Commercial Vehicle Adhesives Market Size, Share, By Resin Type (Polyurethanes, Epoxy, Acrylics, Silicone, Silyl-Modified Polymers (SMP), Polyamide, and Others), By Technology (Hotmelt, Solvent-Based, Water-Based, Pressure-Sensitive, and Others), By Applications (Body-in-White, Paintshop, Powertrain, and Assembly), By End User (OEMs and Aftermarket), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4585

Published

April 9, 2026

Pages

320 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

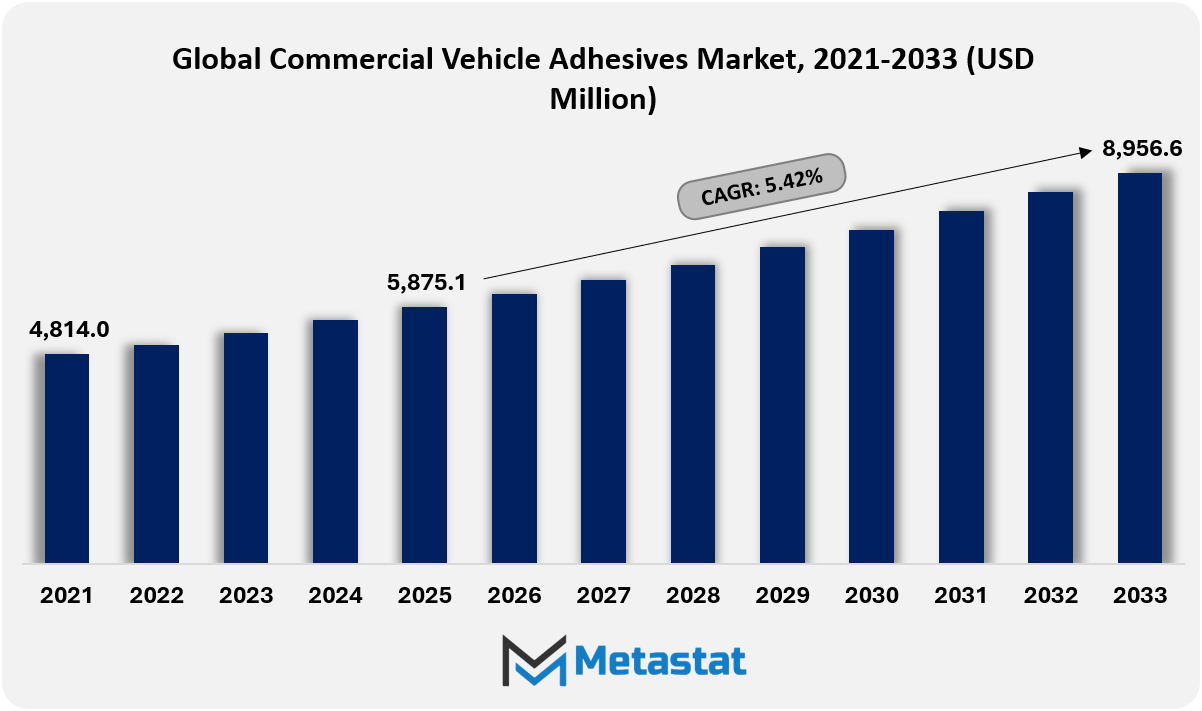

The Global Commercial Vehicle Adhesives market size is valued at USD 5,875.1 million in 2025 and projected to grow at a CAGR of 5.4% during the forecast period, reaching USD 8,956.6 million by 2033.

Global Commercial Vehicle Adhesives Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

Global Commercial Vehicle Adhesives market was valued at USD 5,875.1 million in 2025 and is projected to reach USD 8,956.6 million by 2033, at a CAGR of 5.4% during 2026-2033.

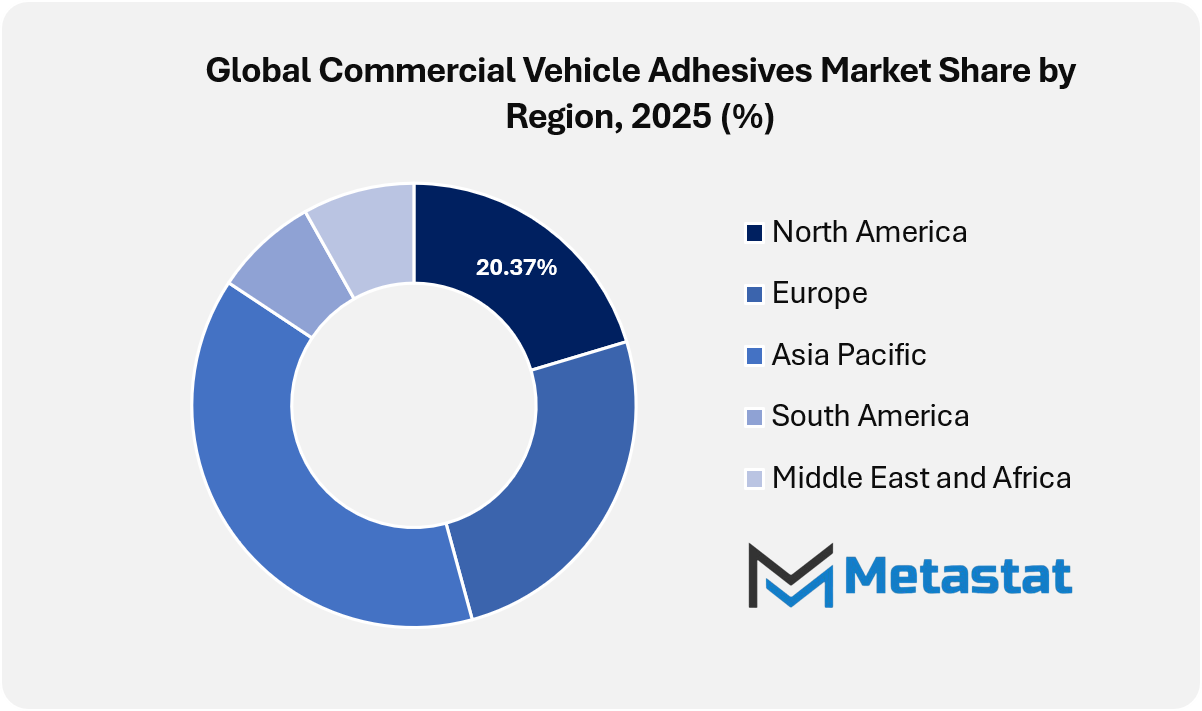

North America held 20.4% share in 2025, led by the United States.

Polyurethanes segment accounted for 25.2% share in 2025.

Key trends driving growth include increased adoption of lightweight materials in commercial vehicles, propelling advanced adhesive bonding over mechanical fastening, along with a rising focus on durability, noise reduction, and structural integrity across long-haul vehicle platforms, supporting wider adhesive integration.

Opportunities include the expansion of electric and next-generation commercial vehicle production, creating strong potential for multifunctional adhesives in battery, thermal, and structural bonding applications.

Key insight: Lightweight design priorities and electrification trends reshape adhesive demand across global commercial vehicle manufacturing.

The global commercial vehicle adhesives market is projected to expand beyond current penetration levels, supported by deeper integration into vehicle engineering programs that prioritize structural efficiency over mechanical reliance. Adhesive technologies increasingly operate as design-enabling inputs, shaping how cabins, chassis interfaces, and load-bearing assemblies are specified during early development stages.

Future applications are likely to align strongly with modular vehicle architectures. Adhesives are projected to support interchangeable body panels, flexible cargo systems, and adaptive interior layouts for logistics fleets with varied operating profiles. This shift is likely to strengthen collaboration between adhesive formulators and vehicle design teams, improving decision-making efficiency within production planning cycles.

Market Dynamics

Growth Drivers:

Increased adoption of lightweight materials in commercial vehicles propels the use of advanced adhesive bonding over mechanical fastening.

Increased adoption of lightweight materials across commercial vehicle manufacturing strengthens preference for adhesive bonding over mechanical fastening. Lower vehicle mass supports fuel-efficiency targets and tightening emission standards. Over the forecast period, structural adhesives support mixed-material assemblies and improve design flexibility while maintaining long-haul performance requirements.

Rising focus on durability, noise reduction, and structural integrity across long-duty vehicle platforms supports adhesive integration.

Rising focus on durability, noise reduction, and structural integrity across heavy-duty transport platforms strengthens adhesive use across cabins, panels, and chassis zones. Advanced bonding solutions enhance vibration control and fatigue resistance. Longer service cycles in fleet operations encourage manufacturers to integrate adhesive technologies aligned with durability-driven engineering goals.

Restraints and Challenges:

Higher material and process costs for high-performance adhesives restrict penetration among cost-sensitive fleet operators.

Higher material and process costs linked to high-performance adhesive systems restrict adoption among cost-sensitive fleet operators. Premium formulations often require specialized application equipment and trained labor. Over the forecast period, pricing pressure across logistics and freight operators influences procurement decisions, slowing broader penetration despite operational benefits delivered by adhesive bonding solutions.

Stringent qualification and validation requirements from OEMs extend approval timelines for new adhesive solutions.

Stringent qualification and validation protocols imposed by original equipment manufacturers extend approval timelines for new adhesive technologies. Extensive testing for safety, thermal stability, and load-bearing performance delays commercialization. Such process intensity increases entry barriers and slows the pace of innovation within the global commercial vehicle adhesives market.

Opportunities:

Expanding electric and next-generation commercial vehicle production creates strong opportunities for multifunctional adhesives in battery, thermal, and structural bonding applications.

Expansion of electric and next-generation commercial vehicle production creates strong avenues for multifunctional adhesive solutions supporting battery enclosures, thermal management systems, and lightweight structures. Electrification reshapes bonding requirements across platforms. Manufacturers are investing in adhesive innovation supporting energy efficiency, safety compliance, and modular vehicle architecture evolution.

Market Segmentation Analysis

The Global Commercial Vehicle Adhesives market is classified based on Resin Type, Technology, Applications, and End User.

By Resin Type, the market is further segmented into:

Polyurethanes

Polyurethanes segment is estimated at USD 1,556.5 million in 2026 and is projected to reach USD 2,410.2 million by 2033, at a CAGR of 6.4% during the forecast period.

Polyurethane-based adhesives will gain stronger preference owing to flexibility, vibration resistance, and high bonding strength across mixed substrates. Future commercial vehicle platforms will adopt polyurethane systems to support modular designs and improved structural durability, supporting longer service cycles under heavy loads and variable operating conditions.

Epoxy

Epoxy segment is estimated at USD 1,368.3 million in 2026 and is projected to reach USD 1,911.3 million by 2033, at a CAGR of 4.9% during the forecast period.

Epoxy formulations will retain their secure call for applications in which high mechanical and thermal stability remain critical. Power-dense vehicle architectures will require epoxy adhesives for critical joints, strengthening resistance to chemical exposure, fatigue stresses, and temperature fluctuations linked to next-generation freight operations.

Acrylics

Acrylics segment is estimated at USD 1,149.1 million in 2026 and is projected to reach USD 1,645.3 million by 2033, at a CAGR of 5.3% during the forecast period.

Acrylic adhesive systems will see rising adoption owing to fast-curing profiles and compatibility with automated production lines. Commercial vehicle manufacturers will use acrylic solutions to accelerate assembly timelines while maintaining bonding reliability across metals and composite materials aligned with productivity-focused manufacturing strategies.

Silicone

Silicone segment is estimated at USD 631.1 million in 2026 and is projected to reach USD 865.2 million by 2033, at a CAGR of 4.6% during the forecast period.

Silicone adhesives will preserve relevance in programs requiring elasticity and heat resistance. Future vehicle electrification developments will guide the usage of silicone in sealing and insulation features, mainly in which thermal cycling balance and moisture resistance affect durability and operational safety benchmarks.

SMP (Silyl-Modified Polymers)

SMP (Silyl-Modified Polymers) segment is estimated at USD 606.2 million in 2026 and is projected to reach USD 970 million by 2033, at a CAGR of 6.9% during the forecast period.

Silyl-modified polymer adhesives will experience gradual adoption due to their hybrid performance characteristics, combining strength and flexibility. OEM sustainability programs will support SMP solutions for improved assembly practices, offering lower emissions during application and improved recyclability alignment within evolving environmental compliance frameworks.

Polyamide

Polyamide segment is estimated at USD 408.7 million in 2026 and is projected to reach USD 485.4 million by 2033, at a CAGR of 2.5% during the forecast period.

Polyamide adhesives will support applications demanding abrasion resistance and durability under mechanical stress. Heavy-duty commercial platforms will integrate polyamide solutions to reinforce load-bearing zones, promoting structural stability and wear resistance in extended mileage and intensive operating schedules.

Others

Others segment is estimated at USD 467.5 million in 2026 and is projected to reach USD 669.1 million by 2033, at a CAGR of 5.3% during the forecast period.

Alternative resin ranges will address specific bonding requirements driven by material diversification and custom vehicle specifications. Specialty adhesive development will be expanded to support advanced composites and smart materials integration in line with emerging transportation engineering objectives.

By Technology, the market is divided into:

Hotmelt

Hotmelt segment is projected to reach USD 1,709.8 million by 2033, at a CAGR of 6.2% during the forecast period.

Hot-melt adhesive technology will be supported by automation compatibility and energy-efficient application processes. Commercial vehicle assembly lines will increasingly deploy hot-melt systems to achieve faster bonding cycles, lower curing delays, and consistent performance across high-volume production environments.

Solvent-Based

Solvent-Based segment is projected to reach USD 2,013.4 million by 2033, at a CAGR of 4% during the forecast period.

Solvent-based adhesives will retain managed utilization where high bonding performance outweighs environmental constraints. Regulatory alignment will involve manual formula refinement, ensuring compliance while maintaining adhesion reliability required for specialised business automobile additives.

Water-Based

Water-Based segment is projected to reach USD 2,304.5 million by 2033, at a CAGR of 7.1% during the forecast period.

Water-based adhesive technologies will see increased adoption, supported by sustainability initiatives and workplace safety standards. Commercial vehicle manufacturers will deploy water-based systems to reduce emissions while maintaining suitable bonding strength for interior and non-structural applications.

Pressure-Sensitive

Pressure-Sensitive segment is projected to reach USD 1,681.2 million by 2033, at a CAGR of 5.4% during the forecast period.

Pressure-sensitive adhesives will gain relevance in lightweight component fixation and insulation tasks. Future commercial vehicle designs will use pressure-sensitive formats to simplify installation processes while supporting noise control and vibration-damping performance targets.

Others

Others segment is projected to reach USD 1,247.7 million by 2033, at a CAGR of 4.1% during the forecast period.

Emerging adhesive technologies will maintain development to satisfy evolving manufacturing complexity. Innovation pipelines will focus on multifunctional bonding answers able to adapt to automation, electrification, and smart automobile integration trends.

By Applications, the market is further divided into:

Body-in-White

Body-in-White segment is projected to reach USD 2,403.9 million by 2033.

Body-in-white applications will represent an important growth area supported by structural bonding demand. Adhesive use will enhance stiffness, corrosion resistance, and crash performance while supporting weight reduction goals for future commercial vehicle efficiency strategies.

Paintshop

Paintshop segment is projected to reach USD 1,243.2 million by 2033.

Paintshop adhesive applications will evolve to support surface preparation, sealing, and finish durability. Advanced adhesive solutions will enable smoother coatings, lower defect rates, and improved aesthetic longevity in line with brand differentiation objectives.

Powertrain

Powertrain segment is projected to reach USD 2,011.6 million by 2033.

Powertrain adhesive use will increase along with electrification and hybrid system expansion. High-performance bonding solutions will secure thermal management components, reduce vibration effects, and support compact system architectures demanded by future drivetrain innovation.

Assembly

Assembly segment is projected to reach USD 3,297.8 million by 2033.

Assembly-stage adhesive integration will streamline production workflows and reduce mechanical fastener dependency. Commercial vehicle manufacturers will prefer adhesive-driven assembly for improved design flexibility, increased structural integrity, and cost optimization in mass production cycles.

By End User, the Global Commercial Vehicle Adhesives market is divided as:

OEMs

OEMs segment is projected to grow at a CAGR of 5.2% during the forecast period.

Original equipment manufacturers will remain the primary adopters owing to early-stage integration capabilities. Strategic OEM and supplier partnerships will support customized bonding solutions aligned with proprietary vehicle platforms and defined regulatory performance benchmarks.

Aftermarket

Aftermarket segment is projected to grow at a CAGR of 6.1% during the forecast period.

Aftermarket demand will increase through maintenance, repair and renovation activities. Adhesive solutions will support extended vehicle lifecycles, enabling efficient part replacement and structural reinforcement without extensive disassembly requirements.

By Region:

Based on geography, the Global Commercial Vehicle Adhesives market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Commercial Vehicle Adhesives Market is set to expand at a CAGR of 5.4% during 2026-2033, reaching a market size (TAM) of USD 1,802.6 million by 2033.

North America drives the global commercial vehicle adhesives market through increasing production of electric trucks supported by stringent emission norms and lightweight design priorities.

North America strengthens demand for advanced bonding solutions due to increased adoption of modular vehicle architectures among logistics and fleet operators.

Asia Pacific presents strong opportunities within the global commercial vehicle adhesives market through the rapid expansion of commercial vehicle manufacturing centers in China and India.

Asia Pacific unlocks growth potential supported by infrastructure-led freight demand and increasing localization of adhesives supply chains.

The Middle East, Africa, and South America reflect steady progress for the global commercial vehicle adhesives market, supported by gradual fleet modernization, construction-linked transportation demand, and improving industrial assembly standards.

Competitive Landscape and Strategic Insights

The Global Commercial Vehicle Adhesives Market shows a steady shift in how manufacturers approach vehicle assembly, durability, and efficiency. Adhesives support bonding across mixed materials used in vans, buses, and heavy-duty trucks, enabling lightweight structures and cleaner finishes. Increased adoption supports vibration control and resistance to heat and moisture. Rising demand for fuel-efficient commercial vehicles and tighter safety requirements across manufacturing lines is strengthening market momentum.

Several players shape product improvement and alertness requirements within the industry. Henkel Adhesives, Sika, 3M, H.B. Fuller, and Bostik under Arkema keep sturdy positions through broad portfolios masking structural, indoor, and outdoors bonding desires. DuPont, Dow, and Huntsman Advanced Materials recognition on advanced chemical solutions suited for demanding vehicle environments. These companies assist producers through steady performance, technical support, and long-term reliability across more than one automobile platform.

Other players contribute specialized expertise that strengthens market depth. Parker LORD, ITW Plexus, Jowat, Permabond, DELO Industrial Adhesives, Dymax, Gurit, Permatex, Loxeal, Hylomar, Chemence, Evonik, KCC Silicone, and Silicone Solutions address niche bonding, sealing, and vibration management requirements. Their solutions find use in panels, glazing, electronics protection, and interior fittings, helping manufacturers meet design and safety needs without adding extra weight.

Tape and film adhesive vendors also maintain strong relevance in business automobile production. Companies that include Tesa SE, Nitto Denko, Saint-Gobain Tape Solutions, Lohmann, Lintec, Mativ, Shurtape Technologies, Nichiban, Teraoka Seisakusho, and Sekisui Chemical guide applications together with wire management, surface protection, insulation, and noise discount. Their products support streamlined assembly processes and consistent quality control across large-scale manufacturing. Together, those industry players keep shaping the route of the Global Commercial Vehicle Adhesives Market through innovation, adaptability, and practical manufacturing assistance.

Forecast and Future Outlook

Market size is forecast to rise from USD 5,875.1 million in 2025 to over USD 8,956.6 million by 2033.

The global commercial vehicle adhesives market is expected to progress in a phase defined by technical specification and application-driven customization. Competitive positioning is likely to depend on the ability to align chemical performance with evolving vehicle platforms, regulatory frameworks and operational realities, reflecting a shift from volume orientation towards precision-based value creation.

Commercial Vehicle Adhesives Market Key Segments:

By Resin Type:

Polyurethanes

Epoxy

Acrylics

Silicone

SMP (Silyl-Modified Polymers)

Polyamide

Others

By Technology:

Hotmelt

Solvent-Based

Water-Based

Pressure-Sensitive

Others

By Application:

Body-in-White

Paintshop

Powertrain

Assembly

By End User:

OEMs

Aftermarket

Key Global Commercial Vehicle Adhesives Industry Players

This research report categorizes the Commercial Vehicle Adhesives market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyzes the key growth drivers, opportunities, and challenges influencing the Commercial Vehicle Adhesives market. Recent market developments and competitive strategies such as expansion, new site development, partnership, merger, and acquisition are included to present the competitive landscape.

The report strategically identifies and profiles key market players and analyzes their core competencies across sub-segments of the Commercial Vehicle Adhesives market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 5.4% from 2026 to 2033

Revenue Unit

USD million

Sales Volume Unit

Kilotons

Segmentation

By Resin Type, Technology, Application, End User, and Region

By Region

North America (By Resin Type, Technology, Application, End User, and Country)

United States

Canada

Mexico

Europe (By Resin Type, Technology, Application, End User, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Resin Type, Technology, Application, End User, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Resin Type, Technology, Application, End User, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Resin Type, Technology, Application, End User, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Key Company Market Share and Revenue

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

UK Bus & Coach Fleet Leasing, Rental and Finance Market Size, Share, Trends, 2033

UK Bus & Coach Fleet Leasing, Rental and Finance market size is valued at USD 886.4 million in 2025 and is projected to reach USD 1,442.8 million in 2033, at a CAGR of 6.3% from 2026 to 2033

UK Bus & Coach Fleet Leasing, Rental and Finance Market, UK Bus & Coach Fleet Leasing, Rental and Finance Market Size, UK Bus & Coach Fleet Leasing, Rental and Finance Market Share, UK Bus & Coach Fleet Leasing, Rental and Finance Market Analysis, UK Bus & Coach Fleet Leasing, Rental and Finance Market Growth, UK Bus & Coach Fleet Leasing, Rental and Finance Market Trends, UK Bus & Coach Fleet Leasing, Rental and Finance Market Research Report, UK Bus & Coach Fleet Leasing, Rental and Finance Market Forecast, UK Bus & Coach Fleet Leasing, Rental and Finance, UK Bus & Coach Fleet Leasing, Rental and Finance Market Research, UK Bus & Coach Fleet Leasing, Rental and Finance Industry, UK Bus & Coach Fleet Leasing, Rental and Finance Industry Report, UK Bus & Coach Fleet Leasing, Rental and Finance Market Data, UK Bus & Coach Fleet Leasing, Rental and Finance Statistics, UK Bus & Coach Fleet Leasing, Rental and Finance Market Statistics, UK Bus & Coach Fleet Leasing, Rental and Finance Industry Trends, UK Bus & Coach Fleet Leasing, Rental and Finance Market Report, UK Bus & Coach Fleet Leasing, Rental and Finance Market Trends, UK Bus & Coach Fleet Leasing, Rental and Finance Market News, UK Bus & Coach Fleet Leasing, Rental and Finance Forecasts, UK Bus & Coach Fleet Leasing, Rental and Finance Market Intelligence Report

Inductive Loop Vehicle Detector market size is valued at USD 93.1 million in 2025 and is projected to reach USD 205.5 million in 2033, at a CAGR of 10.4% from 2026 to 2033.

USA EVSE Procurement Market Size, Share, Trends, 2033

USA EVSE Procurement market size is valued at USD 6.6 billion in 2025 and is projected to reach USD 52.1 billion in 2033, at a CAGR of 29.5% from 2026 to 2033.

USA EVSE Procurement Market, USA EVSE Procurement Market Size, USA EVSE Procurement Market Share, USA EVSE Procurement Market Analysis, USA EVSE Procurement Market Growth, USA EVSE Procurement Market Trends, USA EVSE Procurement Market Research Report, USA EVSE Procurement Market Forecast, USA EVSE Procurement, USA EVSE Procurement Market Research, USA EVSE Procurement Industry, USA EVSE Procurement Industry Report, USA EVSE Procurement Market Data, USA EVSE Procurement Statistics, USA EVSE Procurement Market Statistics, USA EVSE Procurement Industry Trends, USA EVSE Procurement Market Report, USA EVSE Procurement Market Trends, USA EVSE Procurement Market News, USA EVSE Procurement Forecasts, USA EVSE Procurement Market Intelligence Report

Heavy Duty Truck Wash Market Size, Share, Trends, 2033

Global Heavy Duty Truck Wash market size is valued at USD 1,240.7 million in 2025 and is projected to reach USD 1,863.2 million in 2033, at a CAGR of 5.0% from 2026 to 2033

Heavy Duty Truck Wash Market, Heavy Duty Truck Wash Market Size, Heavy Duty Truck Wash Market Share, Heavy Duty Truck Wash Market Analysis, Heavy Duty Truck Wash Market Growth, Heavy Duty Truck Wash Market Trends, Heavy Duty Truck Wash Market Research Report, Heavy Duty Truck Wash Market Forecast, Heavy Duty Truck Wash, Heavy Duty Truck Wash Market Research, Heavy Duty Truck Wash Industry, Heavy Duty Truck Wash Industry Report, Heavy Duty Truck Wash Market Data, Heavy Duty Truck Wash Statistics, Heavy Duty Truck Wash Market Statistics, Heavy Duty Truck Wash Industry Trends, Heavy Duty Truck Wash Market Report, Heavy Duty Truck Wash Market Trends, Heavy Duty Truck Wash Market News, Heavy Duty Truck Wash Forecasts, Heavy Duty Truck Wash Market Intelligence Report