Breast Cancer Market By Type (Ductal Carcinoma In Situ (DCIS), Invasive Ductal Carcinoma (IDC), Invasive Lobular Carcinoma (ILC), and Other), By Treatment (Surgery, Radiation Therapy, Chemotherapy, Hormone Therapy, Targeted Therapy, Medication, and Other), By End User (Hospitals, Specialty Clinics and Ambulatory Surgical Centers), By Stage (Stage 0, Stage I, Stage II, Stage III, and Stage IV), Industry Analysis, Size, Share, Growth, Trends, and Forecast, 2033

Report ID

MSI-4286

Published

January 15, 2026

Pages

255 Pages

Format

Market Size 2026

Leadership Strategies

Key Trends

Market Size 2033

Report Details

Comprehensive Market Analysis And Insights

Global Breast Cancer Market- Comprehensive Data-Driven Market Analysis & Strategic Outlook

The global breast cancer market is a dynamic, multifaceted part of the overall oncology market that today includes diagnostics, therapeutics, and care services. It is a story that starts some decades ago when breast cancer initially appeared as a serious scientific question as a distinct disease process in its own right and not just a clinical curiosity. Surgeons and pathologists of the mid-20th century recognized patterns of breast tumors, and mastectomy was standard, albeit radical, therapy

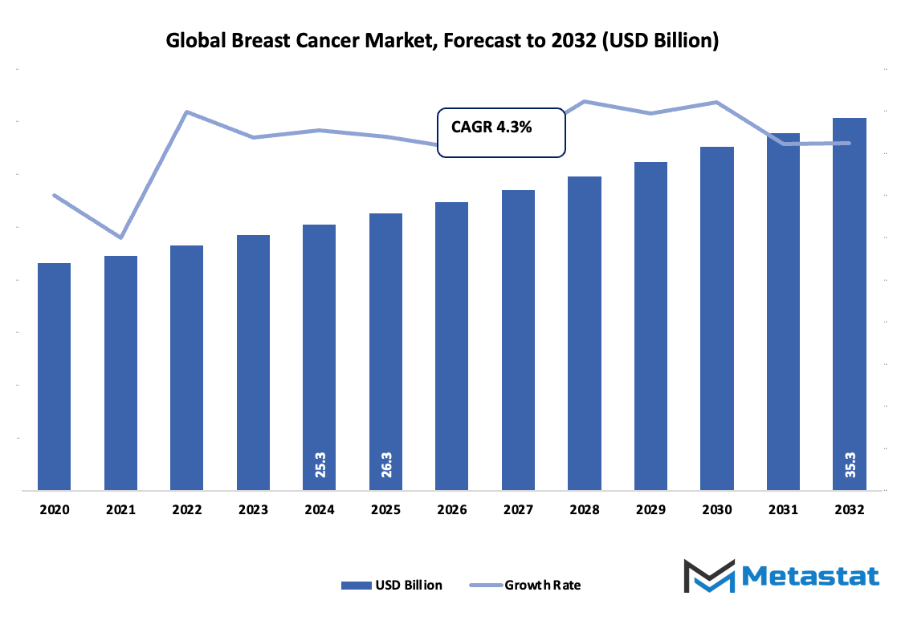

Global breast cancer market size of about USD 26.3 million in 2025 and slated to grow at a CAGR of about 4.3% over the forecast years 2032 with potential reaching more than USD 35.3 million.

Ductal Carcinoma In Situ (DCIS) lead the chart with near 15.5% market share, seeking and investigating new applications by vigorous research.

Driver forces fueling growth: Increased awareness and uptake of early detection and screening initiatives, Targeted treatments and precision medicine evolving

Opportunities: New diagnostic equipment and minimally invasive therapies introduction

Major observation: The market will see several times value growth within the coming decade, with potential for dramatic growth.

Chemotherapy and hormone therapy had entered the debate in time. Adjuvant therapy after surgery in the 1970s and 1980s was a breakthrough with mounting survival outcomes. In the 1990s, with new targeted drugs such as tamoxifen in estrogen receptor–positive disease, treatment individualization was reconsidered by doctors. During this period, screening trials for mammography introduced into the clinic the principle that detection of small lesions at an earlier stage would improve outcomes. Diagnoses and treatments hence evolved side by side, each influencing the market. The researchers also expanded molecular biology and genomics in the early 2000s. It became common to subtype tumors by HER2 status, hormone receptor status, and gene expression profiles. Oncology DX and MammaPrint exams began to drive treatment, reducing overtreatment and tailoring the level of therapy. That revolution transformed the marketplace: pharmaceutical companies were forced to partner with diagnostic companies, and payers started demanding evidence of cost-effectiveness.

Two trends have steered the path of the market over the past decade. First, more vocal patients: less toxic therapy, oral therapy, and improved quality of life during therapy picked up momentum. Breast cancer survivors and patient advocacy groups demanded access and equity geographically. Second, regulators began to approve new modalities antibody-drug conjugates, PARP inhibitors, CDK4/6 inhibitors with companion diagnostics as part of approval. That drug-diagnostic link allowed closer coordination in product development.

Regulatory, the majority of governments initiated coverage mandates on genetic testing and screening, progressing penetration into the previously undercovered populations. Health technology assessment organizations began requiring value evidence, which encouraged companies to produce real-world evidence and biomarker validation. In addition, digital health, telemedicine, and AI-based imaging models supplemented outreach and triage and established new channels in low- and middle-income nations.

The global breast cancer market trends have evolved due to surgical, chemotherapeutic, hormonal, and molecular advances. It is currently confronted with new points of inflection: new world prevalence growth, demands for affordability and access equivalence, and convergence of liquid biopsy and AI innovation. The market will, in the foreseeable future, continue to draw towards early detection, prevention and precautionary measures, and flexible therapy models. Its fate will be founded on equipoise between science innovation, patient expectation, and health system constraint.

Market Segments

The global breast cancer market is mainly classified based on Type, Treatment, End User, Stage.

By Type is further segmented into:

Ductal Carcinoma In Situ (DCIS): DCIS is a stage-one pre-cancerous breast cancer with non-invasive traits where the affected cells are within the lining of a breast duct. DCIS will be invasive cancer if left untreated. The patient outcomes must be optimized with prompt diagnosis and treatment in the global breast cancer market.

Invasive Ductal Carcinoma (IDC): IDC is the most common breast cancer. It starts in the milk ducts and spreads to other breast tissues. Treatment of the disease is focused on avoiding further growth of the tumor and prolonging survival. This cancer is the major propellant of breast cancer market growth and demand across the world.

Invasive Lobular Carcinoma (ILC): ILC starts in the lobules, or the glands that produce milk, and over time can spread to nearby tissues. It can be harder to find on imaging exams than others. The incidence of ILC affects research and treatments for the Breast Cancer global market.

Other: They are other kinds of breast cancer that are excluded in DCIS, IDC, or ILC. They might have separate therapy and diagnosis procedures. They form a smaller but sizable share of the global breast cancer market.

By Treatment the market is divided into:

Ductal Carcinoma In Situ (DCIS): DCIS is a stage-one pre-cancerous breast cancer with non-invasive traits where the affected cells are within the lining of a breast duct. DCIS will be invasive cancer if left untreated. The patient outcomes must be optimized with prompt diagnosis and treatment in the global breast cancer market.

Invasive Ductal Carcinoma (IDC): IDC is the most common breast cancer. It starts in the milk ducts and spreads to other breast tissues. Treatment of the disease is focused on avoiding further growth of the tumor and prolonging survival. This cancer is the major propellant of breast cancer market growth and demand across the world.

Invasive Lobular Carcinoma (ILC): ILC starts in the lobules, or the glands that produce milk, and over time can spread to nearby tissues. It can be harder to find on imaging exams than others. The incidence of ILC affects research and treatments for the Breast Cancer global market.

Other: They are other kinds of breast cancer that are excluded in DCIS, IDC, or ILC. They might have separate therapy and diagnosis procedures. They form a smaller but sizable share of the global breast cancer market.

On the basis of Treatment the industry is divided into:

Surgery: The most frequent first-line treatment for breast cancer is surgery, where the tumor is removed or the cancerous breast tissue is removed. It enables local disease control and offers tissue for histopathological assessment. Surgical techniques are a major growth driver for the overall breast cancer market.

Radiation Therapy: Radiation therapy employs beams of high energy to destroy cancer cells after surgery or as standalone treatment. It reduces the likelihood of recurrence. Innovations in precision technologies further expand its application within the world Breast Cancer market.

Chemotherapy: Chemotherapy is treatment with drugs to kill cancer cells within the body. Chemotherapy is used when cancer is established or has a tendency to relapse. Its use remains the center in the world trend of the breast cancer market.

Hormone Therapy: Hormone therapy reduces or blocks hormones that fuel some types of breast cancer. Hormone therapy is effective for hormone receptor-positive breast cancer and stops cancer from growing. Hormone therapy dominates the world's Breast Cancer market significantly.

Targeted Therapy: Targeted therapy attacks specific molecules that help the cancer grow. It offers targeted treatment with less side effect compared to chemotherapy. Targeted therapy is increasing remarkably in the market.

Treatment: Treatment is medications that are used to heal symptoms or mitigate the progression of the illness. Treatment is an add-on to other treatment and improves quality of life for the patients. It is still an ongoing phase in the global breast cancer market.

Others: Others or experimental treatment involve other medication used in certain situations. These centers provide other control methods for breast cancer and expand research for the whole world's Breast Cancer market.

By End User the market is further divided into:

Hospitals: Hospitals provide comprehensive breast cancer care, including diagnosis, surgery, therapy, and follow-up. They serve as a major point of treatment delivery and research, playing a central role in the market.

Specialty Clinics: Specialty clinics focus on specific aspects of breast cancer care, such as oncology consultations and targeted therapies. These clinics help streamline treatment processes and support patient-centered care in the market.

Ambulatory Surgical Centers: Ambulatory surgical centers offer same-day procedures for less complex surgeries and therapies. They provide efficient care options and contribute to the treatment infrastructure of the global breast cancer market.

By Stage the global breast cancer market is divided as:

Stage 0: Stage 0 represents non-invasive breast cancer confined to the ducts. Early detection and intervention are key to preventing progression. It is an important focus area in the global breast cancer market for awareness and screening programs.

Stage I: Stage I indicates small tumors that have not spread extensively. Treatments at this stage aim to remove the tumor and prevent recurrence. Early-stage intervention is a priority within the market.

Stage II: Stage II involves larger tumors or limited spread to nearby lymph nodes. Treatment often combines surgery, radiation, and medication. This stage forms a significant portion of patient care in the market.

Stage III: Stage III includes more extensive tumors with significant lymph node involvement. Aggressive treatment approaches are required, combining multiple therapies. This stage reflects a critical segment of the market.

Stage IV: Stage IV represents advanced breast cancer that has spread to other organs. Treatment focuses on managing symptoms and prolonging survival. Advanced-stage care is a key consideration in the market.

Forecast Period

2025-2032

Market Size in 2025

$26.3Million

Market Size by 2032

$35.3 Million

Growth Rate from 2025 to 2032

4.3%

Base Year

2025

Regions Covered

North America, Europe, Asia-Pacific, South America, Middle East & Africa

By Region:

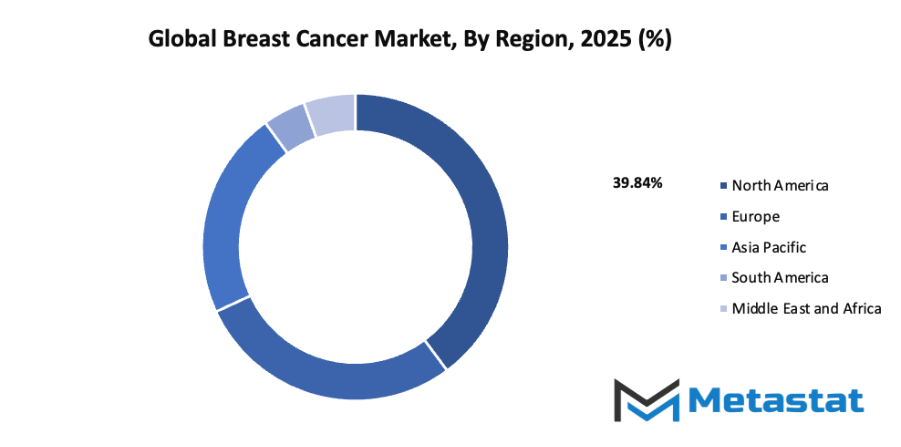

Based on geography, the global breast cancer market is divided into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

North America is further divided into the U.S., Canada, and Mexico, whereas Europe consists of the UK, Germany, France, Italy, and the Rest of Europe.

Asia-Pacific is segmented into India, China, Japan, South Korea, and the Rest of Asia-Pacific.

The South America region includes Brazil, Argentina, and the Rest of South America, while the Middle East & Africa is categorized into GCC Countries, Egypt, South Africa, and the Rest of the Middle East & Africa.

Growth Drivers

Increasing awareness and adoption of early detection and screening programs: The market will benefit from growing awareness campaigns and education about early detection. Screening programs will help identify cancer at earlier stages, improving survival rates. Governments and organizations will invest in outreach efforts, encouraging regular check-ups and self-examination practices to reduce late-stage diagnoses.

Advancements in targeted therapies and personalized medicine: The market will see significant growth through advancements in targeted therapies and personalized medicine. Tailored treatments will improve patient outcomes by focusing on specific cancer types and genetic profiles. Research and clinical trials will expand, allowing more effective drugs and therapies to reach patients faster, improving survival and quality of life.

Challenges and Opportunities

High cost of treatment and diagnostic procedures: High costs of treatments and diagnostic procedures will remain a challenge for the global breast cancer market. Expensive therapies and frequent testing can limit accessibility for many patients. Financial burden on healthcare systems and patients will slow adoption of advanced treatments, requiring solutions that balance effectiveness with affordability.

Limited access to healthcare facilities in low-resource regions: Limited healthcare facilities and infrastructure in low-resource regions will continue to restrict access to timely diagnosis and treatment. The market will face challenges in reaching rural and underserved populations. Efforts to expand healthcare infrastructure and mobile medical units will be necessary to improve access.

Opportunities

Development of innovative diagnostic tools and minimally invasive treatment options: The global breast cancer market will have opportunities through the development of innovative diagnostic tools and minimally invasive treatments. New technologies will allow earlier detection and less disruptive procedures, improving patient comfort and recovery. Investment in research and new devices will strengthen the market and expand access to better care.

Competitive Landscape & Strategic Insights

The global breast cancer market is poised to witness significant transformation in the coming years. This industry is a mix of both international industry leaders and emerging regional competitors, creating a competitive and dynamic environment. Key competitors include Roche Holding AG, Novartis AG, Pfizer Inc., Biocon Limited, Merck & Co., Inc., Eli Lilly and Company, Bristol-Myers Squibb Company, Gilead Sciences, Inc., Teva Pharmaceutical Industries Ltd., Sanofi, Incyte Corporation, AbbVie Inc., Daiichi Sankyo Company, Limited, Takeda Pharmaceutical Company Limited, and Mylan N.V. These companies have established strong positions through research, innovation, and strategic collaborations, while newer regional players are gradually increasing their influence by introducing cost-effective and region-specific solutions.

Future advancements in the breast cancer market will be driven by rapid developments in targeted therapies, immunotherapies, and personalized medicine. Precision medicine will play a crucial role, as treatments will increasingly focus on the genetic and molecular profile of individual patients. This shift will improve treatment outcomes and reduce side effects, making therapies more efficient and patient-centric. Technological progress in diagnostic tools will also help in early detection, enabling timely intervention and better management of the disease.

The market will experience continued globalization, with international leaders setting high benchmarks for research and innovation, while emerging competitors will challenge traditional models by offering region-specific solutions and leveraging cost advantages. Strategic partnerships between global and regional companies will become more common, enabling faster introduction of advanced therapies into local markets. Additionally, government policies and healthcare infrastructure improvements will play a significant role in shaping access to treatment across different regions.

Investment in research and development will remain a central focus, with companies competing to introduce novel therapies that address unmet medical needs. Artificial intelligence and data analytics will increasingly assist in identifying treatment patterns, predicting disease progression, and designing clinical trials more efficiently. These technological applications will help streamline drug discovery and development, allowing companies to respond more quickly to patient needs and market demands.

Market size is forecast to rise from USD 26.3 million in 2025 to over USD 35.3 million by 2032. Breast Cancer will maintain dominance but face growing competition from emerging formats.

The market will continue to grow, influenced by demographic changes, increasing awareness, and advances in treatment options. While established companies maintain their dominance through extensive research pipelines and financial strength, regional players will capitalize on agility and localized strategies. The interplay between global expertise and regional innovation will define the future landscape, offering hope for improved therapies and better patient outcomes worldwide.

Report Coverage

This research report categorizes the global breast cancer market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the global breast cancer market.

India Maternal Health Monitoring Market Size, Share, Trends, 2033

India Maternal Health Monitoring market size is valued at USD 416.0 million in 2025 and is projected to reach USD 834.4 million in 2033, at a CAGR of 9.1% from 2026 to 2033

India Maternal Health Monitoring Market, India Maternal Health Monitoring Market Size, India Maternal Health Monitoring Market Share, India Maternal Health Monitoring Market Analysis, India Maternal Health Monitoring Market Growth, India Maternal Health Monitoring Market Trends, India Maternal Health Monitoring Market Research Report, India Maternal Health Monitoring Market Forecast, India Maternal Health Monitoring, India Maternal Health Monitoring Market Research, India Maternal Health Monitoring Industry, India Maternal Health Monitoring Industry Report, India Maternal Health Monitoring Market Data, India Maternal Health Monitoring Statistics, India Maternal Health Monitoring Market Statistics, India Maternal Health Monitoring Industry Trends, India Maternal Health Monitoring Market Report, India Maternal Health Monitoring Market Trends, India Maternal Health Monitoring Market News, India Maternal Health Monitoring Forecasts, India Maternal Health Monitoring Market Intelligence Report

Global Anaerobic Incubators market size is valued at USD 177.5 million in 2025 and is projected to reach USD 323.6 million in 2033, at a CAGR of 7.8% from 2026 to 2033

Global Radiochemical Synthesizers market size is valued at USD 450.5 million in 2025 and is projected to reach USD 746.6 million in 2033, at a CAGR of 6.7% from 2026 to 2033.

Global Radiochemical Synthesizers Market, Global Radiochemical Synthesizers Market Size, Global Radiochemical Synthesizers Market Share, Global Radiochemical Synthesizers Market Analysis, Global Radiochemical Synthesizers Market Growth, Global Radiochemical Synthesizers Market Trends, Global Radiochemical Synthesizers Market Research Report, Global Radiochemical Synthesizers Market Forecast, Global Radiochemical Synthesizers, Global Radiochemical Synthesizers Market Research, Global Radiochemical Synthesizers Industry, Global Radiochemical Synthesizers Industry Report, Global Radiochemical Synthesizers Market Data, Global Radiochemical Synthesizers Statistics, Global Radiochemical Synthesizers Market Statistics, Global Radiochemical Synthesizers Industry Trends, Global Radiochemical Synthesizers Market Report, Global Radiochemical Synthesizers Market Trends, Global Radiochemical Synthesizers Market News, Global Radiochemical Synthesizers Forecasts, Global Radiochemical Synthesizers Market Intelligence Report

Thoracolumbar Posterior Fixation Systems Market Size, Share, Trends, 2033

Global Thoracolumbar Posterior Fixation Systems market size is valued at USD 875.8 million in 2025 and is projected to reach USD 1,526.6 million in 2033, at a CAGR of 7.2% from 2026 to 2033

Thoracolumbar Posterior Fixation Systems Market, Thoracolumbar Posterior Fixation Systems Market Size, Thoracolumbar Posterior Fixation Systems Market Share, Thoracolumbar Posterior Fixation Systems Market Analysis, Thoracolumbar Posterior Fixation Systems Market Growth, Thoracolumbar Posterior Fixation Systems Market Trends, Thoracolumbar Posterior Fixation Systems Market Research Report, Thoracolumbar Posterior Fixation Systems Market Forecast, Thoracolumbar Posterior Fixation Systems, Thoracolumbar Posterior Fixation Systems Market Research, Thoracolumbar Posterior Fixation Systems Industry, Thoracolumbar Posterior Fixation Systems Industry Report, Thoracolumbar Posterior Fixation Systems Market Data, Thoracolumbar Posterior Fixation Systems Statistics, Thoracolumbar Posterior Fixation Systems Market Statistics, Thoracolumbar Posterior Fixation Systems Industry Trends, Thoracolumbar Posterior Fixation Systems Market Report, Thoracolumbar Posterior Fixation Systems Market Trends, Thoracolumbar Posterior Fixation Systems Market News, Thoracolumbar Posterior Fixation Systems Forecasts, Thoracolumbar Posterior Fixation Systems Market Intelligence Report