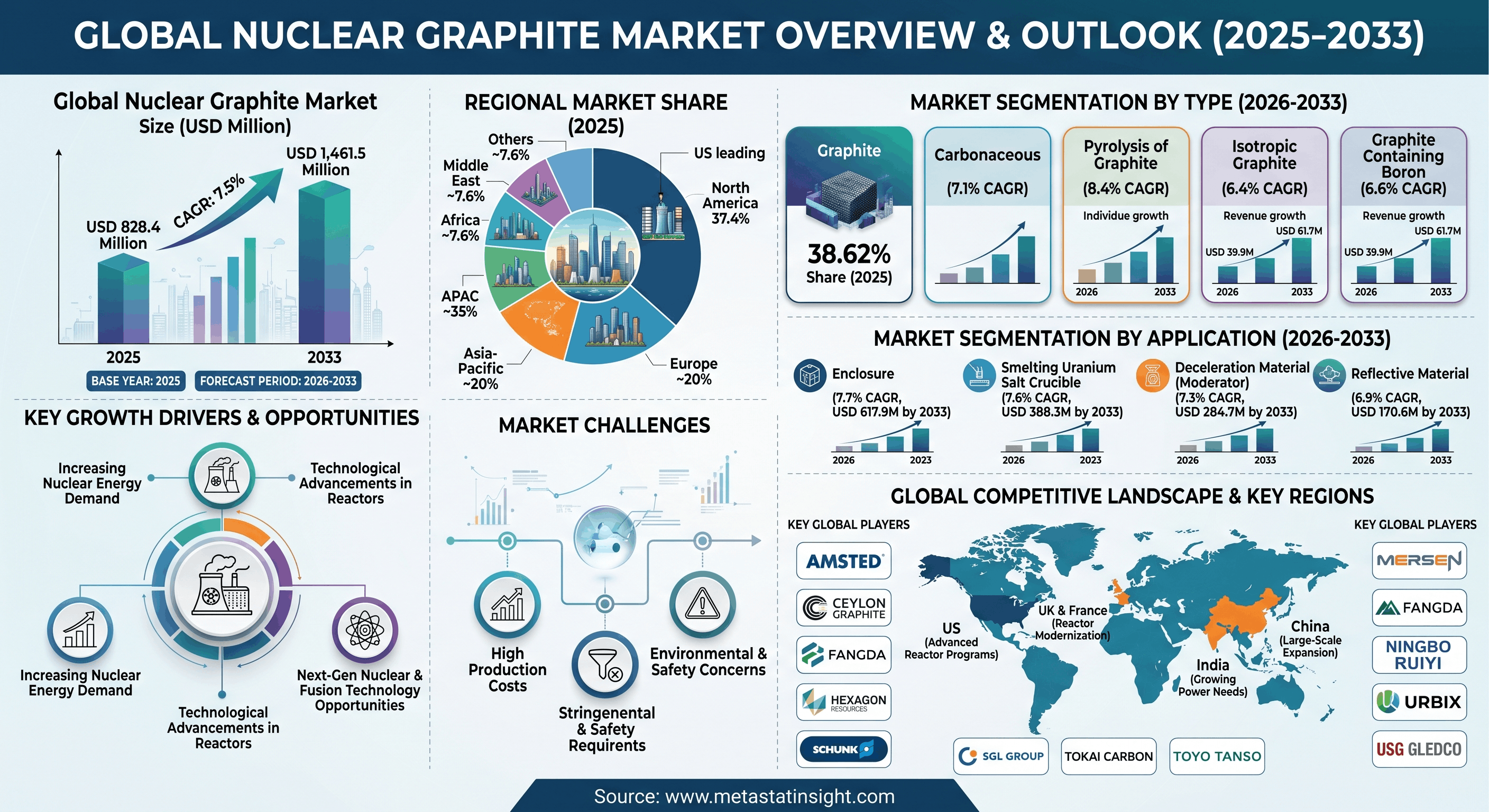

A comprehensive, data-driven market assessment published by MetaStat Insight reveals that the global nuclear graphite market is navigating a phase of robust growth. Valued at USD 828.4 million in 2025, the industry is positioned to experience a compound annual growth rate (CAGR) of 7.5% during the active forecast timeline, climbing steadily to achieve a valuation of USD 1,461.5 million by the year 2033. This upward trajectory is heavily supported by sweeping global transformations in power infrastructure, clean energy targets, and structural modernizations across aging facilities.

The evolving dynamics of low-carbon electricity generation are establishing ultra-high-purity nuclear-grade graphite as a fundamental core resource. As emerging and developed economies aggressively pivot away from fossil-fuel configurations to achieve carbon mitigation goals, the dependency on high-performance materials has intensified. The material’s distinct capacity to sustain absolute chemical stability, tolerate intense structural radiation exposure, and withstand elevated thermal thresholds makes it irreplaceable across high-temperature gas-cooled systems, molten salt frameworks, and evolutionary small modular reactors (SMRs).

Core Performance Metrics & Market Quantifications

-

North American Dominance: Accounts for a substantial 37.4% share of the global valuation in 2025, spearheaded by extensive structural implementation inside the United States.

-

Graphite Product Tier: Represents a definitive baseline share of 38.62% in 2025, with individual projections expanding from USD 339.9 million in 2026 to USD 562.9 million by 2033.

-

Pyrolysis Processing Acceleration: Set to display the fastest structural momentum among product categories, accelerating at an 8.4% CAGR to climb from USD 186.2 million in 2026 to USD 328.1 million by the conclusion of 2033.

-

Structural Enclosure Dominance: Leads individual application segments by volume and expenditure, tracking toward an evaluated valuation of USD 617.9 million by 2033 at a steady 7.7% CAGR.

Catalytic Growth Factors and Strategic Opportunities

The primary operational impetus is rooted in continuous advancements occurring within reactor technology. Precision engineering groups and specialized research entities are focusing heavily on reinforcing safe operating parameters. Refined graphite materials facilitate optimal neutron moderation properties, superior dimensional integrity, and extended product lifecycles. Consequently, these technical improvements encourage a broader implementation of advanced isotropic processing and boron-enhanced absorption materials across long-term utility planning grids.

Furthermore, upcoming horizons in fusion energy design and high-temperature gas reactors create lucrative, unexploited commercial openings. Large-scale structural development projects across prominent nations-notably China, India, and the United States-ensure sustained raw material consumption and create opportunities for key component manufacturers to integrate themselves into long-term nuclear supply agreements.

"Next-generation reactor technologies are fundamentally magnifying the strategic positioning of ultra-high-purity nuclear graphite. As international frameworks prioritize long-term grid security and zero-emission operations, industry partnerships between component processors and utility systems will serve as a cornerstone for supply chain resiliency."

Structural Restraints and Operations Friction

Despite the expanding operational horizon, the market experiences clear structural headwind factors. Strict purification standards mandate highly regulated processing environments, resulting in considerable production overhead costs and localized supply bottlenecks. The cost of complying with stringent nuclear qualification procedures and material certifications frequently impacts infrastructure construction timelines.

Additionally, public anxieties regarding waste processing management and rigorous environmental protocols imposed by global regulatory frameworks prolong infrastructure approval tracks, putting pressure on market scalability in select regions.

Competitive Alignment & Strategic Collaborations

The industrial landscape is marked by selective, quality-driven positioning where manufacturing participants prioritize material consistency, high-purity mining access, and precision machining layouts. Companies are increasingly deploying corporate capital toward international strategic alliances and plant capacity upgrades to maintain a robust foothold.

Entities highlighted as key operational forces within this structural dynamic include Amsted, Mersen (Mersen Graphite / Carbone Lorraine), Ceylon Graphite, Double Peaks Graphite Sealing Materials, FangDa, Hexagon Resources, Ningbo Ruiyi Sealing Material, Schunk, SGL Group (The Carbon Company), Tokai Carbon, Toyo Tanso Co. Ltd., Urbix, and USG Gledco.

About MetaStat Insight

About MetaStat Insight

MetaStat Insight is a premier global market research and strategic consulting firm specializing in high-fidelity industrial intelligence reports. Through meticulous, data-backed analytical methodologies, we empower corporate enterprises, government bodies, and institutional investors with actionable strategies, niche industry assessments, and definitive market dynamics essential for sustained competitive advantage.

-

Corporate Media Relations Site:

https://metastatinsight.com/ -

Inquiry Focus: Global Nuclear Graphite Market Analysis and Strategic Outlook (2026–2033)

-

Core Coverage: Advanced Materials, Clean Energy Infrastructure, and Chemical Engineering