Driver Safety Training Market Size, Share, By Training Type (Classroom Based Training, Online E-Learning Training, Simulator, VR Based Training, and Behind-the-Wheel Practical Training), By Deployment Mode (Cloud-Based Platforms and On-Premises Solutions), By Vehicle Type (Passenger Vehicles, Commercial Vehicles, and Others), By End User (Individual Novice Drivers, Corporate Fleet Drivers, Commercial Drivers, and Defensive Drivers), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4678

Published

April 28, 2026

Pages

318 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

Global Driver Safety Training market size is valued at USD 11.3 billion in 2025 and projected to grow at a CAGR of 4.5% during the forecast period, reaching USD 16.1 billion by 2033.

Global Driver Safety Training Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global Driver Safety Training market valued at USD 11.3 billion in 2025, growing at a CAGR of 4.5% through 2033, with potential to exceed USD 16.1 billion.

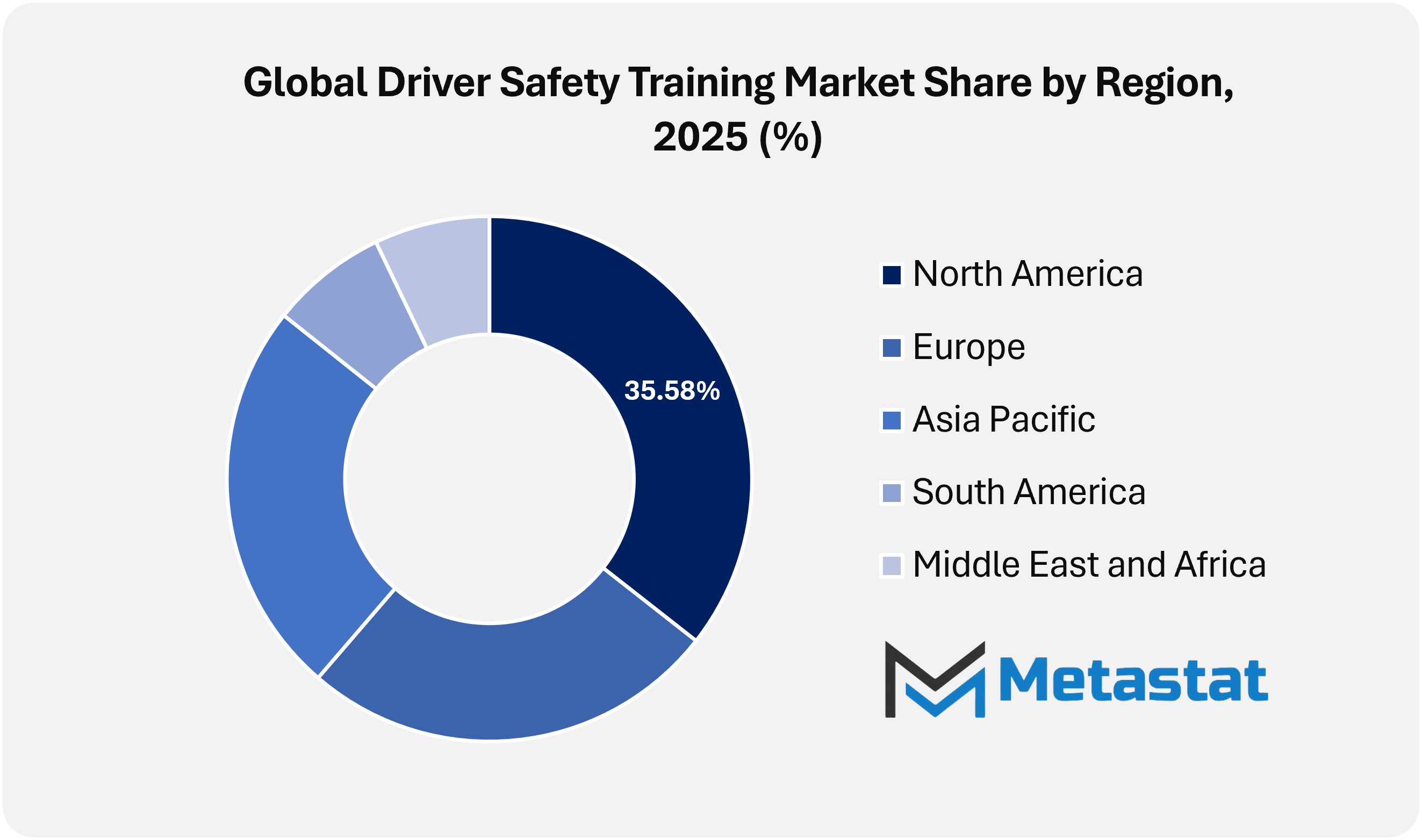

North America holds 35.6% in 2025, with the U.S. leading the regional market.

Classroom-Based Training segment accounts for a market share of 25.4% in 2025.

Opportunities include growth of Digital & Simulator-Based Training Platforms.

Key insight: Rising accident awareness and regulatory pressure position the Global Driver Safety Training Market for structured expansion across corporate, commercial, and individual segments.

The global driver safety training market within the transportation risk management industry is evolving beyond traditional classroom modules and defensive driving manuals. It is becoming a performance-driven ecosystem in which data intelligence, behavioral science, and immersive simulation shape how commercial and private drivers prepare for real-world conditions. Rather than treating instruction as a compliance requirement, market participants are developing structured learning systems that continuously improve through telematics data, fleet diagnostics, and roadway analytics.

In the coming years, training delivery will increasingly incorporate aviation-style simulation environments, where high-fidelity virtual scenarios replicate hazardous weather, low-visibility night conditions, cargo instability, and urban congestion. These environments will not only recreate crash scenarios but also assess driver fatigue, distraction tendencies, and reaction time. Artificial intelligence engines will deliver real-time corrective feedback, transforming static lesson plans into adaptive learning pathways tailored to individual risk profiles.

Market Dynamics

Growth Drivers:

Safety Regulation Enforcement.

Stricter road safety mandates across developed and emerging economies are driving stronger demand in the Global Driver Safety Training Market. Governments are intensifying compliance audits, introducing stricter penalties for violations, and mandating certified training programs for commercial operators. Regulatory alignment across regions is encouraging fleet owners, logistics providers, and transportation companies to invest in structured driver training systems that meet formal safety benchmarks.

Corporate Liability & Fleet Risk Reduction

Rising accident-related litigation and insurance claims are compelling organizations to adopt preventive training models. Within the Global Driver Safety Training Market, companies managing delivery trucks, heavy vehicles, and employee transport fleets are prioritizing risk mitigation frameworks. Structured safety modules, defensive driving certification, and behavioral monitoring programs are reducing operational exposure while strengthening corporate governance standards and insurer confidence.

Restraints and Challenges:

High Training Delivery Costs

Significant expenditure on certified instructors, practical sessions, infrastructure, and assessment tools creates adoption barriers across the market. Smaller transport operators within the Global Driver Safety Training Market face financial pressure when allocating budgets for recurring training cycles. Capital requirements for advanced simulators, compliance documentation, and periodic refresher programs are likely to slow market expansion in price-sensitive regions.

Fragmented Market with Varied Standards

Diverse certification norms and inconsistent curriculum benchmarks across regions restrict uniform service delivery. The Global Driver Safety Training Market faces operational complexity owing to regional regulatory variations, language requirements, and differing vehicle classifications. A lack of standardized assessment metrics limits scalability for multinational providers seeking global program consistency.

Opportunities:

Growth of Digital & Simulator-Based Training Platforms

Rapid advances in immersive technologies are transforming training delivery methods across the Global Driver Safety Training Market. Virtual driving simulators, AI-enabled performance analytics, and cloud-based learning modules are improving training efficiency while reducing long-term costs. Remote accessibility, scalable subscription models, and data-driven feedback systems are expanding adoption across commercial fleets and individual drivers.

Market Segmentation Analysis

The Global Driver Safety Training market is classified based on Training Type, Deployment Mode, Vehicle Type, and End User.

By Training Type, the market is further segmented into:

Classroom Based Training

Classroom Based Training segment is valued at USD 3.0 billion in 2026 and is projected to reach USD 3.6 billion by 2033, at a CAGR of 2.5% during the forecast period.

Classroom-Based Training continues to hold relevance through instructor-led modules focused on traffic regulation interpretation, risk perception theory, and behavioral correction frameworks. Physical learning environments support structured discussions, scenario analysis, and group-based risk assessment exercises. Institutional adoption remains steady across government licensing programs and structured fleet onboarding initiatives.

Online E-Learning Training segment is valued at USD 2.6 billion in 2026 and is projected to reach USD 4.1 billion by 2033, at a CAGR of 6.4% during the forecast period.

Online E-Learning Training is expanding through scalable digital platforms that offer modular coursework, real-time assessments, and adaptive learning paths. Interactive dashboards, AI-based progress tracking, and multilingual content support are improving accessibility across remote regions. Flexible scheduling models are strengthening participation among working professionals seeking certification renewal.

Simulator & VR Based Training

Simulator & VR Based Training segment is valued at USD 1.3 billion in 2026 and is projected to reach USD 2.2 billion by 2033, at a CAGR of 8.1% during the forecast period.

Simulator & VR-Based Training is gaining momentum through immersive risk simulation, adverse weather replication, and emergency response practice without physical exposure to danger. Advanced motion systems and data-driven feedback loops are improving response time measurement and decision accuracy. Adoption is expected to accelerate across professional fleet training programs that require high-precision skill validation.

Behind-the-Wheel Practical Training

Behind-the-Wheel Practical Training segment is valued at USD 4.9 billion in 2026 and is projected to reach USD 6.2 billion by 2033, at a CAGR of 3.5% during the forecast period.

Behind-the-Wheel Practical Training remains foundational for competency validation through supervised road exposure, real-time correction, and maneuver accuracy assessment. Integration of telematics sensors and performance analytics enables measurable evaluation of braking behavior, lane discipline, and situational judgment. Regulatory bodies continue to mandate structured practical certification benchmarks.

By Deployment Mode, the market is divided into:

Cloud-Based Platforms

Cloud-Based Platforms segment is projected to reach USD 9.9 billion by 2033, at a CAGR of 5.8% during the forecast period.

Cloud-Based Platforms are expected to dominate delivery models through centralized content management, remote access capability, and scalable user enrollment. Continuous software updates, performance analytics dashboards, and secure data storage improve administrative efficiency. Enterprises increasingly prefer subscription-based models to optimize cost predictability and compliance tracking.

On-Premises Solutions

On-Premises Solutions segment is projected to reach USD 6.2 billion by 2033, at a CAGR of 2.6% during the forecast period.

On-Premises Solutions retain relevance among institutions that require strict data governance, controlled infrastructure environments, and customized curriculum structures. Dedicated servers and internal IT oversight support regulatory compliance requirements. Large transportation companies continue to invest in proprietary systems aligned with internal safety protocols.

By Vehicle Type, the market is further divided into:

Passenger Vehicles

Passenger Vehicles segment is projected to reach USD 8.4 billion by 2033.

Passenger Vehicles training demand is expanding owing to rising urban congestion, insurance-linked certification incentives, and mandatory licensing reforms. Curriculum frameworks address defensive maneuvering, distracted driving mitigation, and electric vehicle operational safety. Rising personal vehicle ownership continues to support enrollment growth across metropolitan regions.

Commercial Vehicles segment is projected to reach USD 7 billion by 2033.

Commercial Vehicles training programs prioritize cargo safety, long-haul fatigue management, and regulatory transport compliance. Telematics-enabled feedback and route risk modeling are strengthening professional skill assessment across fleet operations. Growth in logistics activity and cross-border freight movement is increasing demand for standardized commercial driver certification modules.

Others

Others segment is projected to reach USD 0.7 billion by 2033.

The Others category includes specialty vehicles used in construction, agriculture, and emergency services. Training modules in this segment address terrain navigation, equipment handling safety, and operational risk response. Continued use of specialized utility vehicles is expected to support demand for structured competency validation aligned with sector-specific safety requirements.

By End User, the Global Driver Safety Training market is divided as:

Individual Novice Drivers

Individual Novice Drivers segment is projected to grow at a CAGR of 3.9% during the forecast period.

The Individual Novice Drivers segment is growing through structured beginner certification pathways that combine theory, simulation exposure, and supervised road assessment. Government safety campaigns and parental awareness initiatives continue to encourage early enrollment. Digital progress tracking systems provide measurable readiness indicators before independent licensing approval.

Corporate Fleet Drivers

Corporate Fleet Drivers segment is projected to grow at a CAGR of 5.6% during the forecast period.

Corporate Fleet Drivers training programs focus on liability reduction, fuel-efficient driving techniques, and compliance documentation. Performance benchmarking tools integrated with fleet management systems improve accountability and operational visibility. Enterprise risk mitigation strategies are positioning structured driver training within broader governance and safety management frameworks.

Commercial Drivers

Commercial Drivers segment is projected to grow at a CAGR of 4.9% during the forecast period.

The Commercial Drivers segment emphasizes advanced maneuver training, regulatory compliance programs, and cross-border transport certification standards. Continuous refresher programs address evolving road safety regulations and technological advancements in heavy vehicles. Professional accreditation requirements continue to sustain recurring enrollment cycles.

Defensive/Aged Drivers

Defensive/Aged Drivers segment is projected to grow at a CAGR of 1% during the forecast period.

Defensive/Aged Drivers programs focus on reaction time improvement, updated traffic law awareness, and adaptive driving techniques for individuals with cognitive or physical limitations. Health-based screening integration and refresher modules support prolonged safe mobility. Insurance-linked participation incentives continue to encourage enrollment among older driver groups.

By Region:

Based on geography, the Global Driver Safety Training market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Driver Safety Training Market is set to expand at a CAGR of 4.5% within the forecast period, reaching a market size (TAM) of USD 5.3 billion by the end of 2033.

North America drives a boost in the Driver Safety Training Market through strict regulatory enforcement and obligatory company fleet compliance applications.

North America strengthens the Driver Safety Training Market with growing insurance-related protection certifications and integration of telematics-based tracking structures.

Europe strengthens the Driver Safety Training Market with advanced training infrastructure, rising simulator-based learning adoption, and increasing emphasis on occupational safety, telematics integration, and cross-border transport compliance.

Asia Pacific unlocks growth possibilities within the Driver Safety Training Market via growing commercial automobile fleets and virtual studying adoption throughout growing economies.

Across the Middle East, Africa, and South America, the Global Driver Safety Training Market records constant progress supported by way of infrastructure improvement, increasing transportation networks, and growing recognition of driver education programs.

Competitive Landscape and Strategic Insights

The Global Driver Safety Training Market continues to expand as governments, corporations, and individuals place stronger emphasis on road safety and responsible driving behavior. Rising traffic density, stricter regulations, and increasing accident rates have made structured training programs more important than before. Both new drivers and experienced professionals are seeking proper training to reduce risk and improve confidence behind the wheel. Training providers are expanding their offerings from basic driving lessons to advanced defensive driving, fleet safety management, and digital learning modules. As awareness increases, demand for certified and technology-enabled training solutions is expected to rise across regions.

Traditional driving schools remain a core part of the market, with established institutions such as AA Driving School, Red Driving School, Young Drivers of Canada, Pass N Go Driving School, LTrent Driving School, Safeway Driving School, A to Z Driving School, Advance Driving Academy, All Seasons Driving School, Champion Driving School, Drive Johnson’s Driving School, First Choice Driving School, Metro Driving Academy, One 2 One Driving School, and Topgear Driving School serving learners through classroom and on-road training. These institutions focus on foundational skills, traffic regulations, risk awareness, and test preparation. Their strong local presence and structured curriculum continue to support stable enrollment, while online theory modules and flexible scheduling are improving learner accessibility.

At the corporate and fleet level, specialized safety training providers are gaining traction. Companies such as Lytx, Inc., Wheels, LLC, TTC GROUP, Fleet Safety International, Smith System Driver Improvement Institute, Inc., Vector Solutions, SambaSafety, LLC, 360training, Thinking Driver Academy, Succeed Safe, and I Drive Safely offer defensive driving courses, compliance training, telematics-based coaching, and risk analytics. These players use data monitoring, dash cameras, and digital platforms to track driver behavior and improve performance. As fleet operators seek to reduce insurance costs and liability exposure, partnerships with such providers are expected to increase.

Regulatory bodies and safety-focused organizations also play an important role in setting standards and promoting awareness across the market. Institutions such as DEKRA, RoSPA, IAM RoadSmart, Drive Dynamics, Wheel-Skills, Safety Circle India, Interactive Education Concepts Inc., and Aceable, Inc. support certification, advanced skill programs, and digital licensing education. Their efforts strengthen quality benchmarks across the industry. With stronger emphasis on safe mobility, electric vehicles, and tighter compliance frameworks, these organizations will continue to influence training models globally.

Forecast and Future Outlook

Market size is forecast to rise from USD 11.3 billion in 2025 to over USD 16.1 billion by 2033.

At the same time, public sector institutions and private providers are expected to collaborate on standardized digital certification models that remain portable across borders. Credential portability will streamline cross-regional logistics operations while reinforcing uniform safety benchmarks. The industry is increasingly redefining professional driving competence through predictive analytics, behavioral modeling, and simulation-based validation, positioning structured training as a strategic component of modern mobility infrastructure.

Driver Safety Training Market Key Segments:

By Training Type:

Classroom Based Training

Online E-Learning Training

Simulator & VR Based Training

Behind-the-Wheel Practical Training

By Deployment Mode:

Cloud-Based Platforms

On-Premises Solutions

By Vehicle Type:

Passenger Vehicles

Commercial Vehicles

Others

By End User:

Individual Novice Drivers

Corporate Fleet Drivers

Commercial Drivers

Defensive/Aged Drivers

Key Global Driver Safety Training Industry Players

This research report categorizes the Driver Safety Training market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Driver Safety Training market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Driver Safety Training market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 4.5% from 2026 to 2033

Revenue Unit

USD billion

Segmentation

By Training Type, Deployment Mode, Vehicle Type, End User, and Region

By Region

North America (By Training Type, Deployment Mode, Vehicle Type, End User, and Country)

United States

Canada

Mexico

Europe (By Training Type, Deployment Mode, Vehicle Type, End User, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Training Type, Deployment Mode, Vehicle Type, End User, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Training Type, Deployment Mode, Vehicle Type, End User, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Training Type, Deployment Mode, Vehicle Type, End User, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Fleet Driver Risk Management and Performance Optimization

Regulatory Compliance, Certification, and Structured Retraining Programmes

Public-Sector Road Safety Initiatives and Government-Led Training Frameworks

Global Adoption Trends in Professional and Commercial Driver Training Services

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

UK Bus & Coach Fleet Leasing, Rental and Finance Market Size, Share, Trends, 2033

UK Bus & Coach Fleet Leasing, Rental and Finance market size is valued at USD 886.4 million in 2025 and is projected to reach USD 1,442.8 million in 2033, at a CAGR of 6.3% from 2026 to 2033

UK Bus & Coach Fleet Leasing, Rental and Finance Market, UK Bus & Coach Fleet Leasing, Rental and Finance Market Size, UK Bus & Coach Fleet Leasing, Rental and Finance Market Share, UK Bus & Coach Fleet Leasing, Rental and Finance Market Analysis, UK Bus & Coach Fleet Leasing, Rental and Finance Market Growth, UK Bus & Coach Fleet Leasing, Rental and Finance Market Trends, UK Bus & Coach Fleet Leasing, Rental and Finance Market Research Report, UK Bus & Coach Fleet Leasing, Rental and Finance Market Forecast, UK Bus & Coach Fleet Leasing, Rental and Finance, UK Bus & Coach Fleet Leasing, Rental and Finance Market Research, UK Bus & Coach Fleet Leasing, Rental and Finance Industry, UK Bus & Coach Fleet Leasing, Rental and Finance Industry Report, UK Bus & Coach Fleet Leasing, Rental and Finance Market Data, UK Bus & Coach Fleet Leasing, Rental and Finance Statistics, UK Bus & Coach Fleet Leasing, Rental and Finance Market Statistics, UK Bus & Coach Fleet Leasing, Rental and Finance Industry Trends, UK Bus & Coach Fleet Leasing, Rental and Finance Market Report, UK Bus & Coach Fleet Leasing, Rental and Finance Market Trends, UK Bus & Coach Fleet Leasing, Rental and Finance Market News, UK Bus & Coach Fleet Leasing, Rental and Finance Forecasts, UK Bus & Coach Fleet Leasing, Rental and Finance Market Intelligence Report

Inductive Loop Vehicle Detector market size is valued at USD 93.1 million in 2025 and is projected to reach USD 205.5 million in 2033, at a CAGR of 10.4% from 2026 to 2033.

USA EVSE Procurement Market Size, Share, Trends, 2033

USA EVSE Procurement market size is valued at USD 6.6 billion in 2025 and is projected to reach USD 52.1 billion in 2033, at a CAGR of 29.5% from 2026 to 2033.

USA EVSE Procurement Market, USA EVSE Procurement Market Size, USA EVSE Procurement Market Share, USA EVSE Procurement Market Analysis, USA EVSE Procurement Market Growth, USA EVSE Procurement Market Trends, USA EVSE Procurement Market Research Report, USA EVSE Procurement Market Forecast, USA EVSE Procurement, USA EVSE Procurement Market Research, USA EVSE Procurement Industry, USA EVSE Procurement Industry Report, USA EVSE Procurement Market Data, USA EVSE Procurement Statistics, USA EVSE Procurement Market Statistics, USA EVSE Procurement Industry Trends, USA EVSE Procurement Market Report, USA EVSE Procurement Market Trends, USA EVSE Procurement Market News, USA EVSE Procurement Forecasts, USA EVSE Procurement Market Intelligence Report

Heavy Duty Truck Wash Market Size, Share, Trends, 2033

Global Heavy Duty Truck Wash market size is valued at USD 1,240.7 million in 2025 and is projected to reach USD 1,863.2 million in 2033, at a CAGR of 5.0% from 2026 to 2033

Heavy Duty Truck Wash Market, Heavy Duty Truck Wash Market Size, Heavy Duty Truck Wash Market Share, Heavy Duty Truck Wash Market Analysis, Heavy Duty Truck Wash Market Growth, Heavy Duty Truck Wash Market Trends, Heavy Duty Truck Wash Market Research Report, Heavy Duty Truck Wash Market Forecast, Heavy Duty Truck Wash, Heavy Duty Truck Wash Market Research, Heavy Duty Truck Wash Industry, Heavy Duty Truck Wash Industry Report, Heavy Duty Truck Wash Market Data, Heavy Duty Truck Wash Statistics, Heavy Duty Truck Wash Market Statistics, Heavy Duty Truck Wash Industry Trends, Heavy Duty Truck Wash Market Report, Heavy Duty Truck Wash Market Trends, Heavy Duty Truck Wash Market News, Heavy Duty Truck Wash Forecasts, Heavy Duty Truck Wash Market Intelligence Report