MARKET OVERVIEW

The Global Automotive Simulation Market represents a dynamic sector within the automotive industry, offering crucial components essential for the production of vehicles worldwide. Automotive simulation plays a significant role in the manufacturing process, providing lightweight and durable parts that contribute to the performance, efficiency, and safety of modern automobiles.

In recent years, the demand for aluminium die-cast automotive parts has surged owing to the growing emphasis on lightweighting in the automotive sector. As manufacturers strive to meet stringent fuel efficiency and emission standards, they increasingly turn to automotive simulation for its ability to produce complex shapes with thin walls while maintaining structural integrity. This trend has propelled the expansion of the global market, with key players continually innovating to enhance production processes and meet evolving industry requirements.

One of the primary drivers of the market is the rising adoption of electric and hybrid vehicles (EVs and HEVs), which require lightweight components to maximize range and efficiency. Automotive simulation offers a viable solution for producing lightweight parts such as powertrain components, battery enclosures, and structural elements in electric vehicles. Additionally, the growing consumer demand for advanced safety features and enhanced driving experience has led to an increased integration of aluminium die-cast parts in automotive chassis, transmission systems, and suspension components.

Moreover, the automotive industry's shift towards autonomous vehicles and connected technologies is fueling the demand for sophisticated aluminium die-cast parts that support advanced sensor systems, electronic components, and vehicle connectivity infrastructure. As automakers continue to invest in research and development to bring autonomous and connected vehicles to market, the demand for high-precision automotive simulation is expected to rise further.

The global automotive simulation market is characterized by intense competition and rapid technological advancements. Key market players are focusing on strategic initiatives such as mergers and acquisitions, partnerships, and investments in research and development to gain a competitive edge and expand their market presence. Furthermore, advancements in die casting technology, including the integration of automation, robotics, and digital manufacturing solutions, are driving efficiency improvements and enabling manufacturers to meet the increasing demand for aluminium die-cast parts with shorter lead times and higher quality standards.

The Global automotive simulation market is a vital segment of the automotive industry, providing lightweight, durable, and high-performance components essential for modern vehicles. With the ongoing evolution of automotive technologies and the growing demand for electric, autonomous, and connected vehicles, the market is poised for sustained growth and innovation, presenting opportunities for manufacturers to thrive in an ever-changing landscape.

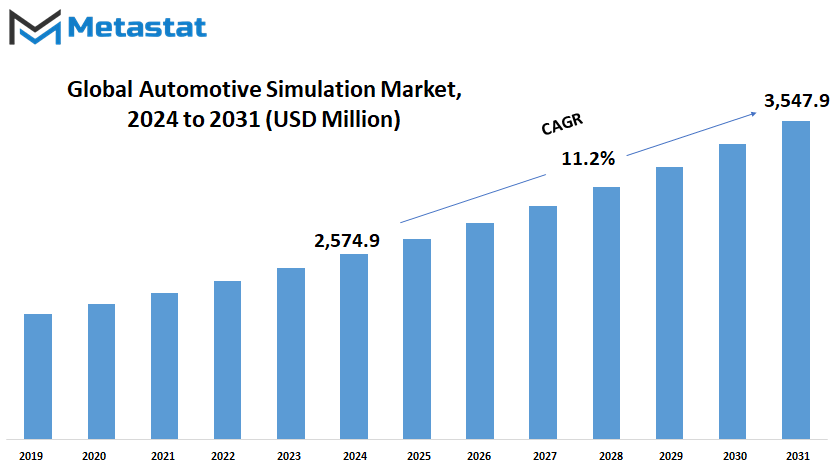

Global Automotive Simulation market is estimated to reach $3,547.9 Million by 2031; growing at a CAGR of 11.2% from 2024 to 2031.

GROWTH FACTORS

The Global Automotive Simulation market is experiencing notable growth owing to several key factors. One significant aspect driving this growth is the increasing complexity of automotive systems. Modern vehicles incorporate a myriad of advanced technologies and functionalities, necessitating comprehensive testing before physical implementation. Simulation enables manufacturers to assess the performance of these intricate systems in a virtual environment, ensuring they meet stringent quality standards before production.

Another pivotal factor contributing to the expansion of the automotive simulation market is the cost and time savings it offers compared to traditional prototyping and testing methods. Building physical prototypes can be time-consuming and expensive, whereas simulation allows for rapid iteration and testing of various design scenarios without the need for physical materials or equipment. This not only accelerates the product development cycle but also reduces overall development costs.

However, despite these advantages, there are challenges that could potentially impede the market's growth. One such challenge is the high initial investment required for developing and implementing simulation software and hardware. While the long-term benefits of simulation are evident, the upfront costs may deter some companies from adopting these technologies.

Moreover, there are limitations in accurately representing real-world scenarios within simulation environments. Factors such as environmental conditions, human behavior, and unforeseen interactions between system components can be challenging to replicate accurately. As a result, there may be discrepancies between simulation results and actual performance, raising concerns about the reliability of simulation-based testing.

Nevertheless, there are promising opportunities on the horizon for the automotive simulation market. The integration of artificial intelligence (AI) and machine learning (ML) technologies holds the potential to enhance the accuracy and predictive capabilities of automotive simulations. By leveraging AI and ML algorithms, simulation models can better adapt to dynamic real-world conditions, improving their effectiveness in predicting system behavior and performance.

The Global Automotive Simulation market is propelled by the need to address the increasing complexity of automotive systems and the cost and time savings offered by simulation technologies. While challenges such as high initial investment and limitations in accuracy exist, the integration of AI and ML presents exciting opportunities for future growth and innovation in the automotive industry.

MARKET SEGMENTATION

By Deployment

The global automotive simulation market is divided based on deployment into two main segments: On-premises and Cloud. These segments offer different ways for companies to access and utilize automotive simulation technology.

The On-premises deployment option involves installing and running the simulation software on the company's own servers and infrastructure. This means that the software and all related data are stored and managed internally, within the company's premises. On-premises deployment offers companies greater control and customization over their simulation environment. They can tailor the software to meet their specific needs and integrate it seamlessly with their existing systems and workflows. Additionally, On-premises deployment may be preferred by companies that have strict security and compliance requirements, as they can keep all sensitive data within their own network.

On the other hand, the Cloud deployment option involves accessing the simulation software and related services over the internet, through third-party providers' servers and infrastructure. With Cloud deployment, companies do not need to invest in or maintain their own hardware or software infrastructure. Instead, they can simply pay a subscription or usage-based fee to access the software on a pay-as-you-go basis. Cloud deployment offers several advantages, including scalability, flexibility, and accessibility. Companies can easily scale up or down their simulation resources based on their needs, without the need for additional investment in hardware or software. Additionally, Cloud deployment enables remote access to the simulation software, allowing users to collaborate and work from anywhere with an internet connection.

Both On-premises and Cloud deployment options have their own set of advantages and considerations. The choice between the two depends on factors such as the company's budget, IT infrastructure, security requirements, and desired level of control and flexibility. Some companies may opt for On-premises deployment to maintain full control over their simulation environment, while others may prefer Cloud deployment for its scalability and accessibility benefits.

The global automotive simulation market offers companies two main deployment options: On-premises and Cloud. These options provide different ways for companies to access and utilize simulation technology, each with its own set of advantages and considerations. Whether a company chooses On-premises or Cloud deployment depends on various factors, including budget, IT infrastructure, security requirements, and desired level of control and flexibility.

By Component

The global automotive simulation market encompasses various components, primarily divided into software and services. In 2020, the software segment recorded a value of $1324 million, while the services segment reached $362 million.

Simulation software plays a crucial role in the automotive industry, facilitating the design, testing, and optimization of vehicles and their components in a virtual environment. This software enables engineers and designers to simulate various scenarios, such as crash tests, aerodynamics, and performance analysis, without the need for physical prototypes. By leveraging simulation, automotive companies can streamline their development processes, reduce costs, and accelerate time-to-market for new products.

On the other hand, services in the automotive simulation market encompass a range of offerings, including consulting, training, and support. Companies providing these services assist clients in implementing simulation software effectively, optimizing their simulation workflows, and training their teams to utilize simulation tools efficiently. Additionally, service providers offer technical support to address any issues or challenges encountered during simulation activities.

The significance of simulation in the automotive industry cannot be overstated. With the growing complexity of vehicle designs and the increasing demand for safety and performance, simulation has become indispensable for automakers and suppliers. By simulating various scenarios and conditions, manufacturers can identify and address potential issues early in the development process, minimizing the risk of costly errors and recalls later on.

Moreover, simulation enables automotive companies to explore innovative design concepts and technologies rapidly. By iterating through different design iterations virtually, engineers can refine their ideas and optimize performance parameters before committing to physical prototypes. This iterative approach not only enhances product quality but also fosters innovation and creativity within the industry.

Furthermore, simulation plays a vital role in advancing vehicle electrification and autonomous driving technologies. With electric vehicles (EVs) gaining momentum and autonomous vehicles on the horizon, simulation allows manufacturers to simulate and validate complex systems and algorithms in a controlled environment. This capability is essential for ensuring the safety and reliability of next-generation vehicles and accelerating their adoption in the market.

The global automotive simulation market is characterized by its diverse components, including software and services. Simulation software enables virtual testing and optimization of vehicle designs, while services support clients in implementing and leveraging simulation technology effectively. With simulation becoming increasingly integral to automotive development processes, its role in driving innovation and advancing industry trends cannot be overlooked.

By Application

The Global Automotive Simulation market is a dynamic industry with various applications driving its growth. When we look at its applications, we see that it is divided into prototyping and testing. These two segments play significant roles in advancing automotive technology and ensuring the safety and efficiency of vehicles.

Prototyping is a crucial phase in the development of new vehicles. It involves creating a preliminary version or model of a product to test its feasibility and functionality. In the automotive industry, prototyping through simulation allows engineers to design and refine vehicle components and systems before physically constructing them. This not only saves time and resources but also enables engineers to identify and address potential issues early in the development process. By using simulation tools, automakers can simulate various scenarios and conditions to assess the performance of different vehicle configurations, materials, and designs.

Testing is another essential aspect of the automotive simulation market. Once a prototype is developed, it undergoes rigorous testing to ensure its safety, reliability, and compliance with regulatory standards. Simulation plays a vital role in this phase by enabling engineers to conduct virtual tests under simulated real-world conditions. This includes evaluating the vehicle's performance in different environments, such as extreme temperatures, road conditions, and traffic scenarios. By simulating these conditions, automakers can identify potential weaknesses and make necessary improvements to enhance the vehicle's overall performance and safety.

The automotive simulation market continues to evolve with advancements in technology. The increasing complexity of vehicles, coupled with the demand for more efficient and safer transportation solutions, is driving the adoption of simulation tools across the automotive industry. Moreover, the integration of technologies such as artificial intelligence and machine learning is further enhancing the capabilities of automotive simulation software, enabling more accurate predictions and simulations of real-world scenarios.

In addition to prototyping and testing, automotive simulation also finds applications in other areas such as training, research, and development. Virtual simulations are increasingly being used for training purposes, allowing automotive engineers and technicians to familiarize themselves with new technologies and procedures in a safe and controlled environment. Furthermore, simulation tools are instrumental in supporting research and development efforts, enabling researchers to explore new ideas and concepts without the need for expensive physical prototypes.

Overall, the automotive simulation market plays a critical role in driving innovation and advancement in the automotive industry. By enabling virtual prototyping, testing, and training, simulation tools help automakers design safer, more efficient, and technologically advanced vehicles that meet the evolving needs of consumers and regulatory requirements. As technology continues to evolve, the automotive simulation market is expected to witness further growth and expansion, shaping the future of transportation.

By End Market

In the vast landscape of the global automotive industry, simulation plays a crucial role in shaping its trajectory. It's a tool that aids in understanding, testing, and refining various aspects of automotive technology and design before they hit the roads. This technology isn't limited to a single sector but extends its reach across multiple dimensions within the industry.

The automotive simulation market is segmented based on its end users, namely Original Equipment Manufacturers (OEMs), Automotive Component Manufacturers, and Regulatory Bodies. Each segment holds its own significance in driving the adoption and advancement of simulation technologies.

OEMs, being the cornerstone of vehicle production, heavily rely on simulation to streamline their design and testing processes. In 2020, the OEMs segment accounted for a substantial value of 998.3 USD Million within the global automotive simulation market. This indicates the substantial investment and reliance placed by manufacturers on simulation technologies to enhance efficiency and ensure product quality.

The Automotive Component Manufacturers segment stands as another key player in this landscape. These manufacturers supply essential components and systems to OEMs, contributing significantly to the overall automotive ecosystem. In 2020, this segment held a value of 462 USD Million within the automotive simulation market. Their utilization of simulation technologies is pivotal in ensuring the compatibility, functionality, and performance of their products within the broader automotive context.

Regulatory Bodies play a critical role in ensuring compliance, safety, and standardization within the automotive industry. They set guidelines and standards that manufacturers must adhere to, ensuring the safety and reliability of vehicles. The Regulatory Bodies segment, valued at 225.7 USD Million in 2020, underscores the importance of simulation in validating and certifying automotive technologies and systems to meet regulatory requirements.

These segments collectively underscore the diverse applications and significance of simulation technologies across various facets of the automotive industry. From design optimization and performance testing to regulatory compliance and component validation, simulation serves as a cornerstone in driving innovation and efficiency throughout the automotive value chain.

Looking ahead, the automotive simulation market is poised for further growth and innovation as emerging technologies like artificial intelligence, machine learning, and virtual reality continue to augment its capabilities. With ongoing advancements and increasing demand for more efficient and sustainable automotive solutions, simulation will undoubtedly remain a key enabler in shaping the future of mobility.

REGIONAL ANALYSIS

The global Automotive Simulation market can be analyzed regionally to gain insights into its various segments and trends. Geographically, the market is segmented worldwide.

Starting with North America holds a significant portion of the global Automotive Simulation market. In 2020, it was estimated to be valued at 505.0 USD Million. This region boasts a robust automotive industry, driven by technological advancements and a strong consumer demand for vehicles. The market here is dynamic, with continuous innovation and adoption of simulation technologies to enhance product development and testing processes. With key players investing in research and development, the North American market is expected to maintain its growth trajectory in the coming years.

Moving on to Europe, this region has a mature and stable Automotive Simulation market. In recent years, it has shown steady development, with a market value of 499.8 USD Million in 2020. The automotive sector in Europe is characterized by a rich history of innovation and a well-established manufacturing infrastructure. Manufacturers here emphasize quality, safety, and sustainability, driving the demand for simulation solutions to optimize design, performance, and efficiency of vehicles. Despite facing challenges such as regulatory changes and economic fluctuations, the European market continues to evolve, propelled by advancements in simulation technology and collaborations between industry stakeholders.

Both North America and Europe play pivotal roles in shaping the global Automotive Simulation market. While North America leads in terms of market size and technological innovation, Europe contributes with its legacy of automotive excellence and emphasis on quality and sustainability. These regions serve as key hubs for research, development, and manufacturing, attracting investments and talent from across the globe.

Moreover, the regional analysis highlights the diverse dynamics within the Automotive Simulation market. Each region has its unique market drivers, challenges, and opportunities influenced by factors such as economic conditions, regulatory frameworks, and consumer preferences. Understanding these regional nuances is essential for businesses to formulate effective strategies and capitalize on emerging trends in the automotive simulation landscape.

The regional analysis offers valuable insights into the global Automotive Simulation market, shedding light on its geographical distribution, market dynamics, and growth prospects. While North America and Europe lead the pack, other regions also contribute to the market's growth, presenting opportunities for industry players to expand their footprint and cater to diverse customer needs.

COMPETITIVE PLAYERS

The global automotive simulation market boasts several key players contributing to its growth and innovation. These companies play a crucial role in driving advancements and shaping the landscape of automotive simulation technology.

Among the prominent competitors in this arena are Altair Engineering, Ansys, PTC, Siemens, Autodesk, Dassault Systemes, Synopsys, Mathworks, ESI Group, Aras, COMSOL AB, SimScale GmbH, MOOG INC., dSPACE GmbH, PG Automotive GmbH, TESIS GmbH, AVL List GmbH, IPG Automotive GmbH, and Cosine Simulation.

These companies bring diverse expertise and solutions to the table, ranging from simulation software to hardware and consultancy services. Altair Engineering, for instance, specializes in providing simulation-driven innovation to optimize design, processes, and decision-making across various industries, including automotive.

Ansys is another key player known for its simulation software offerings, empowering engineers and designers to simulate real-world performance and behavior of products before they are built. PTC, on the other hand, focuses on providing technology solutions to transform how products are created and serviced, offering simulation capabilities as part of its comprehensive portfolio.

Siemens, a global powerhouse in industrial digitalization, offers a wide range of simulation software and services tailored to the automotive sector. Its solutions cover areas such as vehicle electrification, autonomous driving, and digital twin development.

Autodesk, renowned for its expertise in 3D design, engineering, and entertainment software, offers simulation tools that enable automotive manufacturers to optimize designs, improve performance, and accelerate innovation.

Dassault Systemes is a leader in 3D design, simulation, and product lifecycle management software, catering to the automotive industry's needs for virtual testing and validation.

Synopsys specializes in electronic design automation software and services, contributing to the development of advanced automotive electronics through simulation and verification solutions.

Mathworks provides MATLAB and Simulink software widely used for modeling, simulation, and control system design in the automotive domain, facilitating the development of embedded software and electronic systems.

ESI Group offers virtual prototyping software and services, helping automotive manufacturers simulate and optimize manufacturing processes and product performance. Aras focuses on providing resilient platform solutions for digital industrial applications, including automotive simulation and product lifecycle management.

These companies, along with others in the automotive simulation market, continuously innovate and collaborate with industry stakeholders to address evolving challenges and drive the future of mobility. Their contributions are instrumental in advancing vehicle design, safety, efficiency, and sustainability in an ever-changing automotive landscape.

Automotive Simulation Market Key Segments:

By Deployment

- On-premises

- Cloud

By Component

- Software

- Services

By Application

- Prototyping

- Testing

By End Market

- OEMS

- Automotive Component Manufacturers

- Regulatory Bodies

Key Global Automotive Simulation Industry Players

- Altair Engineering

- Ansys

- PTC

- Siemens

- Autodesk

- Dassault Systemes

- Synopsys

- Mathworks

- ESI Group

- Aras

- COMSOL AB

- SimScale GmbH

- MOOG INC.

- dSPACE GmbH

- PG Automotive GmbH

WHAT REPORT PROVIDES

- Full in-depth analysis of the parent Industry

- Important changes in market and its dynamics

- Segmentation details of the market

- Former, on-going, and projected market analysis in terms of volume and value

- Assessment of niche industry developments

- Market share analysis

- Key strategies of major players

- Emerging segments and regional growth potential

US: +1 3023308252

US: +1 3023308252