cavity, similarly benefits from these systems, aiding surgeons in achieving precision during procedures.

Urology and Nephrology applications address conditions related to the urinary and renal systems. Fluid management systems are integral in ensuring effective diagnostics and treatments in these medical domains. Cardiology, focusing on the heart and circulatory system, utilizes these systems for fluid control in various cardiac procedures.

Gynecology/Obstetrics involves the study and management of women’s reproductive health. In this field, fluid management systems contribute to successful procedures and surgeries. Gastroenterology, dealing with the digestive system, benefits from these systems in ensuring optimal conditions during endoscopic procedures.

The broad category of Others has various medical applications where fluid management systems find utility, contributing to advancements in medical practices. In essence, the diverse applications of fluid management systems underscore their crucial role in modern medical procedures, enhancing precision and efficacy across a spectrum of healthcare disciplines.

By End-Users

In the expansive global market of Fluid Management Systems, end-users play a pivotal role in shaping its dynamics. This market segment is broadly categorized into Hospitals, Dialysis Centers, Ambulatory Surgical Centers, and Other End Users.

Hospitals stand out as key consumers, relying on Fluid Management Systems to enhance patient care and medical procedures. The precise control and distribution of fluids prove crucial in various hospital settings, from surgeries to routine treatments.

Dialysis Centers constitute another significant end-user group, relying on these systems to maintain optimal fluid balance in patients undergoing dialysis. The critical nature of fluid management in this context underscores the importance of reliable systems for effective healthcare delivery.

Ambulatory Surgical Centers form a distinct category within the end-user spectrum. These facilities, emphasizing outpatient services, benefit from Fluid Management Systems to ensure seamless procedures, emphasizing efficiency and patient comfort.

The category of Other End Users encapsulates diverse entities leveraging fluid management solutions for specific requirements. This could range from specialized medical facilities to research institutions, reflecting the versatile applicability of these systems beyond the conventional healthcare settings.

Understanding the diverse landscape of end-users in the global Fluid Management Systems market illuminates the varied applications and the integral role these systems play in enhancing healthcare across different settings.

REGIONAL ANALYSIS

The worldwide market for Fluid Management Systems can be categorized geographically into North America, Europe, and Asia-Pacific. These regions play a pivotal role in shaping the dynamics of the global Fluid Management Systems market.

Understanding the global distribution of Fluid Management Systems is crucial for assessing market trends and opportunities. North America, as one of the key regions, significantly influences the market landscape. The diverse economic activities and healthcare infrastructure in this region contribute to the demand for efficient fluid management solutions.

Moving across the Atlantic, Europe emerges as another vital player in the global market. The continent's well-established healthcare systems and technological advancements drive the adoption of fluid management systems. Market dynamics here are influenced by factors unique to the European context.

On the other side of the globe, Asia-Pacific stands out as a dynamic and rapidly evolving market for Fluid Management Systems. The region's economic growth and increasing healthcare awareness contribute to the expanding market share. The unique characteristics of Asia-Pacific create distinct challenges and opportunities that shape the fluid management landscape.

The geographical distribution of the global Fluid Management Systems market underscores the importance of understanding regional nuances. North America, Europe, and Asia-Pacific each bring their own dynamics to the table, contributing collectively to the vibrancy and growth of the market.

COMPETITIVE PLAYERS

In the global Fluid Management Systems market, a variety of competitive players actively contribute to shaping the industry's trajectory. Leading the charge are prominent entities such as Medline Industries, LP., Cardinal Health Inc., Serres OY, Medela AG, DeRoyal Industries, Inc., VacSax Ltd, Amsino International, Inc., M.A.S. Medical S.R.L., Hologic Inc., Stryker Inc., Medtronic PLC, Baxter International Inc., Fresenius Medical Care AG, Olympus Corporation, and DePuy Synthes.

These key players play a pivotal role in the Fluid Management Systems industry, each bringing its unique strengths and innovations to the table. Medline Industries, LP., for instance, is known for its commitment to delivering high-quality products, while Cardinal Health Inc. stands out with its extensive distribution network. Serres OY and Medela AG, on the other hand, have made significant strides in advancing fluid management technologies.

DeRoyal Industries, Inc. and VacSax Ltd showcase their expertise through specialized solutions, contributing to the diversified offerings in the market. Amsino International, Inc. and M.A.S. Medical S.R.L. bring their own distinctive approaches, catering to specific needs within the industry. Hologic Inc., Stryker Inc., and Medtronic PLC are recognized for their continuous efforts in research and development, driving innovation and efficiency in Fluid Management Systems.

The presence of industry giants like Baxter International Inc., Fresenius Medical Care AG, Olympus Corporation, and DePuy Synthes further amplifies the competitive landscape. Each entity competes not only on a global scale but also shapes the regional dynamics of the Fluid Management Systems market.

As these competitive players navigate the intricacies of the industry, their collective impact is undeniable. Together, they contribute to the growth, innovation, and evolution of Fluid Management Systems, ensuring a vibrant and competitive market that continually strives for excellence.

Fluid Management Systems Market Key Segments:

By Product

- Fluid Management Systems

- Disposables and Consumables

By Application

- Arthroscopy

- Laparoscopy

- Urology and Nephrology

- Cardiology

- Gynecology/Obstetrics

- Gastroenterology

- Others

By End-Users

- Hospitals

- Dialysis Centers

- Ambulatory Surgical Centers

- Other End Users

Key Global Fluid Management Systems Industry Players

- Medline Industries, LP.

- Cardinal Health Inc.

- Serres OY

- Medela AG

- DeRoyal Industries, Inc.

- VacSax Ltd

- Amsino International, Inc.

- A.S. Medical S.R.L.

- Hologic Inc.

- Stryker Inc.

- Medtronic PLC

- Baxter International Inc.

- Fresenius Medical Care AG

- Olympus Corporation

- DePuy Synthes

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential

US: +1-(714)-364-8383

US: +1-(714)-364-8383