Agricultural Robotics Market Size, Share, By Product Type (Driverless Tractors, Unmanned Aerial Vehicles, Milking Robots, Autonomous Field Robots, and Others), By Farming Environment (Indoor and Outdoor), By Farm Size (Small-Sized Farms, Mid-Sized Farms, and Large-Sized Farms), By Application (Planting, Seeding Management, Spraying Management, Milking, Monitoring, Surveillance, Harvest Management, Livestock Monitoring, and Others), Industry Analysis, Growth, Trends, and Forecast, 2026-2033

Report ID

MSI-4677

Published

April 28, 2026

Pages

317 Pages

Format

Report Details

Comprehensive Market Analysis And Insights

Market Overview

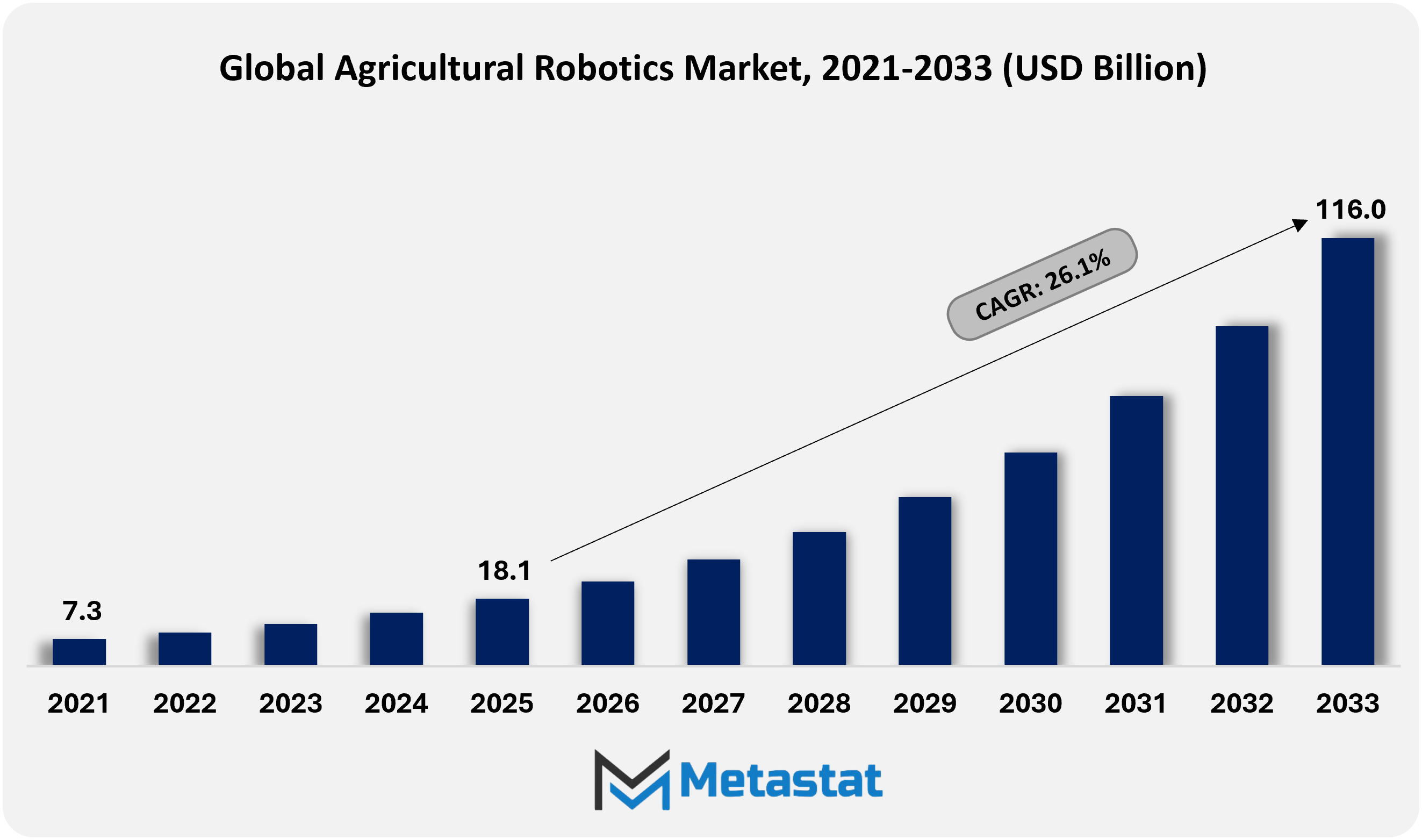

The Global Agricultural Robotics market size was valued at USD 18.1 billion in 2025 and projected to grow at a CAGR of 26.1% during the forecast period, reaching USD 116 billion by 2033.

Global Agricultural Robotics Market: Comprehensive Data-Driven Market Analysis and Strategic Outlook

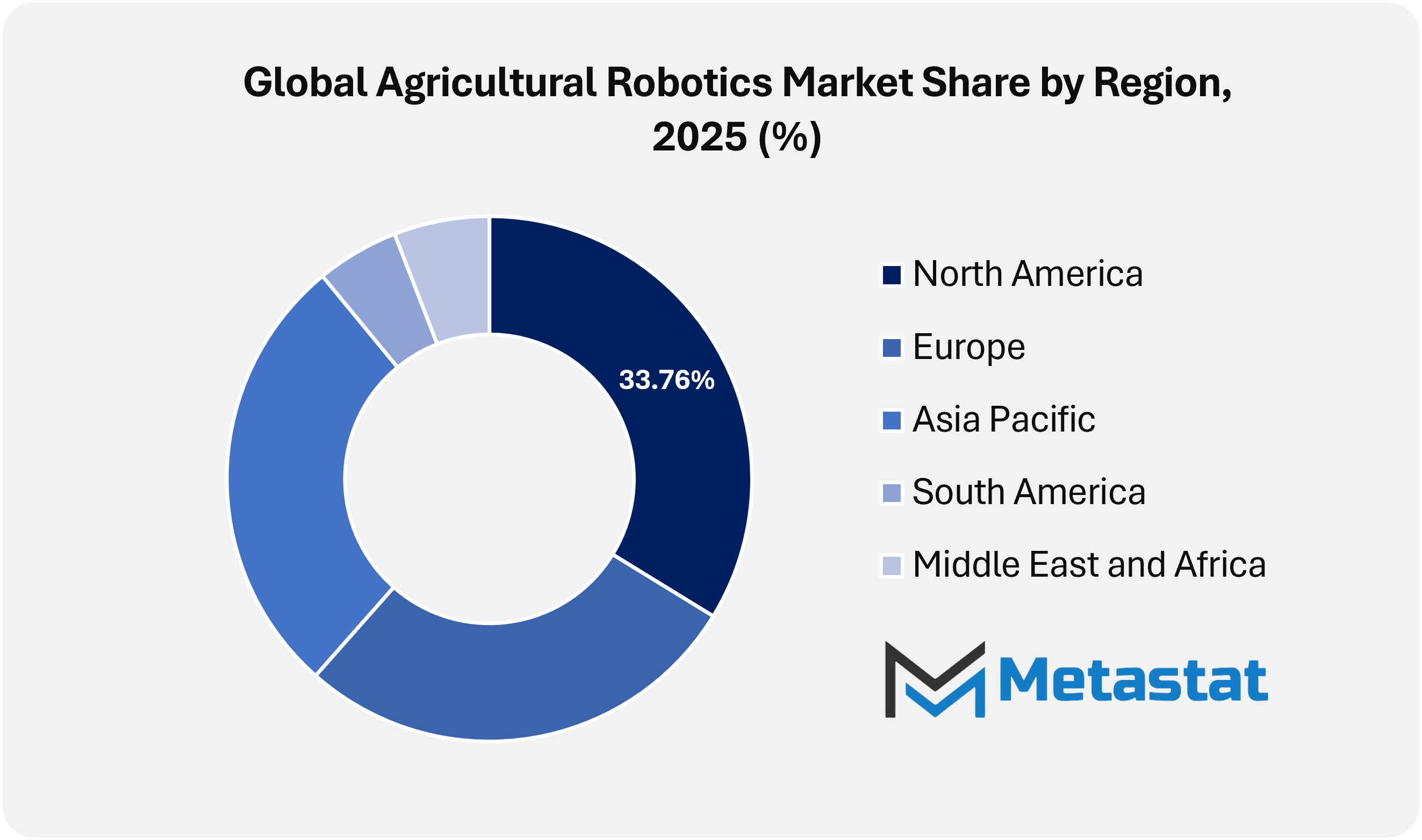

North America held 33.8% of the global market in 2025, with the U.S. leading the regional market.

Driverless Tractors segment accounted for a market share of 22.5% in 2025.

Key trends driving growth include increasing labor shortages and rising labor costs in agriculture, along with growing adoption of precision farming practices and AI/IoT-integrated technologies to optimize inputs, improve yields, and reduce environmental impact.

Opportunities include expansion of smart farming initiatives and investments in AIdriven agricultural solutions present significant growth potential, especially in regions investing in sustainable agriculture and digital infrastructure.

The Global Agricultural Robotics market is set to become a core part of modern farm operations, positioned at the convergence of automation, precision agriculture, and digital farm management. As farming systems become increasingly data-led, robotic technologies are moving beyond pilot-stage deployment into structured integration across large-scale commercial agriculture. Autonomous tractors, robotic harvesters, and AI-enabled crop monitoring systems are being designed to operate as part of connected farm ecosystems rather than as standalone machines. This transition is steadily repositioning agricultural robotics from an emerging innovation area into a strategic capital investment category across global farming operations.

Investment activity across the Agricultural Robotics market is increasingly favoring modular robotic platforms that support software upgrades, fleet coordination, and integration with broader digital agriculture systems. Agricultural enterprises are adopting interoperable solutions that connect with satellite imagery, soil intelligence platforms, and farm management dashboards to improve operational visibility and decision-making. Competitive activity is also expanding beyond machinery manufacturing, with partnerships emerging among robotics developers, agronomy specialists, and cloud technology providers. As a result, business models are evolving toward combined hardware, analytics, and service offerings, including robotics-as-a-service arrangements with performance-based maintenance and seasonal support structures.

Market Dynamics

Growth Drivers:

Increasing labor shortages and rising labor costs in agriculture, driving demand for automation to maintain productivity and profitability.

Labor shortages and rising wage pressure across agricultural economies are becoming major operational concerns for growers, particularly during planting, harvesting, and crop maintenance periods. An aging farm workforce and continued migration toward urban employment are reducing labor availability, placing pressure on farm productivity and cost structures. In response, automated harvesters, robotic planters, and autonomous tractors are being adopted to maintain workflow continuity and reduce dependence on manual labor. These technologies are improving operational consistency while supporting long-term cost efficiency across a wide range of farming systems.

Growing adoption of precision farming practices and integration of AI/IoT technologies to optimize inputs, improve yields, and reduce environmental impact.

Precision agriculture is becoming a key foundation for robotics adoption across the Global Agricultural Robotics market. AI-enabled sensors, crop monitoring drones, automated irrigation systems, and soil analytics platforms are helping farmers improve decision-making across planting, input management, and harvesting cycles. Robotics integrated with AI and IoT frameworks allows more accurate application of fertilizers, pesticides, and water, improving productivity while reducing waste and environmental burden. This combination of precision farming and automation is strengthening the commercial case for agricultural robotics across both developed and emerging farming markets.

Restraints and Challenges:

High upfront capital costs for robotic systems and infrastructure make adoption difficult for small and mid‑sized farms.

High upfront investment remains a major barrier to wider adoption of agricultural robotics, particularly among small and medium-sized farms. The cost of robotic equipment, supporting infrastructure, software integration, and ongoing maintenance can create a substantial financial burden for operators with limited capital flexibility. Longer payback periods can delay purchasing decisions, especially in price-sensitive agricultural markets. Broader adoption will depend on the expansion of financing models, leasing options, and service-based delivery structures that reduce initial capital requirements.

Limited rural connectivity and technical expertise in many agricultural regions restrict effective deployment and maintenance of robotics systems.

Limited rural connectivity and gaps in technical expertise continue to restrict the effective deployment of agricultural robotics in several regions. Reliable broadband infrastructure is essential for remote monitoring, cloud-based analytics, predictive maintenance, and real-time equipment coordination. In many agricultural zones digital infrastructure remains underdeveloped, constraining the performance of connected robotic systems. At the same time, shortages of trained personnel for calibration, system monitoring, and troubleshooting reduce operational efficiency, making training programs and rural digital expansion critical for long-term market growth.

Opportunities:

Expansion of smart farming initiatives and investments in AI‑driven agricultural solutions present significant growth potential, especially in regions investing in sustainable agriculture and digital infrastructure.

Expanding smart farming initiatives and rising investment in AI-driven agricultural technologies are creating strong growth opportunities for the Global Agricultural Robotics market. Public and private investment aimed at digital agriculture, climate-resilient cultivation, and resource-efficient farming is accelerating interest in robotic systems across multiple crop and livestock environments. Regions prioritizing sustainable agriculture and rural technology modernization will present favorable conditions for large-scale deployment. These trends will strengthen opportunities for product innovation, collaborative research, and long-term commercialization across agricultural robotics platforms.

Market Segmentation Analysis

The Global Agricultural Robotics market is classified based on Product Type, Farming Environment, Farm Size, and Application.

By Product Type, the market is further segmented into:

Driverless Tractors

Driverless Tractors segment is estimated at USD 5.1 billion in 2026 and is projected to reach USD 23.7 billion by 2033, at a CAGR of 24.4% during the forecast period.

Driverless tractors represent one of the most commercially important categories within the Global Agricultural Robotics market, supporting autonomous navigation, route optimization, and precision field operations. These systems are increasingly integrated with satellite guidance, sensor fusion, and connected farm management platforms to improve accuracy across soil preparation, planting, and cultivation activities. Their ability to reduce labor dependency while improving operating efficiency is strengthening adoption across large-scale farming operations.

Unmanned Aerial Vehicles/Drones segment is estimated at USD 6.7 billion in 2026 and is projected to reach USD 40.8 billion by 2033, at a CAGR of 29.5% during the forecast period.

Unmanned aerial vehicles and drones are strengthening their position in the Global Agricultural Robotics market through applications in crop monitoring, field imaging, input assessment, and targeted spraying. These systems provide high-resolution visibility into crop health, irrigation stress, nutrient distribution, and pest activity, enabling faster and more precise field interventions. Integration with AI-based analytics is expanding their value beyond imaging into predictive farm intelligence.

Milking Robots

Milking Robots segment is estimated at USD 4.1 billion in 2026 and is projected to reach USD 14.3 billion by 2033, at a CAGR of 19.5% during the forecast period.

Milking robots continue to play a vital role in the dairy-focused segment of the Global Agricultural Robotics market by improving automation, herd monitoring, and operational consistency. These systems are designed to support hygienic milking procedures, track output levels, and capture animal health data with minimal manual intervention. Their use helps dairy operators improve labor efficiency, maintain routine milking schedules, and enhance herd management decisions through continuous data collection.

Autonomous Field Robots

Autonomous Field Robots segment is estimated at USD 5.8 billion in 2026 and is projected to reach USD 32.6 billion by 2033, at a CAGR of 27.9% during the forecast period.

Autonomous field robots are emerging as an important innovation area within the Global Agricultural Robotics market, particularly for precision tasks such as weeding, thinning, scouting, and micro-spraying. These systems operate close to the crop line and use machine vision, sensors, and AI-based decision models to perform targeted actions with high accuracy. Their ability to reduce chemical use, lower soil disturbance, and improve crop-level intervention supports their relevance in sustainable farming systems.

Others

Others segment is estimated at USD 1.1 billion in 2026 and is projected to reach USD 4.4 billion by 2033, at a CAGR of 22.4% during the forecast period.

The Others category includes robotic systems used in irrigation control, sorting, grading, packing, and other auxiliary agricultural operations. This segment reflects the broadening use of automation beyond core field and dairy functions into post-harvest and support processes. Growth in this area is being supported by demand for modular and crop-specific solutions, particularly across specialty farming and controlled-environment agriculture.

By Farming Environment, the market is divided into:

Indoor

Indoor segment is projected to reach USD 28 billion by 2033, at a CAGR of 29.7% during the forecast period.

Indoor farming environments are expected to increase their use of robotics for climate control, nutrient management, crop inspection, and automated harvesting. Controlled-environment agriculture offers a favorable setting for robotics deployment owing to predictable layouts, stable conditions, and high-value crop production. Robotic arms, mobile units, and AI-based monitoring systems are helping operators improve consistency, reduce labor intensity, and optimize growing conditions.

Outdoor

Outdoor segment is projected to reach USD 87.9 billion by 2033, at a CAGR of 25.1% during the forecast period.

Outdoor farming environments represent the largest operational landscape for the Global Agricultural Robotics market, supported by demand for automation across broad-acre and specialty crop farming. These environments require robotics systems capable of handling variable terrain, changing weather conditions, and large-area field coverage. Autonomous tractors, drones, field robots, and remote monitoring systems are being developed to improve productivity, reduce labor pressure, and support precision farm execution at scale.

By Farm Size, the market is further divided into:

Small-Sized Farms

Small-Sized Farms segment is projected to reach USD 22 billion by 2033.

Small-sized farms are expected to adopt agricultural robotics through compact, flexible, and service-based solutions designed to reduce upfront investment pressure. Adoption in this category is likely to be supported by shared equipment models, subscription-based platforms, and simplified robotic systems suited to limited acreage. These technologies can help improve yield quality, reduce labor dependency, and support farm modernization without requiring full-scale automation investment.

Mid-Sized Farms

Mid-Sized Farms segment is projected to reach USD 43.2 billion by 2033.

Mid-sized farms are expected to represent an important demand base for agricultural robotics as operators seek to balance productivity targets with labor availability and operating efficiency. These farms are increasingly evaluating semi-autonomous and fully automated solutions that can improve planting, crop care, and field monitoring without the complexity of large enterprise deployments.

Large-Sized Farms

Large-Sized Farms segment is projected to reach USD 50.8 billion by 2033.

Large-sized farms are expected to remain the primary adopters of advanced robotics systems owing to their greater capital capacity, scale advantages, and need for operational coordination across extensive cultivation areas. In the Global Agricultural Robotics market, these farms are deploying connected fleets of tractors, drones, harvesters, and monitoring systems linked through centralized control platforms. Robotics is enabling improved labor efficiency, better resource allocation, and stronger visibility across large-scale agricultural operations.

By Application, the Global Agricultural Robotics market is divided as:

Planting & Seeding Management

Planting & Seeding Management segment is projected to grow at a CAGR of 23.7% during the forecast period.

Planting and seeding management are increasingly benefiting from robotics systems designed to improve seed placement accuracy, planting depth control, and row spacing consistency. Automated planting solutions are supporting better germination outcomes and more efficient use of seed inputs across varying soil conditions. Integration with field data and precision agriculture tools is also improving calibration and crop planning decisions. These capabilities are strengthening the role of robotics in early-stage crop establishment.

Spraying Management

Spraying Management segment is projected to grow at a CAGR of 27.4% during the forecast period.

Spraying management is becoming a major application area within the Global Agricultural Robotics market as growers seek greater precision in fertilizer, pesticide, and crop protection input delivery. Robotic sprayers and drone-based application systems can target specific crop zones based on sensor readings and field intelligence, helping reduce overuse and improve input efficiency. This precision supports both cost control and environmental compliance across modern farming systems.

Milking

Milking segment is projected to grow at a CAGR of 20% during the forecast period.

Milking remains a key application area in the Global Agricultural Robotics market, within commercial dairy operations focused on productivity, hygiene, and herd-level monitoring. Robotic milking systems help standardize milking routines, reduce manual labor requirements, and improve the capture of production and animal health data. These systems also support better operational continuity and more consistent dairy output.

Monitoring & Surveillance

Monitoring & Surveillance segment is projected to grow at a CAGR of 29.8% during the forecast period.

Monitoring and surveillance applications are gaining strong importance in the Global Agricultural Robotics market through the use of drones, ground robots, and sensor-enabled systems for real-time crop and field observation. These solutions help identify disease risk, irrigation imbalance, nutrient deficiency, pest activity, and soil stress at earlier stages. Continuous data collection and analytics support faster decisions and reduce the likelihood of productivity loss across the crop cycle.

Harvest Management

Harvest Management segment is projected to grow at a CAGR of 27.3% during the forecast period.

Harvest management is expected to witness strong development within the Global Agricultural Robotics market as labor shortages and quality control requirements increase across high-value crop segments. Robotic harvesting systems equipped with machine vision and maturity analysis tools can improve picking accuracy, reduce crop damage, and enhance harvesting efficiency. These systems are particularly relevant in applications where timing, consistency, and post-harvest quality are commercially critical.

Livestock Monitoring

Livestock Monitoring segment is projected to grow at a CAGR of 28.6% during the forecast period.

Livestock monitoring is becoming an increasingly important application within the Global Agricultural Robotics market through the use of robotic systems, wearable sensors, and automated observation tools. These technologies support real-time tracking of animal health, feeding behavior, movement patterns, and reproductive indicators, helping operators improve herd management and reduce disease risk. Data-driven monitoring also supports more efficient decision-making across livestock operations.

Others

Others segment is projected to grow at a CAGR of 24.1% during the forecast period.

The Others application segment includes robotics used in grading, storage management, irrigation scheduling, and additional support functions across agricultural operations. The broadening role of automation across both pre-harvest and post-harvest workflows. Integrated robotics solutions are helping farms improve operational transparency, coordinate resource use, and strengthen process efficiency across the wider agricultural system.

By Region:

Based on geography, the Global Agricultural Robotics market is divided into North America, Europe, Asia-Pacific, South America, Middle East, and Africa.

North America Agricultural Robotics Market is set to expand at a CAGR of 26.1% within the forecast period, reaching a market size (TAM) of USD 36.8 billion by the end of 2033.

North America, High adoption of precision farming technologies across the U.S. And Canada is accelerating demand for superior agricultural robotics solutions.

North America, Strong funding from agritech companies and supportive federal innovation packages are strengthening large-scale deployment of independent farm device.

Europe represents a technologically advanced market for agricultural robotics, supported by strong focus on precision farming, sustainable agriculture, and labor-efficient farm operations.

Asia Pacific, Rapid farm mechanization throughout China, India, and Japan provides full-size growth possibilities for cost-efficient and AI-integrated agricultural robotics structures.

Asia Pacific, Rising hard work shortages in rural economies are developing favorable conditions for robotics vendors concentrated on horticulture and specialty crop segments.

Across the Middle East, Africa, and South America, agricultural robotics adoption is gaining sluggish momentum via modernization initiatives, increasing industrial farming operations, and increasing awareness on food security resilience.

Competitive Landscape and Strategic Insights

The Global Agricultural Robotics market is attracting strong commercial interest as farms seek practical solutions to improve productivity, manage rising labor pressure, and increase operating efficiency. Agricultural robotics is moving from experimental use into regular farm activity across crop production, dairy operations, and field monitoring. Technologies such as autonomous tractors, robotic harvesters, drones, and milking systems are helping reduce repetitive manual work while improving precision and operational consistency. The market is also being shaped by demand for better field intelligence, real-time monitoring, and measurable return on investment across increasingly data-driven farm environments.

Leading participants in the Global Agricultural Robotics market include Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, Yanmar Holdings Co., Ltd., CLAAS KGaA mbH, and Sentera, Inc. These companies are strengthening their automation capabilities through the integration of smart guidance systems, AI-enabled tools, and precision farming technologies across tractors, harvesters, and aerial monitoring platforms. Many companies are also expanding their portfolios to address the needs of small and mid-sized farms through compact and scalable robotic equipment. This broadening product strategy is supporting stronger competitive positioning across developed and emerging agricultural markets.

Technology-focused companies are shaping the competitive structure of the market by developing specialized robotics platforms for crop care, monitoring, and livestock operations. Companies such as Topcon Corporation, Hexagon AB, Odd.Bot B.V., Lely Holding S.à r.l., DeLaval Holding AB, GEA Group Aktiengesellschaft, BouMatic LLC, Fullwood JOZ B.V., FJDynamics Co., Ltd., SwarmFarm Robotics Pty Ltd, and Naio Technologies SAS are expanding innovation across field robotics, positioning systems, dairy automation, and precision farm analytics. Their presence reflects the increasing role of specialized solutions in improving crop-level efficiency and data-led farm execution.

The competitive landscape reflects a mix of established agricultural machinery companies and agile robotics innovators working toward more efficient, sustainable, and data-driven farming models. Large manufacturers are embedding robotics into existing equipment portfolios, while smaller players are focused on targeted solutions for specific crops, tasks, and farm sizes. Strategic partnerships, acquisitions, and technology collaborations are expected to remain central to market expansion. As adoption increases, agricultural robotics is likely to transition further from pilot deployment into mainstream use across modern farming systems.

Forecast and Future Outlook

Market size is forecast to rise from USD 18.1 billion in 2025 to over USD 116 billion by 2033.

Regional deployment strategies are expected to vary according to labor costs, farm structures, digital infrastructure, and regulatory maturity. High-labor-cost markets are likely to accelerate adoption of full-field automation, while emerging agricultural economies may prioritize semi-autonomous and cost-optimized robotic systems. Regulatory frameworks related to equipment safety, autonomous operation, and agricultural data management are also expected to gain importance, influencing product development and compliance investment. Over time, agricultural robotics is expected to become an integrated operational layer within commercial farming, supporting more scalable, efficient, and technology-driven agricultural production worldwide.

This research report categorizes the Agricultural Robotics market based on key segments and regions, forecasts revenue growth, and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Agricultural Robotics market. Recent market developments and competitive strategies such as expansion, product launch, partnership, merger, and acquisition have been included to draw the competitive landscape in the market.

The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Agricultural Robotics market.

Report Attributes

Details

Study Period

2021-2033

Base Year

2025

Estimated Year

2026

Forecast Period

2026-2033

Historical Period

2021-2025

Growth Rate

CAGR 26.1% from 2026 to 2033

Revenue Unit

USD billion

Sales Volume Unit

Thousand Units

Segmentation

By Product Type, Farming Environment, Farm Size, Application, and Region

By Region

North America (By Product Type, Farming Environment, Farm Size, Application, and Country)

United States

Canada

Mexico

Europe (By Product Type, Farming Environment, Farm Size, Application, and Country)

Germany

France

UK

Italy

Spain

Russia

Rest of Europe

Asia Pacific (By Product Type, Farming Environment, Farm Size, Application, and Country)

China

Japan

India

South Korea

Australia

Southeast Asia

Rest of Asia Pacific

South America (By Product Type, Farming Environment, Farm Size, Application, and Country)

Brazil

Argentina

Rest of South America

Middle East and Africa (By Product Type, Farming Environment, Farm Size, Application, and Country)

Saudi Arabia

UAE

South Africa

Rest of Middle East and Africa

WHAT REPORT PROVIDES

Mechanical Weeding Adoption and Field Automation Shift

AI-Driven Crop and Weed Recognition Advancements

Labor Reduction Through Autonomous Farming Systems

Robotics as an Enabler of Sustainable and Low-Input Agriculture

Key Company Market Share, Revenue, and Position/Ranking

Key Market Leaders

Full In-Depth Analysis of the Parent Industry

Industry Statistics

Important Changes in Market and Its Dynamics

Segmentation Details of the Market

Historical, On-Going, and Projected Market Analysis

Assessment of Niche Industry Developments

Market Share Analysis

Key Strategies of Major Players

Company Profiles of Key Players

Unique Selling Propositions of Leading Market Players

Thailand Vegetable Seeds market size is valued at USD 52.4 million in 2025 and is projected to reach USD 69.4 million in 2033, at a CAGR of 3.6% from 2026 to 2033

Vertical Farming market size is valued at USD 10 billion in 2025 and is projected to reach USD 41.1 billion in 2033, at a CAGR of 19.3% from 2026 to 2033.

Herbs Market Size, Share & Growth Analysis Report by 2032

Herbs Market is valued at USD 4.23 billion in 2025 and is expected to expand at a CAGR of 9.1% through 2032, with the potential to exceed USD 7.79 billion.